ID : MRU_ 444513 | Date : Feb, 2026 | Pages : 242 | Region : Global | Publisher : MRU

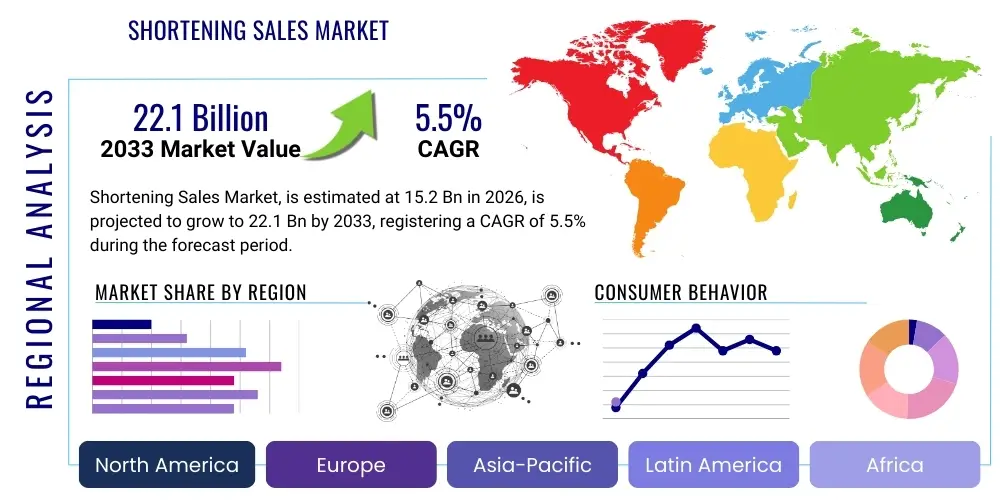

The Shortening Sales Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2026 and 2033. The market is estimated at USD 15.2 billion in 2026 and is projected to reach USD 22.1 billion by the end of the forecast period in 2033. This growth is driven by the sustained demand from the thriving bakery and confectionery industries globally, coupled with the increasing penetration of processed food products in developing economies. The versatility of shortening in various food applications, from improving texture and shelf life to enhancing flavor, positions it as an indispensable ingredient across the food manufacturing landscape, underpinning its steady market expansion over the coming years.

The Shortening Sales Market encompasses the global trade and consumption of various types of fats and oils used primarily in food preparation, characterized by their plastic fat properties at room temperature. Shortenings are essential ingredients in the food industry, valued for their ability to tenderize baked goods, create flaky textures, and provide a smooth mouthfeel. They are typically composed of hydrogenated or partially hydrogenated vegetable oils, animal fats, or a blend of both, processed to achieve specific functional characteristics. The primary objective of shortening is to 'shorten' gluten strands in dough, resulting in a more tender product, while also acting as an excellent medium for frying due to their high smoke points and neutral flavor profiles.

Major applications of shortening span across the bakery and confectionery sectors, where they are integral to the production of cakes, cookies, pastries, breads, and icings. In the frying industry, shortenings are extensively used for deep-frying various food items, imparting a desirable crispness and golden-brown finish. Beyond these core applications, shortening also finds use in savory snacks, convenience foods, and certain spreads and sauces, contributing to product consistency and overall palatability. The benefits of using shortening include improved product texture, extended shelf life due to oxidative stability, enhanced flavor release, and cost-effectiveness compared to some alternative fats. Furthermore, specialized shortenings can offer emulsification properties, crucial for achieving uniform batters and stable creams.

Driving factors for the Shortening Sales Market include the continuous expansion of the global food processing industry, particularly in emerging economies where urbanization and changing dietary habits are fueling demand for convenience foods and baked goods. The rise of disposable incomes in these regions, coupled with an increasing preference for ready-to-eat products, directly translates into higher consumption of ingredients like shortening. Additionally, innovations in shortening formulations, such as the development of trans-fat-free and low-saturated fat options, are addressing consumer health concerns and expanding market acceptability. The robust growth of quick-service restaurants and commercial bakeries also contributes significantly to the demand for bulk shortening products, ensuring a stable trajectory for market growth.

The Shortening Sales Market is experiencing dynamic shifts driven by evolving consumer preferences, technological advancements, and a complex regulatory environment. Business trends indicate a strong emphasis on product innovation, with manufacturers increasingly focusing on developing shortenings that are trans-fat-free, lower in saturated fat, and utilize sustainable sourcing methods, particularly for palm oil and other vegetable oils. The industry is also witnessing a trend towards clean label ingredients and plant-based alternatives, responding to a growing health-conscious consumer base. Strategic collaborations between shortening producers and food manufacturers are becoming more common, aiming to co-develop customized solutions that meet specific application requirements and improve product performance. Furthermore, the optimization of supply chain logistics and the adoption of advanced processing technologies are key business imperatives for enhancing efficiency and competitiveness within the market.

Regionally, the Asia Pacific market stands out as a significant growth engine for shortening sales, propelled by its rapidly expanding population, rising disposable incomes, and the burgeoning food service and processed food sectors. Countries like China, India, and Indonesia are witnessing substantial investments in food manufacturing capabilities, leading to increased demand for key ingredients such as shortening. North America and Europe, while more mature markets, are characterized by a strong focus on premium, healthier, and specialty shortening products, driven by stringent health regulations and sophisticated consumer demands for clean label and functional foods. Latin America and the Middle East & Africa also present promising growth opportunities, as their food processing industries continue to develop and modernize, adopting Western dietary patterns and convenience food trends, thereby stimulating the uptake of shortening products.

Segmentation trends reveal that vegetable-based shortenings dominate the market, primarily due to widespread availability, cost-effectiveness, and suitability for various dietary preferences, including vegetarian and vegan diets. Palm oil and soybean oil derivatives are particularly prominent in this category. The bakery and confectionery application segment continues to be the largest consumer of shortening, driven by the perennial demand for baked goods globally. However, the frying application segment is also showing steady growth, especially in the fast-food and convenience food sectors. In terms of distribution, the business-to-business (B2B) channel, serving industrial food manufacturers and foodservice providers, accounts for the bulk of sales, although retail channels are also crucial for household consumption, albeit a smaller share of the overall market. Ongoing innovation in product form, such as liquid and solid shortenings tailored for specific uses, further refines market segmentation and consumer choices.

User questions regarding the impact of AI on the Shortening Sales Market frequently revolve around how artificial intelligence can enhance efficiency, sustainability, and innovation within the industry. Common inquiries probe the potential of AI in optimizing raw material sourcing, predicting market demand fluctuations, and improving the consistency and quality of shortening products. There is also significant interest in AI's role in developing novel shortening formulations that meet evolving health standards and consumer preferences, such as identifying ideal fatty acid profiles or designing emulsification systems. Furthermore, users often express curiosity about how AI can streamline complex supply chains, reduce waste, and provide real-time insights into production processes, ultimately contributing to a more responsive and resilient shortening market.

The application of AI in the shortening sales sector holds transformative potential, primarily by enhancing operational intelligence and fostering data-driven decision-making across the value chain. By leveraging machine learning algorithms, manufacturers can analyze vast datasets pertaining to raw material quality, supplier performance, and global commodity prices, leading to more informed procurement strategies and reduced operational costs. AI-powered predictive analytics can also forecast demand patterns with greater accuracy, enabling companies to optimize inventory levels, minimize spoilage, and ensure timely product delivery, thereby improving overall supply chain efficiency and responsiveness to market shifts. This proactive approach not only mitigates risks associated with volatile ingredient markets but also supports more sustainable practices by reducing unnecessary overproduction.

Beyond operational improvements, AI is poised to revolutionize product development and quality control within the shortening market. AI models can analyze intricate correlations between ingredient compositions, processing parameters, and final product attributes, facilitating the rapid development of innovative shortenings with desired functionalities, such as enhanced oxidative stability, specific melting profiles, or improved emulsifying capabilities. This capability is particularly crucial for formulating trans-fat-free or reduced-saturated-fat alternatives that maintain sensory appeal and performance. In terms of quality assurance, AI-driven vision systems and sensor technologies can continuously monitor production lines for consistency, detect anomalies, and ensure that every batch of shortening meets stringent quality specifications, leading to higher product reliability and consumer satisfaction while significantly reducing the potential for costly recalls.

The Shortening Sales Market is significantly influenced by a complex interplay of drivers, restraints, and opportunities, shaping its growth trajectory and competitive landscape. Key drivers include the ever-expanding global food processing industry, particularly the bakery and confectionery sectors which rely heavily on shortening for texture, mouthfeel, and shelf-life extension. Rapid urbanization in developing countries, coupled with rising disposable incomes and changing lifestyles, has led to a surge in demand for convenience foods, processed snacks, and ready-to-eat meals, all of which utilize shortening as a crucial ingredient. Furthermore, technological advancements in food science enabling the production of specialized shortenings with enhanced functional properties, such as improved emulsification or oxidative stability, continue to fuel market growth by meeting diverse industrial requirements. The cost-effectiveness and versatility of shortening compared to other fats also contribute to its sustained demand across various applications.

However, the market faces notable restraints, primarily stemming from growing consumer health consciousness and increasing scrutiny over trans fats and high saturated fat content. Public health campaigns and regulatory pressures in many developed regions have led to a decline in the consumption of traditional shortenings, prompting manufacturers to invest in reformulation efforts. Fluctuations in the prices of raw materials, such as palm oil, soybean oil, and other vegetable oils, due to climatic conditions, geopolitical events, and trade policies, pose significant challenges to manufacturers in terms of cost management and pricing strategies. Additionally, the availability of healthier alternatives like butter, olive oil, and other specialty fats, coupled with a consumer trend towards ‘clean label’ and minimally processed foods, presents a competitive threat to the shortening market, compelling innovation and adaptation.

Opportunities within the Shortening Sales Market largely lie in product innovation and expansion into emerging markets. The development and commercialization of trans-fat-free and reduced-saturated-fat shortenings, often derived from interesterified or fractionated oils, represent a major growth avenue, aligning with global health trends and regulatory mandates. Investment in sustainable sourcing practices, particularly for palm oil, offers an opportunity to enhance brand reputation and appeal to environmentally conscious consumers and businesses. Moreover, the vast untapped potential in developing economies across Asia Pacific, Latin America, and Africa, where food processing industries are still nascent but rapidly expanding, provides significant scope for market penetration and growth. Strategic partnerships, mergers, and acquisitions focused on technological advancement and geographic expansion can further unlock these opportunities, driving innovation and market share for leading players, while continuous research into novel plant-based fat alternatives also presents a promising long-term outlook for specialized shortening applications.

The Shortening Sales Market is comprehensively segmented to provide a detailed understanding of its diverse components and dynamics. This segmentation allows for targeted analysis of market trends, consumer preferences, and competitive landscapes across different product categories, raw material sources, end-use applications, forms, and distribution channels. The market's complexity necessitates a granular breakdown to identify specific growth pockets and challenges. By analyzing these segments, stakeholders can gain insights into the prevailing market structure, identify lucrative opportunities, and tailor their strategies to address distinct demands within the shortening industry, ensuring a more effective and responsive approach to market participation.

Understanding the interplay between these various segments is crucial for predicting market evolution. For instance, the ongoing shift towards healthier fat options directly impacts the demand for specific types of shortenings and their raw material sources. Similarly, the rapid growth of the food service industry versus traditional retail channels dictates the preferred form and packaging of shortening products. Each segment contributes uniquely to the overall market valuation and growth, reflecting the varied requirements of industrial users, commercial kitchens, and household consumers. This detailed segmentation not only aids in market sizing and forecasting but also highlights areas ripe for innovation and product differentiation, fostering a more competitive and consumer-centric market environment. The global shortening industry is thus a mosaic of these interdependent segments, each responding to distinct economic, social, and technological drivers.

The value chain for the Shortening Sales Market begins with the upstream analysis, which primarily involves the agricultural sector and raw material suppliers. This segment focuses on the cultivation and harvesting of oilseeds such as soybeans, palm, sunflower, and rapeseed, as well as the rearing of animals for animal fats like lard and tallow. Key players at this stage include farmers, agricultural cooperatives, and large-scale plantation owners. The quality, yield, and sustainability of these raw materials directly impact the cost and final characteristics of the shortening products. Processing facilities then convert these raw agricultural products into crude oils and fats through extraction and refining processes. This initial stage is crucial for ensuring the foundational quality and availability of ingredients that underpin the entire shortening manufacturing process, making it susceptible to global commodity price fluctuations, weather patterns, and geopolitical influences.

Moving downstream, the refined oils and fats undergo various transformation processes to become shortening. This involves hydrogenation, interesterification, fractionation, and blending to achieve specific functional properties like plasticity, melting point, and oxidative stability required for different applications. Shortening manufacturers, ranging from global agribusiness giants to specialized fat and oil processors, are central to this stage. They invest heavily in research and development to innovate new formulations, such as trans-fat-free or low-saturated-fat shortenings, to meet evolving consumer demands and regulatory standards. The manufacturing segment adds significant value by converting basic commodities into highly functional food ingredients, requiring substantial capital investment in processing technology, quality control systems, and specialized expertise in lipid chemistry and food applications, making it a pivotal stage in the value chain where product differentiation is often achieved.

The distribution channel for shortening products is multifaceted, encompassing both direct and indirect routes to market. Direct distribution typically involves B2B sales from shortening manufacturers directly to large-scale food manufacturers, commercial bakeries, and foodservice chains, often involving bulk deliveries and customized product specifications. This channel emphasizes long-term contracts, technical support, and logistical efficiency. Indirect distribution, on the other hand, involves a network of distributors, wholesalers, and retailers. Wholesalers procure shortening in large quantities and then supply smaller bakeries, restaurants, and convenience stores. Retail channels, including supermarkets, hypermarkets, and online platforms, cater to individual consumers for household use. Each distribution channel plays a vital role in ensuring market penetration and accessibility, with online retail witnessing increasing prominence for both B2B and B2C transactions, driven by digital transformation and convenience. The efficiency and reach of these channels are critical for effectively connecting producers with the diverse array of end-users.

The Shortening Sales Market caters to a diverse range of potential customers, primarily classified as end-users or buyers who integrate shortening into their products or daily operations. At the forefront are industrial food manufacturers, a cornerstone of the market demand. This category includes large-scale producers of baked goods such as cakes, cookies, breads, and pastries, who rely on shortening for its consistent performance in texture, structure, and shelf life extension. Confectionery companies also represent a significant customer segment, utilizing shortening in chocolates, candies, and various sweet treats to achieve desired melting properties and mouthfeel. The demand from these industrial customers is often in bulk, requiring specific formulations and consistent supply, making them pivotal to the market's stability and growth. Their product development cycles and consumer trends heavily influence the types and volumes of shortening purchased.

Another crucial segment of potential customers encompasses the foodservice industry, including restaurants, fast-food chains, hotels, and commercial catering businesses. These entities extensively use shortening, particularly for frying applications, where its high smoke point, neutral flavor, and ability to impart crispness are highly valued. From deep-frying potatoes and chicken to preparing various fried snacks, shortenings are an indispensable part of their kitchen operations. Commercial bakeries, ranging from small artisanal shops to large factory-style bakeries, also form a significant customer base, procuring diverse shortening types tailored for their specific product lines, such as specialty shortenings for flaky pastries or emulsified shortenings for high-ratio cakes. The foodservice and commercial bakery sectors prioritize both functionality and cost-efficiency, often seeking suppliers who can provide reliable products and flexible delivery options to meet their operational demands.

Finally, the retail sector, comprising supermarkets, hypermarkets, convenience stores, and increasingly, online grocery platforms, serves individual consumers for household use. While this segment accounts for a smaller portion of the overall industrial shortening market, it is vital for brand visibility and direct consumer engagement. Home bakers and cooks utilize shortening for various culinary tasks, from baking pies and cookies to pan-frying. This customer base is often influenced by factors such as brand reputation, packaging convenience, perceived health benefits (e.g., trans-fat-free labels), and price point. As health consciousness grows, the demand for premium, specialty, and healthier shortening options within the retail segment is steadily increasing, prompting manufacturers to diversify their product offerings and packaging formats to appeal to a broader array of home consumers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 22.1 Billion |

| Growth Rate | 5.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cargill, Archer Daniels Midland Company (ADM), Bunge Limited, Wilmar International Ltd., AAK AB, Fuji Oil Holdings Inc., Loders Croklaan (IOI Loders Croklaan), Associated British Foods (ABF), Conagra Brands, Inc., JBS USA (Pilgrim's Pride), Ventura Foods, Richardson International Limited, Upfield Holdings B.V., Manildra Group, Olenex Holdings B.V., PT. SMART Tbk, Sime Darby Plantation Berhad, United Plantations Berhad, Louis Dreyfus Company B.V., Golden Agri-Resources Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Shortening Sales Market is underpinned by a sophisticated array of technologies aimed at enhancing product functionality, quality, and health profiles. A foundational technology is hydrogenation, which involves adding hydrogen atoms to unsaturated fatty acids in vegetable oils to solidify them and increase their oxidative stability, thereby extending shelf life. While partial hydrogenation led to trans fat formation, advancements have focused on full hydrogenation combined with blending techniques to achieve desired textures without trans fats. Another critical technology is interesterification, a process that rearranges fatty acids within or between triglyceride molecules, modifying the melting profile and crystal structure of fats to create shortenings with specific functionalities (e.g., plasticity, creaming ability) and improved nutritional profiles, often replacing the need for partial hydrogenation.

Further technological advancements include fractionation, a physical separation process that divides fats into fractions with different melting points, allowing for the creation of tailor-made shortenings with precise textural and functional characteristics suitable for various applications, such as bakery, confectionery, or frying. Blending technology is also crucial, enabling manufacturers to combine different fats and oils (e.g., palm, soybean, sunflower) in precise ratios to achieve desired sensory attributes, nutritional profiles, and performance metrics, optimizing for cost-effectiveness and specific end-user requirements. Emulsification techniques and the incorporation of food-grade emulsifiers are vital for producing shortenings that can effectively blend oil and water, essential for high-ratio cakes and creamy icings, contributing to product stability and texture.

Beyond these core processing technologies, the shortening market also leverages advancements in analytical chemistry and quality control. Spectroscopic methods (e.g., Near-Infrared, NMR) and chromatographic techniques (e.g., GC-MS, HPLC) are used to precisely characterize fatty acid profiles, detect contaminants, and ensure product consistency and safety. Emerging technologies such as enzyme-catalyzed interesterification offer more environmentally friendly and energy-efficient alternatives to chemical processes, further refining product quality. Moreover, sustainable sourcing technologies, including traceability systems and certification schemes for palm oil (e.g., RSPO), are becoming increasingly important, driven by consumer demand and corporate social responsibility initiatives, shaping the long-term technological and ethical landscape of shortening production. The continuous evolution of these technologies is pivotal for manufacturers to meet rigorous industry standards and adapt to changing market demands effectively.

Shortening is a type of fat, typically solid at room temperature, used in cooking and baking to tenderize baked goods, create flaky textures, and serve as a frying medium. Its primary uses are in bakery and confectionery products, as well as for deep frying various foods, due to its ability to 'shorten' gluten strands and provide a high smoke point.

Key drivers include the expanding global food processing industry, particularly the bakery and confectionery sectors, rising demand for convenience foods due to urbanization and disposable income growth, and technological advancements creating specialized shortenings with enhanced functional benefits.

Health concerns, specifically regarding trans fats and saturated fats, are a significant restraint. This has led to stringent regulations and a shift among manufacturers towards developing and marketing trans-fat-free, low-saturated-fat, and plant-based shortening alternatives to meet evolving consumer preferences and health mandates.

The Asia Pacific region, particularly countries like China, India, and Indonesia, is demonstrating the strongest growth in shortening sales. This is driven by rapid urbanization, increasing disposable incomes, and the robust expansion of their respective food processing and foodservice industries.

Technological innovations such as interesterification (to eliminate trans fats), fractionation (for tailored functional properties), and enzyme-catalyzed processes (for cleaner production) are crucial. Additionally, advanced analytical methods and sustainable sourcing technologies are enhancing product quality, safety, and environmental responsibility.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.