ID : MRU_ 442246 | Date : Feb, 2026 | Pages : 243 | Region : Global | Publisher : MRU

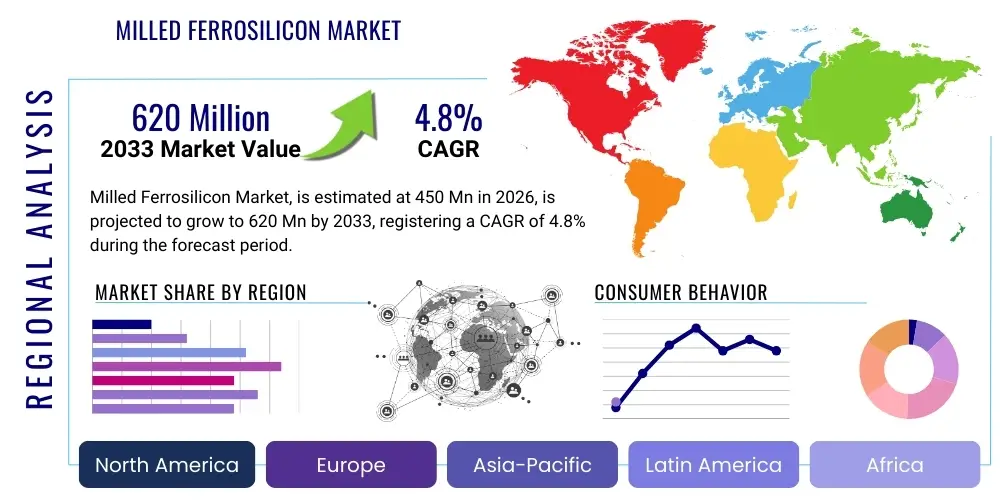

The Milled Ferrosilicon Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 620 Million by the end of the forecast period in 2033.

Milled Ferrosilicon (FeSi) is a specialized iron alloy containing varying percentages of silicon, typically ranging from 15% to 90%, which is mechanically processed into a fine powder or grit. This material is indispensable across several heavy industries, notably within the mining sector for Dense Medium Separation (DMS) processes, and in metallurgy for manufacturing welding electrodes and specialized powder components. Its primary benefit stems from its high density, excellent magnetic properties, and corrosion resistance, which make it an ideal medium for gravity separation of minerals, particularly in coal and iron ore processing where precise density control is paramount for efficiency and recovery rates. The stringent quality requirements for particle size distribution and chemical purity drive continuous innovation in milling and classification technologies, ensuring the final product meets the demanding specifications of end-users.

The market for milled ferrosilicon is fundamentally influenced by global industrial output, particularly the demand for refined steel, high-quality welding materials, and the need for efficient mineral processing, especially in developing economies scaling up mining operations. Its stability under harsh operating conditions and its recoverability in DMS circuits contribute significantly to its economic viability and sustained demand. Furthermore, the shift towards higher-grade steel production requires specific compositions of ferrosilicon powder to control oxygen content and microstructural integrity during the casting process, cementing its role as a critical additive. Ongoing urbanization and infrastructural development projects globally are indirectly boosting demand for steel, which in turn fuels the consumption of high-pquality ferrosilicon products.

Key driving factors for the Milled Ferrosilicon Market include the global emphasis on resource optimization and increased efficiency in mineral extraction, particularly the processing of low-grade ores which necessitates highly effective separation media like FeSi. The steady growth in the welding and fabrication industry, which utilizes milled ferrosilicon in flux coatings for welding electrodes to improve arc stability and deoxidizing capabilities, also provides robust market momentum. Environmental regulations promoting resource recovery and waste reduction further encourage the adoption of closed-loop DMS systems, where the recyclability of milled ferrosilicon is a significant operational advantage. Technological advancements in milling processes, leading to finer and more uniform particle sizes, are broadening its applications in advanced powder metallurgy.

The Milled Ferrosilicon Market exhibits stable growth, primarily driven by robust expansion in the global mining sector and consistent demand from the metallurgical and welding industries. Business trends indicate a strong focus among key manufacturers on optimizing particle size distribution and enhancing the purity of the milled product to cater to high-end applications such as high-purity powder metallurgy and sophisticated DMS circuits. Strategic acquisitions and vertical integration, especially by companies controlling both the raw ferrosilicon production and the subsequent milling and classification processes, are defining the competitive landscape. Supply chain stability, influenced by the availability of metallurgical-grade silicon and iron scrap, remains a critical operational consideration, pushing companies toward long-term raw material sourcing agreements to mitigate price volatility and ensure continuous supply capacity.

Regionally, the Asia Pacific (APAC) stands as the dominant and fastest-growing market, largely due to extensive coal mining operations in China, India, and Australia, coupled with monumental infrastructure investments driving steel and construction demand. North America and Europe, while mature, demonstrate stable demand, focusing primarily on high-purity grades for advanced manufacturing and specialized welding applications, driven by stringent quality controls in the automotive and aerospace sectors. Emerging markets in Latin America and the Middle East and Africa (MEA) are showing promising growth, attributed to new mining projects commencing operation and increasing domestic steel production capabilities, requiring substantial volumes of separation media and alloy additives.

Segment trends reveal that the Dense Medium Separation (DMS) application segment maintains the largest market share, directly correlated with the cyclical yet enduring nature of the global mining industry, particularly the separation of iron ore, coal, and non-ferrous metals. Within the mesh size segments, the 100-200 Mesh and 200-325 Mesh sizes are highly sought after, reflecting the optimal balance between cost and efficiency required for most standard DMS applications. The High-Purity Grade segment is projected to experience a slightly higher growth trajectory, fueled by technological requirements in advanced powder metallurgy and specialized magnetic applications demanding minimal impurities, thus commanding premium pricing and attracting specialized manufacturing investments.

User inquiries regarding the impact of Artificial Intelligence on the Milled Ferrosilicon Market frequently center on themes such as predictive maintenance in milling operations, optimization of DMS circuit performance, and the use of machine learning to enhance raw material sorting and quality control. Users are keen to understand if AI can reduce operational costs, improve the consistency of the milled product (particle size uniformity), and accelerate material recovery rates in mining. The key expectations revolve around leveraging AI to model complex separation parameters in real-time, predict equipment failures in energy-intensive milling machinery, and automate decision-making processes regarding alloy composition adjustments during initial ferrosilicon production, thus minimizing waste and maximizing yield across the entire value chain.

The Milled Ferrosilicon Market is characterized by a dynamic interplay of factors that both stimulate and constrain its growth. Key drivers include the revitalization of the global mining industry, particularly the demand for coal and iron ore requiring effective DMS techniques, and sustained growth in the welding consumable sector. Opportunities reside in the expansion of high-purity applications in powder metallurgy for electric vehicle components and specialized magnetic materials, alongside geographical expansion into rapidly industrializing regions. However, market growth is primarily restrained by the cyclical volatility inherent in the prices of raw materials (silicon metal and steel scrap) and the high energy requirements and associated costs of the milling and classification processes, which significantly impact operational profitability and pricing strategies, making efficient energy management a competitive necessity.

Drivers: Increased global demand for efficient mineral processing, especially in large-scale coal and iron ore beneficiation plants, remains the paramount driver. The superior recyclability and magnetic properties of milled ferrosilicon over alternative separation media, coupled with stringent quality standards for welding electrodes used in high-integrity structures, contribute substantial momentum. Furthermore, governmental initiatives worldwide focusing on infrastructure modernization and heavy construction necessitate large volumes of structural steel, indirectly bolstering demand for metallurgical additives and specialized DMS media.

Restraints: Significant restraints include the substantial capital investment required for establishing high-precision milling facilities capable of producing uniform particle sizes, creating high barriers to entry. The market is also sensitive to environmental regulations concerning dust emissions during processing and the disposal of industrial waste from ferrosilicon production. Furthermore, the inherent price instability of metallurgical silicon, influenced by energy costs and international trade tariffs, introduces significant complexity and risk into the supply chain management, challenging long-term planning for manufacturers.

Opportunity: The largest opportunities lie in penetrating niche markets requiring ultra-fine and high-purity milled ferrosilicon, such as soft magnetic composites (SMCs) used in advanced electronics and electric motors, and specialized fillers in chemical composites. Geographic expansion into emerging markets in Africa and Southeast Asia, where resource extraction and basic industrialization are accelerating, presents untapped demand. Additionally, innovation in milling technology that improves energy efficiency and reduces operating expenditure offers a pathway for competitive differentiation and market share gain.

Impact Forces: The degree of influence exerted by these forces is substantial. The primary impact force is the level of industrial activity, particularly steel production and commodity prices, which directly dictates demand from end-user sectors. Technological impact forces, primarily focused on enhancing particle geometry and minimizing impurities, influence product differentiation and pricing power. Environmental impact forces are increasing, pushing manufacturers toward cleaner production methods and more efficient recycling of the separation media. The cumulative effect of these forces determines market trajectory, profitability margins, and the strategic viability of market participants.

The Milled Ferrosilicon Market is comprehensively segmented based on its crucial attributes, including the grade of ferrosilicon used, the final mesh size achieved, the primary application area, and the specific end-use industry utilizing the product. This structural breakdown provides a granular view of market dynamics, revealing varying growth rates and demand characteristics across different product specifications and consumer applications. Segmentation is vital for market participants to tailor their production capabilities and marketing strategies to address specific industrial requirements, such as the high purity demanded by powder metallurgy versus the volume needs of the DMS sector, ensuring optimal resource allocation and competitive advantage in specialized areas of consumption.

The value chain for Milled Ferrosilicon begins with the procurement of raw materials, primarily high-grade quartz (silica) and iron scrap, which are smelted in submerged arc furnaces to produce primary bulk ferrosilicon. This constitutes the upstream segment, where energy cost and raw material quality are the determining factors of initial product cost and quality. Key activities at this stage involve meticulous resource management, effective energy utilization, and ensuring compliance with metallurgical standards for the initial alloy. Stability in the price of silicon metal profoundly impacts the profitability of the entire downstream process, making secure long-term contracts for energy and raw materials essential for large-scale producers to maintain cost stability and competitive pricing in the final milled product market.

The midstream of the value chain involves the specialized processing of the primary alloy. This includes crushing, grinding (milling), and precise classification to achieve the required mesh size and particle distribution for specific applications, such as DMS or powder metallurgy. Milling is an energy-intensive process requiring specialized equipment, such as ball mills or jet mills, often utilizing inert atmospheres for high-purity grades to prevent oxidation. Quality control checks for particle sphericity, density, and chemical purity are critical at this juncture. The distribution channel subsequently handles the logistics, including direct sales to large mining houses or indirect sales through specialized chemical and metallurgical distributors who manage regional inventory and handle technical support for smaller end-users across geographical boundaries.

The downstream segment encompasses the utilization of milled ferrosilicon by end-users, predominantly within the mining (DMS) and metallurgical industries (welding, powder metallurgy). Direct distribution is common for large-volume purchasers, such as major coal processing facilities or large steel mills, ensuring timely supply and technical specification adherence. Indirect channels, involving regional agents or specialized distributors, are crucial for reaching dispersed users in the welding electrode manufacturing or smaller powder metallurgy firms. The efficiency and performance of the milled product directly influence the end-users' profitability, such as mineral recovery rates in DMS, establishing a strong feedback loop that drives product specification changes and quality improvements across the value chain.

Potential customers for Milled Ferrosilicon are primarily large industrial entities whose core operations depend on high-efficiency separation processes or specialized alloy additives. The largest consumer base comprises global mining corporations involved in the beneficiation of bulk commodities such as coal, iron ore, and manganese, where Dense Medium Separation (DMS) is the standard method for upgrading low-grade ores. These customers require high volumes of standard grade, highly uniform FeSi powders that can be efficiently recovered and reused within closed-loop circuits. The reliability, magnetic susceptibility, and wear resistance of the milled product are critical selection criteria for these buyers, prioritizing suppliers with robust quality management and dependable logistics capabilities essential for uninterrupted mining operations.

A second significant customer segment includes manufacturers of welding electrodes and fluxes. These companies incorporate fine ferrosilicon powder into electrode coatings as a deoxidizing agent and alloying element to improve weld strength, appearance, and arc stability. The quality requirements here focus intensely on chemical purity, specifically low carbon and sulfur content, which prevents detrimental porosity in the weld metal. Similarly, companies specializing in advanced powder metallurgy, supplying components for the automotive (especially electric vehicle motors) and aerospace sectors, are increasingly important customers, demanding ultra-fine, high-purity milled ferrosilicon for creating complex soft magnetic composites and high-density sintered parts, driving growth in the high-purity segment.

Furthermore, specialized chemical and magnetic material producers also constitute a niche but valuable customer base. These buyers utilize milled ferrosilicon for its specific chemical properties or high magnetic permeability in niche manufacturing processes. The purchasing decisions of all these end-users are driven not just by price, but predominantly by technical specification compliance, consistent supply capacity, adherence to global certification standards, and the provision of adequate technical support for application-specific optimization, creating a market environment where supplier reputation and proven product performance are paramount competitive differentiators across all procurement processes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 620 Million |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Elkem ASA, FerroGlobe PLC, Russian Ferro-Alloys, IMFA, SMS Group GmbH, Westbrook Resources, AMG Advanced Metallurgical Group, M&M Alloys, RIMA Industrial S.A., Sino-Alloy International, China Minmetals, Gulf Ferro Alloys Company (GULFAS), Pamica Electric, Reade Advanced Materials, Minhang Silicon Industry, FESIL, Essar Group, OM Holdings Limited, OFZ, a.s., Siderurgica Norte |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Milled Ferrosilicon Market is centered around optimizing the mechanical reduction and classification of the ferroalloy to achieve ultra-fine powders with tightly controlled particle size distributions (PSDs) and minimal contamination. The primary technological focus involves advanced milling techniques, such as continuous ball milling systems operating in closed circuits, which maximize grinding efficiency while minimizing energy consumption. For the production of the finest grades required by powder metallurgy, jet mills and stirred media mills are employed, capable of producing powders below 325 mesh size with high sphericity and reduced internal stress. Furthermore, sophisticated air classification systems are integral, ensuring that particles outside the required size range are efficiently separated and returned for further grinding, thereby optimizing product yield and consistency across large production batches.

Beyond the physical reduction, significant technological advancements are occurring in process control and quality assurance. Modern production facilities are integrating laser diffraction and image analysis tools for real-time monitoring of PSD, allowing for immediate adjustments to milling parameters and ensuring compliance with strict industrial standards, especially for materials used in high-precision Dense Medium Separation (DMS) circuits where viscosity control is paramount. Furthermore, specialized surface treatment technologies, including protective coatings or modified atmospheres during milling, are sometimes applied, particularly for high-purity ferrosilicon, to minimize surface oxidation and enhance shelf life, crucial for maintaining the magnetic properties and density required for critical applications such as high-temperature pressing and sintering processes.

Sustainability and operational efficiency are driving the adoption of advanced sensor technology and Industrial Internet of Things (IIoT) platforms within milling operations. These technologies enable predictive maintenance of high-cost components and optimization of the energy-intensive crushing and grinding phases, leading to significant reductions in overall operating costs and environmental footprint. Innovations in material handling, including pneumatic conveying systems specifically designed for abrasive metallic powders, ensure product integrity and prevent segregation or cross-contamination during internal transport and packaging. This continuous technological refinement, focusing on precision, purity, and efficiency, dictates the competitive advantage among leading manufacturers in the global market, particularly those supplying the highly demanding aerospace and automotive powder metallurgy segments.

Milled Ferrosilicon is predominantly used in the mining sector for Dense Medium Separation (DMS), acting as a highly dense, recoverable medium to efficiently separate valuable minerals (like coal, iron ore, and non-ferrous metals) from waste gangue based on specific gravity differences, optimizing resource recovery rates.

The most common mesh sizes utilized in standard DMS applications typically fall within the 100-200 Mesh and 200-325 Mesh ranges. This particle size distribution provides the optimal balance of suspension stability, viscosity control, and recoverability within the heavy media circuit, ensuring operational efficiency.

Fluctuations in the price of primary raw materials, specifically metallurgical silicon and iron scrap, directly impact the cost of producing bulk ferrosilicon. Since milling adds high operational costs (energy), raw material volatility significantly influences the final selling price of milled ferrosilicon and affects manufacturer profit margins and market pricing stability.

Standard Grade FeSi is used for bulk applications like DMS. High-Purity Grade, however, features significantly lower levels of trace elements (such as aluminum, carbon, and sulfur) and is required for specialized uses like high-quality welding electrodes, soft magnetic composites, and advanced powder metallurgy components where impurities negatively affect performance.

The Asia Pacific (APAC) region currently holds the largest market share, driven primarily by extensive, high-volume mining activities for iron ore and coal in countries such as China and India, coupled with substantial, sustained growth in the regional construction and steel manufacturing industries.

For achieving ultra-fine powders (Below 325 Mesh) required by advanced powder metallurgy, critical technologies include jet mills and highly efficient stirred media mills, coupled with advanced closed-circuit air classification systems that ensure precise particle size distribution and minimize batch variation.

In the welding industry, milled ferrosilicon is incorporated into the flux coatings of welding electrodes. It acts as a potent deoxidizer, removing oxygen from the molten weld pool, and as an alloying agent, enhancing the mechanical properties and strength of the deposited weld metal.

Environmental concerns drive demand for highly efficient DMS circuits that minimize water usage and maximize the recovery and recycling of the ferrosilicon medium. Additionally, manufacturers face increasing regulatory pressure regarding dust emissions during the milling process, prompting investments in cleaner, closed-loop processing technologies.

Yes, AI is impacting milling operations by enabling predictive maintenance for complex machinery, optimizing energy consumption in grinding processes, and using machine vision systems for real-time quality control checks on particle size uniformity, leading to improved throughput and reduced operational variance.

The upstream segment involves the sourcing of raw materials—high-purity quartz and iron scrap—and the energy-intensive process of smelting these materials in submerged arc furnaces to produce the primary bulk ferrosilicon alloy, which is the precursor to the milling phase.

The automotive industry, particularly the electric vehicle sector, utilizes ultra-fine, high-purity milled ferrosilicon in powder metallurgy applications to manufacture soft magnetic composite (SMC) cores for high-efficiency electric motors and various specialized components requiring precise magnetic and density properties.

Competitive advantage is primarily determined by the ability to consistently produce high-quality, uniform particle sizes across various mesh requirements, secure stable and cost-effective raw material supplies, achieve superior energy efficiency in the milling process, and provide comprehensive technical support to large-scale industrial customers globally.

Purity is critical in applications like powder metallurgy and specialized welding because trace elements such as phosphorus, sulfur, and carbon can severely degrade the material performance, leading to structural weaknesses, reduced magnetic permeability, or undesirable porosity in the final component or weldment.

Yes, one of the primary advantages of milled ferrosilicon in DMS is its high magnetic susceptibility, which allows for efficient, near-total recovery from the dense medium circuit using strong magnetic separators, minimizing operational losses and making it highly cost-effective and recyclable.

Key restraints include the volatile cost and secure supply of raw materials (silicon metal), the high capital expenditure required for establishing precision milling facilities, and the significant energy costs associated with the mechanical grinding and classification processes essential for product generation.

High-volume sales to major mining corporations and large steel mills typically use direct distribution channels for optimized logistics. Smaller volumes required by welding electrode manufacturers or specialized powder metallurgy firms often rely on indirect distribution through regional agents and specialized industrial distributors who manage localized inventory and technical sales.

Customized Grades refer to ferrosilicon powders manufactured with specific, non-standard silicon contents, mesh size distributions, or tailored impurity levels designed to meet highly specific, proprietary requirements of certain end-users in niche chemical, magnetic, or metallurgical processes where standard grades are insufficient for optimal performance outcomes.

Milled Ferrosilicon DMS is crucial for separating a wide range of materials, including iron ore (beneficiation), coal (upgrading), and non-ferrous metals such as manganese, lead, and zinc ores, particularly where the density difference between the mineral and the gangue material is suitable for heavy media processing.

The Milled Ferrosilicon Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between the forecast period of 2026 and 2033, driven by sustained industrial demand and advancements in mineral processing technologies globally.

The global increase in infrastructure and heavy construction projects mandates higher volumes of structural steel production. This directly boosts the demand for high-quality iron ore (which requires DMS) and increases the consumption of ferrosilicon as a critical deoxidizing and alloying additive in steel manufacturing, creating a robust, indirect market driver.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.