ID : MRU_ 443616 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

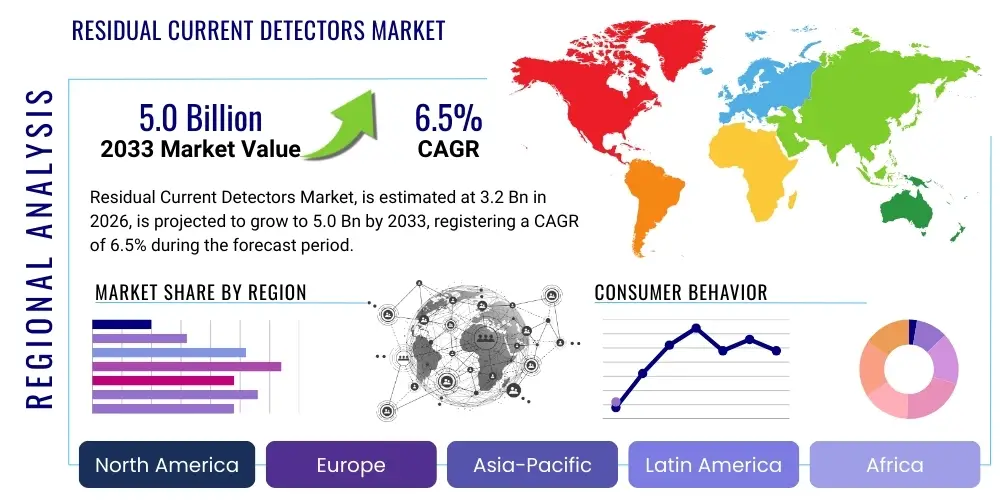

The Residual Current Detectors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 3.2 Billion in 2026 and is projected to reach USD 5.0 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by increasingly stringent global electrical safety regulations and the rapid modernization of aging electrical infrastructure across developed and developing economies. The adoption rate of advanced RCD technologies, particularly those integrated with smart grid capabilities, is contributing significantly to market value expansion.

The Residual Current Detectors (RCD) Market encompasses devices designed to automatically detect and interrupt fault currents to ground, ensuring protection against electric shock and preventing electrical fires. RCDs, which include Residual Current Circuit Breakers (RCCBs), Residual Current Circuit Breaker with Overcurrent Protection (RCBOs), and Ground Fault Circuit Interrupters (GFCIs), are critical components in both residential and industrial electrical installations. The necessity for these devices stems from the fundamental principle of limiting leakage current to safe levels, particularly in wet or harsh environments where the risk of electrocution is heightened. Product descriptions typically highlight fast tripping times, high sensitivity, and robustness against transient surges to ensure reliable operation.

Major applications for residual current detectors span across residential buildings, commercial establishments like hospitals and data centers, and heavy industrial settings, including manufacturing plants and oil and gas facilities. In residential sectors, RCDs are mandated for sockets likely to supply outdoor equipment or those installed in bathrooms and kitchens. In industrial contexts, specialized high-sensitivity RCDs are deployed to protect complex machinery and personnel operating in high-risk zones. The primary benefits derived from RCD deployment are enhanced personnel safety, crucial equipment protection against damage caused by earth faults, and compliance with national and international electrical safety codes, such as IEC standards.

Driving factors propelling market expansion include global urbanization leading to extensive construction activity, the escalating demand for reliable power distribution systems, and mandatory governmental legislation concerning electrical safety, particularly in the European Union and parts of Asia Pacific. Furthermore, technological advancements leading to compact, higher-performance devices and the integration of predictive maintenance features are attracting greater investment from utilities and end-users. The continuous effort to reduce fatal electrical accidents globally reinforces the market's intrinsic growth momentum.

The Residual Current Detectors Market demonstrates robust growth supported by compelling business trends focusing on digitalization and regulatory compliance. Key business trends involve manufacturers shifting towards modular and compact designs that simplify installation and minimize panel space requirements, alongside integrating IoT capabilities for remote monitoring and predictive fault detection. Strategic mergers and acquisitions are common as established players seek to acquire niche technology expertise, particularly in high-speed sensing and communication protocols suitable for smart grids. The overall competitive landscape remains moderately consolidated, driven by innovation in Type B and Type F RCDs which offer enhanced protection against smooth DC residual currents prevalent in variable speed drives and electric vehicle charging infrastructure.

Regional trends indicate that Europe and North America maintain significant market share, primarily due to well-established, strict electrical codes (e.g., NFPA 70 in the US and various harmonized EN standards in the EU) and ongoing infrastructure refurbishment projects. However, the Asia Pacific region, especially China and India, is emerging as the fastest-growing market segment. This accelerated growth is attributed to rapid industrialization, large-scale residential construction booms, and recent governmental initiatives to enforce stricter electrical safety standards, often leapfrogging older technologies directly to advanced RCD solutions. Latin America and MEA are experiencing steady growth fueled by significant investments in utility infrastructure modernization and expansion of commercial real estate.

Segment trends highlight the dominance of RCBOs (Residual Current Circuit Breaker with Overcurrent Protection) due to their dual functionality, saving space and simplifying circuit protection in modern distribution boards. The Type B RCD segment is witnessing the highest percentage growth, reflecting the increasing proliferation of power electronics, solar photovoltaic systems, and electric vehicle (EV) chargers, all of which generate complex leakage current waveforms that standard Type A RCDs cannot reliably detect. Furthermore, the industrial application segment is projected to hold the largest value share, driven by the need for enhanced operational continuity and compliance with occupational safety standards in manufacturing and processing facilities.

Common user inquiries regarding AI's influence on the Residual Current Detectors Market often center on how AI can enhance detection accuracy, minimize false tripping, and integrate RCD data into broader smart building management systems (BMS). Users are concerned about the ability of traditional RCDs to differentiate between genuine fault currents and benign transients or harmonic noise, especially in environments saturated with power electronics. Key expectations revolve around using machine learning algorithms to analyze complex current signatures in real-time, predict insulation degradation before a fault occurs, and enable adaptive tripping thresholds. There is a strong interest in AI-driven diagnostics that can improve system reliability and reduce maintenance costs associated with unnecessary downtime caused by nuisance tripping.

The application of Artificial Intelligence is fundamentally transforming RCD functionality from a reactive safety device into a proactive, predictive asset management tool. AI algorithms are being deployed in advanced residual current monitors (RCMs) to analyze large volumes of operational data, including current harmonics, temperature fluctuations, and historical tripping events. This sophisticated analysis allows the RCD system to learn the normal electrical footprint of an installation. When deviations occur, the system can issue preemptive warnings or adjust sensitivity settings dynamically, thereby reducing nuisance trips caused by non-critical leakage while maintaining protection against genuine shock hazards. This transition from purely hardware-based protection to software-enhanced safety is a major market disruption.

Furthermore, AI facilitates seamless integration of RCD data streams into enterprise asset management and smart grid platforms. By using predictive models, facility managers can optimize maintenance schedules, replacing or repairing circuits based on calculated risk profiles derived from AI-processed leakage current trends rather than fixed time intervals. This improves operational efficiency and extends the lifespan of the electrical infrastructure. The move toward smart, connected RCDs capable of self-diagnosis and communication is crucial for achieving high levels of safety and operational continuity in mission-critical environments like data centers and healthcare facilities, setting a new benchmark for electrical safety technology.

The Residual Current Detectors Market is driven primarily by the mandatory implementation of electrical safety standards globally and the rapid proliferation of electrical equipment generating complex current waveforms. Restraints include the high initial cost associated with deploying advanced RCD types (like Type B) and challenges related to retrofitting older infrastructure where space and compatibility issues arise. Opportunities are abundant in emerging markets focusing on renewable energy integration, specifically solar PV and EV charging stations, both of which require specialized RCD protection. The impact forces indicate that regulatory pressure and technological evolution are the strongest determinants shaping market direction, pushing manufacturers towards continuous innovation in detection accuracy and reliability.

Key drivers include the global push for enhanced worker safety in industrial settings, which mandates the use of highly sensitive RCDs compliant with strict Occupational Safety and Health Administration (OSHA) and European Union directives. The increasing adoption of decentralized power generation, such as rooftop solar installations, mandates the use of specialized Type B or Type F RCDs to handle potential DC fault currents, significantly boosting demand in this segment. Furthermore, growing public awareness regarding the risks of electrical hazards, often catalyzed by consumer safety campaigns and regulatory enforcement, encourages preemptive installation in residential and commercial sectors, even where not strictly mandated.

Major restraints involve the technical complexity and lack of standardization in diagnosing nuisance tripping, which can lead to user frustration and, in some cases, the unauthorized bypassing of safety devices. This undermines confidence in the technology. Additionally, while the overall cost of basic RCDs is decreasing, the specialized, digitally-enabled RCDs required for high-tech applications (e.g., data centers) carry a substantial premium, making large-scale adoption challenging for small and medium enterprises. Opportunities lie in the development of universally compatible, self-testing, and self-monitoring RCDs that simplify maintenance, address nuisance tripping concerns, and provide cost-effective compliance solutions for complex modern electrical networks.

The Residual Current Detectors Market is rigorously segmented based on product type, sensitivity, application, and end-user, reflecting the diverse requirements across electrical safety domains. The analysis across these segments provides critical insights into market penetration rates and growth pockets. Product type segmentation distinguishes between conventional electro-mechanical devices and more advanced electronic RCDs, with the latter gaining prominence due to superior features like adjustable trip times and enhanced immunity to transient voltages. End-user segmentation shows a clear division between high-volume, cost-sensitive residential applications and high-value, specialized industrial and utility applications that demand custom solutions and high reliability.

The segmentation by product type, specifically focusing on the differentiation between RCCBs, RCBOs, and RCD blocks, is crucial for manufacturers in tailoring their offerings. RCBOs dominate the growth metrics due to their integrated functionality (residual current and overcurrent protection), which streamlines installation processes and optimizes distribution board space, highly valued in modern urban construction projects. Furthermore, segmentation by sensitivity (high sensitivity 30mA, medium sensitivity 100mA, and low sensitivity 300mA/500mA) is essential for aligning products with specific regulatory requirements for personnel protection versus equipment and fire protection.

Application-based segmentation reveals significant differential growth rates. The electric vehicle (EV) charging infrastructure segment is forecasted to exhibit the highest CAGR due to the global transition towards e-mobility, necessitating specialized DC-sensitive RCDs (often Type B or EV-specific RCDs). Similarly, the utility and energy sector segment is expanding rapidly, driven by smart grid investments and the requirement for continuous leakage monitoring across vast distribution networks to ensure grid stability and minimize hazards in substations and renewable energy farms. Understanding these segmentation nuances is key for targeted marketing and product development strategies aimed at maximizing market share.

The value chain for the Residual Current Detectors Market commences with upstream activities centered on the procurement and processing of specialized raw materials, primarily high-grade plastics, precision metals (copper and silver for contacts), and ferrite cores used in the sensing coils. Key upstream success factors include securing stable supply chains for copper and managing the volatility in raw material costs, as these directly influence the final device price. Manufacturers often engage in long-term contracts with material suppliers to ensure quality control and minimize cost fluctuations. Technological sophistication in core manufacturing, especially the precise winding of toroid cores for accurate fault detection, is a vital component of upstream efficiency.

The midstream segment involves the core manufacturing, assembly, and testing of RCDs. This stage is highly capital-intensive, requiring specialized automation for high-precision assembly and rigorous quality control testing compliant with international standards (e.g., IEC 61008 and 61009). Manufacturers must invest significantly in R&D to develop compact designs, improve immunity to spurious tripping, and integrate electronic components for smart functionality. Key players often utilize sophisticated manufacturing techniques like lean production to achieve economies of scale, especially for high-volume products like Type A RCCBs aimed at the residential market.

Downstream activities focus on distribution and post-sale services. Distribution channels are bifurcated into direct sales to large utilities and Original Equipment Manufacturers (OEMs), and indirect sales through electrical wholesalers, distributors, and certified installation contractors for the residential and SME market. Indirect channels rely heavily on strong regional partnerships and training programs to ensure proper product selection and installation. After-sales support, including warranty services, technical training for electricians, and replacement part logistics, are crucial for maintaining brand reputation and customer loyalty, especially for complex Type B and electronic RCDs used in sensitive industrial applications.

Potential customers for Residual Current Detectors are broadly categorized into three primary end-user groups: residential consumers, commercial enterprises, and heavy industrial operators, alongside governmental entities responsible for public infrastructure. Residential buyers, though typically purchasing through intermediaries (electricians and hardware stores), represent the largest volume market, driven by mandatory installation requirements for new construction and renovation projects, particularly in kitchens, bathrooms, and outdoor areas where water presence heightens shock risk. Their primary requirement is cost-effectiveness and simple integration with standard circuit breaker panels.

Commercial enterprises, including data centers, healthcare facilities, retail chains, and educational institutions, represent a high-value customer base that prioritizes reliability, uptime, and advanced monitoring capabilities. For these buyers, the cost of downtime far outweighs the initial expense of the RCD. Consequently, they often opt for specialized RCDs, Residual Current Monitors (RCMs), and electronic devices with communication capabilities that allow continuous monitoring and predictive maintenance. Compliance with insurance requirements and local building codes, which are often stricter in commercial settings, further drives their purchasing decisions toward premium, high-performance RCDs.

Industrial and utility customers constitute the segment demanding the most robust and technologically advanced RCD solutions, specifically Type B devices for protecting motor drives, complex machinery, and critical power distribution networks. Key buyers in this segment include major manufacturing corporations, oil and gas refineries, mining operations, and utility providers managing electrical substations and renewable energy plants (solar and wind farms). Their requirements emphasize extreme durability, high fault current ratings, selectivity, and integration with SCADA systems for centralized control, ensuring that only the faulty circuit trips without affecting system-wide stability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 5.0 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, Eaton Corporation plc, Schneider Electric SE, Legrand SA, Hager Group, Mitsubishi Electric Corporation, L&T Electrical & Automation, Chint Group, Nader Electric, Doepke Schaltgeräte GmbH, Noark Electric, Sensata Technologies, Finder SpA, G&W Electric, Hubbell Incorporated, Emerson Electric Co., Fuji Electric Co., Ltd., Zez Silko, ETI Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Residual Current Detectors market is characterized by a strong focus on enhancing sensitivity to complex fault currents and integrating digital capabilities. The primary technological advancement involves the migration from traditional Type AC and Type A RCDs to Type F and Type B devices. Type B technology is critical because it utilizes sophisticated electronic circuits, often incorporating multiple sensing coils and highly specialized digital signal processing (DSP) units, to accurately detect smooth DC residual currents generated by inverters, frequency converters, and modern consumer electronics. This shift necessitates complex semiconductor components and refined coil designs to handle the non-linear magnetic fields generated by DC faults without suffering magnetic saturation.

Another pivotal technological trend is the incorporation of self-testing and self-monitoring mechanisms (SRCDs - Self-Reclosing Residual Current Devices). These features dramatically improve reliability by automatically testing the device's functional integrity at regular intervals and, in some advanced models, automatically reclosing the circuit after a transient trip if conditions allow. This technology relies on embedded microcontrollers and precision voltage/current injectors to simulate a fault and verify the tripping mechanism, ensuring continuous operational readiness, a crucial requirement in unattended remote installations like telecom towers and EV charging stations. Furthermore, advances in magnetic materials are enabling the creation of smaller, more sensitive current transformers that are less susceptible to external electromagnetic interference.

The digitalization of RCDs through the integration of IoT connectivity represents a major technological leap. Smart RCDs are equipped with communication modules (e.g., Modbus, Ethernet, Wi-Fi) that transmit real-time leakage current data, operational status, and historical logs to centralized cloud platforms or local monitoring systems. This remote monitoring capability supports predictive maintenance strategies, helps analyze the root cause of nuisance tripping, and facilitates compliance reporting. This integration often leverages advanced sensor fusion techniques where RCD data is combined with temperature and voltage monitoring for a holistic view of circuit health, optimizing both safety and energy management efficiency within a building or industrial facility.

The distinction lies in the types of fault currents they can detect. Type A RCDs are designed to detect AC (alternating current) and pulsating DC residual currents, making them suitable for standard appliances. Type B RCDs are advanced devices capable of detecting AC, pulsating DC, and smooth DC residual currents. Type B RCDs are mandatory for installations involving devices with internal rectification, such as EV charging points, solar inverters, and variable speed drives, where pure DC faults are a risk.

RCBOs are preferred because they integrate both residual current protection and overcurrent protection (short circuit and overload) into a single, compact unit. This integration saves significant space within the distribution board, simplifies wiring complexity, and allows for selective fault tripping, ensuring that a fault in one circuit does not unnecessarily trip other circuits, thereby enhancing overall system reliability and installation efficiency, particularly in space-constrained commercial settings.

The rapid expansion of EV charging infrastructure is a major growth driver, specifically boosting demand for specialized RCDs. EV chargers often utilize power electronics that can generate dangerous smooth DC leakage currents. Standard RCDs (Type A) cannot detect these. Consequently, regulatory bodies increasingly mandate the use of Type B or specialized EV-specific RCDs to ensure personnel safety, creating a high-growth, high-value segment for manufacturers offering DC fault detection solutions.

Nuisance tripping occurs when an RCD trips unnecessarily due to transient voltage surges, high-frequency electrical noise (harmonics), or small, non-critical cumulative leakage currents, rather than a genuine fault. Manufacturers are addressing this by developing electronic RCDs with time-delay features (S-type/Selective RCDs) and integrating advanced digital signal processing (DSP) or AI algorithms to analyze complex current signatures, enabling the device to differentiate between benign transient noise and genuine hazardous fault conditions, thereby enhancing operational stability.

Digitalization transforms RCDs into smart, communicative devices. Future RCDs are expected to integrate IoT connectivity for remote monitoring, real-time data logging, and predictive maintenance diagnostics. This capability allows facility managers to receive alerts regarding incipient insulation faults before a trip occurs, optimize energy consumption by monitoring leakage current trends, and comply with safety reporting requirements automatically, moving the technology beyond simple protection to comprehensive electrical safety management.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.