ID : MRU_ 443671 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

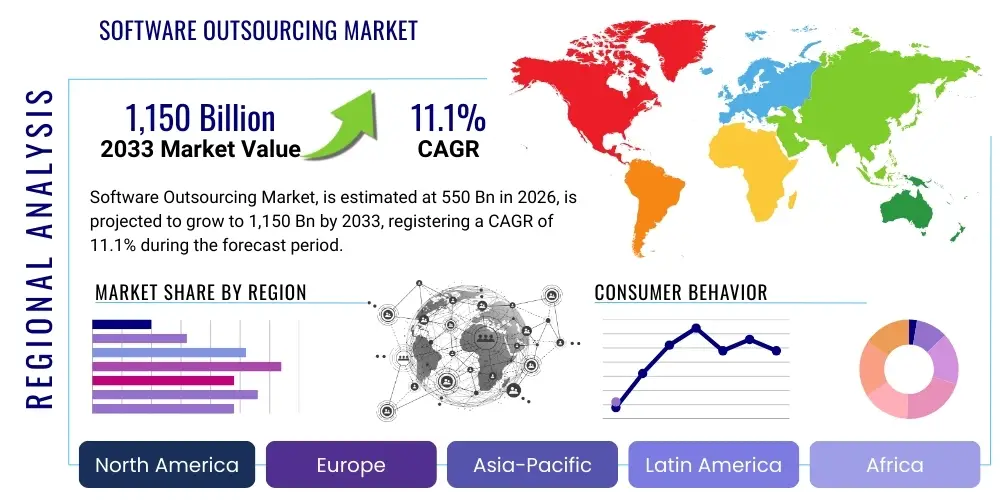

The Software Outsourcing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.1% between 2026 and 2033. The market is estimated at $550 Billion in 2026 and is projected to reach $1,150 Billion by the end of the forecast period in 2033.

The Software Outsourcing Market encompasses the practice of contracting out software development, maintenance, and support services to third-party providers, often located in geographically distant regions. This strategic business model allows enterprises, ranging from startups to Fortune 500 companies, to leverage specialized expertise, reduce operational overheads, and accelerate time-to-market for critical digital products. The core offerings include application development, system integration, cloud services management, quality assurance (QA), and IT infrastructure support. The market’s rapid expansion is fundamentally driven by the global shortage of highly specialized tech talent in developed economies and the imperative for organizations across all sectors—financial services, healthcare, retail, and manufacturing—to undergo comprehensive digital transformation.

Product descriptions within this domain are highly varied, covering everything from niche legacy system modernization projects to large-scale, end-to-end agile product development cycles utilizing cutting-edge technologies like artificial intelligence (AI), machine learning (ML), and blockchain. Major applications span enterprise resource planning (ERP) system customization, customer relationship management (CRM) platform development, mobile application creation, and robust cybersecurity solution implementation. Companies increasingly seek outsourcing partners capable of delivering not just code, but genuine strategic value, necessitating a shift from simple staff augmentation models to full managed services and collaborative product co-creation frameworks. The sophistication of these outsourced services ensures that businesses maintain competitive agility in a rapidly evolving technological landscape.

The primary benefits fueling market growth include substantial cost savings, enhanced resource flexibility, access to a global talent pool, and improved focus on core business competencies. By offloading complex technological challenges to specialized vendors, client organizations can reallocate internal capital and personnel toward innovation and strategic growth initiatives. Key driving factors include the escalating adoption of cloud computing platforms, the widespread demand for robust cybersecurity solutions, and the continuous evolution of development methodologies, particularly DevOps and serverless architectures. Furthermore, government initiatives in several developing nations promoting digital infrastructure and technological education have bolstered the supply side, making high-quality outsourcing accessible and reliable on a global scale, cementing its role as a vital component of modern corporate strategy.

The Software Outsourcing Market is experiencing significant acceleration, transitioning from purely cost-driven engagements to value-centric strategic partnerships focused on innovation and digital transformation efficiency. Key business trends indicate a strong move toward specialized vendor selection, where enterprises prioritize partners with deep vertical expertise (e.g., FinTech, HealthTech) and demonstrable capabilities in emerging technologies such as AI/ML and advanced data analytics. This shift is redefining the vendor-client relationship, moving toward collaborative agile models that integrate outsourcing teams deeply into the client’s internal operational structure, thereby improving transparency and alignment with overarching business objectives. Furthermore, regulatory compliance, particularly concerning data privacy like GDPR and CCPA, is becoming a primary differentiator, pushing providers to invest heavily in robust security frameworks and compliance certifications.

Regional trends reveal the continued dominance of established outsourcing hubs in India and Eastern Europe, though Latin America and Southeast Asia are rapidly gaining traction due to geographical proximity to key North American markets and specialized talent availability, respectively. North America remains the largest consumer market, driven by high demand for cutting-edge technologies and aggressive digital innovation cycles across major industries. The Asia Pacific region is expected to demonstrate the highest growth rate, fueled by substantial investments in digital infrastructure and the expansion of domestic enterprises seeking to scale quickly. Europe is characterized by a strong focus on nearshoring, particularly within the EU, valuing cultural alignment and real-time collaboration facilitated by reduced time zone differences, especially for high-security and regulated projects.

Segmentation trends highlight the increasing prominence of application development and maintenance (ADM) as the largest market segment, closely followed by IT infrastructure management and consulting services related to cloud migration. By pricing model, the fixed-price contract model is being gradually supplanted by the time-and-materials (T&M) and dedicated development team models, reflecting the preference for flexibility and scalability in agile project environments. In terms of end-users, the BFSI (Banking, Financial Services, and Insurance) sector and the Technology and Telecommunications industries remain the largest adopters, requiring constant technological updates and sophisticated security solutions. However, rapid digitalization in the healthcare and retail sectors is driving segment diversification, focusing specifically on patient management systems, e-commerce platforms, and supply chain optimization technologies.

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the Software Outsourcing Market typically center on automation risks, the demand for new skill sets, and the transformation of service delivery models. Users frequently ask if AI-powered tools will automate routine coding and quality assurance tasks, potentially diminishing the need for human developers in certain lower-level outsourcing roles. They also seek clarity on which areas will see the greatest AI integration—ranging from automated testing and code generation to advanced predictive analytics for project risk management. A significant concern revolves around the necessity for outsourcing vendors to rapidly acquire and integrate AI development expertise to remain relevant, shifting the focus from traditional programming to prompt engineering, model training, and ethical AI deployment. Expectations are high that AI will increase productivity and enable smaller, highly skilled teams to deliver complex projects faster, thereby raising the overall quality and strategic value of outsourced services.

The integration of AI technologies is fundamentally reshaping the competitive landscape of software outsourcing. AI tools, particularly Large Language Models (LLMs) and specialized coding assistants, are enabling unprecedented levels of efficiency in tasks such as debugging, boilerplate code generation, and automated documentation. This efficiency gain allows outsourcing providers to focus human capital on higher-value activities—complex problem solving, architectural design, and direct client engagement. Consequently, vendors who successfully deploy AI to streamline internal processes will gain a significant cost and speed advantage. However, this necessitates substantial investment in upskilling existing staff and recruiting specialized AI engineers, ensuring that the human element remains central to sophisticated software engineering challenges.

Furthermore, AI is not just a tool for enhancing existing services; it is becoming a core service offering itself. Clients increasingly seek outsourced teams capable of building and maintaining AI-powered products, including recommendation engines, computer vision systems, and complex predictive maintenance platforms. This demand for AI expertise is creating a premium tier of outsourcing providers who specialize in data science and MLOps. The long-term impact suggests a polarization: routine outsourcing tasks will become highly automated and lower cost, while strategic, complex, and innovative project outsourcing, centered on AI implementation, will command higher rates and require deeper, more integrated partnerships between the client and the vendor.

The Software Outsourcing Market is profoundly influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape the competitive dynamics and growth trajectory of the industry. Primary drivers include the relentless pressure on global corporations to digitally transform operations, necessitating access to specialized technological skills—particularly in cloud computing, cybersecurity, and data science—that are often scarce or prohibitively expensive internally. Concurrently, the proven ability of outsourcing to offer significant operational cost advantages, especially when leveraging optimized labor markets, remains a foundational catalyst for adoption. These factors are reinforced by the maturity of global communication infrastructure and agile development methodologies, making remote collaboration highly effective and reliable.

However, the market faces notable restraints that temper growth. Chief among these are escalating concerns related to data security, intellectual property (IP) protection, and maintaining regulatory compliance across diverse international jurisdictions. Clients often express hesitancy in transferring sensitive projects due to perceived risks associated with outsourcing vendors’ security protocols. Furthermore, managing cultural and linguistic differences, along with time zone disparities, continues to pose communication and project management challenges, potentially impacting project timelines and quality if not expertly mitigated. The increased competition and wage inflation in previously low-cost outsourcing destinations also put pressure on vendor margins and necessitate continuous innovation in delivery models.

Opportunities for future expansion are vast, primarily centered on niche specialization and geographical diversification. The explosive growth of sectors like IoT (Internet of Things), blockchain applications, and augmented/virtual reality (AR/VR) creates fertile ground for specialized outsourcing providers. Additionally, the strategic opportunity lies in evolving beyond basic transactional relationships to become genuine innovation partners, offering consulting and ideation services rather than just execution. The market is also seeing new geographical opportunities in emerging nearshoring destinations in Central and Eastern Europe and Latin America, providing compelling alternatives that balance cost savings with improved cultural alignment and proximity to major Western markets. These opportunities allow vendors to target specific high-value client segments with tailored, strategic offerings.

The Software Outsourcing Market is highly fragmented and segmented based on service type, deployment model, enterprise size, end-user industry, and geographical location, reflecting the diverse needs of client organizations globally. The core service segment, application development and maintenance (ADM), dominates the revenue share as enterprises constantly require updates, scaling, and modernization of their core business applications. The increasing complexity of IT environments has also significantly boosted the infrastructure management and managed security services segments. Analyzing these segments provides strategic insights into investment areas and competitive positioning, revealing a clear trend towards integrating multiple service offerings into comprehensive, end-to-end digital transformation packages tailored for specific industrial verticals.

Service types are further distinguished by the level of vendor involvement, ranging from staff augmentation, where external personnel temporarily join internal teams, to comprehensive project-based outsourcing, where the vendor manages the entire lifecycle of a development project. The choice of segmentation often depends on the client's internal resource availability, budgetary constraints, and the strategic importance of the software being developed. For instance, high-risk or mission-critical systems often demand dedicated teams and managed service agreements, whereas routine maintenance may be handled via transactional, fixed-price contracts. This granular segmentation allows market participants to refine their product portfolios to capture maximum value across the operational spectrum of potential clients.

Geographical segmentation remains critical, dividing the market primarily into offshore (distant location, lowest cost), nearshore (geographically proximate, better time zone alignment, often higher cultural compatibility), and onshore (local, highest cost, maximum control and communication ease). The blend of these delivery models, known as "hybrid sourcing," is gaining momentum as organizations seek to optimize cost efficiency while mitigating collaboration risks inherent in purely offshore models. Understanding these segmentation nuances is key for market sizing, forecasting, and developing targeted sales strategies that address the specific logistical and financial requirements of multinational corporations and regional businesses alike.

The Value Chain in the Software Outsourcing Market begins with upstream activities focused on talent acquisition, infrastructure development, and capability building. Upstream analysis involves examining how vendors acquire, train, and retain a highly skilled workforce, which forms the core asset of the industry. Key activities include setting up sophisticated recruitment pipelines, investing heavily in continuous technical education and certification (especially in emerging technologies like cloud and AI), and establishing robust secure development environments. Strategic vendor positioning at this stage involves securing access to specialized talent pools globally and maintaining state-of-the-art technological infrastructure, ensuring compliance with international quality standards (e.g., ISO, CMMI) necessary to attract major global clients. High-quality upstream inputs directly translate into superior delivery capabilities downstream.

The midstream segment centers on the core service delivery process, encompassing project initiation, requirement analysis, software development, testing, and deployment. This is where value is primarily created through efficient execution methodologies, such as Agile and DevOps, combined with effective project management and client communication protocols. Distribution channels, both direct and indirect, play a crucial role here. Direct channels involve proprietary sales forces and relationship managers negotiating contracts directly with end-user enterprises, ensuring tailored solutions and deep integration. Indirect channels utilize strategic alliances, partnerships with system integrators, and collaborations with major cloud providers (like AWS, Azure, Google Cloud), allowing vendors to reach broader markets and participate in larger, integrated IT transformation projects driven by these global partners.

Downstream analysis focuses on post-implementation services, client relationship management, and value realization. This includes application maintenance, ongoing technical support, continuous system optimization, and advisory services aimed at future technology roadmapping. Customer retention and maximizing the lifetime value of the client relationship are paramount downstream objectives. Successful downstream activities often lead to contract extensions, expansion into new projects, and valuable word-of-mouth referrals. The emphasis shifts from merely delivering code to acting as a long-term strategic advisor, continually seeking opportunities to enhance the client's digital capabilities, thereby cementing the vendor’s position as an indispensable partner in the client’s ecosystem.

The potential customer base for the Software Outsourcing Market is exceptionally broad, spanning nearly every economic sector and ranging dramatically in size and technological maturity. Historically, the Banking, Financial Services, and Insurance (BFSI) sector has been the most significant consumer, driven by the critical need for constant system modernization, robust security infrastructure, and compliance with rapidly changing financial regulations. These institutions require outsourcing services for core banking platform development, fraud detection systems utilizing AI, and customer-facing digital applications. Similarly, the Technology and Telecommunications sector heavily utilizes outsourcing to manage fluctuating demand for specialized product development, network infrastructure support, and scaling consumer-facing digital services rapidly without massive internal overhead.

Beyond the traditional IT heavyweights, the Healthcare and Life Sciences sector represents a rapidly expanding customer segment, fueled by digitalization mandates such as electronic health records (EHR) management, telemedicine platform development, and complex data analytics for clinical trials. These customers seek highly specialized vendors capable of navigating strict regulatory standards like HIPAA and GDPR, prioritizing data privacy and system reliability above all else. Retail and E-commerce entities also constitute major buyers, focusing on outsourced solutions for developing scalable e-commerce platforms, optimizing supply chain logistics using IoT, and implementing personalized customer experience technologies, particularly those involving advanced data modeling and cloud integration.

In essence, any organization facing a shortage of specialized internal IT talent, seeking significant cost efficiencies, or needing rapid scalability to meet market demands qualifies as a high-potential customer. Small and Medium-sized Enterprises (SMEs) increasingly leverage outsourcing to access enterprise-level technology capabilities that would otherwise be unaffordable, often utilizing standardized cloud-based solutions managed by external providers. Large enterprises, conversely, use outsourcing to manage complex legacy systems, accelerate large-scale transformation projects, and establish global centers of excellence without the heavy fixed costs associated with permanent international expansion.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $550 Billion |

| Market Forecast in 2033 | $1,150 Billion |

| Growth Rate | 11.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tata Consultancy Services (TCS), Infosys Limited, Wipro Limited, Cognizant Technology Solutions, HCL Technologies, Accenture, IBM Corporation, Capgemini, NTT Data, DXC Technology, Genpact, Tech Mahindra, EPAM Systems, Atos SE, Globant, Luxoft, Mindtree, Persistent Systems, L&T Technology Services, Mphasis |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the Software Outsourcing Market is defined by a rapid adoption of modern development paradigms and cloud-native solutions, aiming for enhanced agility, scalability, and security. Cloud computing platforms, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), form the foundational technology stack for the majority of outsourced projects, enabling vendors to offer Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS) management. This shift necessitates deep expertise in multi-cloud and hybrid-cloud architectures, as clients require flexible solutions that integrate seamlessly with existing legacy systems while leveraging the scalability of public cloud environments. Containerization technologies, specifically Docker and Kubernetes, are also critical, facilitating microservices architecture deployment and standardized operational environments across different client projects.

Furthermore, the widespread adoption of DevOps practices, which integrate development and operations teams, is central to the modern outsourcing value proposition. Technologies that support Continuous Integration/Continuous Delivery (CI/CD) pipelines, automated testing frameworks, and infrastructure as code (IaC) tools are standard requirements for competitive outsourcing providers. This methodological shift ensures rapid iteration cycles and minimizes deployment risk, directly contributing to faster time-to-market for outsourced solutions. Beyond standard enterprise technologies, niche capabilities in distributed ledger technology (blockchain), particularly for supply chain transparency and financial settlements, and specialized data technologies like advanced business intelligence (BI) tools and large-scale data warehousing solutions, are becoming key differentiators for specialized vendors serving complex industry requirements.

The technological evolution is further propelled by the indispensable role of Artificial Intelligence (AI) and Machine Learning (ML). Outsourcing firms are deploying AI not only within client products (e.g., predictive analytics, computer vision) but also internally to optimize their own delivery processes. Robotic Process Automation (RPA) tools are utilized to automate repetitive back-office and maintenance tasks, freeing up human resources for more complex, creative work. Cybersecurity technology remains paramount; thus, providers must possess cutting-edge expertise in SecDevOps, threat detection platforms, and sophisticated identity and access management (IAM) solutions. The overall technological landscape mandates continuous investment and strategic partnerships with technology platform creators to maintain a competitive edge in delivering next-generation digital services.

The primary factor driving market growth is the global technological skills gap, particularly in specialized fields like Artificial Intelligence (AI), cloud architecture, and advanced cybersecurity, coupled with the mandatory need for rapid digital transformation across all major industries to maintain competitive parity and operational efficiency.

The choice impacts cost, communication, and cultural compatibility. Offshore offers maximum cost savings but higher potential communication barriers; Nearshore balances moderate costs with time zone alignment and cultural proximity; Onshore provides maximum control, minimal communication friction, but at the highest cost structure.

Major risks include data security breaches, intellectual property (IP) theft, and poor project management resulting from misalignment. Mitigation strategies involve stringent contractual agreements, mandatory adherence to global security standards (e.g., ISO 27001), and implementing transparent, agile project management methodologies with strict governance oversight.

The Asia Pacific (APAC) region is forecasted to exhibit the highest Compound Annual Growth Rate (CAGR) due to rapid industrial digitalization, substantial government investment in IT infrastructure, and the continuous development of local outsourcing capabilities expanding beyond traditional service offerings.

AI is not replacing roles entirely but is fundamentally transforming them by automating routine tasks (like boilerplate coding and QA). Vendors must adapt by rapidly upskilling their workforce in AI engineering, MLOps, and strategic consulting to focus on higher-value activities that AI tools currently augment, rather than replace.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.