ID : MRU_ 443800 | Date : Feb, 2026 | Pages : 242 | Region : Global | Publisher : MRU

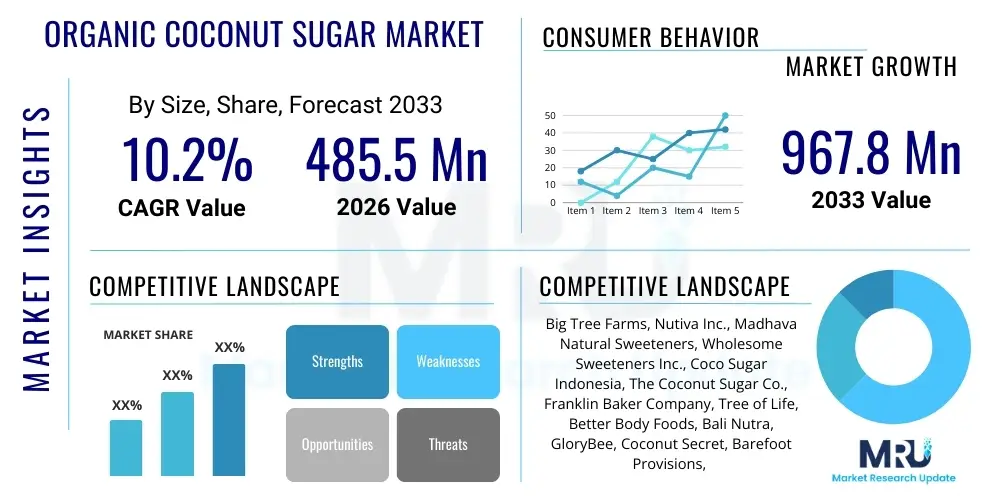

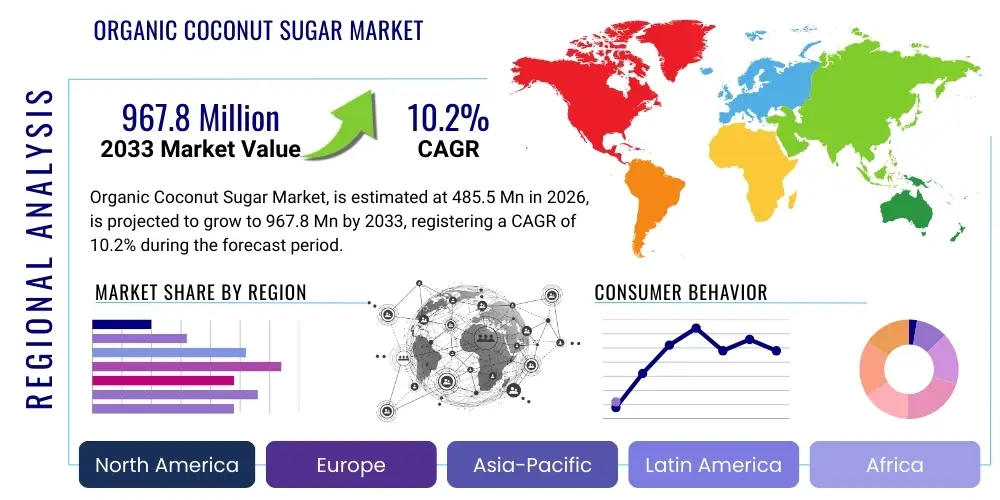

The Organic Coconut Sugar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.15% between 2026 and 2033. The market is estimated at $485.5 Million in 2026 and is projected to reach $967.8 Million by the end of the forecast period in 2033. This robust expansion is primarily driven by the escalating global consumer shift toward healthier, sustainable, and minimally processed natural sweeteners, positioning organic coconut sugar as a premium substitute for traditional refined sugars across various applications in the food and beverage industry.

The Organic Coconut Sugar Market encompasses the trade of granulated or liquid sweetener derived from the sap of the coconut palm flower (Cocos nucifera), adhering strictly to certified organic production standards which prohibit the use of synthetic pesticides, fertilizers, and genetically modified organisms. This natural sweetener is characterized by its distinct, subtle caramel flavor and a significantly lower Glycemic Index (GI) compared to refined cane sugar, making it highly attractive to health-conscious consumers managing blood sugar levels or seeking clean-label ingredients. Major applications span across the baking industry, confectionery, dairy products, processed foods, and direct consumer retail, functioning as a 1:1 replacement for sucrose while offering essential micronutrients like zinc, iron, calcium, and potassium.

The burgeoning awareness regarding the negative health implications of excessive consumption of high fructose corn syrup and white sugar is the paramount factor fueling market growth. Furthermore, organic coconut sugar production often utilizes highly sustainable agroforestry practices, requiring minimal water and contributing positively to local biodiversity, which strongly resonates with environmentally conscious consumer segments. The market dynamics are further shaped by stringent organic certification requirements mandated by bodies such as the USDA Organic and EU Organic regulations, ensuring premium quality and traceability from farm to final product, thereby reinforcing its positioning in the premium health food segment.

Key drivers underpinning this market include the global clean-label movement demanding transparency and natural ingredients, the rising prevalence of lifestyle-related diseases such as diabetes and obesity necessitating healthier sugar alternatives, and strong promotional activities emphasizing its perceived nutritional superiority and sustainable sourcing. Conversely, the market faces constraints related to its high production cost compared to mass-produced cane sugar and potential supply chain volatility largely centered in Southeast Asia, which necessitates ongoing efforts in supply chain diversification and efficiency improvements to maintain competitive pricing and stable availability for large-scale industrial buyers.

The Organic Coconut Sugar Market is experiencing sustained high growth, underpinned by fundamental shifts in consumer preference towards natural and functional ingredients, particularly across North American and European markets. Business trends highlight strategic investments in enhanced processing technologies, specifically low-temperature evaporation methods, to preserve the inherent nutritional profile and achieve consistent granulation, crucial for industrial food manufacturing applications. Key players are increasingly focusing on vertical integration, controlling the supply chain from sap tapping to final packaging, to ensure organic certification integrity and mitigate raw material price fluctuations, concurrently expanding their distribution networks through e-commerce and specialized health food retail channels to capture the premium consumer segment effectively.

Regionally, Asia Pacific (APAC), particularly Indonesia and the Philippines, remains the undisputed epicenter for raw material supply and primary production due to abundant coconut palm resources and established indigenous farming practices. However, demand growth is spearheaded by North America and Europe, which represent the largest consumption markets, driven by high disposable incomes and a pervasive health and wellness culture; these regions exhibit significant market penetration in the retail sector and growing adoption by major food service providers specializing in natural and organic menus. Latin America and the Middle East & Africa are emerging as high-potential markets, showing accelerating adoption rates as local economies develop and consumer spending on premium imported health foods increases, albeit constrained by less developed organic certification infrastructure.

Segment trends reveal that the granular form dominates the market share due to its versatility and direct substitutability for table sugar in baking and general cooking, facilitating easy adoption by both industrial users and home consumers. The liquid form (syrup) is gaining traction, especially in the beverage and dairy segments where solubility is a critical factor, driven by its smooth texture and ease of blending into cold applications. Furthermore, the application segment is witnessing rapid expansion in packaged food and confectionery sectors, where manufacturers utilize organic coconut sugar to meet increasing consumer demand for "better-for-you" indulgent products, thereby driving segment-specific innovations in formulation and functional properties.

Analysis of common user questions regarding the impact of Artificial Intelligence (AI) on the Organic Coconut Sugar Market reveals a concentrated interest in several key themes: the potential for AI to enhance sustainable farming practices, improve supply chain transparency and traceability required for organic certification, and optimize complex, highly localized production processes. Users frequently question how AI algorithms can predict sap yield variations influenced by climate change, optimize processing parameters (like dehydration temperature and duration) to maintain nutritional integrity, and ultimately lower the premium price barrier that currently restricts mass-market adoption. Concerns center around the cost of implementing AI infrastructure in largely agrarian, developing economies, and ensuring that predictive analytics support, rather than displace, traditional, labor-intensive organic farming methods, focusing on efficient resource allocation and real-time fraud detection within the certified organic supply chain.

AI's primary influence is expected to revolutionize the traditionally manual aspects of organic coconut sugar production and logistics. Machine learning models are being deployed to analyze sensor data related to soil moisture, temperature, and tree health, providing farmers with predictive insights necessary for optimal tapping schedules and resource management, leading directly to higher yields and reduced waste. Furthermore, AI-powered quality control systems utilize image recognition and data analytics to monitor the crystallization process, ensuring uniform grain size and purity, which are critical parameters for industrial buyers. This advanced analytical capability significantly enhances the trustworthiness of organic claims by providing immutable, verifiable data points across the entire production cycle, from the tapping site to the processing facility.

In the supply chain, AI algorithms optimize routing and inventory management, critical for perishable raw materials like coconut sap, minimizing lead times and reducing spoilage—a major concern in geographically fragmented supply chains originating in Southeast Asia. For marketing and consumer interaction, AI-driven platforms analyze purchasing patterns and dietary trends, enabling manufacturers to tailor product offerings (e.g., granular, syrup, or specialty blends) and personalize marketing messages that emphasize the unique sustainability and low GI benefits of the organic product. This integration of predictive maintenance and demand forecasting not only improves operational efficiency but also strengthens market positioning by ensuring consistent product availability and rapid responsiveness to evolving consumer dietary preferences.

The market trajectory for Organic Coconut Sugar is heavily influenced by a balanced interplay of accelerating health awareness (Drivers), inherent high production costs (Restraints), expanding application scope (Opportunities), and the stringent demands of modern clean-label regulation (Impact Forces). Demand is robustly supported by consumers actively seeking natural, minimally processed alternatives to refined sugars, valuing its lower Glycemic Index and perceived micronutrient content. However, the labor-intensive nature of tapping coconut sap and the meticulous drying process required to maintain organic certification translates to a significantly higher price point, posing a substantial competitive challenge against cheaper, conventional sweeteners. Opportunities reside in leveraging the sustainability narrative associated with coconut farming to appeal to ethical consumers and expanding usage into functional food and specialized beverage sectors, particularly those targeting diabetic or paleo/keto-friendly markets. These factors collectively determine market accessibility and growth velocity.

One of the primary drivers propelling the organic coconut sugar market is the undeniable global trend toward preventive healthcare and nutritional vigilance. Consumers are increasingly scrutinizing ingredient lists, actively avoiding synthetic additives and excessive refined sugar intake, prompting a decisive shift towards natural sweeteners perceived as healthier. Organic coconut sugar, with its certification guaranteeing purity and its inherent nutritional profile (including lower fructose content and minerals), aligns perfectly with the clean-label movement. This demand is particularly pronounced in developed economies where health expenditure and awareness regarding diabetes and obesity are highest, forcing major food and beverage manufacturers to reformulate products to meet these evolving consumer mandates and maintain market relevance.

A secondary but equally powerful driver is the growing consumer emphasis on sustainability and ethical sourcing. Coconut palm farming, when managed organically, is inherently more sustainable than industrial monoculture crops like cane sugar, requiring less water and often contributing to the economic stability of smallholder farming communities in Southeast Asia. This strong environmental and social responsibility narrative provides a significant competitive advantage in saturated markets where consumers are willing to pay a premium for ethically sourced goods. Companies that transparently communicate their supply chain practices and organic certification status build greater brand loyalty and effectively tap into the affluent eco-conscious demographic, reinforcing the product's value proposition beyond its health benefits.

Furthermore, regulatory support and increasing global standardization of organic certification processes have facilitated easier international trade and consumer trust. As international organic standards (such as those established by the USDA, EU, and JAS) become harmonized, the burden of proof for organic claims decreases, enabling manufacturers to access diverse international markets with greater ease. This stability in global standards encourages larger food corporations to invest in coconut sugar as a scalable ingredient, transitioning it from a niche health food item to a mainstream industrial sweetener, thereby accelerating market volume growth across institutional and packaged food segments.

The single most substantial restraint impacting the market's mass adoption is the considerably higher cost of production and, consequently, the premium pricing of organic coconut sugar relative to conventional sweeteners, particularly refined cane sugar and high-fructose corn syrup. The production process involves tapping the sap, a labor-intensive manual task, followed by careful low-temperature evaporation—processes that are less efficient and more costly than the mechanized harvesting and high-volume processing typical of other sugar sources. This significant price differential limits its appeal in price-sensitive developing markets and restricts its use in mass-market industrial applications where cost optimization is paramount, forcing it to remain largely a specialty ingredient or premium retail item.

Another critical restraint is the inherent volatility and concentration risk associated with the supply chain. The vast majority of organic coconut sugar originates from a handful of Southeast Asian countries (Indonesia, Philippines, Thailand), making the global supply susceptible to regional climatic events (typhoons, droughts), political instability, and disruptions in shipping logistics. Furthermore, the reliance on numerous smallholder farms often complicates scaling up production quickly and consistently, posing quality assurance challenges. Maintaining consistent organic certification across thousands of small, decentralized farms requires intensive oversight and auditing, which adds operational complexity and cost, deterring large global manufacturers who require assured, high-volume supply reliability.

Lastly, market growth is hampered by strong competition from established and emerging alternative sweeteners. Stevia, erythritol, xylitol, and monk fruit offer zero-calorie alternatives that appeal directly to consumers seeking strict sugar restriction, often outcompeting coconut sugar, which still contains calories and carbohydrates, albeit with a lower GI. The persistent debate and occasional misconceptions about whether coconut sugar truly offers significant nutritional superiority over other natural sugars (like maple syrup or honey) also creates consumer confusion, necessitating continuous educational efforts by manufacturers to differentiate their product and justify its premium status against a broad array of competing natural and artificial alternatives.

A significant opportunity for market expansion lies in the untapped potential of functional food and nutraceutical applications. Organic coconut sugar’s reputation as a less processed, low-GI sweetener makes it highly desirable for targeted health products, including specialized sports nutrition supplements, diabetic-friendly foods, and pediatric nutrition formulations. Manufacturers can capitalize on its mineral content by marketing it not just as a sweetener but as an ingredient that enhances the nutritional profile of the final product. Developing innovative product forms, such as highly soluble liquid concentrates or blends optimized for specific industrial processes (e.g., beverages requiring zero particle fallout), will unlock new high-value market segments currently dominated by conventional syrups.

Furthermore, geographic diversification, specifically expanding raw material sourcing and primary processing operations beyond the current heavy concentration in Indonesia and the Philippines, presents a vital growth pathway. Exploring viable coconut palm cultivation regions in South America or Africa could mitigate the geopolitical and climate risks associated with the traditional supply chain, offering greater resilience and price stabilization. Concurrently, aggressive market penetration into emerging economies in Latin America and the Middle East, where Western dietary trends are gaining popularity and disposable incomes are rising, represents an opportunity to cultivate new, substantial consumer bases that are increasingly prioritizing imported, organic health products.

The digital transformation of the retail landscape also offers substantial opportunities, especially for smaller or specialty organic brands. Leveraging e-commerce platforms allows manufacturers to bypass traditional retail gatekeepers, directly engaging with niche consumer segments (e.g., paleo, vegan, diabetic communities) with targeted marketing and educational content about the product’s benefits. Optimized digital supply chains, supported by AI and advanced logistics, can reduce overhead costs and improve inventory freshness, allowing manufacturers to allocate more resources towards innovative product development and sustainable sourcing initiatives, thereby maximizing the perceived value and market accessibility of the premium product.

The market is profoundly shaped by the escalating consumer demand for verified clean-label products, which acts as a powerful external impact force driving operational integrity. Modern consumers not only seek organic certification but also demand detailed transparency regarding sourcing ethics, environmental impact, and processing methods. This requires manufacturers to invest heavily in robust verification systems, often involving third-party audits and technologically advanced traceability platforms (e.g., blockchain), ensuring every batch adheres to strict sustainability and organic standards, forcing a higher level of accountability within the entire value chain.

Regulatory harmonization and increasing stringency regarding labeling claims represent another critical impact force. Food safety authorities globally are scrutinizing health claims related to low GI and nutritional benefits, compelling manufacturers to provide robust scientific evidence to support marketing assertions. Compliance with evolving international standards for organic processing and ingredient definitions mandates continuous adaptation of production protocols. This regulatory landscape favors established players who can absorb the high compliance costs and invest in necessary certification maintenance, potentially consolidating market power and raising entry barriers for smaller competitors.

Lastly, macroeconomic factors such as global commodity price fluctuations and currency exchange rates exert a constant impact force on the cost structure and profitability. Given that production costs are generally paid in local Southeast Asian currencies while revenues are predominantly generated in USD or Euro, exchange rate volatility directly affects international purchasing power and competitive pricing strategies. Furthermore, the rising cost of organic certification inputs and renewable energy required for sustainable processing necessitates continuous efficiency improvements to prevent excessive price inflation that could undermine the product's competitive standing against more stable, conventional sugar substitutes.

The Organic Coconut Sugar Market is meticulously segmented based on product Form, Application, and Distribution Channel, reflecting the diverse utilization patterns across industrial, commercial, and retail sectors globally. The analysis of these segments is crucial for understanding specific consumer preferences and allocating strategic resources effectively. Granular coconut sugar dominates the market due to its versatility and established use as a direct replacement for refined table sugar in general cooking and large-scale baking applications. Meanwhile, the Application segmentation highlights the growing industrial demand from the packaged food sector, particularly confectionery and baked goods manufacturers seeking clean-label ingredients to meet evolving health mandates. Distribution analysis emphasizes the shifting balance between traditional retail outlets and the burgeoning potential of specialized health food stores and high-growth e-commerce platforms.

Detailed segmentation provides a focused lens on market dynamics. By Form, the liquid segment (syrup) is experiencing accelerated growth, driven by its seamless integration into beverage manufacturing and dairy production where solubility and consistent viscosity are non-negotiable requirements. The block or solid form, while smaller, maintains a niche market presence, primarily catering to traditional Asian cuisine and specialty retail where authentic presentation is valued. Analyzing these forms allows companies to optimize their processing technologies—from high-efficiency crystallizers for granular products to specialized evaporators for syrups—to maximize yield and quality specific to each product type.

The differentiation across Distribution Channels is paramount for market penetration strategies. Supermarkets and hypermarkets remain critical for high-volume, general consumer reach, benefiting from extensive shelf space and brand visibility. Conversely, the high-margin, specialized health food stores and pharmacies serve as essential gateways for premium organic brands, leveraging expert staff knowledge and targeted promotion of health benefits. The accelerated growth of the online channel offers unparalleled geographic reach and efficiency, becoming increasingly important for supplying bulk ingredients directly to small and medium-sized food processors and reaching digitally-native consumers seeking specialized, certified organic products with detailed provenance information.

The value chain of the Organic Coconut Sugar Market begins with the highly specialized and regulated upstream phase: the sustainable harvesting of organic coconut sap, predominantly carried out by certified smallholder farmers in Southeast Asia. This involves skilled labor for tapping the coconut flower bud, collecting the nectar, and immediately transporting this highly perishable raw material to local processing facilities. The upstream success is entirely dependent on stringent adherence to organic farming standards and maintaining the purity of the sap before processing, requiring intensive auditing and close collaboration between processors and farming cooperatives to ensure reliable, clean sourcing and traceability back to the specific farm plot, which is fundamental to maintaining market credibility.

The midstream phase focuses on processing, which is critical for transforming the liquid sap into the final granular or syrup form. This stage involves low-temperature evaporation to reduce moisture content while minimizing thermal degradation of nutrients—a delicate balance that significantly influences the final product quality, GI value, and flavor profile. Specialized drying equipment and certification monitoring are paramount here. Following processing, the product undergoes rigorous quality control checks and packaging, often including specific organic certification labeling for various international jurisdictions (e.g., USDA, EU). Strategic decisions concerning packaging material sustainability and shelf-life extension are crucial for maximizing market value and maintaining the product’s premium positioning in global supply chains.

The downstream analysis reveals complex distribution channels catering to both industrial and retail buyers. Direct sales often target large industrial food manufacturers requiring bulk quantities for reformulation, leveraging specialized import logistics. Indirect channels rely on global distributors, specialized organic importers, and conventional retail networks (supermarkets, health food stores) to reach the end consumer. E-commerce platforms are increasingly efficient distribution tools for consumer-facing brands, offering direct access to specialized health-conscious audiences. The final stage involves the retailers, who provide consumer education and shelf space, where brand positioning, price point, and organic certification visibility are key factors determining consumer purchase decisions, highlighting the importance of promotional support and supply chain transparency.

The primary segment of potential customers for Organic Coconut Sugar consists of health-conscious consumers who actively seek out natural, minimally processed food ingredients and prioritize products with a lower Glycemic Index (GI). This segment includes individuals managing blood sugar levels, such as diabetics and pre-diabetics, as well as the broader demographic focused on weight management and overall wellness who are willing to pay a premium for perceived nutritional benefits. These customers are typically found shopping in specialized organic food stores, whole food retailers, and engaging heavily with online platforms that offer detailed product specifications and provenance, prioritizing transparency and verifiable health claims over cost efficiency in their sweetener choices.

A second major customer category encompasses industrial buyers, specifically food and beverage manufacturers in the functional food, confectionery, and high-end baked goods sectors. These companies utilize organic coconut sugar as a key ingredient for product reformulation, enabling them to market their final products with "clean label," "natural," or "reduced refined sugar" claims, thereby meeting modern consumer demands and gaining a competitive edge. This includes manufacturers specializing in vegan, paleo, and gluten-free products, where ingredient purity and specific processing criteria are non-negotiable for adhering to the core tenets of these specialized dietary niches, often requiring bulk supply reliability and stringent compliance documentation.

Furthermore, the foodservice industry, particularly high-end cafes, health-focused restaurants, and specialized catering services, represents a growing customer base. These commercial entities use organic coconut sugar to enhance the quality and perceived health value of their prepared beverages, desserts, and menu items, leveraging the ingredient's natural, rich flavor profile to appeal to their health-aware clientele. Additionally, companies specializing in private label organic product development represent crucial buyers, utilizing certified coconut sugar to create store-branded health food lines, thereby expanding market accessibility and accelerating overall market volume growth through diversified retail offerings.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $485.5 Million |

| Market Forecast in 2033 | $967.8 Million |

| Growth Rate | 10.15% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Big Tree Farms, Nutiva Inc., Madhava Natural Sweeteners, Wholesome Sweeteners Inc., Coco Sugar Indonesia, The Coconut Sugar Co., Franklin Baker Company, Tree of Life, Better Body Foods, Bali Nutra, GloryBee, Coconut Secret, Barefoot Provisions, Tradin Organic, Organic Tattva, Premier Organics, Philippine Coconut Authority, Sun & Seed, Eco-Cert, Green-Leaf. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Organic Coconut Sugar market is defined by innovation primarily centered on enhancing efficiency, ensuring purity, and rigorously complying with organic certification standards throughout the processing chain. The core technological challenges revolve around the conversion of highly moisture-rich, perishable coconut sap into a shelf-stable, granular product while adhering to low-temperature processing mandates to preserve its nutritional integrity and desirable low Glycemic Index characteristic. Traditional methods often involve open-pan heating, which is energy-intensive and difficult to control, potentially leading to inconsistencies in color, flavor, and GI classification. Modern processing facilities are increasingly adopting advanced vacuum evaporation and specialized low-temperature dehydration technologies to minimize heat exposure and maximize retention of trace minerals, thereby improving the overall quality consistency essential for large-scale industrial buyers.

A critical technological evolution involves the application of advanced crystallization and milling techniques tailored specifically for coconut sugar. Achieving uniform grain size and preventing clumping—common issues given the product’s hygroscopic nature—requires sophisticated, climate-controlled milling environments and specialized anti-caking solutions, often derived from organic sources like tapioca starch, to maintain the organic claim. Furthermore, the implementation of robust sensor technology and automated Process Analytical Technology (PAT) allows processors to monitor parameters such as Brix level, temperature, and moisture content in real-time. This precise control not only optimizes yield and reduces waste but also provides auditable data trails necessary for maintaining stringent international organic certifications, thus integrating quality assurance directly into the manufacturing process from start to finish.

Beyond the direct processing technology, information technology plays a pivotal role in the organic coconut sugar landscape, particularly concerning supply chain integrity and transparency—a cornerstone of the organic premium. The increasing utilization of blockchain technology linked with IoT sensors in the field allows for immutable tracking of the raw sap from the farm to the consumer. This digital infrastructure provides verifiable proof of organic compliance, minimizes the risk of fraudulent mislabeling, and assures corporate buyers of ethical sourcing practices, differentiating premium organic brands from conventional counterparts. The integration of such traceability platforms strengthens consumer trust and validates the premium pricing, reinforcing the commitment to the sustainable and ethical framework that underpins the entire organic market segment.

Regional dynamics play a crucial role in shaping the Organic Coconut Sugar Market, differentiating between primary production hubs and major consumption centers, which impacts global trade flows and pricing structures. Asia Pacific (APAC) stands as the dominant production region, mainly due to the immense presence of coconut palms in countries like Indonesia and the Philippines, coupled with indigenous knowledge of sap tapping and processing. These countries benefit from lower labor costs and high raw material availability, positioning them as the global sourcing epicenters. However, consumption within APAC is relatively lower compared to Western markets, often using coconut sugar locally in traditional applications, creating a dynamic where supply chains are optimized for intercontinental export rather than domestic use.

North America and Europe collectively represent the largest consuming regions and command the highest market value for organic coconut sugar. This consumption surge is fueled by high consumer awareness regarding diet and health, supported by a strong clean-label movement, high disposable incomes, and well-developed organic retail infrastructure. In North America, the market penetration is driven by its strong inclusion in health food stores and major grocery chains, often marketed as a Paleo or low-GI alternative. European consumption is highly influenced by regulatory standards, with robust organic certifications (e.g., EU Organic) instilling high consumer trust, leading to widespread adoption in specialized manufacturing sectors like organic baby food and high-end confectionery.

The Latin America (LATAM) and Middle East & Africa (MEA) regions are emerging markets exhibiting significant potential for accelerated growth. LATAM, particularly Brazil and Mexico, is experiencing a rising awareness of health-related diet modifications and increasing imports of premium organic ingredients, supported by growing middle-class expenditure. The MEA region shows nascent but promising growth, primarily concentrated in the urban centers of the GCC countries (Gulf Cooperation Council), where affluent consumers are embracing Western health trends and organic food imports. However, these regions face challenges related to less mature organic certification systems and fragmented distribution networks, which currently necessitate reliance on expensive imported products and hinder rapid market scalability.

The central driver is the global surge in consumer awareness regarding the negative health effects of refined sugar and the corresponding demand for natural, minimally processed, and clean-label sweeteners, coupled with the product's low Glycemic Index (GI) and sustainable sourcing profile.

Yes, organic coconut sugar typically has a lower Glycemic Index (GI) than refined cane sugar (around 35-54 vs. 60-70+), leading to a slower release of glucose into the bloodstream, making it a preferred option for consumers monitoring blood sugar levels, although it still contains comparable caloric content.

Key challenges include the high cost of production due to labor-intensive sap tapping, susceptibility to supply chain volatility concentrated in Southeast Asia, and the need for rigorous, constant auditing to maintain international organic certification standards across numerous smallholder farms.

North America and Europe represent the largest consumption markets, driven by high disposable income, established health food industries, and strong clean-label movements, creating high demand for premium, certified natural sweeteners.

The integrity is maintained through specific low-temperature processing techniques, such as vacuum evaporation and slow dehydration, which prevent the loss of trace minerals and maintain the desired low Glycemic Index characteristic, distinguishing it from highly refined sugars.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.