ID : MRU_ 442177 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

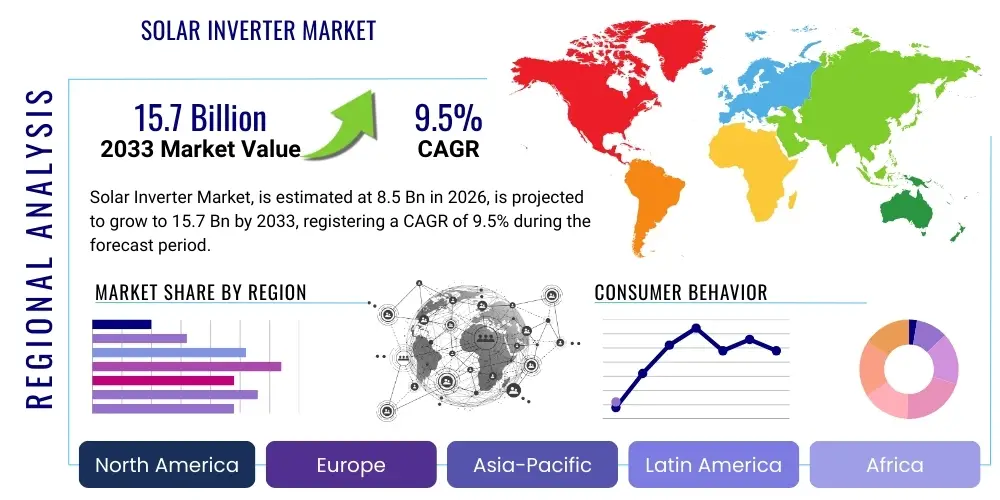

The Solar Inverter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 15.7 Billion by the end of the forecast period in 2033.

The solar inverter market constitutes the backbone of solar photovoltaic (PV) systems, serving the critical function of converting the direct current (DC) generated by solar panels into usable alternating current (AC) power for residential, commercial, and utility-scale applications. Inverters are not merely conversion devices; modern variants include sophisticated monitoring, safety features, grid synchronization capabilities, and increasingly, smart grid interaction tools. The increasing global imperative to transition toward renewable energy sources, driven by climate change mitigation goals and energy security concerns, is the primary accelerator for this market. Furthermore, falling PV module costs have significantly improved the economic viability of solar installations worldwide, thereby boosting the demand for high-efficiency, reliable inverter solutions that maximize energy harvesting and reduce system downtime.

Major applications of solar inverters span across three key segments: residential installations, characterized by microinverters and smaller string inverters focusing on panel-level optimization and safety; commercial installations, which utilize medium-sized string and central inverters tailored for roof-mounted systems on businesses and industrial facilities; and utility-scale projects, which predominantly rely on large central inverters capable of handling hundreds of megawatts of power generation while ensuring robust grid stability and compliance. The benefits derived from advanced solar inverters are numerous, including enhanced system efficiency (maximizing the yield from sunlight), improved operational longevity through advanced thermal management, and sophisticated fault detection capabilities. Hybrid inverters, which integrate battery storage management, are also rapidly gaining traction, offering critical flexibility for energy self-consumption and grid resilience.

Driving factors for the market expansion include supportive government policies such as renewable energy targets, feed-in tariffs, and tax credits implemented across North America, Europe, and Asia Pacific. Technological advancements, particularly in wide-bandgap semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), are enabling the development of lighter, smaller, and significantly more efficient inverter designs, reducing balance-of-system costs and enhancing overall system performance. The accelerating trend of distributed energy generation and the need for smart grid integration capabilities are further compelling utilities and system integrators to adopt advanced inverter technologies that can manage complex energy flows and provide ancillary services to the grid, ensuring stable and reliable power supply.

The solar inverter market is defined by rapid technological evolution, intense competition, and favorable regulatory environments globally. Key business trends indicate a strong shift towards high-power string inverters (100kW+ range) for commercial and small utility-scale projects, largely displacing traditional central inverters due to reduced installation complexity, better fault isolation, and lower maintenance costs. The integration of Energy Storage Systems (ESS) is a dominant trend, driving significant growth in the hybrid inverter segment, which is engineered to manage both PV power generation and battery charging/discharging cycles, crucial for maximizing self-consumption in regions with volatile electricity pricing or high renewable penetration. Furthermore, cybersecurity and robust data communication protocols are emerging as critical differentiators, especially as inverters become key nodes in the smart grid infrastructure, necessitating secure remote monitoring and control capabilities.

Regionally, Asia Pacific, led by China and India, remains the dominant market in terms of installed capacity due to aggressive national renewable energy targets and massive utility-scale deployment programs. However, North America and Europe are exhibiting high growth rates driven by the increasing demand for high-value microinverters and hybrid systems in the residential sector, focusing heavily on aesthetic integration, resilience, and compliance with stringent grid codes (e.g., Module Level Power Electronics, or MLPE, requirements). The Middle East and Africa (MEA) are emerging as high-potential regions, leveraging abundant solar resources and significant infrastructure investment to launch large-scale PV projects, thereby creating substantial demand for robust, high-temperature tolerant central inverters tailored for harsh desert environments.

Segment trends highlight the growing polarization between MLPE solutions (microinverters and optimizers) and high-power string inverters. Residential consumers prioritize MLPE for enhanced safety, granular monitoring, and maximized yield under shading conditions, while the commercial and utility sectors increasingly favor powerful string solutions that streamline deployment and maintenance processes. The rise of multi-MPPT (Maximum Power Point Tracking) technology is enhancing the flexibility of string inverters, allowing them to perform efficiently across complex roof layouts or challenging terrain. The three-phase inverter segment, crucial for connecting to commercial and utility grids, is experiencing innovation focused on higher power density and seamless integration with intelligent grid management systems, thereby supporting the massive influx of intermittent solar power into existing electrical infrastructure without compromising stability or reliability.

Analysis of common user questions regarding AI's influence on the solar inverter market reveals major themes centering on predictive maintenance, optimization capabilities, and system resilience. Users frequently ask: "How can AI predict inverter failures before they happen?", "Will AI optimize my energy yield more effectively than traditional MPPT?", and "Does AI-enabled grid management reduce the complexity of integrating solar farms?" These questions highlight high expectations for AI to move beyond basic monitoring toward proactive, performance-enhancing management. The key concerns revolve around data privacy, the cost of implementing AI infrastructure, and the need for standardized communication protocols to ensure interoperability between AI platforms and diverse inverter hardware across varying operational environments, from residential setups to massive utility parks.

AI is fundamentally transforming solar inverter operations by enhancing fault detection accuracy and reducing operational expenditures. Machine learning algorithms analyze vast datasets encompassing historical performance, environmental factors (temperature, dust, irradiation), and electrical parameters (voltage, current, frequency) to establish highly accurate baseline models. Any deviation from these baselines triggers alerts for potential issues, enabling system operators to perform targeted, preventative maintenance rather than relying on reactive fixes. This shift minimizes downtime, which is critical for utility-scale projects where maximizing uptime directly translates to significant revenue generation. Furthermore, AI facilitates complex diagnostics, distinguishing between temporary system anomalies and genuine hardware failures, thus preventing unnecessary technician dispatches and lowering service costs substantially.

In terms of performance optimization, advanced AI systems are capable of refining Maximum Power Point Tracking (MPPT) algorithms in real time, going beyond standard static or deterministic approaches. By considering immediate weather forecasts, panel degradation patterns, and ambient conditions, AI-driven MPPT can dynamically adjust inverter settings to extract the maximum possible energy yield under highly variable and non-uniform conditions, such as those caused by partial shading or module mismatch. Crucially, AI is pivotal in the integration of solar farms into the smart grid. AI algorithms predict localized power generation spikes and dips, enabling inverters, through advanced communication interfaces, to provide rapid frequency and voltage regulation services, thereby stabilizing the grid and allowing for higher penetration levels of renewable energy without jeopardizing system integrity or reliability.

The solar inverter market is profoundly influenced by a complex interplay of Drivers, Restraints, and Opportunities, which collectively constitute the Impact Forces shaping its trajectory. The dominant drivers stem from global governmental mandates pushing for decarbonization, the favorable economics of solar PV systems achieving grid parity in numerous regions, and significant improvements in power electronics efficiency. These forces create a consistently high baseline demand for conversion technology. However, the market faces notable restraints, particularly the intense price erosion due to commoditization pressure, short product lifecycles necessitated by continuous technological leaps, and the ongoing challenge of managing grid stability as intermittent solar power penetration levels escalate, requiring ever more sophisticated and costly grid-tie compliance features.

Key drivers include rapidly declining solar PV module costs, which make solar energy deployment financially attractive across all sectors, thereby increasing the installation base requiring inverters. Furthermore, supportive regulatory frameworks, such as ambitious national renewable energy targets (e.g., India's 500 GW goal or the EU's Renewable Energy Directive), significantly bolster market confidence and investment in manufacturing and deployment capacity. The technological shift towards higher voltage systems (e.g., 1500V DC) in utility-scale installations necessitates robust and advanced central and high-power string inverters, driving innovation in power semiconductor technology and thermal management systems to handle increased power density and efficiency demands without compromising reliability in extreme operating conditions.

Conversely, significant restraints hinder growth potential. The market is highly saturated, leading to aggressive pricing strategies, particularly among APAC manufacturers, which pressures profit margins for established western players and necessitates constant cost reduction. Additionally, the shortage and volatility in the supply chain for critical semiconductor components, particularly SiC and high-grade microcontrollers, pose challenges to meeting surging demand and maintaining competitive pricing. Opportunities for future growth are rooted in the proliferation of hybrid inverters integrating battery storage, offering solutions for enhanced energy resilience and self-consumption. The nascent but growing market for utility-scale green hydrogen production, requiring massive, specialized power conditioning equipment, also presents a substantial long-term opportunity for high-power inverter manufacturers to diversify their application portfolio beyond traditional grid-connected PV systems.

The Solar Inverter Market is strategically segmented based on factors such as product type, phase, and end-use application, reflecting the diverse requirements across residential, commercial, and utility sectors. Product type segmentation, which includes Central, String, Microinverters, and Hybrid Inverters, defines performance capabilities and suitability for varying scale and complexity of solar arrays. Central inverters dominate very large utility projects due to their high capacity and centralized design, while microinverters and hybrid systems show the fastest growth trajectory, driven by the residential and commercial need for module-level optimization, redundancy, and integration with energy storage. The phase segmentation (single-phase and three-phase) is essential for electrical compliance, with single-phase systems typical for residential applications and three-phase systems mandatory for connecting to medium and high-voltage commercial and utility grids, requiring specialized synchronization features.

End-use segmentation distinguishes the market based on the scale of deployment and typical operational demands. The Utility-Scale segment holds the largest market share by volume, characterized by stringent grid code requirements, long operational lifecycles, and a focus on minimizing Levelized Cost of Energy (LCOE), primarily driving demand for cost-effective, high-efficiency central and large string inverters. The Commercial segment focuses on medium-sized systems often deployed on rooftops or carports, demanding robust, high-power density string inverters that minimize installation footprint and maximize yield under variable shading conditions common in urban settings. The Residential segment prioritizes safety, ease of installation, and system aesthetics, heavily favoring MLPE solutions like microinverters and hybrid inverters that facilitate home energy management and resilience during grid outages.

The evolving technology landscape is blurring some segmentation lines, particularly with the introduction of high-power string inverters (300kW+) that challenge the dominance of central inverters in the mid-size utility sector. Furthermore, the mandatory requirement for advanced grid-forming capabilities in new inverters, especially in high-penetration renewable markets like Australia and parts of Europe, is creating a premium tier within all segments. This trend forces manufacturers to embed complex software and communication hardware, moving the inverter from a simple DC-AC converter to an intelligent grid asset capable of providing reactive power support, voltage regulation, and black start capabilities, thereby justifying increased pricing and differentiation based on software excellence rather than merely hardware efficiency.

The value chain of the solar inverter market is complex, spanning from the manufacturing of specialized raw materials and components to final installation, distribution, and long-term operations and maintenance (O&M). Upstream activities are dominated by the procurement and production of critical high-power electronic components, including Insulated Gate Bipolar Transistors (IGBTs) or Silicon Carbide (SiC) MOSFETs, microcontrollers, specialized magnetics (inductors and transformers), and cooling components. These foundational inputs heavily influence the cost, efficiency, and size of the final inverter product. Companies often form strategic partnerships or engage in long-term supply agreements with semiconductor manufacturers to ensure component quality and mitigate supply chain risks, particularly given the current global scarcity of advanced power electronics and microprocessors crucial for the smart functions of modern inverters.

Downstream analysis focuses on the distribution, integration, and end-user adoption phases. Distribution channels are highly fragmented, involving a mix of direct sales to large utility developers (for central inverters), original equipment manufacturers (OEMs), specialized solar distributors, and certified installers (for residential and commercial string/microinverters). The direct channel is vital for maintaining control over pricing and service quality for large-scale, high-margin projects. Conversely, the indirect channel, relying on electrical wholesalers and solar installers, provides necessary local market penetration and support for the geographically dispersed residential and small commercial segments, necessitating robust training and certification programs from manufacturers to ensure proper product deployment and maintenance standards.

Installation and O&M services form a crucial part of the downstream value chain, impacting the long-term profitability and reputation of manufacturers. Advanced inverters, especially MLPE and hybrid systems, require sophisticated installation techniques and dedicated monitoring software. Post-sale services, including remote diagnostics, firmware updates, and rapid component replacement, are becoming significant competitive differentiators. A well-optimized value chain ensures component supply resilience, efficient manufacturing assembly lines, effective inventory management across diverse global markets, and the provision of localized, reliable technical support, ultimately driving higher customer satisfaction and maximizing the lifetime energy production (LCOE) of the installed PV systems.

The primary customers for solar inverters are broadly categorized into three distinct end-user groups corresponding to the scale of deployment: Utility-Scale Developers, Commercial & Industrial (C&I) Enterprises, and Residential Homeowners. Utility-Scale Developers, including independent power producers (IPPs) and large energy corporations, are the biggest volume purchasers, focusing on minimizing upfront capital expenditure and maximizing LCOE. They require highly reliable, standardized central or high-power string inverters, often procured through large, multi-year framework agreements. Their purchasing decisions are driven primarily by efficiency ratings, proven reliability in harsh environments, grid compliance certifications, and competitive warranties offered by top-tier manufacturers known for robust after-sales support and bankability across international financing institutions.

Commercial and Industrial (C&I) Enterprises, such as manufacturing plants, retail chains, data centers, and educational institutions, represent a rapidly growing segment, driven by the desire for reduced operating expenses, energy independence, and corporate sustainability goals. These customers prioritize solutions that offer superior system performance, flexibility for complex rooftop geometries, and rapid return on investment (ROI). They typically purchase medium to large string inverters or small central inverters, often integrating them with demand-side management systems and increasingly, battery storage solutions managed by hybrid inverters, thereby seeking comprehensive energy management systems that provide load shifting capabilities and resilience against power quality issues.

Residential Homeowners and smaller system integrators focusing on the residential market are characterized by a focus on safety, system monitoring simplicity, aesthetic considerations, and integration with home automation ecosystems. This segment shows high adoption rates for Microinverters and Hybrid Inverters due to the enhanced safety (Module Level Power Electronics, or MLPE), optimized energy harvest under shading, and the growing necessity for battery backup solutions, particularly in regions prone to grid instability or where self-consumption mandates are prevalent. Purchasing decisions here are heavily influenced by installer recommendations, brand reputation, warranty length, and the ease of monitoring via user-friendly smartphone applications, often treating the inverter as a crucial smart home appliance rather than solely an electrical component.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 15.7 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Huawei, Sungrow, SMA Solar Technology, Solaredge Technologies, ABB, Enphase Energy, Fimer, Delta Electronics, Siemens, TBEA Sunoasis, Ginlong Technologies, GoodWe, Power Electronics, KSTAR, Growatt, SolarMax, Chint Power, Fronius International, Schneider Electric, RefuSol |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution within the solar inverter market is accelerating, driven by the need for higher efficiencies, smaller footprints, enhanced grid management capabilities, and improved integration with battery storage. A pivotal development is the increased adoption of wide-bandgap semiconductor materials, primarily Silicon Carbide (SiC) and, to a lesser extent, Gallium Nitride (GaN). SiC MOSFETs replace traditional Silicon IGBTs, enabling inverters to operate at much higher switching frequencies and temperatures while significantly reducing energy losses during the conversion process. This technological leap results in smaller, lighter inverters with higher power density and better thermal performance, crucially improving reliability in high-heat environments typical of solar installations, and contributing to overall system cost reduction by requiring less passive componentry.

Another major technological trend is the proliferation of Maximum Power Point Tracking (MPPT) advancements, moving toward highly localized and distributed tracking. Microinverters and power optimizers (Module Level Power Electronics, or MLPE) ensure that each individual solar panel operates at its optimal power point, mitigating power loss caused by partial shading, soiling, or module mismatch, thereby maximizing overall energy harvest. Modern string inverters now incorporate multiple MPPT channels (e.g., six to twelve MPPTs) to provide similar benefits on a string-level basis, enhancing flexibility and performance on complex or unevenly oriented rooftops and mitigating the traditionally centralized failure point of older inverter architectures, increasing system resilience and redundancy across diverse installation sites.

Furthermore, the focus on smart grid integration has led to the development of sophisticated communication protocols (e.g., SunSpec Modbus, IEEE 2030.5) and advanced inverter functions, notably "grid-forming" capabilities. Unlike traditional "grid-following" inverters that rely on the presence of a stable grid voltage and frequency, grid-forming inverters can autonomously establish and maintain grid voltage and frequency, crucial for supporting microgrids, operating in islanded mode, and stabilizing weak utility grids burdened by high renewable penetration. This advanced capability, often coupled with AI-driven software, positions the inverter as a vital asset for future energy system stability, facilitating ancillary services like reactive power compensation and inertia contribution, which are increasingly mandated by global grid regulatory bodies and significantly raising the technical barrier to entry for manufacturers.

String inverters convert DC power from a series of panels (a string) at a central point. Microinverters convert DC to AC at the individual panel level (Module Level Power Electronics), offering enhanced safety, better performance under shading, and granular monitoring, primarily used in residential settings.

Hybrid inverters are significantly boosting market growth by facilitating the seamless integration of solar PV with battery energy storage systems (ESS). This enables optimized self-consumption, grid resilience (backup power), and participation in virtual power plants (VPPs), driven by increasing global mandates for energy storage.

SiC replaces traditional silicon components, allowing inverters to operate at higher efficiencies, faster switching frequencies, and higher temperatures. This results in smaller, lighter, and more reliable inverter designs with increased power density and lower cooling requirements, reducing overall system costs.

The Asia Pacific (APAC) region, primarily driven by massive utility-scale deployment programs in China and India, currently holds the largest share of the global solar inverter market volume and installed capacity, supported by strong government renewable energy targets.

Yes, 1500V DC system architecture is rapidly becoming the industry standard for new utility-scale solar projects globally. This higher voltage reduces electrical losses, optimizes conductor sizing, and allows for greater power harvesting, significantly improving the Levelized Cost of Energy (LCOE) compared to older 1000V systems.

The technological landscape is also heavily influenced by the imperative for grid modernization. As the penetration of solar PV increases, especially in decentralized environments, inverters are required to possess sophisticated reactive power control capabilities, fault ride-through functions, and the ability to communicate seamlessly with utility control centers. This convergence of power electronics and information technology (IT) is creating a demand for smart inverters that comply with evolving global standards, such as IEEE 1547 in North America and various European grid codes. Compliance often necessitates integrated data loggers, advanced metering infrastructure, and robust cybersecurity features to protect critical energy infrastructure from cyber threats. Manufacturers who successfully integrate these complex software and hardware features are gaining a competitive advantage over those focused solely on hardware efficiency improvements. The movement towards modularity, allowing for easier maintenance and scalability, is also a key design consideration, particularly in the high-power string segment where redundancy and rapid serviceability are paramount for asset owners. These comprehensive requirements ensure that the inverter market remains dynamic, focusing on continuous innovation far beyond simple DC-AC conversion, positioning the device as a crucial, intelligent component of the modern grid architecture.

Furthermore, financing and insurance bankability are powerful, unspoken impact forces in the solar inverter market. Large utility projects require components that are highly reliable and guaranteed by manufacturers with substantial financial stability. This preference often favors established Tier 1 companies, despite potentially higher initial costs, because their inverters are easier to finance and insure over the project's typical 25-year lifespan. This dynamic creates a high barrier to entry for smaller, innovative firms unless they can secure strong strategic partnerships or demonstrate exceptional field performance data. The warranty duration and terms are critical factors, as failures in large-scale systems can lead to massive revenue losses. Consequently, the competitive landscape is not just about price and efficiency, but heavily weighted toward demonstrable reliability, robust quality control, and the long-term solvency of the manufacturer, compelling manufacturers to invest heavily in rigorous testing and global service networks to meet investor confidence requirements and establish enduring market credibility within the risk-averse environment of large-scale renewable energy infrastructure development globally.

The residential segment, while smaller in volume than utility scale, drives innovation in user-experience and safety standards. The rise of integrated home energy management systems (HEMS) mandates that inverters communicate effectively not just with the grid, but also with smart appliances, electric vehicle (EV) chargers, and home battery storage units. This necessitates proprietary software interfaces and open application programming interfaces (APIs) to ensure seamless data exchange and energy flow prioritization based on homeowner preferences, such as maximizing EV charging during peak solar generation hours or reserving battery capacity for expected night-time use. Safety mandates, particularly relating to rapid shutdown protocols (required to ensure safety for first responders), have been a major factor accelerating the adoption of MLPE technologies, creating a premium market where technological sophistication and compliance are valued over simple low cost, fundamentally altering the product design requirements and market dynamics for residential inverter solutions across developed economies globally.

In the context of the DRO & Impact Forces, technological standardization presents both a restraint and an opportunity. While evolving global grid codes (e.g., in Germany, California, and Australia) mandate enhanced features that increase complexity and component costs (restraint), adherence to these advanced standards creates significant differentiation (opportunity). Manufacturers who invest early in meeting stringent requirements, such as those related to voltage and frequency regulation, gain access to high-value markets where utilities prefer proven, compliant solutions that minimize grid integration risk. This regulatory push elevates the importance of software engineering and testing certification within the inverter value proposition, shifting competition from hardware pricing wars toward specialized technical capability and demonstrable software competence in managing complex grid interactions across diverse operational scenarios and varying regulatory jurisdictions.

The segmentation based on power output is becoming increasingly critical for market strategy. Ultra-high-power string inverters (over 300 kW), often utilized in modular building blocks for utility projects, require specialized thermal management solutions, such as liquid cooling, to maintain performance and reliability. The integration of advanced cooling techniques is a technological driver in itself, allowing manufacturers to achieve unprecedented power density and minimize inverter footprint on solar farms, reducing land use and installation costs. Simultaneously, the microinverter market is pushing miniaturization and enhanced reliability, often achieved through rigorous component selection and conformal coating processes to ensure longevity in harsh, rooftop environments. This ongoing power density race, whether through increasing size for utility or decreasing size for residential, ensures capital expenditure remains high for research and development, compelling market players to continuously refine their hardware and software architectures to maintain competitiveness and relevance across specialized end-use applications and geographical markets worldwide.

Analyzing the Value Chain further, the pressure on manufacturers to reduce the embodied carbon of their products is intensifying, driven by environmental, social, and governance (ESG) investing mandates. This downstream pressure impacts upstream decisions, forcing inverter manufacturers to seek out ethically sourced components, optimize material usage, and establish end-of-life recycling programs for electronic waste. Furthermore, the reliance on high-quality component suppliers for semiconductors (SiC/GaN) located primarily in Asia presents a geopolitical risk that major manufacturers must mitigate through diversification or near-shoring strategies, impacting the supply chain stability and logistics costs. The transition towards digital twinning and highly automated manufacturing processes, leveraging robotics and IIoT (Industrial Internet of Things), is essential for maintaining cost efficiency while simultaneously ensuring the highest levels of quality control and traceability, which are crucial for winning large-scale, long-term contracts with utility clients who demand flawless operational performance and minimal risk exposure over decades of service life.

For potential customers in the Commercial & Industrial sector, the shift toward maximizing self-consumption is paramount. Many C&I facilities operate during peak solar hours, making immediate use of generated power economically advantageous. The demand here centers on highly flexible string inverters that can handle asymmetrical loading and complex system configurations, often incorporating smart power sensors and load management software to dynamically adjust power output based on real-time facility energy demand and fluctuating utility rates. The integration capability with existing Building Management Systems (BMS) is a non-negotiable requirement for this customer base, requiring open communication protocols and certified interfaces to ensure the solar system operates harmoniously within the larger ecosystem of enterprise energy infrastructure, thereby making solution providers who offer comprehensive, integrated energy platforms highly attractive to these complex commercial customers globally.

The AI impact extends critically into the warranty and service domain. By using machine learning models to analyze failure patterns across thousands of deployed units, manufacturers can pinpoint design flaws, rapidly iterate on future product generations, and offer more precise warranty coverage based on predicted operational lifespans rather than generic timeframes. This predictive capability reduces manufacturers' warranty risk exposure while simultaneously offering asset owners enhanced certainty regarding system performance over the long term. This data-driven approach is transforming O&M contracts from simple reactive service agreements into proactive, performance-guarantee contracts, where the inverter's smart features and connectivity become central to the value proposition, providing a clear competitive edge to those companies that successfully monetize their extensive field data through intelligent analytical platforms and optimized service delivery models.

In regional terms, Latin America's market acceleration is highly dependent on addressing infrastructure challenges, particularly weak grid stability in rural areas. This weakness creates a specific need for inverters capable of handling voltage fluctuations, providing reactive power support under extreme conditions, and operating reliably in challenging electrical environments. Consequently, manufacturers targeting this region must offer products with robust design specifications and certification for local grid standards, often requiring modifications to standard global models. Moreover, the prevalence of distributed generation mandates, such as net metering schemes in Brazil and Mexico, is fostering growth in the residential and small commercial sectors, creating demand for cost-effective, easily installed string inverters that comply with local utility interconnection rules, necessitating agile manufacturing and localized technical support capabilities to capitalize effectively on these regional growth pockets.

The global competitive landscape remains focused on innovation in modularity and ease of installation. For utility-scale deployment, modular central and high-power string inverters that can be quickly commissioned and replaced reduce construction time and minimize long-term O&M complexity. Standardization of connectors, mounting systems, and commissioning software across product lines is a continuous improvement focus area. This commitment to simplified logistics and rapid deployment is a critical commercial driver, especially in projects where stringent timelines must be met to capture tax credit deadlines or Power Purchase Agreement (PPA) start dates. Therefore, the most successful manufacturers are those that view the entire product ecosystem—from packaging and logistics to commissioning and monitoring—as part of the overall value delivered to the system owner, rather than just focusing narrowly on the technical specifications of the power conversion stage of the solar inverter.

The continued evolution of the Hybrid Inverter segment is not solely driven by battery storage, but also by vehicle-to-grid (V2G) technology readiness. As electric vehicles (EVs) become mobile energy storage units, hybrid inverters are being designed with bidirectional capabilities to manage power flow between the home, solar array, stationary battery, and the EV. This nascent V2G compatibility is a significant long-term opportunity, positioning the solar inverter as the central energy traffic controller for the entire electrified home ecosystem. Manufacturers who successfully integrate these complex bidirectional power electronics and software controls today are strategically positioning themselves for future dominance in the rapidly converging residential solar, storage, and mobility markets, thereby defining the next generation of smart energy management and contributing significantly to the expansion of the market size and value proposition across major developed markets globally over the forecast period.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.