ID : MRU_ 444423 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

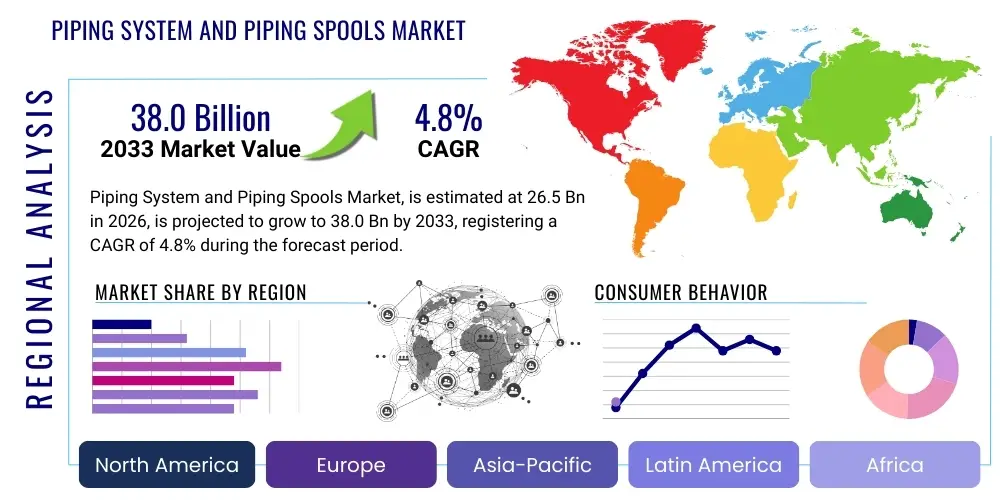

The Piping System and Piping Spools Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 26.5 Billion in 2026 and is projected to reach USD 38.0 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by significant investments in industrial infrastructure, particularly across the energy, chemical, and manufacturing sectors. The increasing demand for efficient fluid transportation, coupled with stringent safety and environmental regulations, is driving the adoption of advanced piping solutions globally. The market's expansion is also fueled by the need for reliable and durable systems capable of operating under diverse conditions, from high-pressure environments to corrosive fluid transport.

The market valuation reflects a robust demand for both standard piping systems and custom-fabricated piping spools, which offer enhanced efficiency, reduced on-site labor, and improved quality control. The trend towards modular construction and prefabrication in large-scale industrial projects is a key accelerator, significantly reducing project timelines and costs. Geographically, emerging economies in Asia Pacific and the Middle East continue to be major growth engines, driven by rapid industrialization, urbanization, and ambitious infrastructure development plans, including new refineries, power plants, and chemical complexes. Developed regions also contribute significantly through upgrades to aging infrastructure and adoption of higher-grade materials and sophisticated designs.

The Piping System and Piping Spools Market encompasses the design, fabrication, supply, and installation of interconnected networks of pipes, valves, fittings, and other components used to transport fluids, gases, or slurries from one location to another within industrial facilities. Piping systems are critical infrastructure in virtually every industrial sector, ensuring the safe and efficient flow of process media. Piping spools, a vital sub-segment, refer to pre-fabricated sections of piping, often including bends, flanges, and branch connections, which are manufactured off-site in controlled environments. This prefabrication approach enhances quality, reduces on-site construction time, minimizes labor costs, and improves safety by shifting complex fabrication tasks away from challenging field conditions.

Major applications for piping systems and spools span a wide array of industries. In the oil and gas sector, they are indispensable for exploration, production, refining, and transportation of hydrocarbons. The chemical and petrochemical industries rely heavily on intricate piping networks for processing and conveying various chemicals, often under extreme temperatures and pressures. Power generation plants, whether fossil fuel, nuclear, or renewable energy-based, require extensive piping for steam, water, and fuel lines. Furthermore, the market serves the water and wastewater treatment sector, pharmaceutical manufacturing, food and beverage processing, and marine applications, where specialized materials and designs are often necessary to meet specific purity, hygiene, or corrosion resistance requirements. The ubiquitous nature of fluid transport makes this market fundamental to global industrial operations and economic activity.

The benefits derived from high-quality piping systems and spools are manifold. They ensure operational efficiency, reduce the risk of leaks and environmental contamination, and enhance worker safety. The precision offered by pre-fabricated spools leads to better fit-up during installation and reduces the need for costly rework. Key driving factors for market growth include escalating global energy demand, necessitating new oil and gas facilities and power plants; rapid industrialization and urbanization in developing countries; increasing investments in chemical and petrochemical expansions; and the refurbishment of aging infrastructure in mature economies. Additionally, stringent regulatory frameworks pushing for safer and more environmentally compliant operations are compelling industries to upgrade to modern, high-performance piping solutions, further propelling market expansion.

The Piping System and Piping Spools Market is experiencing robust growth, driven by an intricate interplay of global industrial expansion, infrastructure development, and technological advancements. Business trends indicate a strong move towards modularization and prefabrication, optimizing project delivery timelines and enhancing cost-efficiency for industrial construction projects worldwide. Companies are increasingly investing in automation, advanced welding techniques, and digital design tools to improve the precision and quality of fabricated spools, catering to the rising demand for bespoke solutions that meet rigorous industry standards. Furthermore, the market is seeing a strategic emphasis on supply chain resilience, with key players diversifying sourcing and manufacturing capabilities to mitigate geopolitical and logistical disruptions. Sustainability considerations are also influencing business practices, encouraging the adoption of materials with lower environmental impact and processes that reduce waste, aligning with global environmental objectives.

Regional trends highlight dynamic shifts in market concentration and growth drivers. The Asia Pacific region stands out as a primary growth engine, fueled by unprecedented investments in energy infrastructure, chemical plants, and manufacturing facilities, particularly in China, India, and Southeast Asian nations. North America continues to be a significant market, driven by shale gas exploration, refinery expansions, and the modernization of existing industrial infrastructure. Europe, while a mature market, exhibits steady demand spurred by the need to upgrade aging assets, stringent environmental regulations necessitating advanced material adoption, and investments in renewable energy infrastructure. The Middle East and Africa remain crucial due to their extensive oil and gas reserves and ongoing ambitious diversification projects, while Latin America presents opportunities through emerging energy projects and industrial development. Each region presents unique regulatory landscapes and operational challenges that shape market demand and competitive strategies.

Segmentation trends reveal significant insights into market dynamics. By material, demand for stainless steel and alloy steel spools is growing due to their superior corrosion resistance and high-temperature performance, crucial for demanding applications in chemical and petrochemical industries. Carbon steel continues to dominate for general-purpose applications due to its cost-effectiveness. Application-wise, the oil and gas sector remains the largest consumer, but significant growth is observed in power generation (including renewables), water treatment, and pharmaceuticals, driven by specific project requirements and regulatory compliance. The increasing complexity of industrial processes and the need for specialized fluid handling solutions are driving the market towards higher-value, engineered piping solutions. The emphasis on safety, reliability, and longevity is influencing material selection and fabrication techniques across all end-use segments, pushing for innovation in product design and manufacturing processes to deliver optimal performance under diverse operational parameters.

Users are keen to understand how artificial intelligence will revolutionize the Piping System and Piping Spools Market, focusing on efficiency gains, predictive maintenance capabilities, and design optimization. There's a strong interest in how AI can streamline complex fabrication processes, minimize errors, and enhance safety across the entire value chain, from initial design to installation and operational monitoring. Concerns often revolve around the initial investment costs, the need for specialized skills to implement AI technologies, and data privacy issues associated with collecting and analyzing operational data. Expectations are high for AI to unlock new levels of productivity and decision-making intelligence, particularly in forecasting material needs, optimizing project schedules, and identifying potential system failures before they occur, thereby reducing downtime and operational expenditures significantly. The consensus is that AI will transform traditional approaches, making them more data-driven and predictive.

The Piping System and Piping Spools Market is significantly influenced by a confluence of drivers, restraints, and opportunities, all shaped by overarching impact forces. Key drivers include the relentless expansion of the global energy sector, particularly in oil and gas, power generation, and renewable energy infrastructure, demanding vast networks for fluid transportation. Rapid industrialization and urbanization in developing economies, leading to extensive infrastructure projects like new chemical plants, water treatment facilities, and manufacturing hubs, also fuel demand. Furthermore, stringent safety and environmental regulations compel industries to invest in high-quality, durable, and leak-proof piping solutions, often requiring advanced materials and fabrication techniques. The inherent benefits of prefabricated spools, such as reduced on-site labor, faster project completion, and improved quality control, are strong motivators for adoption, driving efficiency in large-scale industrial constructions. The continuous need for maintenance, repair, and upgrades of aging industrial infrastructure in mature economies further sustains market demand, ensuring a consistent stream of projects for both new installations and retrofits.

However, the market faces several significant restraints. Volatility in raw material prices, particularly for steel and other metals, can directly impact manufacturing costs and project budgets, creating uncertainty for both suppliers and end-users. The scarcity of skilled labor in specialized welding and fabrication, particularly for complex materials and designs, poses a challenge to meeting project demands and maintaining quality standards. Moreover, the long project cycles and substantial capital investments required for large-scale industrial projects can lead to delays and cost overruns, impacting market stability. Intense competition among market players, both local and international, can lead to price pressures and compressed profit margins. Additionally, the increasing focus on decarbonization and the transition away from fossil fuels in some regions could potentially dampen long-term demand from traditional oil and gas applications, necessitating adaptation and diversification for market participants to remain competitive and relevant.

Despite these challenges, numerous opportunities exist for market participants. The growing adoption of advanced technologies such as 3D modeling, building information modeling (BIM), and automated welding offers avenues for enhanced efficiency, precision, and cost reduction in fabrication processes. The increasing trend towards modularization and prefabrication across diverse industrial sectors presents a significant growth opportunity for specialized spool fabricators, allowing for better project control and faster deployment. Furthermore, the rising demand for specialized piping solutions in niche applications, such as hydrogen transport, carbon capture and storage (CCS), and ultra-pure systems for pharmaceuticals, opens new market segments. Investments in smart piping systems, incorporating sensors and IoT for real-time monitoring and predictive maintenance, represent a substantial opportunity for value-added services and technological differentiation. Geographically, emerging markets in Asia Pacific, Latin America, and Africa, with their burgeoning industrial bases and infrastructure deficits, continue to offer fertile ground for expansion and new project development, providing long-term growth prospects for the market.

The Piping System and Piping Spools Market is comprehensively segmented to provide a granular understanding of its diverse components, reflecting the varied applications, materials, and end-user requirements across the industrial landscape. These segmentations are critical for market players to tailor their product offerings, develop targeted strategies, and identify specific growth opportunities within a highly specialized and technically demanding industry. The market's structure is defined by how products are manufactured (product type), the materials used due to specific operational requirements (material type), the industries they serve (application), and the overarching economic sectors (end-use industry), each contributing uniquely to the market's overall dynamics and growth trajectories.

The value chain for the Piping System and Piping Spools Market is a complex network involving various stages, from raw material sourcing to final installation and aftermarket services, each adding value to the end product. It begins with upstream activities, primarily involving the extraction and processing of raw materials such as iron ore, bauxite, and petroleum, which are then refined into metals like steel, stainless steel, and various alloys, or polymers for plastic pipes. Manufacturers of valves, fittings, flanges, and other ancillary components also form a crucial part of the upstream segment, supplying the necessary elements for pipe assembly. The quality and cost of these raw materials and components significantly influence the overall cost and performance of the final piping system. Strong relationships with reliable raw material suppliers are paramount for maintaining consistent production schedules and managing price volatility, ensuring a steady flow of inputs for fabricators.

The midstream segment of the value chain is dominated by pipe manufacturers and, more critically for this market, specialized piping spool fabricators. These companies procure raw pipes and components, then employ advanced engineering, cutting, bending, welding, and assembly techniques to produce finished piping spools according to precise specifications. This stage often involves significant investment in automation, skilled labor, and quality control systems (e.g., non-destructive testing) to ensure that fabricated spools meet stringent industry standards and project requirements. Fabrication workshops often leverage 3D modeling and CAD/CAM software to optimize designs and minimize waste. The efficiency and accuracy of this fabrication process are key determinants of project success, as errors can lead to costly rework and delays during on-site installation.

Downstream activities encompass the distribution, installation, and post-installation services. Distribution channels can be direct, where fabricators supply directly to large engineering, procurement, and construction (EPC) firms or end-users for major projects, facilitating closer collaboration and tailored solutions. Indirect channels involve distributors, wholesalers, and specialized industrial suppliers who stock and supply a range of standard pipes, fittings, and sometimes spools to smaller projects or for maintenance, repair, and operations (MRO) needs. The installation phase, typically carried out by EPC contractors or specialized mechanical contractors, involves transporting the spools to the project site, lifting, fitting, and final welding to integrate them into the larger industrial facility. After-sales services, including maintenance, inspection, repair, and upgrades, form a long-term revenue stream and are crucial for ensuring the continued safe and efficient operation of piping systems throughout their lifecycle. This entire chain emphasizes quality, safety, and efficiency at every step, driven by highly specialized expertise.

The potential customers for the Piping System and Piping Spools Market are incredibly diverse, primarily comprising large-scale industrial operators, engineering firms, and construction companies across a multitude of sectors where efficient and reliable fluid transport is critical. These end-users are typically organizations undertaking significant capital projects, such as building new processing plants, power stations, refineries, or expanding existing facilities. Their purchasing decisions are heavily influenced by factors such as system reliability, compliance with safety and environmental regulations, project budget constraints, and the need for durable materials capable of withstanding specific operational conditions like high pressure, extreme temperatures, or corrosive media. The demand from these customers is often project-specific, requiring customized solutions rather than off-the-shelf products, which is a key driver for the prefabricated spools segment. The long operational lifespan of piping systems means that initial investment in quality often translates into lower lifetime costs and reduced maintenance requirements.

Major end-user segments include global oil and gas corporations, both national and international, involved in upstream extraction, midstream transportation via pipelines, and downstream refining and petrochemical processing. Chemical and petrochemical manufacturers, who operate complex facilities to produce a vast array of chemicals, are also significant buyers, requiring highly specialized piping for various reactive and corrosive substances. Power generation companies, including those operating conventional fossil fuel plants, nuclear power stations, and increasingly, renewable energy facilities (e.g., geothermal, concentrated solar power), constitute another crucial customer base for steam, water, and cooling systems. Furthermore, municipal and industrial water and wastewater treatment authorities, food and beverage producers needing hygienic processing lines, and pharmaceutical companies requiring ultra-pure systems are consistent purchasers. These customers prioritize compliance with stringent industry standards, ensuring product integrity and public safety.

In addition to these direct operators, potential customers also include major Engineering, Procurement, and Construction (EPC) companies. These firms are responsible for designing, procuring, and constructing entire industrial facilities, and they often sub-contract the fabrication and installation of piping systems and spools to specialized vendors. EPCs act as intermediaries, specifying requirements from their ultimate clients and integrating various vendor solutions into a cohesive project. Therefore, strong relationships with leading EPC contractors are vital for market players seeking to secure large-scale projects. Furthermore, shipbuilders and marine operators for offshore platforms, as well as mining companies for slurry transport, also represent significant segments of potential buyers, each with unique technical demands and operating environments. The consistent need for maintenance, repair, and operations (MRO) services ensures a continuous demand from existing industrial facilities, complementing the demand from new capital projects and upgrades.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 26.5 Billion |

| Market Forecast in 2033 | USD 38.0 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | MRC Global, Pipeline Supply & Service (PSS), Shawcor, Tenaris, Erne Fittings, WeldFit Energy Services, TIW Western, Proclad, Dyna-Mac Holdings, Tadweld, Pipe Fabrication Inc., Penn Machine Company, KAEFER, Isolux Corsán, Piping Technology & Products (PTP), Wärtsilä, Zoltek Corporation, Future Pipe Industries, Advanced Pipe & Fabrication, Fluor Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Piping System and Piping Spools Market is continually evolving, driven by the adoption of sophisticated technologies aimed at enhancing efficiency, precision, quality, and safety throughout the design, fabrication, and installation phases. At the forefront is the widespread use of advanced 3D modeling software, such as AutoCAD Plant 3D, Intergraph SmartPlant 3D, and AVEVA PDMS, which enables engineers to create highly detailed, accurate digital models of piping systems. This technology facilitates clash detection, optimizes routing, and generates precise bills of materials, significantly reducing design errors and rework. Complementing 3D modeling are Building Information Modeling (BIM) principles, which integrate piping system models with broader project data, improving coordination across various disciplines and enhancing project management. The digital transformation extends to Computer-Aided Manufacturing (CAM) tools that directly translate design models into machine instructions for automated cutting, bending, and welding equipment, ensuring high fabrication accuracy and consistency.

In the fabrication workshop, automation and robotics are transforming traditional processes. Advanced welding technologies, including orbital welding, robotic welding, and specialized processes like narrow gap welding, are increasingly employed to achieve high-quality, consistent welds with greater speed and efficiency, particularly for alloy steels and other demanding materials. These automated systems reduce reliance on manual labor, minimize human error, and enhance worker safety. Furthermore, non-destructive testing (NDT) techniques, such as ultrasonic testing (UT), radiographic testing (RT), and eddy current testing (ECT), are crucial for ensuring the integrity of welds and materials, often integrated with digital data capture for comprehensive quality assurance. The trend towards modularization and prefabrication is itself a technological advancement, leveraging controlled factory environments to produce large, complex sections of piping off-site, which are then transported and assembled at the project location, dramatically cutting down on-site construction time and risks.

Beyond design and fabrication, emerging technologies are also impacting the operational phase of piping systems. The development of smart piping systems incorporating Internet of Things (IoT) sensors for real-time monitoring of critical parameters like pressure, temperature, flow, and vibration is gaining traction. This sensor data, when combined with analytics and artificial intelligence (AI), enables predictive maintenance, allowing operators to anticipate potential failures, detect corrosion, or identify leaks proactively, thereby minimizing downtime and extending the operational life of assets. Digital twin technology, where a virtual replica of the physical piping system is created and updated with real-time data, further enhances operational visibility and decision-making for asset management. Furthermore, the use of advanced materials, such as high-strength low-alloy steels (HSLA), composite materials, and corrosion-resistant alloys (CRAs), continues to push the boundaries of piping system performance in harsh and demanding environments, supported by metallurgical advancements and improved manufacturing processes to handle these specialized materials effectively.

Piping spools are pre-fabricated sections of piping, often including bends, flanges, and branch connections, manufactured off-site in controlled environments. They are preferred because they significantly reduce on-site construction time and labor costs, improve quality control through factory fabrication, enhance safety by minimizing complex field work, and ensure greater precision and consistency in design specifications, leading to faster project completion and reduced rework.

The primary end-users include the oil and gas industry (for exploration, production, refining, and transportation), chemical and petrochemical sectors, power generation plants (conventional, nuclear, and renewable), water and wastewater treatment facilities, food and beverage processing, pharmaceuticals, and marine applications. These industries rely on reliable piping for transporting various fluids and gases critical to their operations.

Advanced technologies like 3D modeling and BIM software optimize design and clash detection, while automated welding and robotics enhance fabrication precision, speed, and consistency. Non-destructive testing (NDT) ensures quality control. These innovations lead to reduced errors, faster production cycles, improved material utilization, and higher overall quality of fabricated spools, making projects more efficient and safer.

Key growth drivers include rising global energy demand, necessitating new infrastructure in oil and gas and power generation; rapid industrialization and urbanization in emerging economies; increasing investments in chemical and petrochemical sectors; the need for upgrades to aging infrastructure in developed regions; and stringent safety and environmental regulations demanding high-performance piping solutions. The efficiency benefits of prefabrication also strongly drive adoption.

Major challenges include volatility in raw material prices, which can impact costs and project budgets; a shortage of skilled labor for specialized welding and fabrication; long project cycles and high capital investments leading to potential delays; intense market competition putting pressure on profit margins; and the long-term implications of decarbonization trends on traditional fossil fuel-related demand. These factors require continuous adaptation and strategic planning from market players.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.