ID : MRU_ 442294 | Date : Feb, 2026 | Pages : 257 | Region : Global | Publisher : MRU

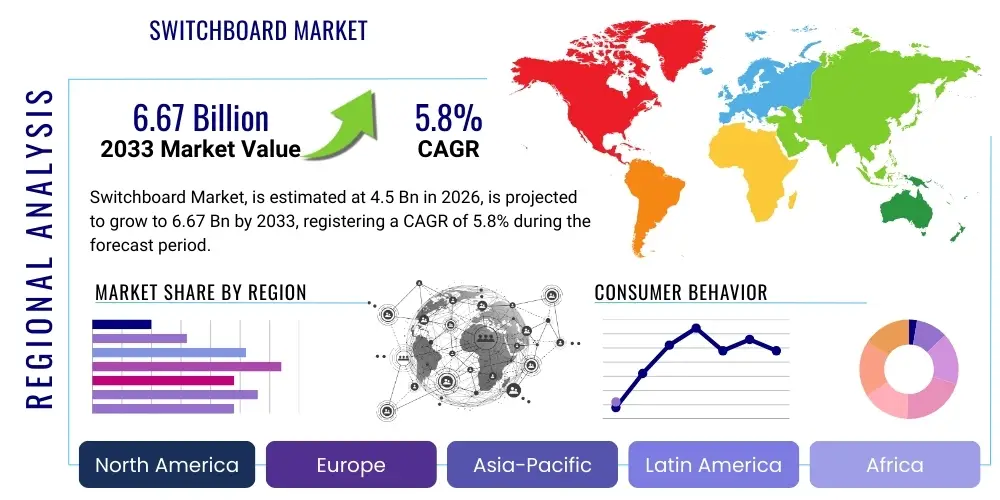

The Switchboard Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 4.5 billion in 2026 and is projected to reach USD 6.67 billion by the end of the forecast period in 2033.

The Switchboard Market encompasses the manufacturing, distribution, and utilization of centralized electrical distribution equipment designed to safely control, protect, and isolate electrical circuits. A switchboard functions as the primary point of control for electricity entering a facility, distributing power to various subsidiary circuits, feeders, and load centers. These systems are essential components of any electrical infrastructure, ranging from residential complexes and commercial buildings to heavy industrial plants and utility substations, providing reliable overcurrent protection, isolation capabilities, and metering functions. The core product category includes low-voltage (LV) switchboards, medium-voltage (MV) switchgear (often integrated into comprehensive switchboard solutions), and specialized control and distribution panels tailored to specific operational requirements.

Major applications for switchboards span across critical infrastructure sectors. In the industrial segment, they are vital for managing high-capacity power flows to manufacturing equipment, motors, and process control systems, necessitating robust designs and advanced protective relays. Within the utility sector, switchboards are integral to substation infrastructure, ensuring safe interconnection and distribution across grids, increasingly focusing on smart grid compatibility and remote monitoring. Commercial applications, such as data centers, hospitals, and large office buildings, require highly reliable, fault-tolerant switchboards to manage essential services and minimize downtime, driven by the increasing density of electrical loads.

Key benefits derived from modern switchboard implementation include enhanced electrical safety through arc flash mitigation features, optimized power distribution efficiency, and prolonged equipment lifespan via superior protection mechanisms. Driving factors for market expansion include rapid urbanization and subsequent infrastructural development in emerging economies, massive global investments in renewable energy integration requiring specialized grid interface switchboards, and the persistent need to replace aging electrical infrastructure in developed regions. Furthermore, the push towards automated and smart buildings is catalyzing demand for intelligent, digitized switchboards capable of real-time monitoring and advanced diagnostic reporting, fueling market evolution towards higher technological integration.

The global Switchboard Market is characterized by steady growth, primarily fueled by massive infrastructure investment cycles, particularly in the Asia Pacific region, alongside the global energy transition driving renewable integration into existing grids. Current business trends indicate a strong shift towards modular and compact switchboard designs that facilitate quicker installation and lower footprint requirements, essential for densely populated urban centers and retrofit projects. Furthermore, digital transformation is pushing manufacturers to incorporate smart functionalities, including integrated sensors, remote diagnostics, and communication capabilities (IoT enablement), positioning switchboards as crucial nodes within smart energy management ecosystems. Regulatory compliance concerning safety standards, especially arc flash protection, remains a primary influencing factor on design and material choices, favoring vendors who offer highly compliant, robust solutions.

Regionally, the Asia Pacific (APAC) dominates the market, largely attributable to rapid industrialization, extensive government investments in power generation and transmission infrastructure, and escalating construction activities across commercial and residential sectors in countries like China and India. North America and Europe, while mature markets, maintain significant demand driven primarily by infrastructure modernization, grid reinforcement initiatives, and the implementation of sophisticated energy management systems in commercial and industrial settings. Latin America and the Middle East & Africa (MEA) are emerging as high-growth potential regions, underpinned by large-scale mining operations, oil and gas expansion, and state-backed utility projects focused on electrification and grid stability improvements.

Segmentation trends highlight the increasing importance of the Industrial and Utility application segments, where reliability and operational resilience are paramount. Within the product type category, low-voltage (LV) switchboards constitute the largest volume segment due to their pervasive use in nearly all building types, while medium-voltage (MV) switchgear components, critical for larger substations and industrial feeders, represent a higher value segment characterized by complexity and specialized manufacturing requirements. The trend towards Gas Insulated Switchboards (GIS) is notable in high-density urban areas and regions demanding superior environmental performance and minimized maintenance, although Air Insulated Switchboards (AIS) maintain dominance due to their cost-effectiveness and proven reliability in standard applications.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Switchboard Market often revolve around predictive maintenance capabilities, optimal load balancing, and the future necessity of human intervention. Users are highly interested in how AI algorithms can leverage vast amounts of operational data generated by smart switchboards (voltage, current, temperature readings) to predict potential component failures, thereby preventing costly downtime and enhancing system reliability. Another frequent query concerns AI's role in optimizing energy consumption and distribution efficiency within a facility, using machine learning to analyze historical consumption patterns and dynamically adjust power routing or shedding loads to minimize peak demand charges. The overarching concern is how quickly and affordably existing infrastructure can be upgraded to harness these advanced AI capabilities and what specific training is required for technical staff to manage these highly intelligent systems effectively. Essentially, users seek to understand AI's transition from passive monitoring tools to active, decision-making components within the electrical distribution architecture.

The primary transformative impact of AI on the switchboard domain centers on advanced condition monitoring and diagnostics. By integrating sophisticated machine learning models, switchboards can move beyond simple threshold alarms to provide nuanced assessments of component health, identifying subtle anomalies indicative of insulation degradation, loose connections, or impending circuit breaker failure well before a critical fault occurs. This shift enhances operational safety and dramatically reduces unplanned outages. Furthermore, AI facilitates better integration of variable renewable energy sources (like solar and wind) into microgrids managed by advanced switchboards, using predictive modeling to stabilize the local grid against fluctuations in supply and demand, ensuring seamless power quality irrespective of the source variability.

In the manufacturing sphere, AI is being deployed to optimize the design and production process of switchboards. Generative design algorithms can assist engineers in creating highly efficient, compact layouts that adhere to stringent safety and thermal requirements, minimizing material usage while maximizing accessibility and maintainability. On the operational side, AI-powered supervisory control systems are evolving to manage complex load transfers, fault isolation, and system restoration processes automatically, drastically speeding up reaction times compared to manual or conventional automated systems. This integration transforms the switchboard from a purely passive control mechanism into an intelligent, autonomous element of the modern power distribution network.

The Switchboard Market dynamics are strongly influenced by the interplay of infrastructure spending, technological advancements in smart grid components, and stringent regulatory safety mandates. Key drivers include accelerating global urbanization leading to massive residential and commercial construction booms, particularly in fast-growing economies in Asia and Africa. Furthermore, the pervasive trend toward industrial automation (Industry 4.0) necessitates modern, reliable power distribution solutions capable of handling high levels of power quality and communication demands. The critical global shift towards decarbonization and the subsequent integration of distributed renewable energy sources (solar, wind) require complex, multi-functional switchboards designed for bi-directional power flow and advanced metering, providing consistent uplift to market demand. These drivers collectively establish a strong foundational growth trajectory for the segment.

However, the market faces significant restraints that temper growth rates. The high initial capital investment required for implementing sophisticated, high-capacity switchboards, especially those compliant with the latest arc flash mitigation standards and smart functionalities, can be prohibitive for small and medium enterprises (SMEs). Additionally, the switchboard market is often subject to cyclical trends in infrastructure and construction spending, making long-term growth planning susceptible to economic volatility. Another constraint is the existence of a large installed base of aging, yet functional, equipment in developed markets, which often delays replacement cycles, favoring repair or refurbishment over full system upgrades unless mandatory regulatory changes force modernization.

Opportunities for switchboard manufacturers are predominantly concentrated in the modernization and smartification of the electrical grid. The global push for smart grid implementation offers manufacturers the chance to integrate advanced IoT connectivity, cybersecurity features, and microgrid management functionalities directly into switchboard designs. Retrofitting aging infrastructure in mature markets represents another major opportunity, focusing on modular upgrades that enhance safety and efficiency without requiring complete system overhaul. The emergence of specialized applications, such as large data center facilities demanding unparalleled reliability and redundancy (N+1 architectures), also opens niche, high-value markets for advanced, custom-engineered switchboard solutions. The combined force of these factors ensures that while core market growth remains steady, significant value addition is concentrated around technological superiority and service offerings.

The Switchboard Market is systematically segmented based on multiple critical parameters, including the type of voltage handled, the application sector where they are deployed, the insulation medium used, and the mounting arrangement. This comprehensive segmentation allows market participants to tailor products precisely to regulatory, environmental, and operational requirements unique to each category. The complexity and feature set of a switchboard vary dramatically across these segments; for instance, high-voltage switchgear used in utility transmission differs substantially from low-voltage panels utilized in commercial building distribution, necessitating specialized manufacturing and supply chain expertise for each segment. Understanding these segment dynamics is crucial for market penetration strategies and product development focused on addressing specific end-user needs and optimizing cost structures.

The value chain for the Switchboard Market begins with the upstream segment, primarily involving raw material sourcing and the manufacturing of core components. Key upstream suppliers provide essential materials such as specialized steel and aluminum sheets for enclosures, copper and aluminum busbars for power conduction, insulating materials, and complex electronic components like circuit breakers, protective relays, and control units. Efficiency in this segment hinges heavily on minimizing commodity price volatility and ensuring stringent quality control for foundational electrical components, which directly dictates the ultimate safety and reliability of the final product. Strong partnerships with specialized component manufacturers are essential for vendors aiming for competitive differentiation through superior technology integration and miniaturization.

The midstream segment involves the core activities of design, manufacturing, assembly, and testing of the final switchboard unit. Manufacturers leverage engineering expertise to customize designs according to client specifications, ensuring compliance with diverse international standards (e.g., IEC, ANSI) and local codes. The distribution channel, which spans direct sales and indirect routes, plays a crucial role in delivering the complex, bulky products to end-users. Direct distribution is common for large-scale utility and industrial projects where customization and complex installation support are required. Indirect distribution often utilizes specialized electrical contractors, system integrators, and distributors who provide local sales support, installation services, and after-market maintenance, significantly extending the manufacturer’s reach, particularly in the commercial and smaller industrial sectors.

Downstream activities focus on installation, commissioning, operation, and maintenance. Given the critical nature of electrical distribution, installation must be performed by highly skilled professionals. Post-installation, the lifecycle value extends through maintenance, monitoring, and eventual retrofitting or replacement. Modern switchboards generate significant revenue opportunities in the after-sales market through service contracts, spare parts sales, and software updates for smart functionality. The entire value chain is characterized by a high degree of integration between product and service, where the quality of components and the professionalism of installation jointly determine the overall value proposition delivered to the end-user.

Potential customers for switchboards span a vast spectrum of industries and infrastructure projects, categorized primarily by their application and required power capacity. The industrial sector represents a critical end-user base, encompassing heavy manufacturing facilities, automotive plants, chemical processing units, and highly power-intensive operations such as mining and metallurgy. These industrial clients demand robust, highly reliable switchboards capable of handling large transient loads and adverse operating environments, with a strong focus on motor control centers (MCCs) integrated within the switchboard structure. Reliability and durability are non-negotiable for these end-users, as downtime can lead to substantial financial losses and safety hazards, making them high-value buyers requiring customized engineering solutions.

The utility sector is another dominant customer segment, comprising public and private power generation, transmission, and distribution companies. Utilities procure large, often high-voltage (or specialized medium-voltage) switchgear and control panels for substations, necessitated by grid expansion, reinforcement, and the integration of new renewable energy projects like solar farms and offshore wind installations. These buyers prioritize adherence to stringent grid codes, longevity, and advanced communication capabilities for seamless integration into supervisory control and data acquisition (SCADA) systems, often engaging in long-term supply contracts with established global manufacturers who can meet rigorous specifications and delivery timelines.

The commercial and infrastructure sector includes developers and operators of large commercial buildings, data centers, hospitals, educational institutions, and airport facilities. These customers typically require sophisticated, space-saving low-voltage and medium-voltage switchboards that emphasize energy efficiency, system redundancy (especially in critical facilities like data centers and hospitals), and advanced metering features necessary for tenant billing and energy performance management. Demand here is driven by new construction activity and ongoing modernization efforts to comply with modern building codes and improve operational sustainability. The residential market, primarily focused on low-voltage distribution panels, represents a high-volume market segment driven by mass housing projects and individual home construction, emphasizing cost-effectiveness and ease of installation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 billion |

| Market Forecast in 2033 | USD 6.67 billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, Schneider Electric SE, ABB Ltd., Eaton Corporation, General Electric (GE), Mitsubishi Electric Corporation, Larsen & Toubro (L&T), Lucy Electric, Powell Industries, Hyosung Heavy Industries, Crompton Greaves, TECO Electric & Machinery Co., Ltd., Hyundai Electric & Energy Systems Co., Ltd., Fuji Electric Co., Ltd., Rockwell Automation, WEG S.A., Norelco, Alstom, Bharat Heavy Electricals Limited (BHEL). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Switchboard Market is rapidly evolving from purely electromechanical distribution centers to highly sophisticated, digitized power management systems, driven primarily by the integration of communication technologies and advanced protection features. Key technological advancements center around enhancing safety, improving reliability, and facilitating seamless network integration. Modern switchboards increasingly incorporate features for arc flash mitigation, utilizing advanced sensor technology and rapid tripping mechanisms, such as arc quenching devices, to significantly reduce the risk and severity of internal electrical faults. This focus on safety compliance is paramount, dictating investment in standardized, certified designs and specialized materials. Furthermore, the adoption of microprocessor-based protective relays has replaced older electromechanical relays, offering superior accuracy, comprehensive diagnostic capabilities, and the flexibility for remote configuration and monitoring, central to modern asset management strategies.

The proliferation of the Industrial Internet of Things (IIoT) is fundamentally reshaping switchboard functionality, enabling them to act as critical nodes in smart grids and smart buildings. Modern switchboards are equipped with integrated smart metering, power quality monitoring systems, and communication interfaces (e.g., Modbus, Ethernet/IP) that allow for real-time data collection and remote supervisory control via Building Management Systems (BMS) or SCADA platforms. This connectivity permits facility managers to monitor load profiles, track energy efficiency metrics, and diagnose system health proactively, moving towards predictive maintenance models. The use of digital twins is also gaining traction, allowing engineers to simulate various operational scenarios and potential fault conditions before deployment, ensuring optimal performance and safety compliance under varying load demands and environmental factors.

In terms of physical design, the market is seeing increased utilization of Gas Insulated Switchgear (GIS), particularly in medium and high-voltage applications where space is constrained and environmental robustness is required. GIS uses inert gas (Sulfur Hexafluoride or increasingly, eco-friendly alternatives) as the primary insulating medium, resulting in much smaller footprints and sealed, maintenance-reduced designs compared to traditional Air Insulated Switchboards (AIS). Material science advancements are also critical, focusing on developing lighter, stronger, and more thermally efficient materials for busbars and enclosures, which contribute to the overall reduction in physical size and improvement in system longevity. The continuous development of vacuum interrupter technology within medium voltage switchgear further enhances operational lifespan and minimizes maintenance requirements, confirming the technological trajectory towards higher reliability and digital integration.

The Switchboard Market is projected to experience a Compound Annual Growth Rate (CAGR) of 5.8% during the forecast period from 2026 to 2033, driven primarily by global infrastructure modernization and smart grid investments.

Renewable energy integration mandates that switchboards be capable of managing bi-directional power flow, incorporating advanced protective relays, and facilitating higher levels of power quality monitoring, driving demand for smart, digitally enabled systems.

The Asia Pacific (APAC) region currently dominates the global Switchboard Market in terms of market share and exhibits the highest growth rate, due to rapid urbanization, massive industrial expansion, and government-led infrastructure investments.

The primary restraint on market growth is the high initial capital investment required for installing modern, high-capacity switchboards, particularly those equipped with advanced safety features like arc flash mitigation technology.

AI integration enables advanced predictive maintenance by analyzing operational data in real-time to forecast potential component failures, thereby minimizing unplanned downtime and enhancing overall system reliability and safety.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.