ID : MRU_ 443683 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

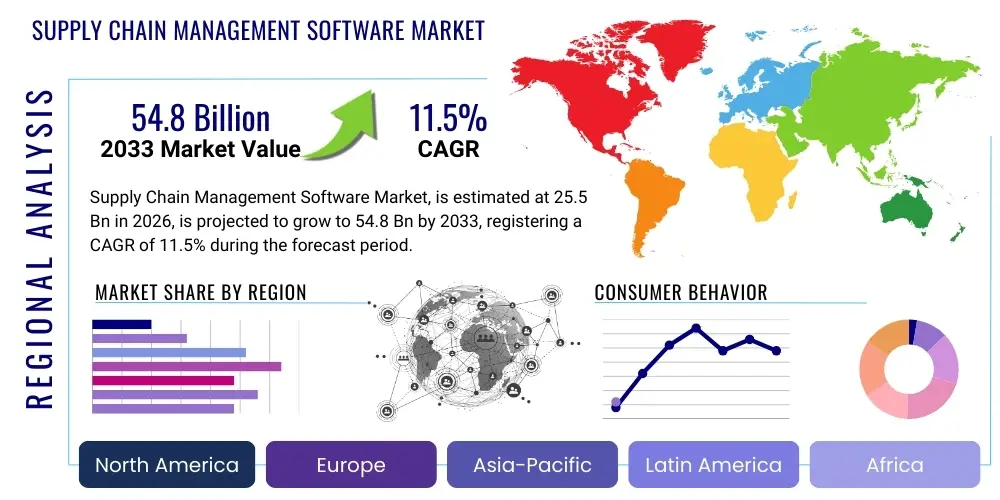

The Supply Chain Management Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 25.5 Billion in 2026 and is projected to reach USD 54.8 Billion by the end of the forecast period in 2033.

The Supply Chain Management (SCM) Software Market encompasses a suite of tools and applications designed to manage end-to-end supply chain operations, spanning planning, procurement, manufacturing, logistics, inventory, and lifecycle management. These solutions integrate critical business processes, enabling organizations to achieve higher levels of operational efficiency, enhance visibility, and improve decision-making across complex global networks. Key SCM product offerings include planning software (Demand Planning, S&OP), execution software (WMS, TMS), and visibility platforms. The core objective of SCM software is to optimize the flow of goods, information, and funds, mitigating risks associated with disruptions, reducing operational costs, and ultimately enhancing customer satisfaction through faster and more reliable service delivery. Widespread adoption is observed across sectors ranging from retail and manufacturing to pharmaceuticals and logistics.

Major applications of SCM software involve strategic sourcing and procurement, real-time tracking and monitoring of inventory levels across distributed locations, and sophisticated route optimization for transportation management. Furthermore, modern SCM platforms are increasingly focused on improving resilience, allowing businesses to dynamically respond to unforeseen challenges such as geopolitical instability or pandemic-related shutdowns. The underlying benefit of implementing robust SCM solutions is the transformation from reactive supply chains to predictive, data-driven supply networks. This shift is crucial for businesses operating in highly competitive and volatile markets where speed and adaptability are paramount competitive differentiators. The increasing complexity of global trade, coupled with consumer demands for rapid fulfillment and transparent supply chain practices, acts as a primary driving factor for market expansion.

The market trajectory is significantly influenced by the accelerating shift toward cloud-based deployment models (SaaS), which offer scalability, reduced infrastructure investment, and faster deployment cycles compared to traditional on-premise systems. Furthermore, the imperative for sustainable and ethical sourcing practices is driving demand for software features that enable supply chain traceability and compliance monitoring. As companies navigate post-pandemic recovery and increasing inflationary pressures, the focus remains firmly on leveraging SCM software to achieve cost efficiencies through automation and improved resource utilization. These factors collectively establish a robust foundation for sustained growth in the global SCM software sector throughout the forecast period.

The Supply Chain Management Software Market is undergoing a rapid digital evolution, characterized by pervasive cloud adoption and intense integration of advanced technologies like Artificial Intelligence (AI) and Internet of Things (IoT). Current business trends indicate a significant pivot towards building highly resilient, agile supply chains capable of instantaneous adaptation to market volatility and unexpected disruptions. Enterprises are prioritizing investment in integrated SCM suites over siloed applications, seeking unified platforms that offer comprehensive visibility from raw material sourcing to final product delivery. The drive toward sustainability and environmental, social, and governance (ESG) compliance is shaping product development, pushing vendors to incorporate features for carbon tracking and ethical sourcing verification. Furthermore, merger and acquisition activities remain high, as large technology companies seek to acquire specialized vertical solutions or bolster their AI/ML capabilities within their existing SCM portfolios.

Regionally, North America maintains its dominance, driven by high technological maturity, substantial enterprise spending on digitalization, and the early adoption of advanced solutions such as Blockchain for SCM and predictive analytics. However, the Asia Pacific (APAC) region is poised for the fastest growth, fueled by rapid industrialization, the expansion of e-commerce markets, and increasing governmental investments in logistical infrastructure and manufacturing capabilities, particularly in emerging economies like India and Southeast Asian nations. Europe demonstrates strong adoption, primarily driven by stringent regulatory requirements, sophisticated manufacturing bases (especially Germany), and a regional focus on optimizing cross-border logistics through centralized systems. The competitive landscape in all regions is intensifying, with traditional ERP vendors competing fiercely against specialized SaaS providers who offer superior flexibility and rapid innovation cycles.

Segmentation trends highlight the increasing prominence of Transportation Management Systems (TMS) and Warehouse Management Systems (WMS) due to the explosion of omnichannel retail and complex final-mile delivery requirements. Functionally, the planning segment, specifically demand forecasting and Sales & Operations Planning (S&OP), is experiencing revitalization through AI-driven predictive modeling. Deployment wise, Software-as-a-Service (SaaS) continues its trajectory as the preferred model across all enterprise sizes, owing to its lower Total Cost of Ownership (TCO) and rapid time-to-value. Small and Medium Enterprises (SMEs) are emerging as significant growth drivers for SaaS-based solutions, democratizing access to enterprise-grade SCM capabilities previously only affordable by large corporations. This confluence of technological integration, strategic regional expansion, and specialized functional demand underscores a robust growth outlook for the SCM software industry.

User inquiries regarding AI's influence on the Supply Chain Management Software Market primarily center on three key areas: predictive capability, automation efficacy, and the resulting impact on job roles. Users frequently ask how AI can enhance demand forecasting accuracy amidst high volatility, what specific SCM tasks can be fully automated (e.g., invoice processing, inventory ordering), and whether the implementation of advanced AI algorithms requires specialized data science teams. There is a strong expectation that AI will transition SCM from a reactive function to a highly proactive and resilient strategic capability. Concerns often revolve around data quality requirements for effective AI training, the transparency (or 'explainability') of AI-driven decisions (especially for regulatory compliance), and the cybersecurity implications of integrating external data sources into AI models. The overarching theme is the pursuit of operational excellence and enhanced resilience through intelligent automation, making the supply chain both smarter and more autonomous.

The integration of Artificial Intelligence and Machine Learning (AI/ML) is fundamentally transforming the SCM software landscape, moving beyond simple automation to enable advanced cognitive capabilities. AI is instrumental in processing massive datasets generated by IoT devices and enterprise systems, uncovering non-obvious patterns that influence demand and supply. This capability facilitates superior prescriptive and predictive analytics, allowing supply chain planners to simulate various scenarios and select the optimal course of action before disruptions materialize. For instance, AI algorithms can analyze thousands of geopolitical, weather, and commodity price data points to proactively adjust inventory buffers or reroute shipments, thereby significantly reducing lead times and mitigating financial risk. This shift elevates SCM from a transactional function to a strategic lever for competitive advantage.

Furthermore, AI is driving significant advancements in operational execution, particularly within warehouse and transportation environments. Machine learning models optimize picking routes, balance labor schedules based on predicted workload peaks, and dynamically manage fleet utilization. In procurement, AI enhances spend analysis, identifies potential supplier risks through anomaly detection, and automates negotiation parameters for routine purchases, ensuring compliance and maximizing savings. The long-term impact is the creation of 'self-aware' supply chains—systems capable of learning from past performance and external stimuli, continuously optimizing themselves without manual intervention, thereby achieving unprecedented levels of efficiency and responsiveness across the entire supply network.

The Supply Chain Management Software Market is propelled by powerful macro-economic and technological forces (Drivers), yet its expansion is tempered by significant operational and infrastructural challenges (Restraints), opening various avenues for disruptive innovation (Opportunities). The primary impact force driving current growth is the overwhelming necessity for organizations to achieve operational resilience against geopolitical instability, climate change impacts, and persistent inflationary pressures. Global supply chain fragility exposed during recent crises has elevated SCM technology investment from an operational expense to a strategic imperative. Organizations are mandated to transition from traditional, linear supply chains to highly integrated, mesh networks capable of dynamic reconfiguration. This systemic pressure ensures sustained, high-CAGR growth in the enterprise software sector dedicated to supply chain excellence.

Drivers: The fundamental drivers include the exponential growth of e-commerce and omnichannel retailing, which necessitates highly efficient fulfillment and logistics operations, coupled with the global adoption of cloud computing, lowering the barrier to entry for advanced SCM tools. Additionally, the increasing complexity of regulatory environments, especially related to trade compliance, customs declarations, and sustainability reporting (ESG), drives demand for sophisticated, traceable software solutions. The need for real-time visibility across global supply networks to prevent inventory stockouts or costly delays further fuels software implementation. Digital transformation initiatives across major industries, aimed at replacing legacy ERP modules with dedicated, best-of-breed SCM applications, are providing consistent market momentum. Finally, the compelling ROI derived from automation—including reduced labor costs and error rates—serves as a constant catalyst for adoption.

Restraints: Significant restraints impede market growth, most notably the high initial implementation costs associated with large-scale, integrated SCM suites and the complexity involved in integrating new software with existing, often decades-old legacy ERP systems. Furthermore, a persistent shortage of skilled professionals capable of effectively implementing, managing, and utilizing advanced SCM technologies, particularly those incorporating AI and IoT, poses a bottleneck. Data standardization and quality issues remain a hurdle; effective SCM software relies heavily on clean, consistent data across disparate organizational silos, which is often difficult to achieve in global enterprises. Resistance to organizational change and cybersecurity concerns regarding sensitive supply chain data also necessitate cautious investment strategies, potentially slowing deployment across risk-averse organizations.

Opportunities: Key opportunities lie in the expansion of specialized SCM solutions tailored for specific verticals (e.g., cold chain logistics for pharmaceuticals, traceable sourcing for luxury goods). The growing need for end-to-end supply chain planning solutions (e.g., integrated business planning or IBP), which align financial planning with operational execution, presents a major growth opportunity. The market is also ripe for innovation in hyper-local and final-mile delivery optimization through edge computing and geo-spatial analytics. Furthermore, the massive potential within the Small and Medium Enterprise (SME) segment, leveraging affordable, scalable, micro-SaaS SCM modules, provides an expansive untapped customer base. Vendors focusing on user-friendly interfaces and robust integration capabilities stand to capture significant market share by simplifying complex SCM tasks for less technologically mature organizations, ensuring the market continues to diversify its application base and geographical reach.

The Supply Chain Management Software Market is segmented based on deployment model, solution type, component, enterprise size, and industry vertical, reflecting the diverse needs of modern supply chains. The solutions segment is granular, encompassing strategic applications like procurement and planning, and execution applications like transportation and warehouse management. This segmentation allows vendors to target specific operational pain points within an organization, offering specialized tools that maximize efficiency in defined areas. The trend favors integrated suites, but strong growth persists in best-of-breed solutions offering deep specialization within niche areas, such as advanced optimization or specific industry regulatory compliance. Understanding these segment dynamics is critical for market participants aiming to tailor their product offerings and maximize competitive advantage.

The transition from on-premise to cloud deployment is the most influential factor defining current market dynamics. Cloud-based solutions (SaaS) dominate new installations due to their inherent scalability, lower infrastructure burden, and rapid upgrade cycles, making them highly attractive to mid-market and global enterprises alike. Simultaneously, the component segment highlights the necessity for both core software functionality and the ongoing value derived from professional services, including implementation, customization, and continuous data integration consulting, which form a significant revenue stream for leading vendors. Analyzing these segments provides a detailed map of investment priorities across different customer profiles, confirming the strategic importance of flexible, service-oriented business models.

The value chain of the Supply Chain Management Software Market begins with upstream activities dominated by core technology providers, including infrastructure vendors (cloud service providers like AWS, Azure, Google Cloud), database developers, and specialized component vendors providing AI/ML algorithms and advanced optimization libraries. These upstream players supply the foundational platforms and specialized intellectual property necessary for SCM software developers to build their applications. Key activities at this stage involve continuous R&D into cutting-edge technologies (e.g., quantum computing optimization algorithms, advanced security protocols) and securing partnerships to ensure platform compatibility. High dependency on these foundational technologies means that disruptions or advancements in the upstream segment significantly impact the feature set and performance capabilities of the final SCM solutions.

The central stage of the value chain involves the SCM software vendors themselves. Activities here include product development, customization, integration, sales, and ongoing support. This stage is highly complex, involving integrating various functional modules (WMS, TMS, SCP) and ensuring seamless data flow across the enterprise ecosystem. Distribution channels are varied, including direct sales teams for major enterprise contracts, indirect sales through channel partners and resellers specializing in specific geographies or industry verticals, and, increasingly, cloud marketplaces for easy adoption of SaaS solutions. The success of a vendor largely depends on the strength of their partner ecosystem, their ability to provide specialized professional services, and the perceived ease of integration with diverse client environments. The trend towards specialized systems integrators who manage complex cloud migrations and system rollouts is particularly notable.

Downstream activities center on the end-users—the manufacturers, retailers, logistics providers, and distributors who consume the software. Value is realized when the software is effectively deployed to optimize business processes, reduce operational expenditure, and improve overall supply chain responsiveness. The final component involves continuous support and maintenance provided by the software vendor or third-party service providers, ensuring the system evolves with the business needs. Customer feedback and usage data are critical for the iterative refinement of the software, feeding back into the upstream R&D cycle. Direct interaction often occurs for highly customized enterprise implementations, while indirect channels (such as consultants or system integrators) frequently facilitate the initial adoption and ongoing management, particularly for SMEs utilizing standardized SaaS offerings.

The potential customer base for Supply Chain Management software is broad and diverse, primarily encompassing any organization involved in the movement, storage, transformation, or tracking of physical goods—spanning global manufacturers to local e-commerce operations. The primary buyers include Chief Operating Officers (COOs), Chief Supply Chain Officers (CSCOs), Head of Logistics, and IT decision-makers who are tasked with improving efficiency, reducing costs, and mitigating risks within the physical flow of goods. These buyers prioritize solutions that offer robust integration capabilities, superior analytical engines (especially predictive planning), and demonstrate a clear Return on Investment (ROI) through tangible operational improvements, such as reduced inventory holding costs or faster order fulfillment cycles. The shift towards resilience has made risk mitigation a primary purchase criterion across all verticals.

In manufacturing, customers are typically seeking advanced solutions for demand forecasting, production scheduling, and inventory optimization to manage complex Bills of Material (BOMs) and lean manufacturing principles. For the Retail and E-commerce sector, the focus is heavily skewed toward execution systems, specifically sophisticated WMS to handle high-volume, quick-turn inventory, and TMS for efficient final-mile delivery and reverse logistics. Healthcare and Pharmaceutical customers are driven by stringent regulatory compliance (e.g., temperature monitoring, drug traceability), requiring SCM software that provides certified audit trails and secure chain-of-custody documentation, making them high-value, albeit challenging, clientele due to specialized requirements. These diverse industry needs mandate that SCM vendors offer flexible, configurable platforms rather than generic solutions.

Furthermore, the logistics and third-party logistics (3PL) providers represent a significant customer segment, as their core business viability depends entirely on maximizing asset utilization and operational efficiency through best-in-class SCM technology. They invest heavily in advanced TMS, warehouse automation software, and visibility platforms to offer differentiated, competitive services to their clients. Increasingly, SMEs are becoming vital customers, driven by competitive pressures to operate efficiently, adopting scalable, low-cost SaaS solutions. The common thread among all potential buyers is the relentless pursuit of end-to-end visibility and the ability to leverage real-time data to make instantaneous, optimized decisions, cementing SCM software as essential business infrastructure.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 25.5 Billion |

| Market Forecast in 2033 | USD 54.8 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Oracle, SAP SE, IBM, Microsoft, Infor, JDA Software (Blue Yonder), Kinaxis, Manhattan Associates, Descartes Systems Group, E2open, HighJump (Körber), Coupa Software, PLEX Systems, Epicor Software, Solvoyo, FourKites, Llamasoft (Coupa), MercuryGate International, GT Nexus (Infor), TECSYS |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Supply Chain Management Software Market is rapidly evolving, driven by the convergence of several sophisticated digital technologies aimed at enhancing visibility, automation, and predictive capabilities. Cloud computing, particularly SaaS models, remains the dominant infrastructure, facilitating rapid deployment, scalability, and seamless updates, which are essential for agile supply chain operations. This foundational shift enables greater collaboration across disparate internal departments and external partners. Beyond the cloud, the Internet of Things (IoT) sensors and devices play a pivotal role, providing real-time data on asset location, inventory status, and environmental conditions (temperature, humidity). This influx of real-time operational data is the lifeblood for advanced analytical engines, transforming raw logistical information into actionable insights.

Artificial Intelligence (AI) and Machine Learning (ML) constitute the core intelligence layer of next-generation SCM software. These technologies are integral for moving beyond descriptive analytics to prescriptive modeling, enabling highly accurate demand forecasting, optimal network design, dynamic pricing, and automated risk detection. Furthermore, the adoption of Digital Twin technology is gaining traction, allowing organizations to create high-fidelity virtual replicas of their entire supply chain, enabling sophisticated "what-if" scenario planning without impacting physical operations. This modeling capability is crucial for stress-testing resilience strategies and optimizing massive capital investments in infrastructure before physical execution. The ability to simulate complex logistics under real-world constraints provides a significant competitive edge.

Blockchain technology, while still maturing, is poised to revolutionize specific SCM applications, primarily focusing on enhancing transparency, traceability, and ensuring data immutability, especially critical for regulatory compliance in pharmaceutical, food, and high-value goods sectors. Blockchain facilitates secure, shared ledger transactions, reducing fraud and streamlining complex cross-border documentation processes. Concurrently, advancements in Robotic Process Automation (RPA) are automating routine, high-volume transactional tasks within procurement and administrative logistics, freeing up human staff for higher-value strategic planning. These integrated technologies collectively define the modern SCM platform—a highly interconnected, intelligent system designed for optimal performance in a globally interconnected yet volatile business environment, positioning technology integration as the primary differentiator among competing vendors.

North America currently holds the dominant share of the SCM Software Market, characterized by high levels of technological maturity, significant enterprise expenditure on digital transformation, and the presence of major software vendors and key early adopters. The US, in particular, drives this dominance, fueled by a sophisticated logistics network, a massive e-commerce market, and a strong regulatory push for supply chain transparency, particularly within the pharmaceutical and food safety sectors. High labor costs within this region accelerate the adoption of advanced automation solutions, including robotics integrated with WMS and AI-driven planning software, yielding a high per capita investment in SCM technology. The competitive environment is saturated but intensely focused on integrating AI/ML and cloud migration, setting global standards for technological implementation and innovation.

Asia Pacific (APAC) is projected to be the fastest-growing region during the forecast period. This rapid growth is underpinned by burgeoning manufacturing sectors, booming e-commerce penetration (especially in China, India, and Southeast Asia), and increasing foreign direct investment in logistics and infrastructure development. While many emerging APAC economies are currently focused on basic SCM execution software (WMS/TMS), the rapid digital maturity of large enterprises is quickly shifting demand toward integrated planning suites and advanced analytics. Governmental initiatives promoting 'smart city' logistics and supply chain digitization further stimulate market expansion. However, regional complexity, fragmented regulatory frameworks, and diverse linguistic requirements pose challenges, necessitating highly localized and configurable software solutions from vendors looking to capitalize on this exponential growth.

Europe represents a mature market with high adoption rates, particularly in Western European nations like Germany, the UK, and France. The market here is driven primarily by the need for cross-border logistics optimization necessitated by the European Single Market, stringent manufacturing standards, and a strong regional emphasis on sustainability and traceability (ESG reporting). European firms prioritize highly efficient, precise supply chain planning and execution to manage complex, multi-national distribution networks. The region is a significant adopter of specialized technologies such as Global Trade Management (GTM) software to navigate complex customs requirements and regulations. The market growth, while steady, is increasingly focused on modernization through cloud migration and the integration of advanced optimization algorithms to enhance efficiency within existing infrastructure rather than large-scale, greenfield investments.

The primary benefit of migrating Supply Chain Management software to a Cloud (SaaS) model is increased agility and reduced Total Cost of Ownership (TCO). SaaS deployments eliminate the need for extensive on-premise infrastructure, offer superior scalability to match fluctuating business demands, ensure rapid implementation, and provide continuous updates with the latest security and AI features automatically, enhancing resilience and collaboration across the supply network.

AI is transforming demand forecasting by moving beyond historical data analysis to incorporate thousands of external, non-linear variables such as macroeconomic indicators, social media sentiment, and competitor pricing. Machine Learning algorithms identify complex patterns and correlations far surpassing human capability, leading to significantly higher forecast accuracy and enabling prescriptive planning that anticipates market volatility, thereby minimizing inventory risks.

The Transportation Management System (TMS) segment, alongside Supply Chain Planning (SCP) solutions focused on Integrated Business Planning (IBP), is experiencing the fastest growth. This surge is driven by the complexity of omnichannel fulfillment, global trade, and the imperative for real-time logistics optimization, making efficient final-mile and global freight management critical competitive differentiators across all major industry verticals, particularly retail and 3PL.

The greatest challenges for SCM adoption often revolve around integration complexity, particularly connecting modern cloud-based SCM suites with existing, disparate legacy Enterprise Resource Planning (ERP) systems and achieving reliable data quality. Furthermore, organizational resistance to change and the scarcity of personnel skilled in optimizing and managing advanced AI-driven planning tools pose significant operational hurdles to successful, full-scale deployment.

Blockchain's primary role is to ensure immutable data records, providing enhanced transparency and traceability across multi-tiered supply chains, which is vital for regulatory compliance (e.g., food safety, ethical sourcing) and reducing fraud. While not a replacement for core SCM systems, blockchain acts as a trust layer, streamlining cross-border transactions, contract validation, and securing the digital chain of custody for high-value or highly regulated goods, thereby improving overall auditability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.