ID : MRU_ 441415 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

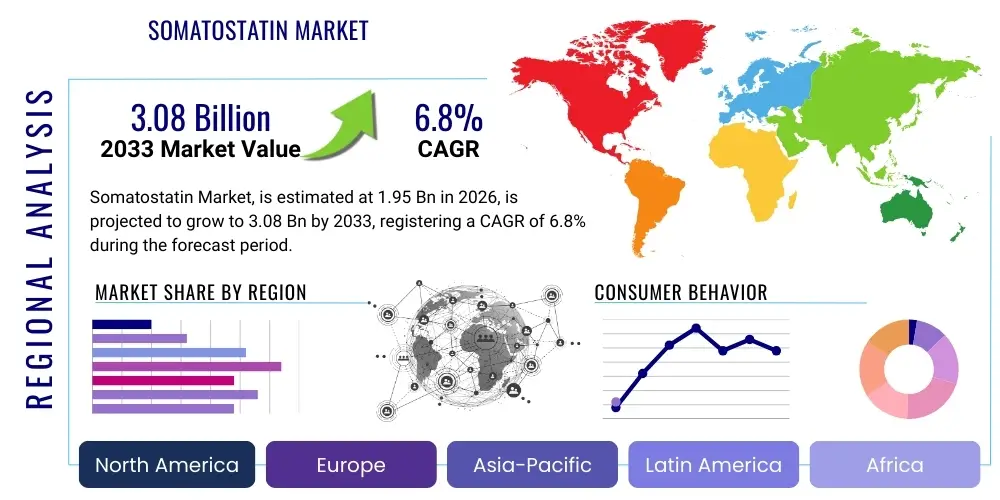

The Somatostatin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.95 Billion in 2026 and is projected to reach USD 3.08 Billion by the end of the forecast period in 2033.

The Somatostatin Market encompasses the global trade and utilization of the peptide hormone somatostatin and its synthetic analogs, primarily used in the management and treatment of neuroendocrine tumors (NETs), acromegaly, and specific types of gastrointestinal bleeding. Somatostatin, also known as growth hormone inhibiting hormone (GHIH), acts broadly to inhibit the secretion of various hormones, including growth hormone, insulin, glucagon, and gastrin. This inherent inhibitory capability makes its analogs, such as octreotide and lanreotide, indispensable therapeutic agents in oncology and endocrinology.

These synthetic analogs are preferred over the natural hormone due to their prolonged half-life and enhanced stability, providing significant advantages in chronic disease management. Major applications revolve around controlling the symptoms associated with NETs, particularly carcinoid syndrome, by reducing excessive hormone secretion. Furthermore, they are crucial in normalizing growth hormone levels in patients suffering from acromegaly, a condition resulting from pituitary tumors. The benefits derived from these treatments include improved quality of life, reduced tumor burden progression, and effective symptom relief, driving consistent demand across developed healthcare systems.

The market expansion is fundamentally driven by the rising global incidence of neuroendocrine tumors, which often require long-term somatostatin analog (SSA) therapy. Improvements in diagnostic techniques leading to earlier detection of these slow-growing cancers, coupled with the increasing geriatric population—a demographic highly susceptible to chronic diseases—further fuel market growth. Additionally, ongoing research into new formulations, particularly long-acting injectable versions, enhances patient adherence and therapeutic efficacy, solidifying the market's trajectory towards substantial valuation by the end of the forecast period.

The Somatostatin Market is experiencing robust expansion propelled by advancements in oncology treatments and targeted drug delivery systems, positioning it as a critical sector within specialty pharmaceuticals. Key business trends include strategic collaborations between major pharmaceutical companies for the development of novel SSAs and the increasing focus on personalized medicine approaches, particularly in dosing and administration schedules for NET patients. The shift toward long-acting release (LAR) formulations significantly impacts market dynamics, offering improved convenience and therapeutic profiles, thus dominating market share compared to short-acting formulations.

Regionally, North America maintains the dominant market position, attributed to high healthcare expenditure, sophisticated diagnostic infrastructure, and favorable reimbursement policies for expensive chronic disease treatments like SSA therapy. However, the Asia Pacific (APAC) region is projected to register the highest growth rate, fueled by rapid improvements in healthcare access, rising awareness of NETs, and a growing patient pool in countries like China and India. European markets remain strong, driven by robust regulatory frameworks and well-established clinical guidelines for the use of SSAs in endocrinology and gastroenterology.

Segmentation trends highlight the dominance of octreotide-based products due to their established clinical efficacy and broad indication range. By application, the neuroendocrine tumors segment commands the largest share, reflecting the high utilization of SSAs as first-line and maintenance therapy. Furthermore, the increasing adoption of SSAs in niche applications, such as refractory diarrhea or certain surgical prophylactic scenarios, contributes to the overall segment diversification and sustained market stability throughout the forecast period.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Somatostatin Market often revolve around its potential to optimize treatment regimens, accelerate new drug discovery, and improve diagnostic accuracy for conditions treated by SSAs, such as neuroendocrine tumors (NETs) and acromegaly. Users frequently inquire if AI algorithms can predict patient responsiveness to different SSA analogs (e.g., octreotide vs. lanreotide), reducing trial-and-error in clinical settings. Concerns also focus on whether AI can streamline the synthesis and development of novel, highly specific SSA peptides or predict complex drug interactions and side effects more efficiently than traditional methods. Essentially, users expect AI to transition SSA therapy from generalized protocols to highly precise, patient-specific interventions, lowering costs and improving overall efficacy while speeding up preclinical validation phases for next-generation analogs.

The Somatostatin Market dynamics are shaped by a strong interplay of drivers and opportunities, which are constantly balanced against specific market restraints, creating impactful forces on strategic decision-making. A primary driver is the growing prevalence of chronic diseases requiring hormonal regulation, notably the rising incidence of neuroendocrine tumors globally. Furthermore, the continuous introduction of advanced, long-acting depot formulations enhances patient compliance and improves treatment outcomes, sustaining high demand. Opportunities reside in exploring novel routes of administration and expanding the therapeutic indications of SSAs beyond their established roles into areas such as proliferative diabetic retinopathy or certain refractory pain syndromes, which could unlock significant untapped revenue streams.

However, the market faces significant restraints, primarily revolving around the high cost of brand-name SSA therapies, which poses affordability challenges, especially in developing economies. Additionally, the complex biological structure and manufacturing difficulty of peptide therapeutics present a barrier to entry for smaller players and contribute to manufacturing limitations. The stringent regulatory landscape for approving new biologics and biosimilars also acts as a constraint, demanding extensive clinical data and prolonged validation processes, which can delay market entry of innovative products. These restraints necessitate robust pricing strategies and evidence generation to justify the economic value of these treatments.

The core impact forces driving competition include the threat of patent expiry and the subsequent entry of somatostatin biosimilars, which pressures pricing power and shifts market share. Conversely, significant investment in Research and Development (RD) for targeted radiolabeled SSAs (like PRRT therapies) creates a major upward force, offering high-value treatment alternatives for advanced NETs and potentially increasing the overall addressable patient population. The ongoing evolution of diagnostic imaging techniques (e.g., DOTATATE scans) ensures that patients who can benefit most from SSA therapy are accurately identified, further optimizing market utilization and driving specific product adoption based on clinical necessity.

The Somatostatin Market is meticulously segmented based on several key parameters, including product type, application, and end-user, allowing for a granular understanding of consumer preferences and market penetration rates. Product type segmentation primarily distinguishes between the natural somatostatin peptide (rarely used therapeutically due to short half-life) and synthetic analogs, with the latter category further divided into short-acting (Immediate Release - IR) and long-acting release (LAR) formulations, which exhibit vastly different market shares and growth trajectories. The LAR segment, exemplified by monthly injectables, dominates due to superior patient convenience and clinical management protocols, making it the foundational element of current SSA therapy.

Application-based segmentation is crucial, identifying the primary therapeutic areas driving demand. Neuroendocrine Tumors (NETs), encompassing carcinoid syndrome and other hormone-secreting tumors, represent the largest segment due to the established efficacy of SSAs as primary symptom management and antiproliferative agents. Acromegaly represents the second significant application, where SSAs are instrumental in normalizing growth hormone levels. Other applications, while smaller, include the management of specific gastrointestinal fistulas, acute pancreatitis, and variceal bleeding, reflecting the broad inhibitory role of somatostatin analogs across multiple physiological systems.

Furthermore, segmentation by end-user illustrates the primary points of consumption. Hospitals and specialized clinics are the primary buyers, given the requirement for professional administration of injectable LAR formulations and the complex care coordination required for NET and acromegaly patients. Ambulatory Surgical Centers (ASCs) and specialized oncology centers also represent growing consumption points, particularly as outpatient treatment models gain traction. This detailed segmentation allows manufacturers to tailor marketing efforts and distribution logistics effectively based on the specific needs and consumption patterns of each target group, ensuring optimal resource allocation and market coverage.

The value chain for the Somatostatin Market is characterized by highly specialized steps, beginning with the upstream synthesis of complex peptide molecules. Upstream activities involve sourcing high-purity raw materials, particularly amino acids, followed by sophisticated solid-phase or liquid-phase peptide synthesis (SPPS/LPPS). This manufacturing stage is capital-intensive and requires stringent quality control due to the complexity and sensitivity of peptide structures. Research and Development (RD) efforts at this stage focus on optimizing synthesis yield, developing novel analogs with enhanced pharmacokinetics (PK), and formulating the peptide into stable, long-acting delivery systems (microparticles or gels) which are critical for commercial success.

Midstream processes focus on the clinical validation, regulatory approval, and mass production of the final drug product, particularly the injectable LAR formulations. This stage involves complex sterile manufacturing and specialized packaging necessary to maintain product integrity and ensure patient safety. Manufacturing excellence and compliance with Good Manufacturing Practices (GMP) are paramount. Marketing and promotion activities are typically highly targeted, focusing on endocrinologists, oncologists, and gastroenterologists, who are the key prescribers for SSA therapies. Strategic positioning often emphasizes clinical efficacy data, ease of administration, and improved patient quality of life relative to competitors.

Downstream activities involve the distribution channel, which is crucial for managing the cold chain requirements of these high-value therapeutics. The distribution channel is predominantly direct or through specialized pharmaceutical wholesalers that manage hospital and specialty clinic deliveries. Due to the high cost and specialized nature, retail pharmacy presence is lower compared to standard prescription drugs. Direct channels ensure efficient inventory management and mitigate risks associated with temperature excursions. Indirect channels often involve national or regional distributors fulfilling bulk hospital orders. Ultimately, the successful completion of the value chain is highly dependent on managing the intellectual property rights associated with the specific analog structure and its patented formulation technology, thereby dictating market access and profitability.

The primary potential customers and end-users of somatostatin analogs are healthcare institutions and individual patients suffering from chronic hormone-related disorders and specific types of cancer. Hospitals, particularly those with specialized oncology, endocrinology, and gastroenterology departments, represent the largest institutional customer segment. These facilities rely on SSAs for the acute management of hormone crises, prophylactic use during surgery, and long-term maintenance therapy for large patient cohorts requiring injectable LAR formulations, which demand professional administration and comprehensive monitoring within a structured setting.

Specialty clinics and Ambulatory Surgical Centers (ASCs) constitute a growing customer base, driven by the trend toward outpatient treatment and cost containment. These centers are increasingly utilizing SSAs for routine administration, offering convenience for patients with stable conditions, and reducing the burden on inpatient hospital resources. Furthermore, the burgeoning field of nuclear medicine, utilizing radiolabeled SSAs for imaging and peptide receptor radionuclide therapy (PRRT), means that specialized nuclear medicine clinics are emerging as vital, high-value end-users, requiring both the SSAs for imaging contrast and therapeutic application.

Ultimately, the individual patient, diagnosed with conditions such as metastatic neuroendocrine tumors or uncontrolled acromegaly, is the final beneficiary and driver of prescriptions. Patient organizations and advocacy groups indirectly influence the market by pushing for improved access and reimbursement policies. The focus on patient-centric care, adherence, and quality of life strongly influences prescribing habits, making formulations that reduce injection frequency and minimize side effects highly desirable, thereby sustaining the demand from this end-user segment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.95 Billion |

| Market Forecast in 2033 | USD 3.08 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Novartis AG, Ipsen Pharma, Pfizer Inc., Sun Pharmaceutical Industries Ltd., Teva Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories Ltd., Amneal Pharmaceuticals Inc., Hikma Pharmaceuticals PLC, Akorn Operating Company LLC, Bristol-Myers Squibb Company, Eli Lilly and Company, AstraZeneca PLC, Takeda Pharmaceutical Company Limited, Mylan N.V. (Viatris), Sanofi S.A., Chong Kun Dang Pharmaceutical Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Somatostatin Market is primarily defined by advanced drug delivery systems designed to overcome the inherent limitations of peptide therapeutics, specifically their short biological half-life and susceptibility to degradation. The most impactful technology is the development of Long-Acting Release (LAR) formulations, which utilize biodegradable polymer microspheres (such as poly-lactic-co-glycolic acid, PLGA) or novel gel matrices. These technologies encapsulate the SSA peptide, allowing for sustained, controlled release over a period of weeks to months (typically 28 days), significantly reducing the frequency of injections and enhancing patient adherence. Ongoing research focuses on refining these microparticulate technologies to achieve even longer duration of action (e.g., three-month injections) and minimize local injection site reactions, optimizing the pharmacokinetic profile for chronic management.

Another crucial technological advancement involves the synthesis and modification of the peptide structure itself. Researchers are utilizing rational drug design and computational chemistry to create novel somatostatin analogs (e.g., Pasireotide, which binds with higher affinity to multiple somatostatin receptor subtypes, particularly SSTR5) to improve efficacy in tumors refractory to first-generation treatments. This involves sophisticated peptide chemistry techniques, including the use of non-natural amino acids and cyclization strategies, to enhance metabolic stability and target specificity. This continuous technological refinement aims not only to improve binding selectivity but also to reduce off-target effects, thereby broadening the safety margin.

Furthermore, the convergence of SSAs with diagnostic and therapeutic nuclear medicine represents a significant technological leap. Peptide Receptor Radionuclide Therapy (PRRT) utilizes radiolabeled SSAs (like DOTATATE or DOTATOC labeled with radionuclides such as Lu-177 or Ga-68) to specifically target SSTR-expressing tumors. This dual-use technology—for diagnosis (via PET imaging) and targeted treatment—demands advanced radiopharmaceutical manufacturing and precise quality assurance protocols. The integration of high-resolution imaging technology with specific SSA receptor binding technology is fundamentally reshaping the treatment paradigm for metastatic neuroendocrine tumors, representing the leading edge of innovation in this market segment.

North America, particularly the United States, commands the largest share of the global Somatostatin Market. This dominance is underpinned by several factors: exceptionally high healthcare expenditure, a sophisticated regulatory environment that facilitates the commercialization of specialized drugs, and the presence of major pharmaceutical innovators and key opinion leaders in oncology and endocrinology. The high adoption rate of premium-priced, long-acting SSA formulations, coupled with favorable and broad reimbursement coverage by private and public insurance payers (e.g., Medicare/Medicaid), ensures that eligible patients have reliable access to expensive, life-saving therapies. The region benefits from robust clinical trial infrastructure and a strong focus on advanced diagnostics, which contribute to the accurate identification and prompt treatment initiation for patients with NETs and acromegaly, sustaining market momentum.

The competitive landscape in North America is intense, driven by patent battles and strategic marketing efforts surrounding both brand-name innovators and the nascent biosimilar market. Academic medical centers and large integrated health networks are the primary utilization points, emphasizing adherence to established clinical guidelines that strongly recommend SSAs as standard-of-care. The region’s focus on personalized treatment regimens, increasingly utilizing pharmacogenomics and molecular imaging (like Gallium-68 DOTATATE PET scans), further optimizes the use of SSAs, reinforcing its status as the leading market contributor and technology adopter.

The regulatory environment, primarily governed by the FDA, while stringent, provides clear pathways for novel SSA formulations and indications, encouraging continuous investment in the market. The significant market size and high purchasing power ensure that manufacturers prioritize launching new products and advanced delivery technologies here first, capitalizing on the lucrative patient population. Furthermore, strong lobbying and patient advocacy groups ensure sustained public and governmental focus on improving access to high-quality chronic care, including SSA therapy, ensuring the market remains resilient against economic fluctuations.

Europe represents the second largest market for somatostatin analogs, characterized by universal healthcare systems and a high level of clinical acceptance for SSA treatments across countries like Germany, France, and the UK. Market growth is sustained by the high prevalence of neuroendocrine tumors and well-structured national guidelines that define the appropriate use of SSAs in symptomatic control and anti-tumor treatment. However, the diverse regulatory and pricing systems across the EU present challenges, as national healthcare authorities often negotiate hard on drug prices, leading to variations in product availability and pricing structures compared to the U.S. market.

A key dynamic in the European market is the increasing penetration of biosimilars, particularly for established molecules like Octreotide. This biosimilar entry exerts downward pressure on the average selling prices of innovator products but simultaneously expands patient access by making treatment more economically viable for national health systems. Manufacturers must employ dual strategies: defending their innovator products through robust clinical evidence and patient support programs, while also competing effectively in the biosimilar space to maintain market relevance across the continent.

Central and Eastern European countries are rapidly integrating Western treatment protocols, leading to accelerated market growth, although resource constraints often favor cost-effective or generic options. Western Europe remains focused on innovation, including the adoption of advanced SSA delivery systems and the rapid uptake of novel PRRT treatments utilizing radiolabeled SSAs. Collaborative research initiatives and strong scientific communities in countries like Switzerland and Sweden continually push the boundaries of SSA applications, supporting moderate yet stable market expansion.

The Asia Pacific (APAC) region is forecasted to exhibit the highest Compound Annual Growth Rate (CAGR) in the Somatostatin Market during the forecast period. This accelerated growth is primarily attributed to rapidly improving healthcare infrastructure, substantial government investments in cancer care, and increasing urbanization leading to a greater prevalence and diagnosis rate of chronic diseases like NETs. Countries such as China, India, Japan, and South Korea are key growth engines, driven by their massive populations and expanding middle classes who can afford better access to specialty pharmaceuticals.

While the market historically relied on locally manufactured generics, there is a clear shift towards adopting long-acting, international brand formulations as economic prosperity and insurance coverage improve. Increasing medical tourism for complex treatments also contributes to higher consumption of advanced SSAs in regional healthcare hubs. However, the APAC market faces challenges related to low disease awareness in certain rural areas and logistical complexities in cold-chain distribution across vast geographical distances.

Key opportunities in APAC lie in establishing strong distribution partnerships and focusing on localized clinical data generation to satisfy regional regulatory bodies. Japan and South Korea, with their mature healthcare systems, are quick adopters of the latest SSA technologies, including PRRT. Meanwhile, emerging economies like India and China are seeing burgeoning demand, driven by domestic manufacturers developing cost-effective biosimilar options and the government initiative to reduce the financial burden of chronic disease management, setting the stage for significant market penetration and expansion over the next decade.

SSAs are primarily used for the long-term management of neuroendocrine tumors (NETs), particularly for controlling symptoms associated with carcinoid syndrome and as anti-proliferative agents. They are also standard first-line therapy for treating acromegaly by inhibiting excessive growth hormone secretion.

LAR formulations, such as those administered monthly, significantly enhance patient compliance and convenience compared to short-acting injections. They dominate the market share due to their superior pharmacokinetic profiles, making them the preferred standard of care for chronic SSA therapy.

North America, particularly the United States, leads the market due to high healthcare spending, advanced infrastructure for chronic disease management, favorable reimbursement policies for premium biologics, and high diagnosis rates for neuroendocrine disorders.

The introduction of Somatostatin biosimilars is expected to increase market competition, exert downward pressure on overall pricing, and improve access to treatment, especially in cost-sensitive regions, by offering more affordable therapeutic alternatives to originator products.

PRRT is an advanced targeted therapy utilizing radiolabeled SSAs (like Lu-177-DOTATATE) which specifically bind to SSTR-expressing tumors. This technology allows for precise delivery of radiation to cancer cells, representing a major technological advancement in the treatment of advanced NETs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.