ID : MRU_ 442429 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

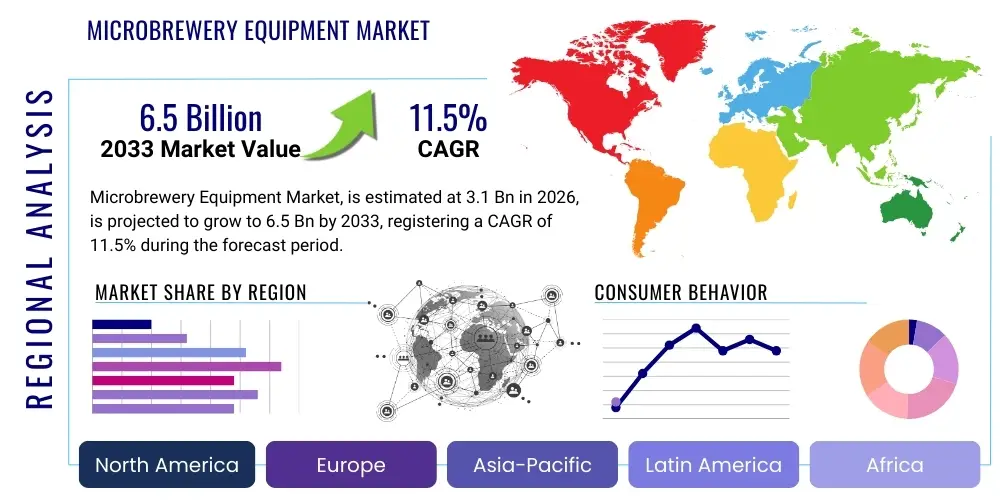

The Microbrewery Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 3.1 Billion in 2026 and is projected to reach USD 6.5 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for specialized and unique craft beers, necessitating advanced, scalable, and efficient brewing systems for smaller-scale operations. The continuous shift in consumer preferences towards locally sourced and artisanal beverages, particularly among millennial and Gen Z populations, provides a robust foundation for consistent investment in modern microbrewing infrastructure across mature and emerging economies.

The calculation of this market size encompasses revenues generated from the sale of essential machinery such as fermenters, mash tuns, lauter tuns, boil kettles, bright tanks, control systems, and associated ancillary equipment used in microbreweries and brewpubs. Factors influencing the rapid market valuation increase include technological advancements in automation, which improve batch consistency and reduce labor costs, along with increasing customization options available from equipment manufacturers. Furthermore, supportive regulatory environments in key regions, which facilitate the establishment of small breweries, contribute significantly to market expansion, making the equipment purchase a primary capital expenditure for thousands of new entrants globally.

The Microbrewery Equipment Market comprises the manufacturing, distribution, and sale of machinery and systems specifically designed for producing beer in smaller quantities, typically ranging from 3 barrels (BBL) to 30 BBL systems. This specialized equipment caters primarily to microbreweries, brewpubs, taprooms, and smaller regional craft breweries that emphasize quality, experimentation, and local appeal over mass production volume. Key components include brewing vessels (like mash tuns and kettles), fermentation tanks, cooling systems, cleaning mechanisms (CIP systems), filtration units, and sophisticated control panels that manage temperature and process parameters. Major applications of this equipment involve the production of diverse craft beer styles, including IPAs, stouts, lagers, and experimental seasonal brews, serving a discerning consumer base seeking authenticity and variety in their alcoholic beverages. The primary benefits of modern microbrewery equipment include enhanced brewing efficiency, superior quality control, reduced utility consumption through optimized design, and the flexibility to rapidly switch between different product recipes. Driving factors fueling this market growth include the explosive popularity of the craft beer movement globally, increased disposable income in urban centers allowing for premium beverage consumption, favorable taxation policies for small-scale alcohol producers in many jurisdictions, and continuous technological innovation focusing on modular and space-saving equipment designs, thereby lowering the barrier to entry for aspiring brewers.

The global Microbrewery Equipment Market is poised for substantial growth, driven by dynamic shifts in consumer preferences favoring localized, high-quality craft beer over standardized commercial brands. Major business trends indicate a strong focus on modular and highly automated brewing systems that allow microbreweries to maximize throughput in limited physical footprints while maintaining stringent quality consistency. Equipment manufacturers are increasingly offering end-to-end solutions, from design consultation to installation and post-sales technical support, strengthening vendor-client relationships and ensuring system scalability. Regional trends highlight North America and Europe as mature markets characterized by replacement demand and upgrades to higher-capacity or more efficient systems, whereas the Asia Pacific region, particularly China and India, represents the fastest-growing opportunity due to nascent but rapidly expanding local craft beer scenes and a rising middle class adopting Western consumption patterns. Segment trends show that fermentation tanks and ancillary equipment, such as sophisticated yeast management systems and specialized filtration units, are experiencing particularly high demand, reflecting brewers' focus on ingredient optimization and complex flavor profiles. Furthermore, the 10 BBL to 20 BBL capacity range dominates the market, catering to successful microbreweries seeking to transition from hobbyist volumes to regional distribution, effectively balancing capital outlay with production scalability and market reach.

User queries regarding AI in the Microbrewery Equipment Market center primarily on process optimization, predictive maintenance, and recipe development accuracy. Key concerns revolve around the potential for AI-driven systems to standardize the craft process, potentially undermining the artisanal nature cherished by consumers, versus the efficiency gains necessary for business viability. Users frequently ask how AI can stabilize fermentation without human intervention, whether predictive analytics can truly forecast equipment failure in complex brewing environments, and how machine learning algorithms aid in scaling up successful small-batch recipes accurately. The consensus view derived from this analysis is that AI's primary influence will be operational: enabling precise control over mash temperatures, optimizing fermentation curves based on real-time data from internal sensors (pH, gravity, temperature), and enhancing cleaning-in-place (CIP) efficiency by calculating optimal chemical concentrations and contact times. This technological integration aims to reduce human error, minimize batch variation, and lower utility costs, thereby making microbrewery operations significantly more efficient and sustainable without diminishing the crucial creative input of the brewmaster, who will utilize AI as an advanced decision-support tool.

The Microbrewery Equipment Market is dynamically shaped by a crucial interplay of Drivers, Restraints, and Opportunities (DRO), which collectively form the Impact Forces dictating market trajectory and investment decisions. A primary Driver is the unrelenting growth in craft beer consumption globally, fueled by consumer demand for premium, localized, and unique beverage experiences, compelling new entrepreneurs to invest in specialized brewing infrastructure. This is strongly supported by the increasing acceptance of brewpubs as social hubs, driving localized demand for equipment tailored to food service integration. Conversely, the market faces significant Restraints, most notably the extremely high initial capital investment required for establishing a fully operational microbrewery, including specialized machinery, complex piping, and facility build-out, which often acts as a significant barrier to entry for smaller enterprises. Furthermore, stringent and often complex regulatory hurdles pertaining to alcohol production, licensing, and distribution vary widely by region, imposing administrative and compliance costs that slow market penetration, particularly in emerging economies.

Opportunities within the sector are vast, stemming primarily from the potential for equipment modularity and automation. Advances in compact, skid-mounted systems appeal to urban microbreweries with limited space, while digitalization and automation technologies offer a clear path toward greater efficiency and reduced labor dependency. The growing global focus on sustainable brewing practices presents a unique opportunity for manufacturers specializing in energy-efficient heat recovery systems, water conservation technology, and low-utility fermentation vessels. These impact forces—high consumer demand driving investment (Driver) coupled with high upfront costs (Restraint) and the potential for technological innovation (Opportunity)—create a highly competitive yet promising landscape where success hinges on efficient capital deployment, adherence to high-quality standards, and leveraging automation to overcome labor challenges.

The Microbrewery Equipment Market is strategically segmented based on factors such as equipment type, capacity, material, and automation level, reflecting the diverse needs of small-scale brewers worldwide. Understanding these segments is crucial for manufacturers to tailor their product offerings and for investors to identify high-growth niches. Segmentation by equipment type, for instance, helps categorize core functional areas, with fermentation tanks and chilling systems often representing the largest revenue streams due to their necessity in every batch cycle and their critical role in quality preservation. Capacity-based segmentation, ranging from pilot systems to larger 30 BBL setups, differentiates between small brewpubs focused solely on on-site sales and microbreweries aiming for limited distribution, enabling targeted sales strategies based on customer maturity and business model. Furthermore, the material segment, primarily stainless steel, is crucial, as the quality and grade of steel directly impact equipment longevity, sanitation efficacy, and, consequently, the final product quality. The complexity and depth of these segments underscore the specialized nature of the microbrewing supply chain.

The Microbrewery Equipment Market value chain initiates with the upstream analysis, focusing on the procurement of raw materials, primarily high-grade stainless steel (304 and 316) crucial for vessels, along with specialized components like pumps, valves, sensors, and electronic control boards. Manufacturers often face challenges regarding stainless steel price volatility and maintaining stringent quality standards to ensure food-grade compliance and longevity. Key upstream activities involve precision metal fabrication, welding, and component sourcing, requiring specialized workshops capable of hygienic design and pressure vessel certification. Efficient management of these upstream logistics is critical for cost control and maintaining competitive pricing in the final product assembly. Manufacturers who establish reliable, high-volume sourcing relationships for stainless steel tubing and sheets gain a distinct cost advantage, while those who integrate advanced sensor and control panel manufacturing internally benefit from superior customization capabilities and integration reliability, a key differentiator in a specialized market.

The midstream phase involves the core manufacturing process, encompassing system design (often highly customized based on brewery space and desired capacity), fabrication, assembly, testing, and rigorous quality assurance checks, particularly hydrostatic testing of pressurized vessels. This stage is marked by high engineering complexity and the need for skilled labor capable of orbital welding to ensure sanitary surfaces. Downstream analysis focuses on distribution channels and delivery to the end-user. Direct distribution, where manufacturers sell directly to microbreweries, is common for custom or high-value systems, allowing for direct consultation and bespoke tailoring of the equipment package. Indirect distribution relies on specialized dealers, distributors, and agents who provide localized sales support, financing options, and installation services, particularly beneficial for reaching small, geographically dispersed start-ups and reducing the manufacturer’s logistical burden.

The distribution channel structure ensures that sales teams must possess deep technical knowledge of brewing science and process engineering, differentiating the equipment sale from standard industrial machinery. Furthermore, strong after-sales service, including maintenance contracts and spare parts inventory, is a critical value-added component in the downstream segment, contributing significantly to customer loyalty and long-term revenue streams. The efficiency of the commissioning and installation process, typically managed by specialized field service engineers, directly impacts the customer's time-to-market, making rapid deployment a key competitive factor. Overall, successful firms in this value chain integrate robust supply chain management upstream with technically competent direct and indirect sales channels downstream, providing comprehensive solutions that extend beyond mere hardware provision.

The primary potential customers and end-users of microbrewery equipment are specialized commercial entities operating within the beverage industry, seeking to produce high-quality, distinctive beer for local or limited regional consumption. Microbreweries, defined by their production volume (typically less than 15,000 U.S. beer barrels per year) and high percentage of beer sold off-site, represent the largest and most frequent buyers, requiring complete brewing systems, from milling to packaging. These customers prioritize efficiency, scalability, and adherence to strict hygienic standards. Brewpubs, which produce beer primarily for sale on-site through their own attached restaurant or taproom, form another significant customer base; they often seek smaller, visually appealing systems that can be integrated into public-facing spaces, emphasizing aesthetic design alongside functionality, requiring robust, space-saving vessels capable of high-frequency brewing cycles to meet immediate demand.

A growing segment includes expanding craft breweries that are scaling up production but remain below the regional brewery classification threshold, often seeking to upgrade existing equipment with larger fermentation tanks, sophisticated automation controls, or dedicated packaging lines (canning/bottling) to improve distribution capabilities. Additionally, educational institutions offering brewing science programs and research laboratories constitute a niche but important customer segment, requiring pilot brewing systems (typically 1-3 BBL) for instruction and experimentation. Finally, hospitality groups and high-end resorts are increasingly incorporating small, on-site brewing operations to offer exclusive, house-brand beers, treating the equipment purchase as a premium amenity investment. Targeting these diverse customers requires manufacturers to offer a wide range of modular equipment options, customized financing solutions, and strong technical consultancy, ensuring the chosen system aligns perfectly with the customer's operational scale, budget constraints, and long-term growth strategy.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.1 Billion |

| Market Forecast in 2033 | USD 6.5 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Meheen Manufacturing, JV Northwest, Alpha Brewing Operations, Braukon, Specific Mechanical Systems, NDL Keg, Newlands Systems, A.B. Vickers, Kaspar Schulz, Rolec, Esau & Hueber, Deutsche Beverage Technology, Premier Stainless Systems, Psychobrew, Criveller Group, SSV Tech, GEA Group, DME Brewing Solutions, Ziemann Holvrieka, Minibrew. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Microbrewery Equipment Market is undergoing a rapid evolution, moving away from purely manual operations toward integrated, automated, and IoT-enabled systems designed for precision and efficiency. A core technology shaping the market is the development of advanced Programmable Logic Controllers (PLCs) and Human-Machine Interface (HMI) touchscreens that offer precise control over every stage of the brewing process—from grain milling and mash temperature profiles to fermentation kinetics and chilling cycles. These sophisticated control systems utilize algorithms to maintain ultra-tight tolerances, which is critical for ensuring the consistency and replication of complex craft beer recipes. Furthermore, modular skid-mounted systems are a significant technological trend; these compact units integrate multiple components (mash tun, boil kettle, pumps, heat exchanger) onto a single, movable frame, significantly reducing installation time, footprint requirements, and overall capital expenditure, making them ideal for urban microbrewery installations where space is severely restricted. The adoption of remote diagnostic capabilities, facilitated by cloud connectivity, allows manufacturers to monitor equipment performance in real-time, anticipate maintenance needs, and provide instant technical support to brewers globally, enhancing operational reliability and reducing potential downtime associated with system failures.

In terms of vessel design and material technology, the focus remains heavily on maximizing thermal efficiency and sanitation effectiveness. High-grade stainless steel (316L) is becoming standard for critical components due to its superior corrosion resistance, crucial for handling the high acidity inherent in certain brewing styles and cleaning chemicals. Advanced jacket designs, particularly dimpled jackets, are widely employed in fermentation and bright tanks to maximize heat transfer efficiency for rapid cooling or precise temperature holding, thereby reducing energy consumption. Moreover, innovative technologies are emerging in the post-brewing phase, specifically in separation and filtration. Cross-flow filtration and centrifugation are increasingly accessible to larger microbreweries, allowing for yeast and haze removal without the traditional use of diatomaceous earth (DE) filters, leading to clearer beer, reduced environmental waste, and enhanced safety protocols in the brewery. The continuous integration of these diverse technologies underscores a market shift towards high-tech brewing that balances traditional craftsmanship with industrial-grade efficiency.

The push for sustainability is also driving technological adoption, with manufacturers introducing highly efficient heat recovery systems (HRS) that capture heat from the boiling kettle exhaust and waste streams to pre-heat incoming water or sanitize tanks, drastically reducing natural gas consumption. Additionally, sophisticated water treatment and reverse osmosis (RO) systems are now commonplace, allowing brewers to precisely mimic water profiles from famous brewing regions worldwide, ensuring recipe accuracy regardless of local municipal water quality. Coupled with this, automated Clean-in-Place (CIP) systems are leveraging ultrasonic technology and smart sensor feedback to minimize water usage and chemical consumption during the cleaning process, proving that environmentally conscious operations can also be financially advantageous. This commitment to smart, green, and efficient technology is a defining characteristic of the modern microbrewery equipment landscape, setting the stage for future expansion predicated on minimized resource usage and maximized product consistency.

The dynamics of the Microbrewery Equipment Market vary significantly across major geographical regions, influenced by localized craft beer maturity, regulatory support, and consumer spending power. North America, particularly the United States, represents the largest and most established market. This maturity means demand is shifting from initial installations to equipment upgrades and replacements, focusing on larger-capacity fermenters, automated packaging lines (canning being dominant), and energy-saving systems. The region benefits from a well-developed supply chain and high levels of technical expertise, driving manufacturers to innovate constantly in automation and modularity. Market saturation in some U.S. states is counterbalanced by continuous consumer demand for variety and hyper-local products, maintaining a steady, albeit slower, growth rate compared to emerging markets. European growth is robust, led by countries like Germany, the UK, and Italy, where craft brewing traditions are being revitalized with modern equipment. Demand here is characterized by a strong emphasis on quality, precision engineering, and adherence to strict regional brewing purity laws, such as the German Reinheitsgebot, driving sales of high-specification, reliable equipment often manufactured regionally.

The Asia Pacific (APAC) region is projected to exhibit the fastest growth over the forecast period, primarily driven by nascent but explosive market penetration in China, Japan, and Australia. China, in particular, is witnessing a proliferation of small, independent breweries in major metropolitan areas, driven by increasing disposable incomes and a rapid cultural shift towards Western-style consumption. These emerging markets represent significant greenfield opportunities, where the demand is for complete, turnkey 5 BBL to 15 BBL systems, making system integration capabilities a key competitive advantage for suppliers. However, challenges include establishing reliable distribution networks and navigating complex import duties and differing industrial standards. Latin America (LATAM), with promising markets like Brazil and Mexico, is following a similar trajectory, demonstrating strong consumer interest in craft beer, though economic volatility remains a constraint, often leading to preference for cost-effective or locally sourced equipment over high-end European or North American imports. Finally, the Middle East and Africa (MEA) remain smaller, highly regulated markets, where equipment sales are restricted mainly to tourist areas, specific licensed facilities, and South Africa, which has a more developed, indigenous craft beer sector.

The typical ROI for high-quality microbrewery equipment ranges between 3 to 5 years, highly dependent on the system's capacity utilization, regional craft beer pricing, and efficient brewery management. Investing in highly efficient, automated systems can accelerate this timeline by reducing operational expenses and enhancing batch consistency, thus maximizing revenue generation.

The most critical factors are the projected annual production volume, the intended distribution model (brewpub vs. off-site sales), and the physical footprint available. A 10 BBL system is often cited as a standard starting point, providing a balance between initial capital cost and sufficient scalability to meet early regional demand without over-investing in excess capacity.

Stainless steel 304 is standard for most fermentation and bright tanks, offering excellent durability. However, 316 grade stainless steel is superior, offering enhanced resistance to corrosion from chlorides, harsh cleaning chemicals, and high-acid brews. Using 316L (low carbon) in critical areas like heat exchangers ensures maximum longevity and maintains optimal sanitation integrity required for food-grade processing.

Automation, facilitated by advanced PLCs and sensor technology, ensures precise temperature control, process monitoring, and repeatable batch quality, minimizing human error. While the upfront cost is higher, automation is increasingly cost-effective for small-scale operations as it significantly reduces labor reliance, minimizes waste, and provides critical data for optimizing utility consumption, leading to long-term savings.

The Asia Pacific (APAC) region, particularly emerging economies like China, India, and Southeast Asian nations, offers the highest growth opportunities. These regions possess rapidly developing craft beer markets, large untapped consumer bases, and relatively low market penetration compared to the saturated, mature markets of North America and Western Europe, driving demand for new turnkey installations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.