ID : MRU_ 442978 | Date : Feb, 2026 | Pages : 241 | Region : Global | Publisher : MRU

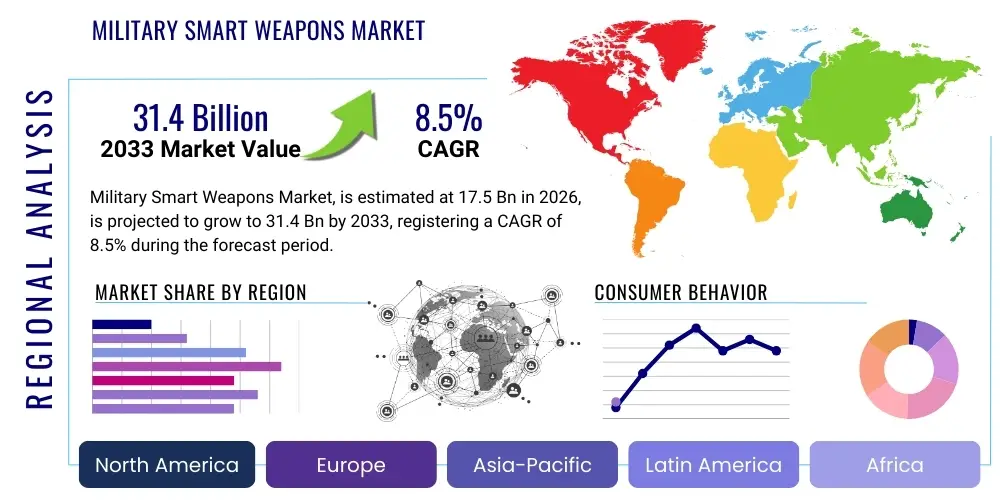

The Military Smart Weapons Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $17.5 Billion in 2026 and is projected to reach $31.4 Billion by the end of the forecast period in 2033.

The Military Smart Weapons Market encompasses advanced ordnance systems equipped with sophisticated guidance, navigation, and control (GNC) technologies designed specifically to maximize target probability while drastically minimizing the risk of collateral damage, a critical imperative in modern asymmetric warfare and constrained conventional conflicts. These precision-guided munitions (PGMs) represent a fundamental evolution in military capability, offering armed forces the ability to execute surgical strikes using integrated sensors, advanced processors, and flight control actuation mechanisms that allow for real-time trajectory correction based on live data feeds from the battlefield. The portfolio of products within this highly strategic sector is broad, ranging from tactical guided missiles—used extensively for air-to-ground and anti-tank roles—to strategic cruise missiles, guided artillery shells, and smart bombs such as the Joint Direct Attack Munition (JDAM) family, all unified by their common reliance on advanced electronics and software for precision targeting and terminal engagement. The core value proposition of these systems lies in their exceptional accuracy, ensuring that fewer munitions are needed to neutralize high-value targets, thereby reducing logistical burdens and improving overall operational efficiency in complex theater environments.

Major applications of military smart weapons span across the full spectrum of military operations, deeply integrating into air, land, and naval platforms to provide a layered defense and offense capability crucial for modern power projection. In the air domain, smart weapons facilitate stand-off engagement, allowing fighter and bomber aircraft to engage targets at safe distances using long-range cruise missiles and advanced air-to-surface munitions that employ multi-mode seekers for all-weather capability. Naval applications concentrate on sea denial and control, leveraging sophisticated anti-ship missiles (ASCMs) and smart torpedoes capable of advanced autonomous search and evasion maneuvers to counter contemporary maritime threats. Furthermore, the land warfare segment is rapidly expanding its reliance on smart artillery and guided rocket systems that convert previously area-denial weapons into precision instruments, effectively bridging the gap between direct fire and air support by providing immediate, highly accurate fire on demand. This ubiquitous integration across platforms highlights the essential role smart weapons play in achieving tactical surprise and maximizing combat effectiveness in multi-domain operational theaters.

The substantial operational and strategic benefits derived from the deployment of smart weapons are driving sustained market investment. These benefits include significantly enhanced mission success rates, reduced platform vulnerability by enabling standoff engagement, and crucial compliance with global ethical standards due to minimized civilian casualties and reduced environmental impact, which is increasingly factored into military planning. Market expansion is primarily propelled by three core factors: the sustained global increase in defense spending allocated specifically for modernization efforts aimed at replacing aging, inaccurate inventories with networked PGMs; continuous technological breakthroughs in sensor miniaturization, advanced materials science, and resilient guidance systems resistant to electronic warfare; and the critical need to develop and field sophisticated counter-capabilities, such as hypersonic weapons, necessary to penetrate increasingly dense and integrated anti-access/area denial (A2/AD) networks being established by potential state adversaries. This dynamic environment of threat evolution and technological leapfrogging guarantees robust market growth and continuous innovation throughout the forecast period, emphasizing speed, stealth, and autonomous guidance.

The global Military Smart Weapons Market is experiencing substantial structural shifts driven by intensified geopolitical competition and an unprecedented technological arms race focusing on speed, autonomy, and range. Current business trends show a marked shift in procurement towards advanced tactical missile systems (including loitering munitions, often referred to as 'suicide drones') and strategic long-range capabilities, particularly the highly coveted hypersonic weapons capable of maneuvering at speeds exceeding Mach 5, making them virtually indefensible by current systems. The competitive landscape is characterized by high levels of vertical integration among defense prime contractors, who are strategically acquiring specialized AI and GNC software firms to secure proprietary knowledge essential for developing next-generation autonomous capabilities. Furthermore, international sales remain critical, highly dependent on geopolitical alignment, with the Foreign Military Sales (FMS) program facilitating substantial technology transfer, albeit under strict regulatory regimes aimed at curbing proliferation risks and maintaining technological advantage over non-allied nations, thus consolidating market power among established global leaders.

Regionally, the market exhibits a dichotomy defined by mature technological dominance and high growth potential. North America, led by the colossal purchasing power and technological expertise of the U.S. Department of Defense (DoD), serves as the global innovation hub, pouring vast resources into R&D for AI-enabled targeting and advanced seeker technologies, thereby maintaining the largest market share in terms of value. Conversely, the Asia Pacific (APAC) region is demonstrating the most aggressive compound annual growth trajectory, driven by massive defense spending increases in key economic and military powers like China and India, focusing specifically on bolstering maritime strike capabilities, developing indigenous guided missile systems, and acquiring strategic stand-off weapons to manage complex regional security challenges. European market momentum is bolstered by renewed urgency for capability enhancements under NATO frameworks, focusing on standardization and the collective replenishment of ammunition stocks, particularly air-launched PGMs and modern anti-tank systems, reflecting a focused approach to conventional defense strengthening following regional geopolitical crises.

Segment-specific trends reveal that the 'Missiles' category, encompassing tactical and strategic systems, remains the largest revenue generator, largely due to the continuous demand for enhanced range and advanced ECCM (Electronic Counter-Countermeasure) features required in contested environments. The 'Technology' segment is seeing accelerating investment in Precision Guidance Kits (PGKs), which offer a lower-cost entry point for precision capability by upgrading existing inventories of unguided ordnance, making precision fire accessible to a wider range of defense organizations. Moreover, the 'Land Platform' segment is experiencing a significant uplift, driven by the deployment of highly mobile, rapidly targetable guided rockets and enhanced artillery systems. This trend reflects a crucial shift in military doctrine toward decentralized precision fire support, ensuring that ground maneuver units possess integral PGM capabilities without sole reliance on centralized air assets, optimizing response times and survivability in dynamic land operations against peer and near-peer adversaries across diverse terrains.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally redefining the performance characteristics and operational capabilities of military smart weapons, moving beyond simple programmed flight paths to genuine intelligent autonomy. AI algorithms are now critical for advanced sensor data fusion, allowing a missile or guided projectile to simultaneously process inputs from multiple sensor types—such as imaging infrared (IIR), millimeter-wave (MMW) radar, and high-resolution cameras—to generate a single, highly accurate target solution, especially critical in environments where visibility is degraded by weather or smoke. This advanced processing allows the weapon system to distinguish complex targets from decoys, clutter, and non-combatant vehicles with vastly superior reliability than human operators or older, template-matching systems, directly translating into enhanced precision, reduced risk of mission failure, and increased system effectiveness in dense urban or highly sophisticated battlefields characterized by advanced adversary deception tactics.

Furthermore, AI significantly enhances the survivability and mission success of smart weapons by enabling autonomous navigation and sophisticated in-flight decision-making, particularly concerning Electronic Counter-Countermeasures (ECCM). AI-driven guidance systems can detect jamming signals, classify the type of electronic attack in real-time, and instantaneously switch to alternative, non-GPS-dependent guidance modes, or adapt flight profiles to avoid interception, a level of adaptive resilience unattainable with pre-programmed systems. This ability to self-optimize the flight path and continuously reassess the threat environment is essential for penetrating sophisticated Anti-Access/Area Denial (A2/AD) layers. The application extends to network connectivity, where AI facilitates cooperative engagement, allowing multiple munitions launched from different platforms to communicate and share targeting data dynamically, coordinating a synchronized strike that maximizes the probability of target destruction while optimizing munition allocation and striking effectiveness against widely dispersed targets.

The long-term impact of AI on the market is centered around the development of fully autonomous, "fire-and-forget" capabilities that require minimal human intervention post-launch, drastically speeding up the decision-to-strike cycle, which is a key advantage in high-speed conflict scenarios like hypersonic engagements. However, this advancement simultaneously intensifies ethical and regulatory scrutiny regarding the human-in-the-loop requirement and accountability for autonomous actions in combat. The ongoing research focuses on developing robust Verification and Validation (V&V) protocols for AI-driven weapons to ensure predictable and compliant behavior under all operational conditions. Despite these hurdles, the technological benefits—particularly the capacity to handle vast amounts of sensor data and execute complex maneuvers at speeds that preclude human control—ensure that AI technology remains the central investment priority for all leading defense manufacturers and military powers shaping the future landscape of precision weaponry and integrated smart ordnance systems.

The Military Smart Weapons Market is strategically shaped by a robust framework of Drivers, Restraints, and Opportunities (DRO), collectively exerting powerful Impact Forces on investment, regulation, and technological development worldwide. A primary driver is the accelerating pace of global military modernization, compelled by evolving geopolitical flashpoints, including heightened tensions in the South China Sea, Eastern Europe, and the Middle East, which necessitate the deployment of highly accurate, stand-off capabilities to deter or prosecute high-intensity conflicts effectively. The shift in military doctrine towards precision targeting, driven by the desire to minimize collateral damage and maximize efficiency by reducing the required number of platforms and sorties, further fuels continuous demand for advanced PGMs. Moreover, the replacement cycle of vast global stockpiles of aging, unguided ordnance with modern smart weapons ensures a sustained revenue stream for manufacturers over the long term, cementing this as a critical growth accelerator.

Conversely, market expansion faces significant restraints, chiefly stemming from the exorbitant Research and Development (R&D) expenditures required to develop cutting-edge guidance electronics, advanced propulsion systems, and resilient navigation software, posing a steep barrier to entry for smaller firms and limiting adoption rates among developing nations. The high unit cost of precision-guided munitions (PGMs) compared to their conventional counterparts creates substantial budgetary pressure on defense procurement agencies, forcing strategic prioritization of acquisitions. Furthermore, the stringent regulatory environment, including export control regimes like the Missile Technology Control Regime (MTCR) and various national defense policies governing technology transfer, severely restricts the potential market size and dictates sales geography, limiting the ability of manufacturers to capitalize fully on global demand and necessitating complex licensing and end-user agreements for international sales.

Opportunities for future market growth are heavily concentrated in technological breakthroughs, notably the commercialization and mass production of hypersonic weapons, which offer entirely new strategic capabilities for rapid, long-range global strikes, opening multibillion-dollar development programs. Additionally, the increasing demand for cost-effective PGMs, such as the aforementioned Precision Guidance Kits (PGKs) for existing artillery, presents a lucrative opportunity for democratizing precision capability, expanding the customer base beyond the handful of tier-one military powers. The predominant impact forces are inextricably linked to the technological arms race—where rapid adversary deployment of advanced electronic warfare (EW) countermeasures necessitates continuous, responsive innovation in seeker resilience, autonomous guidance, and robust communication links, creating a constant pressure for system upgrades and generational replacements, guaranteeing sustained long-term market vitality and strategic defense spending across all major global defense budgets.

The Military Smart Weapons Market is meticulously analyzed through segmentation across Platform, Type, Technology, End-User, and Range, providing a detailed framework for understanding specific procurement trends and technological investment priorities within the global defense sector. This detailed segmentation is paramount for defense planners and industry analysts as it accurately maps where capital is being deployed—for instance, distinguishing between investments in strategic long-range capabilities (e.g., strategic missiles for Air Force platforms) versus investments in mass-deployable, cost-effective tactical solutions (e.g., guided projectiles for Army forces). The granularity allows defense contractors to precisely tailor their product development roadmaps and marketing efforts to address the unique performance requirements and budgetary constraints of specific military branches and operational environments globally.

In terms of segmentation by Type, the Missiles category continues to dominate the market in value, fueled by continuous requirements for air superiority, anti-ship interdiction, and deep-strike capabilities that necessitate sophisticated, long-range platforms. However, the fastest-growing segment by volume is increasingly centered around Guided Projectiles and Loitering Munitions. Guided projectiles, often representing converted conventional artillery or mortar shells, are favored for their ability to provide precision fire support at a fraction of the cost of a dedicated missile, enhancing ground unit effectiveness. Loitering munitions, offering persistent surveillance and the capacity for delayed, precise engagement, are becoming indispensable tools in modern asymmetric conflicts, reflecting a critical shift towards small, networked, expendable assets for tactical supremacy in close-quarters combat environments, significantly impacting the Land Platform segment's growth trajectory.

The Technology segmentation highlights the progression from basic Inertial Navigation Systems (INS) and legacy GPS integration to advanced, multi-modal seekers utilizing Imaging Infrared (IIR) and Millimeter-Wave (MMW) radar simultaneously for target acquisition and tracking resilience. Precision Guidance Kits (PGK) remain a high-volume technology segment, offering rapid capability enhancement to existing ammunition stocks worldwide. Within the End-User analysis, while the Air Force has historically been the leading procurer of high-value PGMs like stand-off and cruise missiles, the Army segment is demonstrating accelerated growth due to increased spending on smart artillery, Anti-Tank Guided Missiles (ATGMs), and loitering systems, reflecting a global military doctrine that prioritizes integrated, all-domain precision fire. This detailed analysis of segmentation ensures a holistic understanding of where the innovation dollars are being spent and how defense doctrines influence product adoption rates globally.

The value chain within the Military Smart Weapons Market is characterized by extremely high levels of complexity, proprietary technology, and stringent government control, creating a tiered structure where trust and security are paramount. The upstream segment is anchored by specialized component manufacturers who supply critical, often custom-made inputs necessary for performance. This includes producers of advanced composite materials (e.g., carbon fiber, high-strength alloys) for lightweight airframes; developers of hardened microelectronics and specialized radiation-tolerant processors for the GNC unit; and highly specialized manufacturers of micro-electromechanical systems (MEMS) gyroscopes and accelerometers essential for precision Inertial Navigation Systems (INS). Given the sensitive nature of the technology, these suppliers are typically tightly integrated into the defense ecosystem and must comply with rigorous security and quality standards, resulting in a highly consolidated supplier base predominantly located in NATO or allied nations.

The central manufacturing segment is dominated by a few global defense prime contractors (e.g., Lockheed Martin, Raytheon, MBDA) responsible for the core task of systems integration, which includes developing and embedding the proprietary guidance software, integrating the warhead and fusing mechanism, and conducting extensive, costly qualification and certification trials. This is the stage where maximum value addition occurs, requiring deep expertise in aerodynamics, sensor technology, and complex software engineering. The distribution channel is near-exclusively direct: finished smart weapons move from the prime manufacturer directly to the procuring governmental entity (Ministry of Defense, Air Force, Navy). Sales routes are strictly bifurcated into domestic procurement and tightly controlled international sales, often managed via government-to-government agreements like the U.S. Foreign Military Sales (FMS) program or similar mechanisms in European nations, ensuring that technology leakage and unauthorized proliferation are mitigated through legally binding contractual and diplomatic frameworks.

The downstream activities involve the end-users—the military forces—and the critical sustainment phase. Since smart weapons incorporate highly sensitive and often encrypted electronic components, maintenance, repair, and overhaul (MRO) services, along with software updates and mid-life modernization (MLU) programs, are almost always provided directly by the original equipment manufacturer (OEM) or its licensed partners. This reliance on the OEM for lifelong support creates significant, high-margin aftermarket revenue streams, effectively extending the value chain far beyond the initial purchase. The focus in the downstream segment is not merely on logistics, but on ensuring operational readiness, continuous software integrity, and personnel training. The strategic imperative for security and performance overrides commercial cost considerations throughout this value chain, contrasting sharply with standard commercial product markets where efficiency and decentralized distribution are prioritized over strict control and proprietary technology safeguards.

The pool of potential customers for the Military Smart Weapons Market is inherently restricted to sovereign nation-states and their formally recognized defense and security organizations, primarily comprised of Ministries of Defense and the operational military branches: the Air Force, Navy, and Army. These customers are driven by national security mandates, requiring weaponry that ensures deterrent capability, tactical superiority, and alignment with alliance commitments (such as NATO or regional security pacts). Procurement decisions are lengthy, multi-faceted processes influenced by geopolitical risk assessment, long-term strategic planning, complex budget allocations, and the industrial offset requirements often demanded by the purchasing government to foster local defense industry development, making relationship management and diplomatic engagement critical components of the sales cycle for manufacturers.

Key tier-one customer groups include the major global military spenders: the United States, China, Russia, India, Saudi Arabia, and NATO members (e.g., United Kingdom, France, Germany). These entities possess vast budgets and consistently seek cutting-edge technology—such as hypersonic capabilities, advanced networked munitions, and AI-enabled targeting systems—to maintain a technological edge or achieve parity with rival powers. For example, the U.S. Navy and Air Force are heavy procurers of high-value strategic cruise missiles and advanced anti-ship systems, while the Indian Army is focusing on acquiring or developing highly mobile Anti-Tank Guided Missiles (ATGMs) and precision artillery kits to address specific border conflicts and terrain challenges, demonstrating diverse, high-value needs across the top tier.

Emerging and tier-two customer groups, primarily located in regions undergoing rapid modernization (Southeast Asia, Eastern Europe, and select Middle Eastern nations), also represent substantial market potential. These customers typically prioritize proven, reliable tactical smart weapons, such as laser-guided rockets, cost-effective PGKs for artillery, and readily available tactical missiles, often acquired via international defense partnerships or FMS programs from established suppliers. Their purchasing criteria often balance capability enhancement against budgetary limitations, making technologies that offer maximum precision at a competitive unit cost particularly attractive. This segmentation illustrates that while tier-one customers drive innovation and high-cost sales, tier-two customers drive volume and demand for accessible, field-proven precision strike solutions to enhance their regional deterrence postures effectively.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $17.5 Billion |

| Market Forecast in 2033 | $31.4 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Raytheon Technologies, Lockheed Martin, BAE Systems, Northrop Grumman, General Dynamics, Boeing, Thales Group, MBDA, Rafael Advanced Defense Systems, Israel Aerospace Industries (IAI), L3Harris Technologies, Saab AB, Leonardo S.p.A., Hanwha Defense, Diehl Defence, Roketsan, Kratos Defense & Security Solutions, Hindustan Aeronautics Limited (HAL), Nexter Systems, Kongsberg Gruppen |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Military Smart Weapons Market is undergoing rapid and disruptive evolution, primarily focused on achieving higher velocities, greater ranges, and enhanced immunity to sophisticated electronic warfare (EW) techniques. The core technological foundation remains the seamless integration of high-accuracy Inertial Navigation Systems (INS) with resilient Global Positioning System (GPS) receivers, often augmented by specialized anti-jamming antennas and processing filters to maintain positional accuracy even in high-threat environments. However, recognizing the critical vulnerability of satellite navigation, there is a substantial technological shift toward GPS-independent solutions, including sophisticated terrain-following navigation (TERCOM), advanced scene-matching algorithms using digitized mapping data, and astrodynamic guidance systems for long-range strategic missiles, ensuring operational capability when GPS is denied or degraded by adversarial jamming or spoofing attacks.

Terminal guidance system development represents the paramount area of current technological investment, moving beyond legacy laser-only or infrared-only systems to highly advanced multi-modal seekers that simultaneously employ multiple detection methodologies. These systems combine high-resolution Imaging Infrared (IIR) for target shape recognition, Millimeter-Wave (MMW) radar for all-weather ranging and velocity tracking, and possibly semi-active laser (SAL) guidance for terminal engagement precision. The real breakthrough lies in the sensor fusion software, often powered by embedded AI processors, which instantly weighs data from all sensors to maintain a lock on the target while filtering out decoys and environmental clutter. This technological fusion allows smart weapons to operate effectively day or night, in heavy fog, through smoke, and against targets employing advanced camouflage or active countermeasures, substantially increasing the probability of a first-shot kill across diverse and contested operational theaters.

Two other critical technology areas are advanced propulsion and digital connectivity. The race for hypersonic weapons (Mach 5 and above) relies entirely on breakthroughs in air-breathing propulsion systems, specifically scramjet technology, which allows missiles to travel at extreme speeds over vast distances, significantly shrinking an adversary’s reaction time and rendering conventional missile defense systems obsolete. Simultaneously, for tactical weapons, the technology emphasis is on robust, secure, and high-bandwidth data links that maintain connectivity between the launching platform and the munition (man-in-the-loop capability) until the final engagement phase. This bi-directional communication ensures target updates, mission abort capabilities, and battle damage assessment can be performed instantaneously, integrating the munition into the broader networked battlespace, allowing for real-time human oversight or autonomous coordination among multiple smart weapons, enhancing overall mission flexibility and operational strategic capability.

The global distribution and growth profile of the Military Smart Weapons Market are heavily skewed towards regions with dominant military spending and intensifying security challenges, necessitating extensive analysis of North America, Asia Pacific (APAC), and Europe as the core revenue drivers. North America, unequivocally anchored by the robust defense industrial base of the United States, holds the largest market share globally. The U.S. commitment to maintaining decisive technological superiority mandates continuous, expansive investment in cutting-edge smart weapon R&D, focusing heavily on strategic initiatives such as fielding operational hypersonic platforms, perfecting AI-enabled autonomous guidance, and integrating stealth capabilities into PGM designs to ensure effectiveness against near-peer threats. This sustained governmental funding guarantees North America's continued leadership in innovation, establishing it as the primary market for high-value, high-performance strategic weapons systems and shaping global defense technology standards.

The Asia Pacific region stands out as the primary engine for future growth, exhibiting the highest projected CAGR, driven by complex and escalating maritime and territorial disputes that fuel a massive military buildup across multiple nations. China's rapid indigenous development and deployment of advanced anti-ship missiles, including carrier-killer capabilities and sophisticated cruise missile variants, fundamentally alter the strategic balance, compelling nations like Japan, South Korea, Australia, and India to accelerate their own acquisition of modern smart weapons for defense and deterrence. This regional arms modernization race concentrates investment in naval PGMs, advanced air-to-ground guided munitions, and indigenous guided rocket systems, transforming APAC from a regional procurement hub into a critical consumer and, increasingly, a significant producer of sophisticated smart weaponry, ensuring that market growth here will significantly outpace global averages over the forecast period.

Europe, driven by the renewed urgency of collective defense planning within NATO and the need to replace stockpiles and upgrade conventional deterrence capabilities, represents a stable and growing market segment. European nations prioritize interoperability and standardization, often procuring smart weapons through collaborative frameworks like the MBDA consortium, focusing on tactical air-to-ground missiles (ATGMs), multi-role guided rockets, and advanced air defense systems. The Middle East and Africa (MEA) continues to be a crucial consumer market, although heavily reliant on imports from the U.S. and Israel. Procurement decisions in MEA are often highly reactive, driven by immediate localized security threats, counter-insurgency requirements, and the necessity to maintain regional power balances, resulting in steady demand for proven, high-precision tactical smart weapons, particularly those effective in desert and urban combat scenarios, maintaining its role as a strategic high-value import market.

The primary factor driving growth is the escalating global geopolitical instability and the resulting imperative for national defense forces to modernize their arsenals with precision-guided munitions (PGMs) that minimize collateral damage and enhance operational lethality, particularly against highly mobile or fortified targets. This includes significant investment in counter-A2/AD capabilities and stand-off weapons.

AI is being utilized to enable fully autonomous target recognition, optimize in-flight trajectory correction in real-time, enhance resistance to electronic countermeasures (ECCM), and facilitate cooperative engagement between multiple networked munitions, moving weapons from guided systems to intelligent, self-optimizing assets.

The Asia Pacific (APAC) region is projected to register the fastest growth rate, primarily fueled by massive military modernization programs in countries like China and India, driven by increasing territorial disputes and the necessity to counter regional power shifts through sophisticated long-range precision strike capabilities.

The main types include guided missiles (both tactical and strategic, such as air-to-air, air-to-ground, and anti-ship systems), guided bombs (e.g., JDAM variants), guided artillery projectiles (PGKs), and loitering munitions, with tactical missiles retaining the largest market share due to their versatile application across all combat domains.

Major restraints include the extremely high upfront Research & Development (R&D) costs associated with advanced guidance technology, the high unit cost of precision-guided munitions compared to conventional ordnance, and strict international regulatory frameworks and export controls (e.g., MTCR) governing the transfer of sensitive defense technology.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.