ID : MRU_ 442174 | Date : Feb, 2026 | Pages : 255 | Region : Global | Publisher : MRU

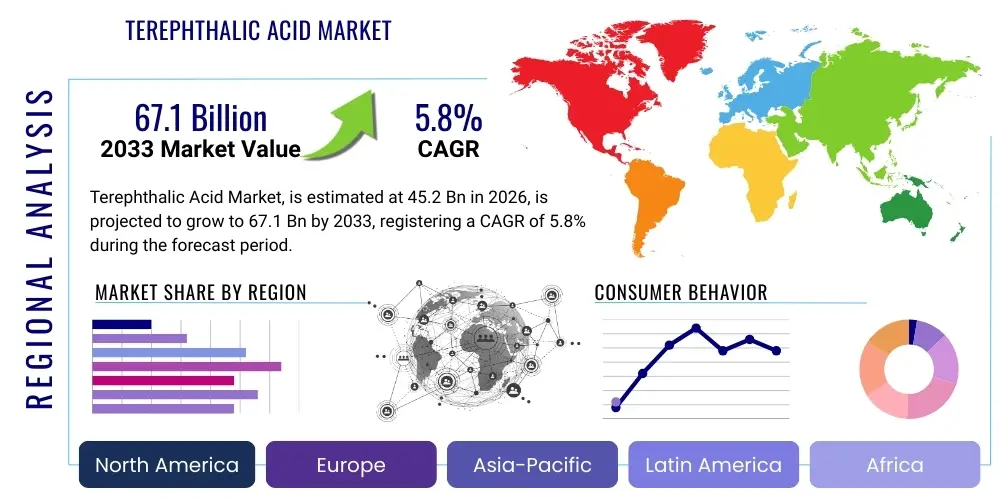

The Terephthalic Acid Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $45.2 Billion in 2026 and is projected to reach $67.1 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for Polyethylene Terephthalate (PET), primarily across the packaging and textile sectors. Developing economies, particularly in Asia Pacific, are central to this growth trajectory, characterized by rising disposable incomes, rapid urbanization, and a consequential surge in packaged consumer goods consumption. The transition towards lightweight and recyclable packaging solutions further cements TPA’s crucial role as a primary chemical intermediate, positioning it for robust market expansion over the forecast horizon.

Terephthalic Acid (TPA) is a crucial aromatic dicarboxylic acid, predominantly consumed in the form of Purified Terephthalic Acid (PTA), which serves as a vital intermediate chemical feedstock for producing Polyethylene Terephthalate (PET) and Polybutylene Terephthalate (PBT). The product, typically derived through the catalytic liquid-phase oxidation of p-Xylene, is foundational to numerous industries, most notably in the manufacture of polyester fibers for textiles, resins for beverage bottles, and films for advanced packaging applications. Its widespread adoption is underpinned by its superior physical properties, including high strength, excellent thermal stability, and effective barrier characteristics, making it indispensable in modern material science and consumer product manufacturing.

The major applications of TPA are intrinsically linked to the performance characteristics of PET, which accounts for over 85% of global TPA consumption. In the textile industry, polyester fibers derived from TPA offer durability, wrinkle resistance, and cost-effectiveness, sustaining strong demand, especially from fast-fashion and sportswear segments. Furthermore, the increasing preference for safe, lightweight, and shatterproof packaging drives the demand for PET bottles and containers used in carbonated soft drinks, water, and edible oils, significantly bolstering the TPA market’s revenue streams. Environmental considerations are also subtly shaping the market, as TPA enables the creation of highly recyclable PET materials, appealing to both producers and consumers focused on sustainability initiatives.

Key benefits associated with TPA utilization include its high reactivity in polymerization processes, resulting in materials with excellent clarity and mechanical properties, essential for demanding packaging standards. The primary driving factors for the TPA market include sustained population growth, infrastructural development leading to increased construction and automotive applications utilizing derived plastics, and the continuous expansion of the food and beverage industry in emerging markets. Economic recovery and stabilized crude oil prices, which influence the cost of the key feedstock p-Xylene, also play a significant role in maintaining favorable production economics for TPA manufacturers globally, ensuring continued investment in large-scale production facilities.

The global Terephthalic Acid (TPA) market is characterized by intense integration within the petrochemical value chain, with capacity additions largely concentrated in the Asia Pacific region, driven primarily by China and India’s burgeoning polyester and packaging sectors. Business trends show a strong shift towards mega-scale integrated refining and petrochemical complexes to achieve economies of scale and improve feedstock security, particularly concerning p-Xylene supply. Furthermore, market players are increasingly focusing on process optimization, aiming to reduce energy consumption and improve the purity of the end product (PTA) to meet stringent requirements from specialized PET applications, such as high-performance barrier films and bio-based plastics blending. Consolidation among major manufacturers and strategic joint ventures aimed at geographical expansion and technology sharing are also prominent trends shaping the competitive landscape.

Regionally, the Asia Pacific dominates the TPA market in terms of both production capacity and consumption volume, owing to its massive textile manufacturing base and rapidly expanding packaged goods sector. While North America and Europe demonstrate mature market growth, they are characterized by slower, more stable demand, alongside a strong emphasis on sustainability, leading to higher adoption rates of recycled PET (rPET) and increasing regulatory scrutiny on plastic usage. The Middle East and Africa (MEA) region is emerging as a potential export hub, leveraging access to cheap natural gas and oil resources for feedstock, positioning its manufacturers advantageously in the global supply chain, though domestic consumption remains comparatively low relative to Asia.

Segment trends highlight the overwhelming dominance of the Polyethylene Terephthalate (PET) resin segment, fueled by the relentless demand for packaging materials. Within PET, the bottle grade category shows the fastest growth, propelled by the shift from glass and aluminum packaging in the beverage industry due to PET’s lightweight nature and improved carbon footprint during transport. The polyester fiber segment, although mature, maintains significant volume due to its foundational role in apparel and technical textiles. Furthermore, the market is observing a growing interest in specialty applications like polybutylene terephthalate (PBT) for engineering plastics in the automotive and electrical/electronics sectors, suggesting diversification opportunities outside the conventional large-volume PET market segments, albeit these specialty applications account for a much smaller share.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Terephthalic Acid market primarily center on operational efficiency, predictive maintenance for complex reactor systems, optimization of supply chain logistics for bulk chemicals, and enhancing R&D for novel catalysts. Key themes reveal user expectations that AI will significantly reduce manufacturing costs, improve product purity consistency through real-time process adjustments, and provide advanced forecasting capabilities for volatile p-Xylene prices. There is also a keen interest in how AI algorithms can accelerate the development and scale-up of sustainable and bio-based TPA production routes, addressing growing environmental and regulatory pressures on traditional petrochemical synthesis. These inquiries underscore the industry’s readiness to leverage advanced analytics for achieving competitive advantage in a high-volume, low-margin commodity market.

AI’s deployment within TPA manufacturing facilities enables sophisticated process control far beyond traditional automation capabilities. Machine learning models analyze vast streams of operational data—including temperature, pressure, flow rates, and catalytic reaction kinetics—to predict deviations and optimize reaction conditions in real-time, maximizing yield and reducing off-spec product generation. This level of precision is critical in PTA production where maintaining high purity is paramount for subsequent polymerization processes. Moreover, AI-driven simulations can rapidly test and refine new catalyst formulations or optimize existing catalyst lifecycles, translating directly into lower operational expenditure and improved overall plant reliability. This capability is vital for maintaining sustained high-capacity utilization rates essential for profitability in the petrochemical sector.

From a commercial perspective, AI algorithms are revolutionizing the feedstock procurement and logistics components of the TPA value chain. Given the global nature of p-Xylene supply and its price volatility influenced by geopolitical and refining market shifts, AI provides highly accurate predictive models for purchasing decisions, minimizing raw material costs. Furthermore, AI-powered systems optimize shipping schedules, inventory management, and warehousing of large volumes of TPA, reducing demurrage and logistical bottlenecks across major ports and inland distribution networks. The strategic application of AI thus transforms TPA production from a reactive, historical data-driven operation into a proactive, predictive enterprise, ensuring resilience against market fluctuations and enhancing responsiveness to customer demand variations globally.

The Terephthalic Acid (TPA) market dynamics are shaped by a complex interplay of Drivers, Restraints, Opportunities, and broader Impact Forces. The primary driver is the unceasing global demand for packaging materials, particularly PET resin, fueled by population growth, urbanization, and the expanding e-commerce sector requiring durable and lightweight shipping materials. Opportunities lie significantly in the development and commercialization of bio-based TPA (Bio-PTA) alternatives, which align with circular economy goals and offer manufacturers a pathway to meet increasingly stringent sustainability standards imposed by global consumer brands and regulators. Conversely, the market faces restraints, chiefly volatile feedstock prices, specifically p-Xylene, which directly influences production costs, and increasing environmental opposition to single-use plastics, which could mandate greater substitution with recycled materials or non-PET alternatives, placing pressure on virgin TPA demand.

One major impact force shaping the competitive environment is regulatory pressure concerning plastic waste management and recycling mandates, particularly in Europe and North America. These regulations encourage investment in advanced recycling technologies, potentially stabilizing demand for TPA as a high-quality polymer base, but simultaneously fostering growth in recycled PET (rPET) consumption, which might slow the growth rate of virgin TPA production. The continuous commissioning of large-scale, integrated TPA plants in the Asia Pacific region, primarily China, acts as another significant impact force, leading to temporary oversupply situations and compressing profit margins globally, requiring continuous technological innovation to maintain cost competitiveness among international players.

The long-term viability of the TPA market is heavily reliant on sustained technological advancements, particularly in reducing the energy intensity of the PTA manufacturing process and improving catalyst performance. The potential market opportunity presented by emerging applications, such as high-performance PBT for electric vehicle components and specialized polyester films for photovoltaic backsheets, promises avenues for premium pricing and market diversification away from solely commodity PET bottles. However, global economic uncertainties and trade tensions impacting cross-border petrochemical supply chains represent persistent restraints, demanding careful capacity management and resilient sourcing strategies from key industry stakeholders to mitigate macroeconomic risks. Successful market players are those that effectively navigate the transition toward sustainable practices while ensuring superior operational efficiency.

The Terephthalic Acid market is primarily segmented based on its application, derivative type, and grade, reflecting its versatile use across industrial sectors, though the Polyethylene Terephthalate (PET) application segment remains the overwhelmingly dominant consumer. Understanding these segmentations is critical for analyzing market dynamics, pricing mechanisms, and future investment strategies. The major derivative, Purified Terephthalic Acid (PTA), largely dictates the market structure due to its high purity requirements essential for high-quality PET production. Analyzing growth across the various end-use segments, such as packaging versus textiles, allows manufacturers to strategically allocate capital towards higher-growth or higher-margin application niches.

The Application segmentation clearly delineates the massive influence of the packaging sector, particularly the beverage industry, on TPA demand volumes, which is directly linked to global consumer trends and regulatory shifts regarding food contact materials. Conversely, the Derivative segmentation differentiates between PTA and the historically significant, though now less common, Dimethyl Terephthalate (DMT), highlighting the industry's technological evolution toward more efficient and environmentally preferable PTA routes. The Grade segmentation reflects the varying quality needs across end-user industries, with high-purity TPA necessary for clear PET bottles and standard grades often sufficing for bulk industrial fibers or certain construction materials, driving differential pricing structures across the market.

Strategic analysis of these market segments reveals that future growth is most concentrated in the application of PET resin, particularly in markets experiencing significant economic modernization and rising middle-class consumption patterns. Technological advancements are focused on maintaining the ultra-high purity required for bottle-grade PET while simultaneously exploring ways to lower the carbon footprint of production, impacting both derivative processing and raw material sourcing. This detailed market segmentation provides the framework for assessing competitive intensity, identifying white space opportunities, and accurately forecasting the future trajectory of TPA consumption across diverse geographical and industrial landscapes.

The Terephthalic Acid value chain is complex and highly capital-intensive, starting from the upstream procurement of crude oil and natural gas, followed by refining processes to yield key aromatics, primarily paraxylene (p-Xylene), which constitutes the single largest cost component in TPA production. Upstream analysis focuses heavily on the integration of p-Xylene production capabilities with large refining complexes, as this co-location significantly reduces transportation costs and enhances feedstock security, a critical competitive advantage. Major players often operate integrated refinery-petrochemical complexes, minimizing exposure to volatile spot market prices for p-Xylene. The efficient and continuous supply of high-quality p-Xylene is paramount, as interruptions or purity variations can severely impact the TPA conversion process and downstream product quality.

The core manufacturing stage involves the catalytic liquid-phase oxidation of p-Xylene, known as the Amoco/BP process, followed by purification to produce Purified Terephthalic Acid (PTA). This stage demands high technological sophistication and stringent quality control, especially to achieve the ultra-high purity required for bottle-grade PET. Downstream analysis focuses on the rapid conversion of PTA into polymer products, predominantly PET, which is then utilized across various end-use sectors. The major downstream industries include packaging (bottles, containers, films), textiles (polyester fiber), and engineering plastics (PBT). The efficiency and scale of downstream conversion capacity directly influences the sustained demand for PTA, creating a highly interdependent relationship within the value chain.

Distribution channels for TPA are typically bulk and centralized due to its nature as a commodity chemical sold in powder form, often transported in specialized rail cars, trucks, or ships to large-scale polymer manufacturing facilities. Direct distribution characterizes the relationship between large integrated TPA producers and major PET resin manufacturers, often involving long-term supply contracts and pipeline delivery for adjacent facilities, ensuring minimal logistical friction. Indirect distribution involves trading companies and specialized chemical distributors for smaller or localized end-users, though this constitutes a minor portion of the overall market. The strategic location of TPA production facilities, often near large ports or major consumption centers in Asia, is crucial for optimizing logistics and minimizing delivery times to high-volume end-users, thus consolidating the global trade flow of this essential chemical intermediate.

The primary potential customers and buyers of Terephthalic Acid (TPA), predominantly in its purified form (PTA), are large-scale polymer manufacturers specializing in the production of Polyethylene Terephthalate (PET) resin and polyester fibers. Companies operating in the packaging sector, particularly those focused on bottling carbonated soft drinks, mineral water, and edible oils, represent the most significant purchasing cohort due to the unmatched barrier properties and lightweight nature of PET containers. These customers demand extremely high purity levels of PTA to ensure product clarity and mechanical strength, making supplier quality consistency a crucial purchasing determinant. The volume requirement from this sector is immense and directly correlated with global consumer trends in beverages and packaged foods.

A secondary, yet substantial, group of customers includes textile and apparel manufacturers who rely on PTA for producing polyester staple and filament fibers. These fibers are integral to the fast-fashion supply chain, technical textiles, and industrial fabric production, offering durability and cost-effectiveness. Furthermore, specialized chemical companies that manufacture engineering plastics, specifically Polybutylene Terephthalate (PBT), are growing customers, leveraging TPA derivatives for high-performance applications in the automotive, electrical, and electronics industries where strength, heat resistance, and dimensional stability are critical requirements. The demand profile of these customers is often less volume-driven but highly specification-dependent, seeking suppliers capable of customizing purity levels or offering specialized derivatives.

The customer base also extends to manufacturers of plasticizers (such as Dioctyl Terephthalate - DOTP), which are increasingly preferred over traditional phthalate plasticizers due to environmental and health concerns, providing a growing niche market for TPA utilization. Finally, petrochemical trading houses and distributors act as intermediaries, connecting major TPA producers with smaller, localized converters and manufacturers who require smaller, more flexible delivery volumes. Understanding the specific quality requirements, inventory management practices, and geopolitical supply constraints of these diverse customer segments is essential for TPA producers aiming to maximize market penetration and secure long-term, high-value supply contracts.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $45.2 Billion |

| Market Forecast in 2033 | $67.1 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Reliance Industries, Sinopec, BP (now INEOS), Eastman Chemical Company, Mitsubishi Chemical Corporation, SABIC, Indorama Ventures Public Company Limited, SIBUR Holding, Indian Oil Corporation, Hanwha Group, Lotte Chemical Corporation, PTT Global Chemical Public Company Limited, Nan Ya Plastics Corporation, Jiangsu Sanfangxiang Group, Zhejiang Hualian, CEPSA, FENC (Far Eastern New Century), Yisheng Petrochemical, BASF SE, Formosa Plastics Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Terephthalic Acid market is primarily defined by continuous advancements in the catalytic oxidation process, aiming for enhanced yield, reduced energy consumption, and crucially, higher purity of the Purified Terephthalic Acid (PTA). The established benchmark technology remains the modified Amoco/BP process (now owned by INEOS and various licensees), which utilizes liquid-phase catalytic oxidation of p-Xylene in acetic acid solvent. Recent technological innovations focus on optimizing the purification stage through hydrogenation—specifically, improving reactor design and catalyst efficiency to minimize impurities like 4-carboxybenzaldehyde (4-CBA), which can negatively affect downstream PET polymerization processes, thus ensuring the high quality demanded by the bottle-grade market.

A significant trend in technological development involves the exploration and scaling up of sustainable and circular TPA production methods. Chemical recycling technologies, such as glycolysis or methanolysis, are gaining traction, allowing TPA to be recovered directly from post-consumer PET waste. While currently nascent in large-scale commercial viability compared to virgin production, these processes represent a critical technological pathway for achieving circular economy goals and reducing reliance on fossil fuel feedstocks. Furthermore, bio-based TPA (Bio-PTA) production, derived from renewable resources like sugars or biomass through fermentation and subsequent chemical conversion, is an emerging technology seeking to provide a low-carbon footprint alternative, attracting significant R&D investment from major chemical companies and consumer brands committed to green sourcing.

Moreover, digitalization and advanced control systems are becoming integral to modern TPA plants. The implementation of digital twins, advanced process control (APC), and sophisticated sensor technologies allows for real-time monitoring and adaptive adjustments to the complex catalytic reactors, optimizing throughput and reducing variability. This integration of Industrial Internet of Things (IIoT) and AI-driven analytics minimizes waste, optimizes the lifespan of expensive catalysts, and reduces operational risk associated with high-pressure, high-temperature chemical reactions. These technological shifts are essential not only for improving profitability but also for meeting increasingly stringent environmental performance metrics related to emissions and energy efficiency in the competitive petrochemical manufacturing sector.

The overwhelming primary application driving TPA demand is the production of Polyethylene Terephthalate (PET) resin, which is extensively utilized in the packaging industry for manufacturing plastic bottles, containers, and films, accounting for over 85% of global consumption.

P-Xylene is the critical feedstock for TPA production, representing the largest single cost component. Its price volatility, influenced by crude oil prices and refinery operations, directly impacts the operating margins and profitability of TPA manufacturers globally, necessitating robust hedging and integration strategies.

The Asia Pacific (APAC) region, led by China and India, holds the largest market share. This dominance is attributed to rapid industrialization, massive investments in textile and polyester fiber manufacturing, high urbanization rates, and explosive growth in packaged consumer goods consumption.

Key technological trends include the integration of advanced process control (APC) and AI for operational efficiency, continuous improvement in hydrogenation purification to achieve ultra-high purity PTA, and intense R&D investment into sustainable alternatives like bio-based TPA and chemical recycling technologies for PET waste.

Purified Terephthalic Acid (PTA) is the dominant derivative used today, offering higher purity and cost efficiency for PET production. Dimethyl Terephthalate (DMT) is an older derivative, historically used but now largely superseded by PTA due to process efficiency, though it retains niche applications in certain specialized polyester and PBT manufacturing.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.