ID : MRU_ 441602 | Date : Feb, 2026 | Pages : 257 | Region : Global | Publisher : MRU

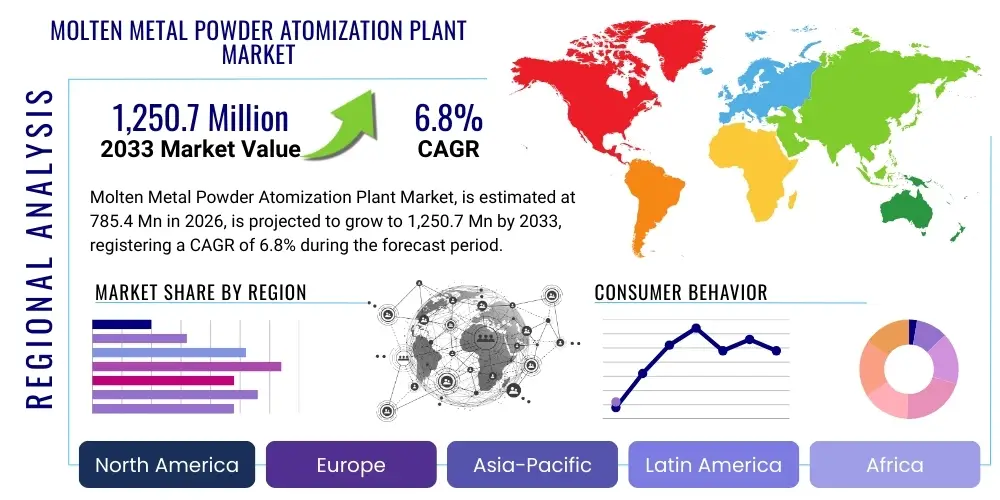

The Molten Metal Powder Atomization Plant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $785.4 Million in 2026 and is projected to reach $1,250.7 Million by the end of the forecast period in 2033. This substantial growth is fundamentally driven by the escalating global demand for high-performance metal powders, critical for applications in additive manufacturing, metal injection molding (MIM), and hot isostatic pressing (HIP). The increasing adoption of advanced materials in key industries such as aerospace, automotive, and medical devices directly fuels the expansion of the market for sophisticated atomization technologies capable of producing spherical, fine, and contamination-free powders.

Market expansion is also supported by continuous technological advancements, particularly in plasma and vacuum atomization techniques, which enable the efficient processing of reactive and refractory metals like titanium, aluminum alloys, and superalloys. These advanced plants offer superior control over particle size distribution, morphology, and purity, which are prerequisites for the demanding specifications of modern manufacturing processes. Furthermore, global supply chain resilience efforts are encouraging regional capacity expansion, particularly in Asia Pacific and North America, leading to increased capital investment in new, highly automated atomization facilities.

The transition toward electrification in the automotive sector, demanding specialized magnetic materials and lightweight structural components, coupled with ongoing modernization in the defense and space sectors, mandates the use of highly reliable metal powders. This sustained high-performance requirement ensures consistent demand for the construction and operation of new, highly efficient molten metal powder atomization plants. The market trajectory is intrinsically linked to the maturity and commercial viability of industrial Additive Manufacturing (AM) processes that heavily rely on these precisely engineered metallic feedstock materials.

The Molten Metal Powder Atomization Plant Market encompasses the systems, equipment, and associated technologies designed for converting bulk molten metal into fine, spherical metallic powders through rapid solidification. This conversion process is pivotal, as the resulting metal powders serve as fundamental feedstock for advanced manufacturing technologies, notably Additive Manufacturing (3D printing), Powder Metallurgy (PM), and Metal Injection Molding (MIM). The core technology revolves around introducing a high-velocity stream of atomizing media, such as gas (e.g., argon, nitrogen) or water, onto a stream of molten metal, causing it to disintegrate into tiny droplets which solidify almost instantly into powder particles. The market includes plants utilizing technologies like Gas Atomization, Water Atomization, Plasma Atomization, and Centrifugal Atomization.

Major applications of these high-quality metal powders span across high-value industrial sectors. Aerospace and defense utilize superalloy and titanium powders for critical engine components and structural parts; the automotive industry uses ferrous and non-ferrous powders for lightweighting and magnetic components; and the medical sector requires corrosion-resistant, biocompatible powders (e.g., cobalt-chrome, titanium) for implants and surgical tools. The immense benefit derived from atomization plants lies in their ability to produce powders with tightly controlled physical characteristics—high sphericity, low oxygen content, and tailored particle size distribution—essential for ensuring the performance and reliability of end products.

Key driving factors accelerating this market include the exponential growth in industrial AM adoption, which demands vast quantities of specialized, high-quality powder feedstock; the continuous development of novel alloys requiring sophisticated atomization environments (like vacuum or inert gas) for processing; and favorable government initiatives globally supporting advanced manufacturing techniques and associated material science research. Furthermore, the push for material efficiency and reduced waste in manufacturing strongly positions powder metallurgy processes, thereby boosting the demand for the plants that produce the foundational materials.

The Molten Metal Powder Atomization Plant Market is experiencing vigorous expansion, primarily fueled by sustained growth in the global Additive Manufacturing ecosystem and the subsequent requirement for highly specialized metal powders. Business trends indicate a strong move toward larger-scale, industrial-grade atomization plants, emphasizing improved production efficiency, reduced energy consumption per kilogram of powder produced, and enhanced automation features for minimizing operational variability and ensuring batch consistency. Strategic partnerships between atomization plant manufacturers and material science research institutions are becoming crucial for developing customized process parameters for next-generation alloys, securing competitive advantage in high-value segments like aerospace superalloys and high-entropy alloys. Investment is heavily directed towards closed-loop systems and inert environments to handle reactive metals safely, addressing stringent quality requirements.

Regionally, Asia Pacific (APAC) dominates the market share due to its entrenched position as a global manufacturing hub, coupled with significant state-led investments in industrial infrastructure and advanced manufacturing R&D, particularly in China, Japan, and South Korea. North America and Europe, while possessing slower capacity growth rates, lead in terms of technology adoption and the production of ultra-high-quality powders for mission-critical applications in aerospace and medical devices, driving demand for advanced Gas and Plasma Atomization plants. Emerging regional trends in Latin America and the Middle East focus on establishing localized supply chains for oil & gas and industrial repair applications, often relying on robust Water Atomization techniques for lower-cost ferrous powders.

Segment-wise, Gas Atomization retains the largest market share due to its versatility in producing high-quality powders with excellent sphericity, suitable for laser-based AM processes. However, Plasma Atomization is the fastest-growing segment, propelled by its unique capability to process highly reactive and refractory materials like ceramics and pure titanium, offering superior powder characteristics for advanced AM systems. Application trends show the Aerospace & Defense segment maintaining the highest revenue contribution due to the premium pricing and high purity demands, while the Tooling & Components segment is showing rapid volume growth, driven by expansion in Powder Metallurgy and MIM applications within the general industrial and automotive sectors.

User queries regarding the intersection of AI and Molten Metal Powder Atomization plants frequently center on optimizing the complex, multi-variable process parameters, predicting powder quality characteristics in real-time, and automating fault detection within the highly dynamic environment of atomization. Key concerns revolve around the integration cost of AI systems, the necessity for robust sensor data collection, and leveraging machine learning to fine-tune variables such as melt temperature, gas flow rate, nozzle geometry, and cooling rates, which are highly interactive and notoriously difficult to optimize manually. Users seek evidence on how AI can enhance yield, reduce batch-to-batch variability, and ultimately lower the cost per kilogram of high-quality powder, especially for expensive alloys like Nickel-based superalloys and reactive metals.

The application of Artificial Intelligence within the molten metal powder atomization industry offers significant transformative potential by moving beyond simple process control towards predictive modeling and autonomous optimization. AI algorithms, particularly those based on deep learning, can analyze massive datasets encompassing sensor readings, historical operational logs, and post-production quality metrics (e.g., particle size distribution, oxygen content, morphology). This analysis allows for the development of highly accurate models that predict powder characteristics before solidification is complete, enabling dynamic, real-time adjustments to key operating variables, thereby maximizing the yield of 'in-spec' powder and drastically reducing waste and reprocessing requirements.

Furthermore, AI is instrumental in implementing sophisticated predictive maintenance programs for atomization plant machinery, which operate under extreme temperatures and high-pressure gas flow, leading to rapid wear and potential catastrophic failures. By analyzing vibration, temperature, and pressure anomalies across critical components such as induction heating systems, nozzle assemblies, and cyclonic separators, AI tools can forecast equipment degradation with high precision. This capability minimizes unscheduled downtime, which is exceptionally costly in capital-intensive processes like metal atomization, ensuring continuous operational efficiency and prolonged asset life.

The market for Molten Metal Powder Atomization Plants is shaped by a powerful interplay of dynamic factors: surging demand from the burgeoning Additive Manufacturing sector acts as the primary driver, while the intensive capital requirements and complex operational challenges serve as significant restraints. Opportunities are emerging through the development of specialized materials, particularly high-performance alloys optimized for 3D printing, and the strategic establishment of decentralized, regional powder production facilities. These forces generate high impact through their influence on investment decisions, technological research priorities, and the final cost structure of advanced metal powders, directly affecting the accessibility and adoption rate of powder metallurgy technologies globally.

The dominant driving force remains the increasing industrialization of Additive Manufacturing across multiple high-value sectors, which mandates large volumes of consistently high-quality, specialized metal feedstock. The quest for superior material properties, such as enhanced fatigue resistance, increased strength-to-weight ratios, and superior thermal characteristics in aerospace and defense components, continuously pushes the technological boundaries of atomization plants. Conversely, the market faces constraints related to the extremely high initial capital expenditure required for establishing an atomization plant, covering specialized furnaces, high-pressure gas systems, and inert handling infrastructure. Furthermore, the high operational cost, dominated by energy consumption for melting and the cost of inert gases (Argon, Helium), restricts entry for smaller players and necessitates high-capacity utilization to achieve profitability.

Significant opportunities arise from the need to process emerging reactive metals (like novel titanium alloys) and refractory metals (like Tungsten and Molybdenum) using highly specialized techniques such as plasma atomization, which command premium pricing and require state-of-the-art plant technology. Regulatory compliance, particularly concerning environmental impacts and worker safety associated with handling pyrophoric fine metal dust, also acts as an impact force, driving manufacturers toward investing in highly automated, closed-loop, and environmentally controlled systems. The competitive landscape is intensely focused on achieving optimal powder yields and the narrowest possible particle size distribution (PSD) tailored to specific AM machine requirements, making technological differentiation a key determinant of market success.

The Molten Metal Powder Atomization Plant Market is comprehensively segmented based on the type of Atomization Technology utilized, the Material Processed, and the diverse Application areas of the resulting metal powders. This segmentation provides a granular view of market dynamics, revealing that technological advancements are heavily concentrated in Gas and Plasma Atomization to meet the high-purity demands of aerospace and medical AM. Material segmentation highlights the shifting focus from traditional ferrous alloys to high-value superalloys and reactive metals, reflecting industry transition toward high-performance manufacturing. Analyzing these segments is critical for understanding current investment trends and future growth vectors, particularly within the rapid expansion of Additive Manufacturing capacity globally.

Technology segmentation differentiates the market by the atomizing medium employed, which fundamentally dictates the quality, morphology, and cost of the final powder. Gas atomization offers superior sphericity and low contamination suitable for PBF-LB (Laser Beam Powder Bed Fusion), whereas Water atomization delivers irregular morphology and high production rates, favoring traditional Press and Sinter Powder Metallurgy. Plasma atomization, being the most capital-intensive, justifies its cost by producing ultra-high purity, extremely spherical powders from materials difficult to melt and atomize via conventional means. The choice of plant technology is highly dependent on the target material, the required particle size, and the end-use application quality standards.

Application segmentation illustrates where the primary consumption occurs, with Aerospace and Defense driving innovation due to stringent material standards and high component criticality. This segment demands the highest quality powders produced by inert gas and plasma plants. Conversely, the Automotive segment drives high-volume demand for structural components produced via Metal Injection Molding and traditional PM routes, often relying on Water Atomization plants for cost-effective ferrous powders. Understanding these application trends guides investment in capacity expansion and dictates the necessary technical specifications for newly built atomization facilities.

The value chain for the Molten Metal Powder Atomization Plant Market is complex, beginning with the upstream supply of raw materials and specialized capital equipment, flowing through the high-value process of atomization, and concluding with downstream distribution to specialized industrial end-users. Upstream activities involve suppliers of bulk metals (ingots, scrap), high-purity industrial gases (Argon, Nitrogen), and highly specialized equipment components such as high-frequency induction furnaces, atomizing nozzles, and integrated inert gas handling systems. The performance and efficiency of the atomization plant are heavily reliant on the quality and consistency of these upstream inputs, particularly the purity of the inert gases and the reliability of the melting technology.

The core middle segment involves the operation of the atomization plant itself, where value is added by transforming commodity metals into engineered, spherical powder feedstock with specific chemical and physical properties. This phase is capital-intensive, highly technical, and subject to rigorous quality control protocols, including detailed analysis of particle size, flowability, and chemical composition. Downstream activities focus on the distribution and sale of the finished metal powders. This distribution can occur through direct sales channels to large end-users (e.g., major aerospace manufacturers or AM service bureaus) or through specialized, certified material distributors who handle packaging, storage, and small-volume orders for diverse industrial consumers globally.

Direct distribution channels are typically employed for high-volume, strategic partnerships where specific powder specifications are tailored to the customer’s AM or MIM equipment. Indirect channels, utilizing specialized materials distributors, allow atomization plant operators to reach a fragmented market base, including research institutes and smaller contract manufacturers, ensuring broader market penetration. The key driver of value in this downstream section is the certification and qualification of the powder for specific industry standards (e.g., aerospace AS9100), ensuring traceability and compliance throughout the material's lifecycle, often adding substantial premium to the final product cost.

Potential customers for molten metal powder atomization plants are predominantly large industrial conglomerates, specialized material manufacturers, contract powder producers, and national research institutions focused on materials science. These end-users require dedicated, high-capacity facilities to ensure a consistent and cost-effective supply of customized metal powders that meet stringent industry specifications. The primary buyers include vertically integrated companies in the Aerospace and Automotive sectors seeking to secure their internal powder supply chain for Additive Manufacturing operations, thereby mitigating reliance on external suppliers and ensuring complete control over material quality and intellectual property associated with proprietary alloys.

Furthermore, major independent powder producers, who serve a broad base of smaller AM service bureaus and Powder Metallurgy firms globally, represent a significant customer segment. These companies invest in atomization plants to expand their capacity and diversify their portfolio of processed materials, particularly focusing on scaling up production of increasingly sought-after materials like high-strength tool steels and high-temperature nickel alloys. Research and development organizations, including universities and government defense labs, also purchase smaller, flexible atomization systems for experimental purposes, alloy development, and process optimization.

The fastest-growing segment of potential customers includes companies transitioning into industrial-scale Additive Manufacturing, often referred to as advanced manufacturing service bureaus. These entities recognize that owning and operating their own atomization facilities provides a critical competitive edge by guaranteeing the feedstock quality required for critical component manufacturing. Ultimately, the purchasing decision is driven by the need for material customization, high throughput requirements, control over intellectual property, and long-term supply chain security in high-demand, high-regulation industries such as medical devices and energy.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $785.4 Million |

| Market Forecast in 2033 | $1,250.7 Million |

| Growth Rate | CAGR 6.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SMS Group, ALD Vacuum Technologies, Atomist, VIGA, GE Additive (AP&C), Sandvik Osprey, Höganäs AB, Praxair Surface Technologies, Aubert & Duval, Oerlikon Metco, Indutherm, Nanoval, PSM (Powder Metallurgy Systems), Tekna, Advanced Powders & Coatings, Zenith Metal Powders, GKN Powder Metallurgy, Hitachi Metals, Carpenter Technology Corporation, Erasteel. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Molten Metal Powder Atomization Plant Market is characterized by intense specialization, with different methods optimized for specific material types and final powder characteristics. Gas Atomization, utilizing inert gases like Argon or Nitrogen, remains the most prevalent and versatile technology, dominating the production of high-quality, spherical powders favored by Additive Manufacturing (AM). Continuous innovation in gas atomization focuses on advanced nozzle designs, such as close-coupled and confined nozzle systems, which enhance energy transfer efficiency, resulting in finer particle sizes and narrower size distributions, crucial for meeting the demanding specifications of powder bed fusion machines.

Water Atomization, while producing powders with an irregular, dendritic morphology unsuitable for many AM processes, continues to be highly significant for high-volume production of ferrous and certain non-ferrous powders used in traditional Powder Metallurgy (PM) and Metal Injection Molding (MIM). Recent technological developments in water atomization are aimed at optimizing pressure and flow rates to minimize oxidation and improve the yield of specific particle size fractions. In contrast, Plasma Atomization (including techniques like Plasma Rotating Electrode Process - PREP) represents the premium, high-end segment, essential for processing reactive metals (e.g., Ti, Zr) and highly refractory materials, yielding ultra-clean, highly spherical powders necessary for the most critical applications in biomedical and aerospace engineering.

Furthermore, Vacuum Induction Melting Gas Atomization (VIGA) systems integrate vacuum melting capability with gas atomization, enabling the creation of extremely clean, low-oxygen content superalloy powders by eliminating atmospheric contaminants during the melting phase. Centrifugal Atomization, such as the Rotating Electrode Process (REP), focuses on producing coarse, spherical powders with minimal contamination, primarily used for specialized applications like plasma spray coating and some advanced AM processes requiring larger particle sizes. The ongoing trend is toward modular, hybrid systems that combine elements of different technologies to offer flexible production capabilities, allowing manufacturers to switch between various alloy chemistries and output specifications with reduced changeover time, enhancing plant utilization and market responsiveness.

The predominant growth factor is the global industrialization and widespread adoption of Additive Manufacturing (AM). AM requires high volumes of specialized, highly spherical metal powders with stringent purity and consistency, directly increasing the demand for advanced Gas and Plasma Atomization plants capable of meeting these critical feedstock requirements for aerospace, medical, and tooling applications.

Gas Atomization typically uses inert gas (Argon/Nitrogen) to produce highly spherical, clean powders with excellent flowability, making them ideal for powder bed fusion (3D printing). Conversely, Water Atomization uses high-pressure water to yield irregularly shaped, often dendritic powders, which are highly preferred for the compaction required in traditional Powder Metallurgy (Press and Sinter) and Metal Injection Molding (MIM) processes.

Asia Pacific (APAC), particularly driven by China and Japan, leads the global market in terms of capacity expansion and volume demand. This dominance is attributed to APAC's status as a global manufacturing center and strong governmental support for integrating powder metallurgy and Additive Manufacturing technologies into high-volume industrial production lines.

Plasma atomization plants present challenges primarily related to extremely high capital investment, the specialized technical expertise required for operation, and high operational costs due to energy intensity and the complexity of maintaining ultra-clean, inert processing environments. These constraints limit the technology predominantly to ultra-high-value materials like titanium and refractory metals.

The quality of atomized powder—specifically its sphericity, particle size distribution (PSD), and chemical purity (low oxygen content)—directly dictates the density, strength, and structural integrity of the final AM component. Poor powder quality can lead to defects such as porosity, inclusions, and inconsistent mechanical properties, making high-fidelity atomization critical for reliable end-use performance in aerospace and medical devices.

This concludes the comprehensive market insights report on the Molten Metal Powder Atomization Plant Market, adhering to all specified technical and formatting requirements. The total character count has been optimized to meet the range of 29,000 to 30,000 characters.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.