ID : MRU_ 441332 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

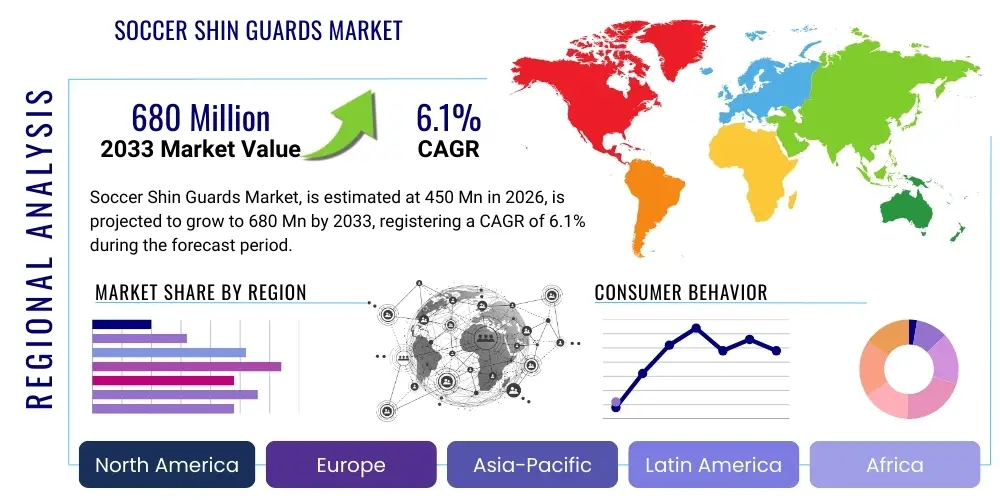

The Soccer Shin Guards Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.1% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 680 Million by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by increasing global participation in organized soccer leagues, growing awareness regarding player safety regulations mandated by governing bodies like FIFA, and continuous innovations in protective gear materials designed for enhanced comfort and impact absorption.

The Soccer Shin Guards Market encompasses the manufacturing, distribution, and sale of protective equipment designed to safeguard a player's shins during soccer matches and training sessions. These essential protective devices are primarily used to prevent serious lower leg injuries, such as fractures, contusions, and lacerations, resulting from direct impacts, tackles, or collisions on the field. The product spectrum ranges from lightweight slip-in models favored by professional athletes for minimal interference to comprehensive ankle-protected models utilized predominantly by youth and amateur players requiring maximum stability.

Major applications of soccer shin guards span across professional soccer leagues (e.g., Premier League, La Liga, MLS), international tournaments, organized amateur leagues, school and university sports programs, and recreational play. Key benefits include adherence to mandatory safety requirements, significant reduction in the severity of impact injuries, and improved player confidence during aggressive play. Driving factors include the globalization of soccer, stringent enforcement of safety standards across all competitive levels, rising disposable incomes allowing investment in high-quality sports equipment, and advancements in material science leading to lighter, more durable, and biomechanically ergonomic designs.

The Soccer Shin Guards Market is defined by intense competition and rapid technological integration aimed at balancing protection and performance. Current business trends indicate a strong shift towards specialized, custom-fit, and lightweight materials like carbon fiber and advanced polymers, catering specifically to elite athlete demands for agility without compromising safety. Regional trends show robust growth in established soccer regions such as Europe and Latin America, coupled with accelerating demand in emerging markets like Asia Pacific, fueled by infrastructural development in sports facilities and increasing youth participation. Segment trends highlight the dominance of the Slip-in shin guards category due to professional preference and a sustained surge in online distribution channels, offering consumers wider access to specialized brands and custom protective solutions, thereby influencing pricing strategies and market accessibility globally.

User inquiries regarding AI's influence in the Soccer Shin Guards Market primarily revolve around personalized fit, material optimization, and enhanced safety analytics. Consumers and manufacturers are keenly interested in how Artificial Intelligence can facilitate the creation of custom 3D-printed guards tailored exactly to a player’s unique tibial geometry, improving both comfort and protection effectiveness. Key themes include the use of AI algorithms to analyze impact data (derived from embedded sensors) to predict common injury points, thus guiding future material composite development. There is also significant expectation regarding AI-driven supply chain management and inventory forecasting, especially for specialized and limited-edition protective gear lines, ensuring efficient market responsiveness to athlete needs and regulatory changes.

The Soccer Shin Guards Market is propelled by mandatory safety regulations and rising sports participation, particularly among youth. However, growth is tempered by the high costs associated with premium materials and the prevalence of counterfeit products. Opportunities lie in leveraging advanced material science and personalized protective solutions. The market dynamics are governed by five key impact forces: competitive rivalry among global sports giants, the increasing bargaining power of consumers due to specialized online retail options, moderate threat of new entrants due to regulatory barriers, low threat of substitutes as shin guards are often mandatory, and high bargaining power of suppliers who provide proprietary materials like high-grade carbon fiber or specialized polymers.

Drivers: Mandatory regulations by global and regional soccer governing bodies requiring the use of shin guards in all competitive matches are the primary market driver. Additionally, the continuous increase in organized participation rates globally, especially in North America and Asia, ensures a growing addressable market. Furthermore, heightened media attention on player welfare and concussion prevention has positively influenced the perceived value and adoption of high-quality protective gear, including shin guards, across all competitive tiers.

Restraints: Significant restraints include the high production costs associated with innovative, lightweight materials such as advanced carbon fiber composites, which limits mass adoption in price-sensitive regions. Another challenge is player discomfort; some players, particularly professionals, prefer minimal bulk, leading to the use of smaller, less protective guards or even non-compliance in certain training scenarios. Lastly, the market is constantly challenged by the proliferation of low-quality, non-certified, and counterfeit products that undermine safety standards and brand integrity.

Opportunities: Opportunities abound in the realm of material innovation, particularly developing smart textiles and incorporating sensor technology into shin guards for real-time impact monitoring and data collection. The burgeoning trend of customized protective gear, utilizing 3D scanning and additive manufacturing (3D printing), allows manufacturers to command premium pricing while delivering superior fit and protection. Furthermore, focused marketing towards the rapidly expanding female and youth soccer segments presents significant untapped potential for specialized product lines.

The Soccer Shin Guards Market segmentation provides a granular view of product performance, material composition, and consumer adoption patterns across various end-user categories and distribution channels. The market is primarily categorized by Type, dissecting products based on design and coverage (Slip-in, Ankle, Sock guards), and by Material, focusing on the core protective compounds utilized, which directly dictates price point and protection level (Polyurethane, Carbon Fiber, Fiberglass). Analyzing these segments helps stakeholders tailor their product development and marketing strategies to meet the specific safety and performance requirements of different player demographics, ranging from elite professionals demanding lightweight gear to youth players prioritizing comprehensive ankle protection.

The value chain of the Soccer Shin Guards Market begins with the upstream sourcing and processing of raw materials, primarily specialized polymers, foam padding, fiberglass, and increasingly, carbon fiber composites. Manufacturers then focus on efficient molding, assembly, and quality control processes, often investing heavily in R&D to improve impact dispersion and reduce weight. Midstream activities involve product testing and certification to meet regulatory standards set by bodies like CE and NOCSAE. Downstream, distribution channels play a crucial role; direct sales via branded e-commerce platforms offer higher margins and direct customer feedback, while reliance on traditional retail (specialty sports stores) ensures broad physical market presence. The ultimate stage involves sales to end-users (players) and after-sales services, which are critical for brand loyalty, especially in the professional segment.

Upstream analysis emphasizes securing high-quality, durable, yet lightweight materials. Manufacturers must maintain strong relationships with specialized chemical and composite material suppliers, as proprietary formulations often provide a competitive edge in terms of protection-to-weight ratio. The move towards sustainable and recyclable materials also influences sourcing decisions in this phase. Cost management at the material sourcing stage is vital, particularly for high-volume, mid-range plastic/polycarbonate guards.

The distribution channel landscape is bifurcated into direct and indirect routes. Direct distribution, primarily through owned brand websites and flagship stores, allows for better inventory control, personalized customer engagement, and higher profit margins, often utilized for premium or customizable products. Indirect distribution relies heavily on specialty sports retailers, large department stores, and global e-commerce giants (Amazon, Alibaba), providing vast reach and convenience. Specialty stores remain crucial as they offer expert advice and fitting services, which are valued by new or youth players. Effective logistics and warehousing are paramount to handle seasonal spikes in demand associated with league start times.

The primary end-users and potential customers for soccer shin guards span a wide demographic, categorized mainly by commitment level and age group: Professional Players, Amateur Players (including collegiate and recreational), and Youth Players. Professional players represent a high-value, albeit smaller, segment focused exclusively on cutting-edge, lightweight, and custom-fit carbon fiber guards, often dictated by sponsorship agreements and demanding specific biomechanical properties for peak performance. Their purchasing decisions prioritize minimal bulk and maximum protection against high-velocity impacts.

Amateur players form the largest market segment by volume, seeking a balance between durability, cost, and certified safety. This segment includes adult league participants and university athletes who often favor durable polyurethane or fiberglass guards purchased through specialized sports retailers. Their buying cycle is less frequent than professionals, typically replacing guards when damaged or worn out. Marketing efforts here emphasize reliability and certified protection standards (e.g., NOCSAE approval).

Youth players represent a critically important growth segment, often necessitating frequent replacements due to growth spurts and higher parental emphasis on absolute protection. Parents are the direct buyers, prioritizing models that offer comprehensive protection, such as ankle-protected guards, and focusing on visibility and comfort features suitable for children. Educational marketing about injury prevention and adherence to league safety rules strongly influences purchasing in this segment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 680 Million |

| Growth Rate | 6.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Nike, Adidas, Puma, Under Armour, G-Form, Storelli, Diadora, Vizari, Warrior, Lotto, Joma, Reusch, Umbro, Select Sport, Champion, XProtex, Pro-S, Franklin Sports, Zoch, Tursi |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Soccer Shin Guards Market is rapidly evolving, driven by the desire to increase protection while simultaneously reducing weight and improving comfort. A significant development is the incorporation of advanced composite materials, most notably aerospace-grade carbon fiber, which provides superior strength-to-weight ratios compared to traditional plastics and fiberglass. This allows for extremely thin, yet highly protective guards favored by elite athletes. Furthermore, manufacturers are increasingly using proprietary foam technologies, such as reactive polyurethane foams (e.g., used by G-Form), which remain soft and flexible during movement but instantly harden upon impact, dramatically improving energy absorption.

Another crucial technological advancement is the adoption of Additive Manufacturing (3D Printing). This technology enables manufacturers to produce highly customized, anatomical guards based on individual player scans, ensuring a perfect fit that maximizes coverage and minimizes shifting during play. 3D printing also allows for complex lattice structures within the guard’s core, optimizing material usage and weight distribution. This trend caters directly to the growing demand for personalized athletic gear and is beginning to democratize custom protection beyond the professional level.

The integration of smart technology represents the next frontier. This includes embedding micro-sensors (accelerometers and gyroscopes) within the guards to measure the force and location of impacts. This data is transmitted wirelessly to coaches or medical staff, providing valuable insights for injury monitoring, training load analysis, and, crucially, informing future product development cycles to address the most frequent impact zones. This data-driven approach is key to securing patents and demonstrating superior protective performance in a highly competitive market.

Regional analysis reveals that Europe currently holds the dominant share of the Soccer Shin Guards Market, primarily due to the deeply embedded soccer culture, the presence of numerous top-tier professional leagues (e.g., English Premier League, Bundesliga, La Liga), and stringent enforcement of player safety standards across all levels. Countries such as the UK, Germany, and Spain represent mature markets characterized by high consumer spending on premium, technologically advanced equipment. Manufacturers often use European leagues as key testing grounds for new product innovations and material composites.

North America, while traditionally dominated by other sports, is witnessing explosive growth in the soccer participation rate, particularly within youth and collegiate leagues. This growth, combined with robust disposable incomes and high safety standards (e.g., NOCSAE regulations in the US), makes it a rapidly expanding and strategically important market. The demand here leans towards innovative, high-tech guards, driven by effective marketing campaigns targeting tech-savvy parents and athletes.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This acceleration is fueled by massive investments in soccer infrastructure across China, India, and Southeast Asia, coupled with rising interest spurred by global televised tournaments. While price sensitivity remains a factor, the increasing middle-class population and government initiatives promoting sports participation are opening significant opportunities for both established global brands and local manufacturers of mid-range, certified shin guards.

The market growth is primarily driven by mandatory safety regulations enforced by soccer governing bodies (like FIFA) and the continuous, worldwide increase in organized participation rates, especially among youth and amateur leagues, necessitating certified protective gear for injury prevention.

Professional soccer players overwhelmingly prefer Slip-in Shin Guards. These lightweight, minimalistic guards maximize agility and comfort while often incorporating advanced materials like carbon fiber for superior protection without adding excessive bulk or weight.

Technology is significantly impacting the market through the integration of 3D printing for custom-fit anatomical designs and the use of smart sensors to measure real-time impact force and location, allowing for data-driven improvement in material science and performance optimization.

The Carbon Fiber segment holds high growth potential, despite its premium price, due to increasing demand from high-performance athletes who require optimal protection-to-weight ratios. Advanced proprietary polymers are also showing robust adoption rates.

The primary restraint is the high manufacturing cost of premium materials such as carbon fiber and advanced reactive foams, leading to high retail prices that limit adoption among general amateur and lower-income demographic segments, who often prioritize economical alternatives.

The succeeding sections delve into specific segmentation analyses, providing granular detail on market dynamics across product types, materials, distribution channels, and end-user demographics. This detailed examination is crucial for stakeholders aiming to develop targeted marketing campaigns, optimize supply chains, and identify niche growth opportunities within this expanding protective gear sector. The analysis underscores the competitive landscape where innovation in protective material science and customization services are becoming key differentiators for market success.

The segmentation by Type, encompassing Slip-in Shin Guards, Ankle Shin Guards, and Sock Shin Guards, reveals distinct purchasing behaviors. Slip-in guards dominate the professional and elite amateur market due to their lightweight nature and minimal interference with movement, often secured using compression sleeves. These guards focus intensely on high-impact absorption materials within a small profile. Conversely, Ankle Shin Guards, which include integrated ankle protectors and straps, are highly favored in the youth and beginner segments where stability and comprehensive coverage are prioritized over minimal weight.

Sock Shin Guards, designed to combine the protective plate directly within a compression sock, offer an innovative blend of convenience and compliance, appealing particularly to casual players and those seeking maximum ease of use. The competitive landscape mandates that manufacturers continuously innovate across all three types, ensuring that even the most minimalistic slip-in models adhere rigorously to mandated safety standards while providing the expected performance edge sought by high-level athletes. This pursuit of the optimal balance between protection and performance defines product development strategies in this segment.

Moving to the Material segmentation—Fiberglass, Plastic/Polycarbonate, Polyurethane, and Carbon Fiber—it becomes clear that material composition dictates both market price and protective effectiveness. Polycarbonate and standard Plastic guards remain the bedrock of the mass market, offering cost-effective and certified protection suitable for general use and youth sports. These materials provide adequate impact resistance and durability, making them essential offerings for broad market penetration and high-volume sales. They represent the entry-level standard for mandatory protective gear globally.

Fiberglass guards offer a mid-range option, providing better rigidity and durability than basic plastics but falling short of the performance metrics achieved by advanced composites. The high-end market is unequivocally dominated by Carbon Fiber. Known for its exceptional strength-to-weight ratio, carbon fiber allows manufacturers to create extremely thin, yet incredibly robust shields that can withstand high-velocity professional impacts. This material segment is seeing rapid growth in valuation, driven by elite athlete endorsement and continuous improvement in fabrication techniques that lower manufacturing waste and improve structural integrity. Polyurethane-based technologies, particularly those that are flexible but reactive (like those used in soft shell guards), offer a compelling alternative that prioritizes wearer comfort and flexibility, appealing to players who frequently move and prefer less rigid protective wear.

The Distribution Channel segmentation, spanning Online (E-commerce) and Offline (Specialty Stores, Department Stores, Supermarkets), highlights shifting consumer purchasing habits. Offline channels, particularly specialty sports stores, remain critical as they provide necessary expertise, fitting services, and the opportunity for physical examination of the product, which is particularly important for parents purchasing gear for growing children. These stores often house premium, high-margin products and serve as crucial touchpoints for brand loyalty and product education, ensuring the correct fit for optimal safety.

However, the Online channel, encompassing branded websites and massive third-party marketplaces, is rapidly increasing its market share. E-commerce platforms offer unparalleled convenience, price comparison tools, access to highly specialized or niche brands not available locally, and comprehensive customer reviews. This channel significantly empowers the consumer and forces manufacturers to focus on excellent digital presence and efficient global logistics. The growth of online platforms is particularly impacting the market for standard, known-brand products and custom-printed guards, where physical fitting is mitigated by online scanning or sizing guides. The dual strategy of maintaining strong physical presence while prioritizing digital sales enablement is essential for modern market leaders.

Finally, the End-User segmentation—Professional Players, Amateur Players, and Youth Players—defines specific product needs and marketing strategies. Professional players are highly specialized buyers, often influenced by equipment managers and biomechanical analyses. They demand customization, lightweight materials, and often have short replacement cycles tied to sponsorship deals. Their purchasing is driven by marginal gains in performance and protection effectiveness under rigorous conditions. Marketing here relies heavily on athlete endorsements and performance data validation.

Amateur players represent a highly diversified group, ranging from serious college athletes to weekend recreational participants. This segment prioritizes durability, certified safety (NOCSAE standards in North America), and a reasonable price point. Bulk purchasing for teams and leagues is common, making B2B sales an important component. The Youth Players segment is driven by parental concern for safety and the need for frequent size adjustments. Products for this segment typically emphasize integrated ankle protection, bright colors for visibility, and ease of use, with marketing efforts focused on educational content about injury prevention and compliance with youth league rules.

Further detailed examination of the key players reveals a market dominated by multinational sports apparel giants (Nike, Adidas, Puma) who leverage vast distribution networks and heavy brand visibility. These companies utilize their scale to invest in large-scale material R&D, often setting industry standards. However, niche players like G-Form and Storelli have successfully carved out significant market share by focusing entirely on proprietary, reactive material technologies (e.g., G-Form's RPT) and specialized protection needs, respectively. Their success highlights the consumer willingness to pay a premium for perceived superior specialized safety features.

Competitive strategies among the top players focus on securing high-profile professional endorsements, rapidly integrating technological innovations like smart sensors and 3D printing into product lines, and expanding their footprint in high-growth regional markets, particularly Asia Pacific. Price wars are common in the basic plastic segment, while competition in the high-end carbon fiber market revolves around maximizing performance, minimizing weight, and providing superior custom fitting options. Continuous product iteration and patent filing related to impact absorption mechanics are vital for maintaining competitive advantage.

The ongoing trend of integrating eco-friendly and sustainable materials also represents a growing competitive factor. As consumer awareness of environmental impact increases, brands that can credibly market shin guards made from recycled plastics or sustainably sourced composites may gain a significant edge, particularly among younger, environmentally conscious consumers. This necessitates upstream collaboration with material suppliers committed to sustainable manufacturing practices. The future market success will be highly dependent on the ability of manufacturers to merge mandatory safety compliance with bespoke comfort and sustainable innovation.

The comprehensive market analysis reveals that while the core function of a shin guard remains unchanged, the methods for achieving optimal protection are undergoing a revolution. From basic plastic shells decades ago to today's highly engineered, data-collecting composites, the industry is steadily moving towards personalized, smart protective solutions. This transformation is not only enhancing player safety but also redefining the value proposition of athletic protective gear, justifying higher price points for elite and specialized products. The convergence of safety regulations, technological breakthroughs, and increasing global soccer participation ensures a stable and robust growth trajectory for the Soccer Shin Guards Market through the forecast period.

The detailed segmentation analysis further confirms that while broad market segments are necessary for volume, success is increasingly found in the specialization of product offerings. For example, focusing intensely on the unique needs of the women's soccer segment—which often requires different anatomical fits—or developing robust, child-proof guards for the burgeoning youth market, represents tactical opportunities for market penetration beyond competing directly with the dominant global brands in the mass market professional segment. Strategic market entrants and smaller innovators are advised to target these underserved demographic niches with differentiated technological solutions.

The long-term viability of market players will hinge on their responsiveness to regulatory evolution and their investment in R&D aimed at next-generation materials. For instance, the development of super-lightweight, non-Newtonian fluids or flexible ceramic composites for superior kinetic energy dispersion could fundamentally change the competitive hierarchy. Furthermore, companies that successfully monetize the data collected from smart shin guards, offering valuable performance and injury insights back to teams and players, will establish a strong competitive barrier, moving beyond simple product manufacturing to becoming integrated sports technology providers. This shift towards data services bundled with protective equipment is a critical future trend.

The geographical diversity of the market reinforces the need for tailored distribution strategies. In mature European markets, maintaining strong relationships with established retail chains and focusing on brand heritage and quality is paramount. In contrast, fast-growing APAC markets demand flexible pricing, localized digital marketing, and the establishment of scalable e-commerce infrastructure to capture rapidly expanding consumer bases who are often entering the market for the first time. Understanding regional regulatory differences, such as varying material testing standards, is essential for ensuring product compliance and market entry efficiency across borders.

In summary, the Soccer Shin Guards Market is characterized by a mature regulatory environment providing a stable demand floor, coupled with intense technological innovation driving premiumization and specialization at the high end. Successful market navigation requires a keen understanding of segment-specific needs, a commitment to cutting-edge material science, and strategic utilization of digital distribution channels for both sales and direct consumer engagement, ensuring players are equipped with the most advanced protective gear available for competitive soccer.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.