ID : MRU_ 443725 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

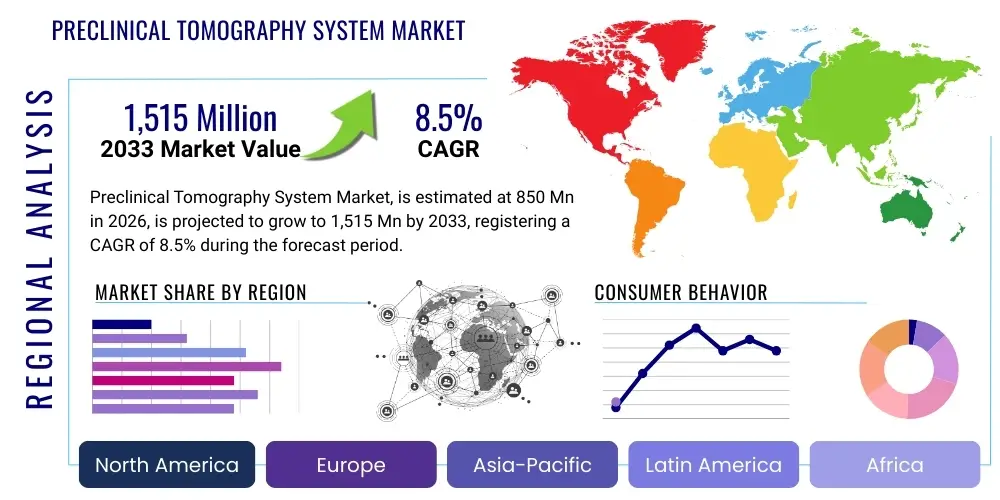

The Preclinical Tomography System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 850 Million in 2026 and is projected to reach USD 1,515 Million by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating demand for advanced, high-resolution imaging modalities necessary for sophisticated biomedical research, particularly in areas concerning oncology, neurology, and cardiology. The capability of preclinical tomography systems to provide non-invasive, longitudinal monitoring of disease progression and therapeutic response in small animal models is irreplaceable, solidifying their critical role within the drug discovery pipeline and translational medicine.

Market expansion is further bolstered by increasing governmental and private sector funding directed towards life sciences research globally. Academic institutions, pharmaceutical companies, and specialized contract research organizations (CROs) are consistently investing in state-of-the-art imaging infrastructure to accelerate the development of novel therapies. The integration of multi-modal systems, combining techniques like Positron Emission Tomography (PET), Computed Tomography (CT), Magnetic Resonance Imaging (MRI), and Single-Photon Emission Computed Tomography (SPECT), offers unparalleled anatomical and functional data, which is crucial for achieving statistically robust and clinically relevant research outcomes, thereby driving system adoption rates across established and emerging research centers.

Geographic market dynamics indicate significant growth potential in the Asia Pacific region, though North America continues to hold the dominant market share due to the high concentration of leading pharmaceutical giants and technologically advanced research infrastructure. Technological advancements focusing on improving image resolution, reducing scan times, and enhancing quantitative accuracy—specifically through automation and improved detector technology—are essential growth catalysts. Furthermore, the decreasing operational cost associated with high-throughput imaging systems over time is making these sophisticated tools more accessible to smaller research laboratories and academic departments, facilitating broader market penetration and sustaining the strong predicted CAGR through 2033.

The Preclinical Tomography System Market encompasses specialized medical imaging devices designed for non-invasive, high-resolution visualization and quantification of biological processes in living small animal models, primarily mice and rats. These systems are indispensable tools in preclinical research, enabling scientists to study disease pathogenesis, drug pharmacokinetics, and therapeutic efficacy in vivo before human trials. Products within this market segment include various imaging modalities such as Preclinical PET (Positron Emission Tomography), Preclinical CT (Computed Tomography), Preclinical MRI (Magnetic Resonance Imaging), Preclinical SPECT (Single-Photon Emission Computed Tomography), and hybrid systems like PET/CT and SPECT/CT, which combine functional and anatomical data for comprehensive analysis. Major applications span cancer research, neuroscience, cardiovascular disease modeling, infectious disease studies, and regenerative medicine, providing critical insights into physiological mechanisms and therapeutic outcomes. The primary benefits of employing these systems are the reduction of experimental variability, the ability to conduct longitudinal studies on the same animal, and the acceleration of the drug development cycle. Key driving factors include the rising prevalence of chronic diseases requiring novel treatment modalities, technological innovation leading to enhanced system performance, and increasing collaborative research initiatives between academia and industry focused on translational medicine.

The Preclinical Tomography System Market is characterized by robust technological innovation and strong investment, resulting in sustained growth projected throughout the forecast period. Business trends indicate a clear shift towards integrated multi-modal systems, offering researchers the capability to acquire simultaneous functional and anatomical information, significantly enhancing the depth and accuracy of preclinical data. There is an increasing emphasis on user-friendly interfaces, automated image analysis software, and systems capable of high-throughput screening to meet the stringent demands of pharmaceutical R&D workflows and contract research organizations. Key industry players are pursuing strategic mergers and acquisitions and forging partnerships with academic institutions to expand their technological portfolios and regional presence, particularly focusing on emerging markets that are rapidly developing their biomedical research infrastructure. The competitive landscape is intensely focused on differentiation through superior resolution, reduced radiation dosage, and faster image acquisition times, crucial factors influencing purchasing decisions among institutional buyers and corporate entities.

Regional trends highlight North America’s continued market leadership, primarily fueled by massive R&D expenditure by U.S.-based pharmaceutical and biotechnology firms, coupled with favorable regulatory environments supporting innovation. Europe follows closely, driven by strong public funding mechanisms like the Horizon Europe program, supporting centralized research facilities. The Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR, propelled by rapid expansion in biomedical research capabilities in countries such as China, Japan, and India, and increasing governmental initiatives aimed at fostering domestic drug discovery ecosystems. Investment in state-of-the-art imaging centers in APAC is a critical factor driving demand, albeit facing challenges related to initial capital investment and the need for highly specialized technical personnel to operate and maintain advanced tomography equipment.

Segmentation trends reveal that the Hybrid Systems segment, particularly Preclinical PET/CT and PET/MRI, dominates the market in terms of revenue, reflecting the growing clinical need for fused imaging data. By application, oncology remains the largest segment due to the extensive use of small animal models for cancer drug testing and personalized medicine studies. End-user analysis shows that pharmaceutical and biotechnology companies are the primary revenue generators, given their large-scale investment in drug screening pipelines. However, academic and research institutes represent a rapidly expanding user base, supported by government grants specifically earmarked for advanced research infrastructure. Furthermore, the increasing complexity of disease modeling, such as modeling Alzheimer’s disease or advanced cardiovascular pathologies, necessitates the high sensitivity and specificity offered by advanced preclinical imaging techniques, further cementing the dominance of multi-modal systems across all end-user categories.

Analysis of common user questions regarding AI's impact on the Preclinical Tomography System Market reveals key themes centered around workflow automation, enhanced diagnostic precision, and the ability to handle massive datasets. Users frequently inquire about how AI can accelerate image processing and reconstruction, which traditionally requires significant manual input and computational power. There is considerable interest in AI algorithms for quantitative image analysis, particularly for automatically segmenting tumors or tracking subtle neurological changes, thereby minimizing inter-observer variability and improving experimental reproducibility. Furthermore, questions often focus on AI's potential in multimodal data fusion—combining inputs from PET, CT, and MRI—to generate a more holistic view of biological phenomena. Concerns, however, revolve around the validation and standardization of AI models across different scanner manufacturers and research protocols, alongside the ethical implications of automating critical interpretation steps. Users anticipate that AI integration will lead to higher throughput capabilities, reducing the overall cost per experiment and fundamentally shifting research focus from data acquisition to insightful interpretation.

The Preclinical Tomography System Market is profoundly shaped by a confluence of driving factors (D), inherent restraints (R), and significant opportunities (O), collectively constituting potent impact forces. Key drivers include the escalating global R&D spending in the pharmaceutical and biotechnology sectors, necessitating sophisticated tools for drug toxicity and efficacy testing. Furthermore, the global rise in chronic and complex diseases, such as various forms of cancer, neurodegenerative disorders like Alzheimer's and Parkinson's, and persistent cardiovascular ailments, continuously pushes researchers to utilize advanced non-invasive imaging systems for developing targeted therapies. Technological progress leading to the commercial availability of ultra-high resolution and highly sensitive scanners, particularly in the micro-PET and micro-MRI segments, further acts as a powerful market impetus, allowing for earlier and more precise detection of subtle biological changes in small animal models. The trend toward personalized medicine also mandates the use of these systems for validating patient-derived xenograft (PDX) models and other translational research models, solidifying their market necessity.

Restraints, however, pose structural challenges to market expansion, primarily concerning the prohibitively high initial capital investment required for purchasing and installing these advanced tomography systems. This significant financial barrier often restricts adoption, particularly among smaller academic institutions and research groups with limited funding. Operational constraints, including the necessity for highly specialized technical expertise to operate and maintain the complex hardware and software, coupled with the ongoing costs of radioisotopes and contrast agents, also impede broader market penetration. Additionally, concerns surrounding regulatory standardization, especially for image analysis algorithms and data comparability across different systems and vendors, represent a restraint that manufacturers are constantly striving to address through robust validation studies and adherence to standardized data formats.

Despite these challenges, substantial growth opportunities abound, particularly stemming from the emergence of hybrid imaging modalities (e.g., PET/MRI) which offer simultaneous data acquisition, leading to superior temporal resolution and diagnostic synergy. Expanding opportunities in contract research organizations (CROs) leveraging their centralized resources to provide preclinical imaging services to numerous clients represent a significant commercial avenue. Geographically, the untapped potential of emerging economies in the Asia Pacific region, characterized by rapidly developing life science sectors and increasing government investment in research infrastructure, presents a vital opportunity for market growth. The ongoing integration of Artificial Intelligence and Machine Learning (AI/ML) into image processing and quantitative analysis software offers a unique opportunity to enhance throughput and derive deeper scientific insights from preclinical data, ultimately solidifying the future market trajectory and impact forces that favor innovation and integration.

The Preclinical Tomography System Market is segmented across various dimensions, including Modality, Application, End-User, and Geography, providing a granular view of market dynamics and adoption patterns. The Modality segment, crucial for defining technological capabilities, includes standalone systems (PET, CT, MRI, SPECT, Optical) and, more significantly, the multi-modal hybrid systems (PET/CT, SPECT/CT, PET/MRI) which offer researchers synergistic anatomical and functional data. Application segmentation reveals the diverse research areas benefiting from these tools, with Oncology dominating due to high R&D activity in cancer therapy development, followed closely by Neurology and Cardiology, where precise longitudinal tracking of disease progression is vital. End-user analysis differentiates between large pharmaceutical/biotechnology companies with extensive R&D budgets, academic/government research institutions driven by grants, and specialized Contract Research Organizations (CROs) offering services on a contract basis. This segmentation highlights the diverse procurement and usage patterns across the preclinical research ecosystem, emphasizing the increasing preference for integrated, high-throughput solutions capable of handling complex experimental protocols and minimizing data variability across different research settings globally.

The value chain for the Preclinical Tomography System Market is intricate, beginning with upstream activities focused on the specialized design and manufacturing of complex components and detectors. Upstream analysis involves highly specialized suppliers providing high-purity scintillator crystals for PET and SPECT detectors, superconducting magnets for MRI systems, and advanced X-ray tubes and detectors for CT systems. These component providers operate in a niche, high-technology environment, where quality control and material science innovation are paramount. Manufacturers then undertake the critical integration and assembly phase, combining these complex components with sophisticated software for image reconstruction, visualization, and quantitative analysis, often requiring significant intellectual property and precision engineering capabilities. The competitive advantage upstream is typically determined by technological differentiation, proprietary sensor technology, and efficiency in scalable, high-precision manufacturing processes, ensuring the system meets the high resolution and sensitivity demands of preclinical research.

Downstream analysis focuses on the distribution, sales, and post-sales service required to support these expensive and complex instruments. The distribution channel is crucial, utilizing both direct sales forces, particularly for major pharmaceutical clients and large government tenders, and indirect distribution through specialized regional dealers and value-added resellers (VARs) who can provide localized support and application expertise. Direct channels are preferred by leading manufacturers to maintain tight control over pricing and customer relationships for high-value contracts. Post-sales service—including installation, calibration, maintenance contracts, and specialized applications training—forms a substantial revenue stream, given the sensitivity and operational complexity of these systems. The effectiveness of the service network significantly influences customer satisfaction and repeat purchases, acting as a crucial differentiator in a market where system downtime can severely impact research timelines and funding milestones.

Effective value chain management necessitates seamless coordination between the high-technology component suppliers and the system integrators, followed by a highly responsive distribution and support network. The unique characteristic of this market is the heavy reliance on application scientists and technical specialists within the sales and support teams, bridging the gap between highly technical instrumentation and specific research requirements (e.g., oncology versus neurology research protocols). The distribution channel strategy is tailored to the end-user profile: large corporate entities often negotiate global direct contracts, whereas academic institutions frequently utilize competitive bidding processes managed by specialized procurement teams. Ultimately, successful players optimize the value chain by investing heavily in R&D to secure advanced component supply and by establishing globally dispersed, highly skilled service organizations to ensure operational continuity for their scientific customer base.

The primary potential customers and end-users of Preclinical Tomography Systems are organizations deeply involved in the drug discovery, validation, and advanced biomedical research continuum. Pharmaceutical and Biotechnology Companies constitute the largest customer base, driven by the intense necessity to screen new drug candidates efficiently, assess toxicity profiles, and demonstrate proof-of-concept for therapeutic efficacy using rigorous in vivo models. These corporations utilize preclinical tomography systems extensively for pharmacokinetics/pharmacodynamics (PK/PD) studies and to monitor the effect of novel compounds on disease biomarkers. The decision-makers here are typically R&D department heads, capital expenditure committee members, and research group leaders who prioritize high throughput, system reliability, and multi-modal integration capabilities to expedite their pipeline development and reduce failure rates in clinical trials, justifying the substantial investment required for the equipment.

Academic and Government Research Institutions represent the second major customer segment. Universities, national laboratories, and public research centers (such as NIH-funded labs) leverage these systems for fundamental scientific exploration, understanding disease mechanisms, and basic biology research funded primarily through competitive grants. These institutions often require systems that are versatile enough to support a wide array of research applications, from gene expression studies to complex physiological measurements, sometimes favoring modular or lower-throughput systems when budget constraints are strict. Procurement in this segment is influenced by factors such as system accessibility, collaborative potential (shared core facilities), and the availability of specialized training and application support to maximize system utility across diverse departmental needs.

Contract Research Organizations (CROs) are rapidly emerging as a critical customer segment, especially those specializing in preclinical drug development and toxicology studies. CROs purchase and maintain tomography systems to offer comprehensive, high-quality imaging services to pharmaceutical and biotech clients who either lack the in-house infrastructure or require specialized expertise. CROs emphasize throughput, cost-efficiency, and the ability to produce standardized, regulatory-compliant data packages. Their demand is highly correlated with the outsourcing trends of large pharma companies seeking to streamline R&D overhead. As translational research accelerates, the reliance on specialized CROs to provide high-caliber preclinical imaging data is expected to grow substantially, positioning them as a key investment driver in the tomography market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1,515 Million |

| Growth Rate | CAGR 8.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bruker Corporation, PerkinElmer Inc., FUJIFILM Holdings Corporation, MR Solutions, Mediso Ltd., Siemens Healthineers, TRIUMF Innovations, MILabs B.V., Aspect Imaging, Cubresa Inc., MOLECUBES, Pingseng Medical, Bioscan, United Imaging Healthcare, Agilent Technologies, LI-COR Biosciences, iThera Medical GmbH, Kaixin Scientific, Promega Corporation, Thermo Fisher Scientific. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Preclinical Tomography System Market is characterized by continuous innovation aimed at enhancing image resolution, sensitivity, and the integration of diverse functional and anatomical information. A critical development is the increasing miniaturization of components and optimization of detector technology, particularly in PET and SPECT systems, leading to superior spatial resolution necessary to visualize very small structures (e.g., micro-tumors or discrete brain regions) in small animals. Furthermore, advancements in specialized detector materials, such as solid-state detectors (e.g., Cadmium Zinc Telluride or CZT) in SPECT, offer higher energy resolution and greater efficiency compared to traditional crystal technologies. For Preclinical MRI, the trend involves increasing magnetic field strengths (e.g., 7 Tesla and higher) to boost signal-to-noise ratios, enabling sophisticated functional and diffusion tensor imaging crucial for detailed neurological studies, while simultaneously developing compact, cryogen-free systems to reduce infrastructure requirements and operational complexity for broader institutional accessibility.

The major technological driver shaping the future of the market is the proliferation of hybrid imaging systems, specifically the integration of PET with MRI (PET/MRI). This coupling allows for simultaneous acquisition of metabolic function (PET) and detailed soft-tissue anatomy (MRI) without requiring animal repositioning, significantly improving temporal registration and reducing experimental artifacts. This technological synergy is particularly valuable for complex longitudinal studies in neuro-oncology and cardiology, where subtle changes in both morphology and function must be precisely correlated over time. Additionally, optical imaging technologies (fluorescence and bioluminescence) are often integrated into existing systems or utilized alongside tomography for preliminary screening, benefiting from developments in highly sensitive cameras and new generations of fluorescent probes that are stable and specific to molecular targets in vivo, offering rapid and cost-effective initial assessments.

Software innovations are equally pivotal in the technological ecosystem. The focus has shifted toward advanced image reconstruction algorithms, particularly iterative methods that handle complex data sets derived from multi-modal acquisitions, and robust automation tools powered by Artificial Intelligence (AI) and Machine Learning (ML). These computational technologies are essential for managing the vast amounts of data generated by high-resolution scanners, facilitating automated organ and lesion segmentation, and enabling quantitative analysis with minimal user bias. Cloud computing platforms are also becoming integral for data storage, collaboration, and high-performance processing, allowing researchers globally to access and analyze large preclinical image archives efficiently, thereby standardizing workflows and accelerating the translation of basic research findings into clinical applications and product development pipelines across the life sciences industry.

Regional dynamics play a significant role in defining the Preclinical Tomography System Market landscape, driven by varying levels of R&D investment, regulatory environments, and the concentration of major pharmaceutical and academic institutions. North America, particularly the United States, commands the largest market share due to its established leadership in biomedical research, substantial funding from government bodies (like the National Institutes of Health or NIH), and the presence of global pharmaceutical and biotechnology heavyweights committed to advanced drug development using sophisticated preclinical models. This region benefits from high adoption rates of cutting-edge hybrid systems and favorable market conditions for technology introduction, coupled with a robust ecosystem of specialized Contract Research Organizations (CROs) facilitating market penetration and specialized service provision.

Preclinical PET/CT provides excellent anatomical structure derived from CT, ideal for oncology and bone studies, combined with functional metabolic data from PET. PET/MRI, conversely, offers superior soft-tissue contrast and advanced functional imaging techniques (like fMRI) from MRI, crucial for neurology and cardiology, coupled with high-sensitivity PET functional data, making it the highest value hybrid modality.

The Pharmaceutical and Biotechnology Companies segment currently drives the majority of revenue growth. This is attributed to their massive R&D investments, the necessity for high-throughput screening of drug candidates, and the requirement for robust, regulatory-compliant preclinical data packages for submission to health authorities like the FDA and EMA.

AI is primarily integrating through advanced software for automated image reconstruction, noise reduction, and quantitative analysis. AI algorithms significantly accelerate the often time-consuming processes of image segmentation and biomarker quantification, enhancing data throughput and minimizing researcher variability, which is vital for longitudinal studies.

The main financial barrier is the high initial capital investment required for purchasing advanced systems, particularly hybrid modalities like PET/MRI, which can cost millions of dollars. Additionally, operational costs, including maintenance contracts and the ongoing expenses for radioisotopes and specialized contrast agents, contribute significantly to the total cost of ownership, limiting adoption by smaller research centers.

APAC’s high projected CAGR is driven by substantial governmental initiatives and increased private sector funding directed towards building advanced life sciences research infrastructure, particularly in countries such as China and India, coupled with a growing regional focus on domestic drug discovery and development programs.

Micro-CT systems provide high-resolution anatomical data, essential for detailed skeletal, lung, and contrast-enhanced vascular imaging. While lacking the functional sensitivity of PET or SPECT, CT is invaluable as a rapid, high-throughput anatomical baseline and is most frequently used in hybrid configurations (PET/CT, SPECT/CT) to provide precise anatomical localization for functional imaging signals.

Preclinical systems are foundational to translational medicine by enabling the non-invasive, longitudinal tracking of disease progression and therapeutic response in animal models, utilizing imaging biomarkers that are directly transferable to human clinical trials. This similarity in imaging technology and quantification methods bridges the gap between basic research and clinical application, accelerating the transition of novel drugs.

Competitive advantage is predominantly determined by technological superiority, specifically ultra-high resolution and sensitivity in detector technology, successful integration of multi-modal capabilities (e.g., robust PET/MRI solutions), superior proprietary software for image analysis, and the quality and global reach of post-sales service and application support.

Yes, there is a steady, albeit niche, growing market for refurbished or used preclinical tomography equipment. This trend is driven by smaller academic institutions and emerging market research centers seeking cost-effective alternatives to acquire high-quality imaging infrastructure without the prohibitive capital outlay of new systems, provided that rigorous quality control and technical support are guaranteed by the refurbishing vendor.

The shift towards cryogen-free MRI technology is highly significant as it drastically reduces the complexity and expense of facility installation and ongoing operational maintenance associated with traditional superconducting magnets requiring liquid helium. This makes high-field MRI technology more accessible to smaller research facilities and less prone to expensive operational interruptions, thus broadening its adoption.

CROs are influencing purchasing patterns by centralizing demand for high-throughput, robust, and versatile multi-modal systems. Their emphasis is on efficiency and standardization across multiple client projects. They often invest in the latest technology to maintain competitive edge, acting as early adopters and driving the requirement for vendor reliability and comprehensive service agreements to minimize downtime and ensure continuous operation for contracted studies.

Challenges in data standardization stem from variations in system hardware (detector types, field strengths), proprietary reconstruction algorithms used by different manufacturers, and differences in preclinical imaging protocols (e.g., choice of radioisotopes, anesthesia levels). This necessitates the development of standardized data formats and robust post-processing tools to ensure data comparability and reproducibility across disparate research environments.

Neurology and Neuroscience research demonstrates the most promising growth potential, driven by the global aging population and the increasing need to understand and develop therapies for complex neurodegenerative disorders such as Alzheimer's, Parkinson's, and ALS. Preclinical PET/MRI systems, offering high soft-tissue contrast and functional insights, are particularly critical for this segment's expansion.

Improvements in radiotracer chemistry are fundamentally expanding the Preclinical PET market by developing novel, highly specific tracers that target a wider array of biological processes, including specific receptors, enzyme activities, and inflammatory markers. This expanded targeting capability increases the utility and relevance of PET imaging across diverse therapeutic areas beyond traditional oncology, making the systems more indispensable for comprehensive functional phenotyping.

Regulatory scrutiny is expected to drive higher standards for data quality, reproducibility, and quantitative rigor in preclinical imaging. This pressure encourages manufacturers to develop highly automated, validated software solutions and promotes the adoption of standardized imaging protocols across institutions, ultimately improving the reliability and clinical translatability of preclinical research outcomes and favoring systems with robust validation history.

Longitudinal imaging, enabled by non-invasive tomography, allows researchers to repeatedly scan the same animal over time, effectively reducing the total number of animals required for a study and minimizing biological variability between cohorts. This capability generates more statistically powerful data on disease progression and therapeutic efficacy within an individual subject, significantly improving the efficiency and ethical standard of preclinical research.

While high-field MRI (7T+) offers excellent soft tissue resolution, the highest spatial resolution for detailed anatomical visualization is typically achieved by Micro-CT systems. For functional imaging, the highest sensitivity and near-millimeter resolution are provided by advanced Preclinical PET systems utilizing detector technologies like monolithic crystals and improved depth-of-interaction (DOI) capabilities.

Manufacturers face challenges in the MEA market primarily related to fragmented research funding, high logistics costs for installation and servicing complex equipment, and the limited availability of specialized technical talent required to operate and maintain high-end tomography systems, necessitating substantial upfront investment in local training and support infrastructure.

Open-source platforms, while promoting collaboration and accessibility for basic research, exert competitive pressure on proprietary software vendors by offering free alternatives for fundamental image processing tasks. This forces manufacturers to differentiate their commercial software offerings through advanced features, AI integration, regulatory compliance tools, and dedicated customer support that open-source solutions often lack, focusing on unique quantitative capabilities.

Researchers prioritize high sensitivity (to minimize tracer dose and scan time), high spatial resolution (to accurately delineate small structures), and quantitative accuracy (to ensure reliable measurement of metabolic activity). Additionally, they prioritize energy resolution and compatibility with multi-modal configurations (e.g., integration into a PET/CT or PET/MRI setup) to maximize the informational content derived from each experiment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.