ID : MRU_ 442415 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

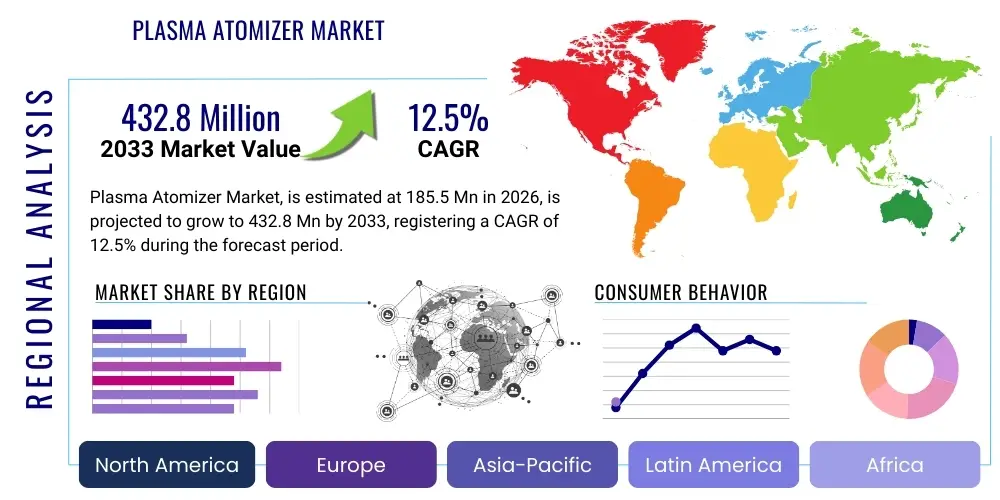

The Plasma Atomizer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at $185.5 Million in 2026 and is projected to reach $432.8 Million by the end of the forecast period in 2033.

The Plasma Atomizer Market centers on advanced technological systems utilized for producing high-quality, spherical metal powders, primarily for demanding applications such as additive manufacturing (3D printing), thermal spray coatings, and specialized materials used in aerospace and medical industries. Plasma atomization is a superior powder manufacturing technique involving the melting of precursor material (wire or rod) in an inert environment using plasma torches, followed by rapid cooling and solidification of the resultant droplets into fine, highly spherical, and clean powders. This method offers distinct advantages over traditional techniques like gas atomization, particularly in controlling particle size distribution, morphology, and purity, which are critical for high-performance applications.

The core product in this market includes the integrated plasma atomization systems, encompassing the plasma torches (typically utilizing radio frequency (RF) or direct current (DC) induction plasma), vacuum chambers, inert gas management systems, and specialized powder collection and sorting mechanisms. Major applications driving market growth involve the production of refractory metals, titanium alloys, nickel-based superalloys, and other high-melting point materials that are challenging to atomize using conventional methods. These powders are essential inputs for laser powder bed fusion (LPBF), electron beam melting (EBM), and metal injection molding (MIM).

Key benefits of employing plasma atomizers include significantly enhanced powder purity due to the crucible-less melting process, superior particle sphericity leading to improved flowability in additive manufacturing processes, and the ability to process reactive and high-temperature materials efficiently. Driving factors for market expansion are the rapid industrialization of additive manufacturing across aerospace and automotive sectors, increasing demand for customized medical implants, and stringent material specifications requiring ultra-low oxygen content and controlled microstructures in advanced components. Furthermore, the push towards achieving zero-defect production in critical supply chains fuels the adoption of these high-precision atomization technologies.

The Plasma Atomizer Market is characterized by intense technological innovation focused on improving throughput and reducing operational costs while maintaining stringent powder quality standards. Current business trends indicate a strong move toward larger capacity systems capable of continuous operation to meet the escalating demand from major metal additive manufacturing service providers and vertically integrated aerospace original equipment manufacturers (OEMs). Strategic collaborations between plasma atomizer manufacturers and materials scientists are becoming common, aimed at developing standardized production protocols for novel alloy powders, particularly those utilized in extreme environment applications. Investment in automation and sensor technology within the atomization process is a critical trend, allowing for real-time monitoring and adjustment of parameters to ensure batch consistency, a key requirement for regulated industries.

Regionally, North America and Europe currently dominate the market, primarily due to the high concentration of major aerospace and medical device manufacturers and strong government funding supporting advanced manufacturing initiatives. However, the Asia Pacific region, led by China and Japan, is emerging as the fastest-growing market segment. This growth is spurred by rapid industrial expansion, significant investment in domestic 3D printing capabilities, and governmental mandates focused on developing advanced materials independence. The regional dynamics highlight a competitive landscape where established Western players are focusing on quality and specialization, while APAC companies emphasize capacity expansion and competitive pricing strategies, accelerating the global proliferation of plasma atomization technology.

Segmentation trends reveal that the titanium and titanium alloys segment maintains a significant market share due to its indispensability in biomedical and aerospace components, requiring the ultra-high purity afforded by plasma atomization. However, the segment concerning specialized superalloys and refractory metals is projected to exhibit the highest CAGR, driven by their increasing use in high-performance engine parts and energy generation systems. By end-user, the aerospace and defense sector remains the largest consumer, valuing the superior material properties and quality assurance offered by plasma-atomized powders. Simultaneously, the medical segment is showing robust growth, propelled by the shift towards patient-specific implants manufactured through additive techniques, necessitating biocompatible and highly consistent powder feedstock.

Common user inquiries regarding AI in the Plasma Atomizer Market center around how machine learning can enhance powder quality predictability, optimize system parameters to minimize waste, and automate quality control processes currently relying on tedious manual inspection. Users frequently ask about the feasibility of using predictive maintenance models trained on historical operating data to maximize system uptime and longevity, given the high investment cost of these complex machines. Key themes summarized from these expectations involve seeking AI integration primarily for achieving 'Smart Atomization'—moving from reactive process control to proactive, self-optimizing manufacturing workflows. The core concern is the ability of AI to effectively manage the myriad variables (plasma power, gas flow, cooling rates) influencing final powder characteristics, thereby ensuring batch-to-batch consistency and accelerating material development cycles, ultimately lowering the total cost of ownership (TCO) for plasma atomization facilities.

The Plasma Atomizer Market is fundamentally shaped by the interplay between the increasing industrial demand for ultra-high-purity metal powders and the significant capital expenditure required for system acquisition and operation. The primary driver is the pervasive growth of the additive manufacturing industry, particularly in sectors where component failure is catastrophic, such as aerospace propulsion and critical medical devices, mandating the superior quality offered by plasma atomization. Furthermore, continuous technological refinement leading to increased throughput and improved energy efficiency is mitigating historical barriers, making the technology more economically viable for a broader range of specialized powder producers. Simultaneously, the restraint posed by the exceptionally high initial investment cost and the complexity of operating and maintaining high-temperature plasma systems limits immediate widespread adoption, confining the market primarily to specialized, high-value applications and large-scale material suppliers. Opportunities abound in the development of customized, small-scale atomizers for research institutions and specialized material startups, alongside geographical expansion into emerging industrial economies seeking to establish domestic advanced material supply chains.

The impact forces within this market are substantial, driven largely by the technological innovation force and the regulatory environment force. The innovation force compels manufacturers to continuously improve yield, energy consumption, and the range of processable materials, fostering intense competition. This pressure ensures that atomizer systems become increasingly sophisticated and automated. The regulatory environment, particularly concerning medical and aerospace materials, acts as a stringent barrier to entry, but also guarantees demand for the certified, high-purity powders produced by plasma systems. If regulators mandate stricter controls on powder feedstock purity, the demand for plasma atomization technology will surge. Conversely, if alternative, less costly atomization technologies (like advanced gas atomization) successfully bridge the quality gap, market growth could be tempered.

The scarcity of highly trained personnel capable of operating, optimizing, and maintaining plasma atomization systems represents another powerful restraining factor. These systems require deep expertise in plasma physics, high-vacuum technology, and metallurgy. This shortage creates a bottleneck in scaling production, especially in emerging regions. Addressing this requires atomizer manufacturers to invest heavily in comprehensive training programs and developing more user-friendly, automated interfaces. Despite this constraint, the overarching force remains the irreplaceable need for spherical, contamination-free powders, ensuring that plasma atomization retains its premium position in the advanced materials supply chain, cementing its long-term viability and growth trajectory.

The Plasma Atomizer Market is segmented based on the type of material processed, the system capacity, the end-user industry, and geographical regions. Analyzing these segments provides a nuanced view of market dynamics, revealing where investment and innovation are most concentrated. The segmentation by material type is crucial as the characteristics of the precursor material dictate the complexity and power requirements of the atomization system; high-melting point materials like refractory metals require the most powerful and specialized equipment. Similarly, system capacity segmentation, ranging from research-scale units to high-volume production systems, reflects the diverse needs of the customer base, spanning from university labs to multi-national production facilities.

Segmentation by end-user highlights the crucial link between material technology and high-stakes application sectors. The aerospace and defense sector drives demand for maximum reliability and purity in powders for structural and engine components, tolerating higher costs for superior quality. The medical sector, focused on biocompatibility and precise geometries for implants, similarly demands plasma-atomized powders. These segments dictate market pricing and R&D focus, pushing manufacturers toward achieving zero-defect production capabilities. Understanding these segments is vital for suppliers to tailor product offerings, whether focusing on high-throughput solutions for established industries or flexible, R&D-focused systems for emerging technological fields.

The value chain for the Plasma Atomizer Market is characterized by highly specialized stages, beginning with the upstream supply of raw materials and complex technical components. Upstream analysis focuses on suppliers of precursor materials—high-quality metal rods or wires—which must be sourced from certified refiners to ensure initial purity, and sophisticated components such as RF generators, plasma torch components (electrodes, nozzles), and high-vacuum pumps. The specialized nature of the plasma equipment mandates reliance on a limited number of highly technical component suppliers, often leading to potential bottlenecks or strong dependency. Success in the upstream segment requires expertise in high-purity metallurgy and vacuum engineering, ensuring the foundational quality of the atomization system itself.

Midstream activities involve the design, manufacturing, assembly, and testing of the complete plasma atomization system. This stage requires significant intellectual property related to plasma physics, fluid dynamics, and process control. Manufacturers invest heavily in R&D to enhance throughput, improve powder yield, and expand the range of materials that can be processed efficiently. Following system production, the downstream element primarily encompasses the operation of these systems by powder producers, the distribution channels, and the final consumption of the metal powder feedstock. Powder producers, who are often the customers of the atomizer manufacturers, market their specialized powders to end-user industries (e.g., aerospace OEMs, medical implant makers).

Distribution channels are predominantly direct, especially for high-value production-scale systems, where installation, commissioning, and long-term technical support are integral parts of the purchase agreement. Atomizer manufacturers maintain direct sales and engineering teams to manage complex customer relationships and provide bespoke solutions. Indirect channels may be utilized for smaller, R&D-scale systems or for selling auxiliary equipment (e.g., sieving machines) through specialized industrial distributors. The tight integration between the system supplier and the powder producer ensures proper system utilization and allows for rapid feedback loops necessary for continuous product improvement and market adaptation.

Potential customers for plasma atomization systems are predominantly large-scale metal powder manufacturers who supply the demanding additive manufacturing supply chain. These customers are driven by the necessity of producing premium-grade powders that meet stringent industry specifications, particularly regarding sphericity, particle size distribution, and chemical purity. Integrated aerospace and defense contractors, who are increasingly internalizing critical material production to secure their supply chain and maintain proprietary material control, represent a high-value customer base. For these entities, the ability to rapidly produce specialized alloys with minimal contamination is non-negotiable, making plasma atomization a strategic asset.

Beyond material producers and large aerospace entities, key end-users also include specialized medical device manufacturers, particularly those focusing on complex orthopedic, spinal, and cranial implants. These companies utilize plasma-atomized titanium and cobalt-chromium alloys due to their excellent biocompatibility and the consistency required for certified medical production processes. The trend toward patient-specific and mass-customized implants manufactured via 3D printing strongly drives this sector’s demand for high-quality feedstock. Furthermore, major automotive companies, particularly those involved in high-performance or electric vehicle component R&D (e.g., lightweight motor parts), represent a rapidly growing segment of potential customers, although they typically demand higher throughput at competitive prices compared to the aerospace sector.

Finally, governmental and university research laboratories focused on advanced materials science and novel alloy development constitute a specialized, yet crucial, customer segment. These R&D organizations often acquire smaller, highly flexible plasma atomization systems to experiment with new metal matrix compositions and tailor powder characteristics for specific research objectives. Their demand is driven by innovation rather than volume. Overall, the buyers in this market prioritize product purity, process repeatability, and the supplier’s ability to provide robust post-sales support and application expertise, reflecting the mission-critical nature of the manufactured powders.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $185.5 Million |

| Market Forecast in 2033 | $432.8 Million |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AP&C (A Metal Powders Company), Tekna Systems, Praxair Surface Technologies (Linde), Arcam AB (GE Additive), Carpenter Technology Corporation, Oerlikon Metco, Heraeus Amloy, Hoganas AB, Sandvik AB, Kennametal Inc., Xi'an Sino-Euro Materials, Advanced Plasma Solutions (APS), Nanjing Youtian Metal Technology Co., Ltd., ALD Vacuum Technologies, Phelly Materials. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Plasma Atomizer Market is defined by continuous evolution in plasma generation and powder handling techniques, aiming to achieve higher energy efficiency and tighter control over particle morphology. Currently, the landscape is dominated by two primary plasma methods: Radio Frequency (RF) Induction Plasma and Direct Current (DC) Plasma. RF plasma atomization, typically favored for producing spherical, fine powders of highly reactive materials like titanium, utilizes an induction coil to generate plasma in an inert gas stream. This crucible-less process is crucial for preventing contamination and achieving exceptional purity. Recent technological advancements in RF systems focus on increasing the power density and optimizing the torch design to improve the melt rate and yield, while simultaneously reducing the energy consumption per kilogram of powder produced, addressing a key operational cost restraint.

In contrast, DC plasma atomization, while also capable of processing high-temperature materials, often involves different feed mechanisms and chamber designs. The technological focus here is on developing multi-torch systems and improving electrode life to ensure continuous, high-throughput production, which is essential for industrial-scale operations. A crucial supporting technology involves the integration of advanced process control software and sensor arrays. These systems monitor critical variables such as chamber pressure, gas flow rates, plasma plume stability, and molten metal droplet trajectory in real-time. This sophisticated control infrastructure is fundamental to achieving the process repeatability required by certified aerospace and medical component manufacturers.

Furthermore, the technology landscape extends to proprietary cooling and powder collection systems that are necessary to preserve the quality and morphology achieved during atomization. Specialized cyclone collectors and vacuum powder conveyance systems are deployed to minimize particle degradation, prevent oxidation post-atomization, and accurately sort powders based on size distribution. The next generation of plasma atomizers is anticipated to incorporate advanced digital twin technology, allowing operators to simulate various process scenarios before physical production, thereby minimizing material waste and speeding up the validation process for new alloys. This convergence of advanced plasma physics, materials engineering, and computational modeling is driving the competitive edge in the market.

The primary advantage is superior powder quality, characterized by near-perfect sphericity, extremely low internal porosity, and significantly higher chemical purity (minimal contamination), essential for critical additive manufacturing applications in aerospace and medical sectors.

Plasma atomizers are ideally suited for processing high-melting point, reactive metals that are difficult or impossible to atomize conventionally, including titanium alloys, nickel-based superalloys, refractory metals (like Tungsten and Tantalum), and complex intermetallic compounds requiring ultra-clean processing.

The structural components of a well-maintained plasma atomizer system can last decades, but wear components like plasma torch electrodes, refractory linings, and certain vacuum seals require frequent replacement. Maintenance is complex, demanding highly skilled technicians and focusing heavily on preventing contamination and managing high temperatures.

The high initial capital expenditure (CapEx) and specialized operational requirements (OpEx, including high energy and inert gas consumption) significantly contribute to the premium pricing of plasma-atomized powders. This limits their application primarily to high-value, mission-critical components where quality justifies the increased cost.

While plasma atomization was historically R&D focused, modern production-scale systems offer throughputs suitable for industrial use (upwards of 100 kg/batch). The technology is increasingly scalable, though it remains predominantly focused on specialty, high-performance powders rather than commodity metals, due to cost considerations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.