ID : MRU_ 441960 | Date : Feb, 2026 | Pages : 249 | Region : Global | Publisher : MRU

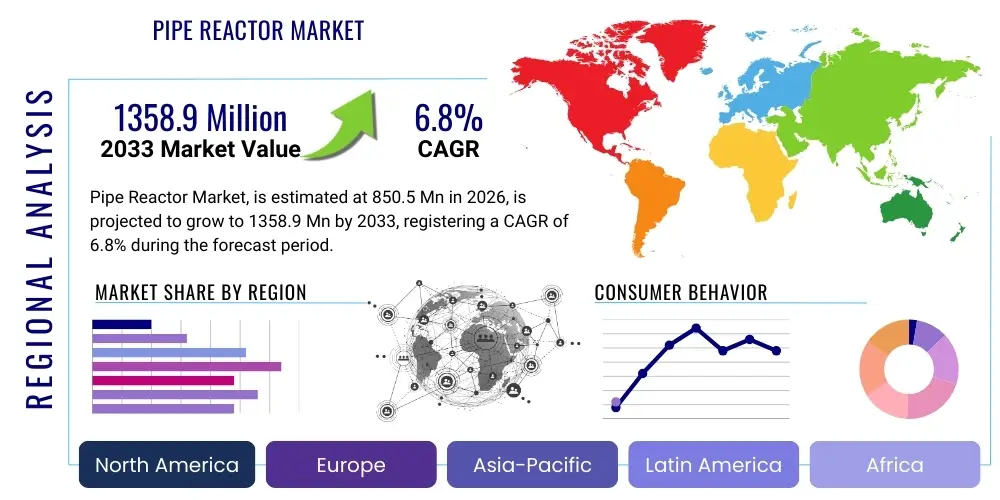

The Pipe Reactor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 850.5 Million in 2026 and is projected to reach USD 1358.9 Million by the end of the forecast period in 2033.

The Pipe Reactor Market encompasses specialized tubular reaction systems primarily utilized in the chemical process industry (CPI) for efficient, continuous-flow chemical synthesis. These reactors, characterized by their high surface-area-to-volume ratio and precise control over reaction parameters, are essential for processes requiring intense mixing, rapid heat dissipation, or operation under harsh conditions such as high pressure or temperature. Unlike traditional stirred tank reactors, pipe reactors facilitate plug-flow characteristics, ensuring uniform residence time distribution and significantly improving product consistency and yield in fast exothermic reactions. The fundamental design leverages the piping infrastructure itself as the primary reaction vessel, enabling streamlined, modular, and often more cost-effective installations compared to conventional large-scale reactors.

Major applications for pipe reactors span the manufacturing of high-value chemical products, including fertilizers (particularly ammonium phosphate and ammonium polyphosphate production), petrochemical intermediates, polymers, and various specialty chemicals. In the agricultural sector, the precision offered by pipe reactors minimizes side reactions and maximizes nutrient concentration in complex fertilizer formulations, directly contributing to improved agricultural productivity. Furthermore, the inherent safety profile associated with smaller inventories and reduced risk of thermal runaway makes them preferred choices in high-risk chemical environments. The adoption of these reactors is heavily influenced by stringent environmental regulations requiring enhanced process efficiency and waste minimization, pushing manufacturers toward continuous processing technologies.

Key benefits driving market adoption include enhanced operational safety due to smaller working volumes, superior process control leading to higher selectivity and product purity, and reduced energy consumption compared to batch processes. The driving factors primarily revolve around the global shift toward continuous manufacturing practices, especially in industries striving for Industry 4.0 compliance. Increasing demand for concentrated and high-quality fertilizers in emerging economies, coupled with significant investments in green chemistry and sustainable chemical production methods, further fuels the expansion of the Pipe Reactor Market globally. Technological advancements in computational fluid dynamics (CFD) modeling allow for highly optimized reactor designs, promising even greater efficiency gains in the foreseeable future.

The global Pipe Reactor Market is experiencing robust expansion, driven primarily by the transition from conventional batch processing to highly efficient continuous manufacturing across critical industrial sectors such as agrochemicals and specialty chemicals. Business trends indicate a strong focus on modularization and digitalization, with leading companies investing heavily in smart sensor integration and advanced control systems to optimize reaction kinetics and ensure real-time quality monitoring. There is a noticeable shift towards employing advanced materials, including exotic alloys and high-performance polymers, to withstand increasingly aggressive reaction chemistries, enhancing the longevity and operational window of the reactors. Strategic partnerships between engineering firms and end-users are becoming common, facilitating custom-designed reactor solutions that precisely meet specific production requirements and scalability challenges.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, fueled by rapid industrialization, massive infrastructure development in the chemical and fertilizer sectors, particularly in China and India, and increasing governmental support for high-efficiency manufacturing technologies. North America and Europe maintain significant market shares, characterized by early adoption of sophisticated continuous processing and stringent regulatory environments that favor the safety and environmental benefits inherent in pipe reactor technology. The market in Latin America and the Middle East & Africa (MEA) is poised for substantial growth, driven by investments in domestic petrochemical processing capabilities aimed at reducing reliance on imported intermediates, necessitating modern, reliable reaction equipment.

Segment trends reveal that the application segment focused on fertilizer production dominates the market, largely due to the widespread use of pipe reactors in producing highly concentrated fertilizers like Diammonium Phosphate (DAP) and Monoammonium Phosphate (MAP). In terms of reactor material, stainless steel remains the workhorse material, balancing cost-effectiveness with corrosion resistance, although high-nickel alloys and non-metallic options are seeing accelerated growth in highly corrosive environments typical of fine chemical synthesis. Continuous flow operation is the overwhelming preference across all major segments, underscoring the market's trajectory towards maximizing throughput and operational consistency, thereby ensuring high commercial returns on investment.

User queries regarding AI's influence on the Pipe Reactor Market often focus on predictive maintenance, real-time optimization of complex reaction parameters, and the potential for autonomous control systems to manage fluctuating feedstocks. Key themes analyzed include how AI can enhance the notoriously challenging modeling of turbulent flow in pipe geometries, whether machine learning can improve the identification of optimal operating points for chemical selectivity, and concerns surrounding data privacy and the integration complexity of AI algorithms with existing legacy Distributed Control Systems (DCS). Users are particularly keen on understanding AI’s role in preventing unplanned downtime by anticipating material degradation and scaling issues within the reactor tubes, which are critical vulnerabilities in continuous chemical processing. The expectation is that AI will move pipe reactor operation from reactive adjustment to truly proactive and predictive control.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the operational paradigm of pipe reactors, moving beyond basic process control towards highly autonomous and adaptive systems. AI algorithms are being deployed to analyze massive datasets generated by high-frequency sensors monitoring temperature, pressure, flow rates, and concentration profiles along the reactor length. This deep analysis allows for the identification of subtle non-linear relationships and process anomalies that human operators or conventional control systems might miss. Consequently, AI enables dynamic adjustments to critical parameters in microseconds, maintaining optimal selectivity and yield even when input variables fluctuate, maximizing economic performance and product quality consistency.

Furthermore, AI significantly enhances the design phase of new pipe reactors through sophisticated Computational Fluid Dynamics (CFD) modeling assisted by ML. Generative AI can rapidly explore and evaluate thousands of possible reactor geometries and operating conditions, identifying optimal designs faster and more accurately than traditional simulation methods, reducing R&D costs and time-to-market for novel chemical processes. Predictive maintenance driven by AI minimizes costly operational failures related to fouling, corrosion, or erosion within the narrow reactor tubes, leading to superior equipment reliability and greater overall plant availability, making AI adoption a critical competitive differentiator in high-intensity chemical manufacturing.

The dynamics of the Pipe Reactor Market are shaped by a complex interplay of growth drivers, inherent operational constraints, and emerging strategic opportunities. Growth is primarily propelled by the worldwide movement toward continuous processing methodologies mandated by the pursuit of higher efficiency, lower environmental footprints, and greater safety standards in chemical plants. Specifically, the rising global demand for complex, high-purity chemicals and specialized agrochemicals requires the precise control and narrow residence time distribution capabilities offered uniquely by pipe reactor technology. Conversely, the market faces significant restraints related to the capital intensity of specialized materials required for corrosive applications and the complexity associated with modeling and scaling up highly turbulent flow regimes, demanding sophisticated engineering expertise. Opportunities lie in integrating these reactors with advanced digitalization technologies, expanding their use in decentralized, modular chemical manufacturing, and exploring novel applications in sustainable chemistry sectors like biomass conversion and CO2 utilization, creating compelling impact forces for future market evolution.

Key drivers include the stringent regulatory pressure on chemical manufacturers to reduce emissions and improve process safety, making the inherently safer, smaller-inventory pipe reactors highly attractive compared to large batch vessels. The increasing economic viability of high-throughput continuous operations also necessitates reliable, robust reaction equipment capable of running 24/7 with minimal variation. A major constraint is the challenge of cleaning and maintenance—specifically, the difficulty in accessing the internal surfaces of the long, narrow pipe structures, which can be prone to deposition or fouling, impacting heat transfer efficiency and pressure drop. This limitation often requires specialized cleaning protocols and temporary shutdowns, which can offset some of the benefits of continuous operation.

Market opportunities are significant, particularly in the realm of electrification and green hydrogen production technologies, where highly efficient heat management and precise fluid handling are paramount. The modular design of many modern pipe reactors makes them ideal candidates for flexible, localized manufacturing tailored to specific regional demands, minimizing logistics costs. Impact forces, therefore, include the necessity for equipment manufacturers to develop advanced anti-fouling technologies and self-cleaning mechanisms, alongside enhancing material resistance to extreme operating conditions. Successfully addressing the constraints related to scale-up modeling and material selection will be crucial for unlocking the full global potential of continuous pipe reactor technology across diverse industrial segments.

The Pipe Reactor Market is segmented based on several critical factors, including the type of material used for construction, the operational mode, and the primary application in the end-use industries. This segmentation provides a clear framework for understanding the diverse technological requirements and market penetration across different industrial domains. The selection of materials, such as stainless steel versus exotic alloys, dictates the reactor's capability to handle corrosive media and high temperatures, directly impacting its suitability for specialty chemical production versus bulk commodity manufacturing. Operational mode primarily differentiates between continuous and batch processes, with continuous flow dominating due to superior efficiency and consistency. Furthermore, the application segments highlight where the highest value and volume growth originate, focusing heavily on fertilizer production and the burgeoning specialty chemical sector globally.

The Type segmentation, often categorized by the predominant material, reflects the trade-off between cost and performance requirements. Stainless steel reactors are typically chosen for milder or commodity chemical processes where excellent mechanical strength is needed without extreme corrosion resistance. Conversely, markets handling strong acids, halogens, or highly aggressive intermediates necessitate reactors built from high-nickel alloys (like Hastelloy or Inconel) or even non-metallic materials (such as graphite or ceramics) to ensure longevity and prevent catastrophic failures. The material segment is highly influenced by global commodity pricing and technological advancements in metallurgy, which continuously introduce more cost-effective, high-performance alloys suitable for increasingly demanding reaction conditions.

The Application segmentation underscores the market's primary revenue streams. The dominance of the fertilizer sector, particularly for phosphate fertilizers, is a defining characteristic, utilizing pipe reactors for the fundamental synthesis steps that require high efficiency and control over crystallization. However, the fastest-growing segment is expected to be specialty chemicals and pharmaceuticals, driven by the demand for small-volume, high-value products where precise temperature control and minimized side product formation are non-negotiable prerequisites. This segment often demands smaller, highly customized, and highly instrumented pipe reactor units, indicating a trend toward flexible manufacturing capabilities.

The value chain for the Pipe Reactor Market begins with the upstream suppliers of raw materials, primarily specialized metals and alloys essential for constructing high-performance reactors capable of withstanding corrosive and high-temperature environments. This phase involves material sourcing (nickel, chrome, molybdenum, etc.) and specialized fabrication processes, where vendors must adhere to strict international standards (e.g., ASME codes) regarding welding and non-destructive testing. Success at the upstream level hinges on maintaining quality control over complex metallurgy and managing supply chain risks associated with volatile commodity pricing. Key players often vertically integrate or form long-term supply agreements to ensure consistent access to high-grade materials, which constitute a significant portion of the total reactor cost.

The core of the value chain involves the design, engineering, and manufacturing of the pipe reactor systems. This middle segment requires sophisticated chemical engineering expertise, computational fluid dynamics (CFD) modeling capabilities, and advanced fabrication skills. Manufacturers transform raw materials into complex, precision-engineered reaction systems, often incorporating advanced mixing elements (static mixers) and integrated heat exchangers. Distribution channels are typically direct, involving specialized engineering procurement and construction (EPC) firms or direct sales to large chemical conglomerates. Due to the high degree of customization and technical integration required, indirect distribution through distributors is less common for large-scale, high-pressure pipe reactors, ensuring direct technical oversight throughout the installation and commissioning phases.

The downstream segment focuses on the integration, commissioning, and subsequent operational support of the installed reactors at the end-user facilities, such as fertilizer plants or specialty chemical refineries. After-sales service, including performance tuning, maintenance contracts, and replacement part supply, forms a crucial, high-margin component of the downstream revenue stream. Direct engagement between manufacturers and end-users ensures that operational challenges, such as fouling or unexpected pressure drops, are quickly addressed. Successful positioning in the downstream segment requires a global service network and specialized technical staff capable of providing expert consultancy on optimizing continuous flow chemical processes, thereby maximizing the lifetime value derived from the pipe reactor investment.

Potential customers for pipe reactors primarily comprise large-scale chemical processing industries and emerging specialty chemical manufacturers that prioritize high throughput, consistency, and process safety. The largest segment of end-users are major global fertilizer producers, including those manufacturing phosphate and nitrogen-based compounds (DAP, MAP, Urea), who rely on pipe reactors for creating highly concentrated, consistent products necessary for modern agricultural practices. These companies seek reactors capable of handling aggressive acidic media and continuous, high-volume production, where operational reliability directly translates to massive economic output. Geographic concentration of these customers is high in regions with robust agricultural sectors and strong governmental support for domestic fertilizer production, notably across APAC, North America, and parts of Europe.

Beyond bulk chemical production, significant growth in the customer base is observed within the specialty chemical sector, including manufacturers of high-value intermediates, polymers, surfactants, and fine chemicals. These users require reactors that offer unparalleled control over reaction temperature and mixing intensity to ensure high selectivity and minimal impurity formation, which is critical for product purity and subsequent regulatory approval, especially in pharmaceutical precursors. This customer group often favors smaller, modular, and highly instrumented reactor units, leveraging pipe reactor technology to conduct challenging or hazardous chemistries safely within a contained, continuous environment. They are constantly looking to adopt next-generation flow chemistry solutions to accelerate product development and scale-up from lab environments.

Additional significant buyers include integrated petrochemical companies involved in producing basic building blocks like ethylene oxide, propylene oxide, and various plasticizers, where high-efficiency heat exchange and rapid mixing are essential for managing highly exothermic reactions. Furthermore, environmental technology firms utilizing chemical processes for water purification or waste stream treatment also represent a growing customer base, utilizing pipe reactors for precise dosage and mixing of chemicals to ensure compliance with environmental discharge regulations. The decision to invest in pipe reactors for all these groups is strongly influenced by total cost of ownership (TCO), demonstrated reliability, and the ability of the vendor to provide robust modeling and scale-up support.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850.5 Million |

| Market Forecast in 2033 | USD 1358.9 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Thyssenkrupp AG, Koch Industries, Inc. (Koch-Glitsch), Sulzer Ltd., Dow Inc., Pfaudler Group, Linde PLC, CB&I (McDermott International), Mitsubishi Chemical Holdings, BASF SE, Yokogawa Electric Corporation, Alfa Laval AB, Corning Incorporated, M&M Pipeline, Flow Chemistry Systems, Heidolph Instruments GmbH & Co. KG. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Pipe Reactor Market’s technological landscape is characterized by constant innovation focused on enhancing mixing efficiency, optimizing heat transfer kinetics, and improving material compatibility under extreme operational regimes. A central technology is the utilization of advanced static mixers (SMX, SMXL, Kenics style) incorporated directly into the reactor pipeline. These mixers introduce controlled turbulence and rapid radial mixing without requiring external power, crucial for managing highly exothermic reactions and ensuring plug-flow characteristics, thereby achieving extremely narrow residence time distributions. Ongoing research focuses on developing customized 3D-printed static mixer geometries tailored through Computational Fluid Dynamics (CFD) to maximize performance for specific reaction types, moving beyond standardized helical designs to achieve superior micro-mixing capabilities necessary for ultrafast chemical reactions and nanoparticle synthesis.

Another pivotal area of technological advancement involves the integration of high-resolution, inline analytical tools and advanced sensing technologies. Traditional temperature and pressure monitoring are being supplemented by Process Analytical Technology (PAT), including spectroscopic methods (e.g., Raman, NIR) and ultrasonic sensors, integrated directly into the pipe wall or via specialized bypass loops. These technologies provide real-time, non-invasive compositional analysis of the reacting mixture, allowing for instantaneous feedback control. This digital instrumentation is foundational for AEO/GEO optimization strategies, ensuring that the process operates precisely at the chemical sweet spot defined by safety limits and maximum product selectivity. The sophistication of these sensor arrays is essential for the effective implementation of AI-driven control systems, enabling adaptive process adjustments.

Material science remains critical, particularly the development and deployment of high-performance materials capable of handling extremely corrosive chemicals, especially concentrated acids, while maintaining structural integrity under high pressure and temperature cycling. Technologies like specialized PTFE linings, borosilicate glass piping, and robust exotic alloys (e.g., high-molybdenum stainless steels) are essential for extending reactor lifespan and minimizing metal contamination, which is paramount in sensitive industries like pharmaceuticals. Furthermore, modular design principles are gaining traction, allowing manufacturers to combine pre-engineered, interchangeable pipe reactor segments, offering end-users enhanced flexibility in scale-up, quicker installation times, and easier relocation or modification of chemical production lines in response to evolving market demands.

Regional dynamics play a crucial role in shaping the demand and adoption patterns within the Pipe Reactor Market, reflecting varying industrial maturity, regulatory frameworks, and investment priorities across major global areas.

A pipe reactor is a tubular vessel designed for continuous chemical reactions, functioning primarily under plug-flow conditions with high efficiency due to its large surface area-to-volume ratio. Unlike batch stirred tank reactors (STRs), pipe reactors ensure uniform residence time, superior heat transfer, and inherent safety due to lower chemical inventory, making them ideal for rapid, exothermic, and high-purity syntheses.

The fertilizer industry, specifically the production of concentrated phosphate and ammonium-based fertilizers (such as DAP and MAP), currently drives the highest volume demand for pipe reactors. This is due to the necessity for continuous, highly controlled synthesis required to achieve specific product quality and nutrient concentration standards efficiently.

The main restraints include the high initial capital investment required for specialized corrosion-resistant materials (exotic alloys) and the inherent technical complexity associated with accurately modeling and scaling up highly turbulent, non-ideal flow patterns within the narrow reactor geometries, demanding sophisticated engineering and computational expertise.

Digitalization, via integrated sensors, Process Analytical Technology (PAT), and AI/ML algorithms, allows for real-time monitoring and predictive control of complex reaction parameters. This reduces process variability, prevents costly fouling, maximizes yield, and facilitates proactive maintenance, significantly boosting operational uptime and efficiency in continuous manufacturing environments.

The Asia Pacific (APAC) region is forecasted to exhibit the fastest growth, primarily fueled by the accelerating industrialization in China and India, massive investments in domestic chemical and fertilizer production capacity, and the widespread adoption of modern, high-efficiency continuous processing technologies across manufacturing sectors.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.