ID : MRU_ 443601 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

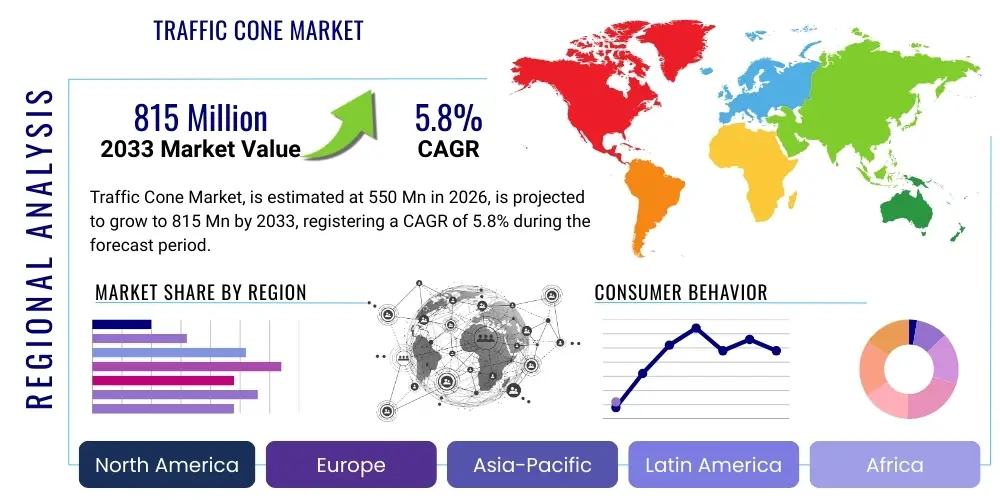

The Traffic Cone Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $550 Million in 2026 and is projected to reach $815 Million by the end of the forecast period in 2033. This consistent expansion is primarily fueled by increasing global infrastructure development, stringent governmental regulations concerning worker and pedestrian safety in construction zones, and the continuous need for temporary traffic control devices across metropolitan areas.

Market valuation growth reflects the mandatory adoption of safety standards codified by bodies such as the Federal Highway Administration (FHWA) and similar international safety organizations. Demand is particularly robust in developing economies undertaking massive urban expansion projects. Furthermore, technological advancements leading to durable, reflective, and eco-friendly traffic cone materials are contributing positively to the overall market valuation. The shift towards recycled and sustainable materials presents a latent opportunity for manufacturers to capture environmentally conscious public sector contracts, ensuring stable revenue streams and market resilience against economic fluctuations.

The Traffic Cone Market encompasses the manufacturing, distribution, and deployment of portable, temporary channelizing devices predominantly used for redirecting traffic, demarcating hazardous areas, and signaling construction zones. Traffic cones, commonly fabricated from materials such as PVC, rubber, and high-density polyethylene (HDPE), are essential components of passive road safety infrastructure. The primary application spans public works, highway construction, utility maintenance, parking lot management, and event management, ensuring the smooth and safe flow of vehicles and pedestrians.

Key benefits derived from the utilization of traffic cones include enhanced visibility due to bright colors (typically orange or lime green) and reflective collars, ease of deployment and retrieval, versatility across diverse weather conditions, and compliance with mandated safety standards. Traffic cones serve as the initial layer of defense in temporary work zones, mitigating risks of accidents and minimizing liabilities for infrastructure developers. Their low cost and high impact visibility make them indispensable tools for effective temporary traffic control planning (TTCP).

Major driving factors influencing the market include rapid urbanization necessitating frequent road repairs and utility upgrades, rising governmental expenditure on public safety infrastructure worldwide, and the increasing focus on occupational safety protocols in industrial and construction sectors. Furthermore, the advent of smart traffic systems and connected infrastructure, while not directly replacing cones, often necessitates their use during installation and maintenance phases, ensuring continued foundational demand for these essential safety products.

The Traffic Cone Market demonstrates stable growth driven by non-discretionary safety expenditure and robust governmental spending on infrastructure maintenance. Key business trends indicate a strong move toward durability and sustainability, with manufacturers investing in specialized UV-resistant PVC and recycled rubber formulations to enhance product lifespan and reduce environmental impact. Pricing remains competitive, though differentiation is achieved through compliance with high-visibility standards (e.g., retroreflectivity performance) and specialized features like interlocking bases or collapsible designs for enhanced storage efficiency. Operational efficiencies in manufacturing, particularly high-volume injection molding processes, are critical for maintaining competitive pricing and maximizing global supply chain responsiveness.

Regionally, North America and Europe maintain maturity, characterized by highly stringent safety regulations mandating sophisticated cone designs, while the Asia Pacific (APAC) region is poised for the fastest expansion, fueled by massive, long-term national infrastructure programs in China, India, and Southeast Asian nations. Latin America and the Middle East & Africa (MEA) are also exhibiting heightened demand, primarily linked to resource extraction projects, expanding urban centers, and the modernization of existing road networks. These regional trends underscore the necessity for market participants to tailor product specifications—such as weight distribution for wind stability or temperature tolerance for extreme climates—to local regulatory and environmental requirements.

Segment trends highlight the dominance of PVC cones due to their favorable cost-to-durability ratio, though demand for specialized reflective and weighted base cones is increasing significantly across premium application segments like high-speed highways. Application segmentation shows Construction & Public Works as the largest user base, though the rise of event management and private sector warehousing logistics is creating niche demand for smaller, stackable, or custom-branded safety cones. The focus on worker safety mandates is continuously elevating the standards for cone height and reflective sheeting quality, pushing manufacturers towards higher-margin, performance-driven products.

User questions regarding the impact of Artificial Intelligence on the Traffic Cone Market frequently center on whether autonomous vehicles (AVs) and advanced construction robotics will render passive safety devices obsolete, or if AI-driven planning systems could optimize cone deployment. Key themes observed include concerns about the long-term relevance of traditional visual markers versus digital signaling, the potential for AI-powered drones to monitor and manage cone placement efficiency, and the integration of smart sensors into cones to transmit real-time data on impacts or movement. Users are keen to understand if AI will lead to the development of 'smart cones' that actively communicate with connected infrastructure and AVs, fundamentally changing the product's function from a passive barrier to an active safety system component.

The reality is that while AI and automation will significantly alter traffic management, they are unlikely to fully replace physical cones in the foreseeable future. AI excels at predictive modeling and optimization; therefore, its primary impact will be in enhancing the efficiency of cone deployment, real-time work zone configuration adjustments based on immediate traffic flow data, and preventative maintenance planning for safety assets. AI algorithms can process sensor data from cones (e.g., GPS location, tilt sensors) to ensure regulatory compliance and immediate notification of displaced devices, minimizing safety hazards associated with poorly managed temporary traffic controls. This integration represents a shift from a basic physical product to an element within a sophisticated, interconnected safety ecosystem, demanding high-durability sensors and integrated communication capabilities within the cone structure itself.

Furthermore, AI-powered computer vision systems deployed in autonomous vehicles still rely on redundant physical markers, especially in adverse weather conditions or unpredictable work zone environments. The traffic cone remains a fundamental, universally recognized physical delimiter. AI’s role is thus transformative, moving the market toward premium, sensor-enabled cones that provide valuable data feedback loops rather than pure replacement. This evolution necessitates partnerships between traditional cone manufacturers and technology providers specializing in low-power IoT sensing and data analytics, driving product innovation in the mid to long-term horizon.

The Traffic Cone Market is substantially influenced by strong safety mandates (Drivers) countered by cyclical economic vulnerability (Restraints), with technological evolution in materials offering significant growth avenues (Opportunities). The primary drivers include aggressive global governmental investments in highway expansion and maintenance, coupled with increasingly strict enforcement of worker safety standards established by organizations like OSHA globally. These mandatory requirements ensure a baseline demand irrespective of short-term economic fluctuations. Furthermore, the longevity and ubiquity of the product ensure that it remains the most cost-effective and universally recognized method of temporary traffic management.

Restraints primarily revolve around the fluctuating cost of raw materials, particularly crude oil derivatives used in PVC and plastic manufacturing, leading to unpredictable input costs for manufacturers. Additionally, the market suffers from a low barrier to entry for standard, non-specialized cones, which intensifies pricing pressure and commoditization, limiting profit margins for non-innovative players. Issues related to cone degradation, high replacement rates due to theft or damage, and environmental concerns regarding non-recyclable plastic waste also pose operational and reputational challenges that must be addressed through material innovation and enhanced durability engineering.

Opportunities are abundant in the sphere of advanced materials and product features. The development of high-performance, eco-friendly cones utilizing recycled plastics or biodegradable polymers attracts environmentally conscious government buyers. Furthermore, integrating smart technology, such as active lighting or embedded RFID/IoT chips for asset tracking and real-time data feedback, provides manufacturers with a premium segment offering. The global expansion of niche applications, including automated parking facilities and mega-event security, offers untapped regional market potential beyond traditional construction segments, diversifying the revenue streams for specialized cone producers. These impact forces collectively define a stable, yet evolving market landscape where innovation in durability and smart features will be key determinants of competitive success.

The Traffic Cone Market segmentation provides a granular view of demand based on material composition, product height, application scope, and purchasing channel. Analyzing these segments is critical for manufacturers to align their production capabilities with specific end-user requirements, particularly regarding compliance with varying national road safety standards. The core segmentation is driven by performance parameters such as wind resistance, UV stability, and crash durability, differentiating standard safety cones from specialized high-performance variants used in high-speed traffic environments. Understanding the dominance of certain materials, like PVC, versus the growing preference for eco-friendly alternatives allows for targeted marketing and strategic inventory management.

The market is broadly categorized into key dimensions that reflect utility and regulatory requirements. Material type dictates cost and resilience, while height and weight classifications are often mandated by regulatory bodies based on the speed limit of the roadway where the cones are deployed. Application segmentation illustrates the primary revenue drivers, with infrastructure maintenance and new construction dominating consumption volumes. Regional differences often influence the preferred cone height and color schemes (e.g., predominantly orange in North America, often variations of red/white in other regions), necessitating localized product offerings for global players. The complexity of these segment requirements necessitates adaptable manufacturing processes capable of small-batch customization alongside high-volume production of standardized products.

The value chain of the Traffic Cone Market begins with upstream activities focused on raw material procurement, primarily petrochemical derivatives (PVC resin, plasticizers) and rubber compounds. Manufacturers must maintain strategic relationships with chemical suppliers to mitigate volatility in input costs, which directly impacts final product pricing. Efficiency in the compounding and coloring process is crucial for achieving mandated regulatory standards for color uniformity and UV resistance. Manufacturing is dominated by injection molding or roto-molding processes, requiring specialized tooling and energy-efficient operations to manage large volumes. Upstream competition heavily relies on scale and technological capability to produce consistent, high-quality material batches suitable for safety-critical applications.

Downstream activities center on distribution, sales, and end-user deployment. The distribution channel is characterized by a mix of large, specialized industrial safety distributors, government procurement agencies, and direct sales to major construction and infrastructure firms. Indirect channels, primarily large e-commerce platforms and specialized safety supply retailers, serve smaller contractors and municipal buyers. The efficacy of the downstream supply chain depends significantly on logistical capabilities, as traffic cones are bulky and require efficient warehousing and shipping to minimize freight costs. Distributors often add value through inventory management, customization (e.g., branding, specialized reflective sheeting), and ensuring regional regulatory compliance, acting as a crucial interface between manufacturers and diverse end-users.

The structure of the value chain is relatively streamlined due to the physical nature of the product. Direct sales channels are often employed for large government tenders or long-term contracts with major highway maintenance contractors, ensuring transparent pricing and quality control. Indirect channels are essential for market penetration into smaller municipal areas and private industrial complexes. Overall, cost optimization at the manufacturing stage and robust logistical networks downstream are the key determinants of competitive advantage within the value chain.

The potential customer base for the Traffic Cone Market is highly diversified, encompassing any entity responsible for temporary changes in traffic flow, crowd control, or defining work boundaries. The largest and most consistent buyers are governmental bodies at federal, state, and municipal levels, including departments of transportation (DOTs) and public works agencies, as they continuously manage infrastructure projects, highway repairs, and utility upgrades. These customers prioritize regulatory compliance, durability, and bulk purchasing capacity, often requiring large volumes through competitive bidding processes.

Private sector customers represent another significant buyer segment, particularly large-scale construction companies engaged in residential, commercial, and industrial site development. These firms require cones for safety compliance on active work sites, parking facilities, and material staging areas. Beyond construction, the energy sector (oil, gas, utility companies) requires extensive cone deployment during maintenance and expansion activities, often demanding specialized, heavy-duty cones suitable for harsh environments and high visibility requirements.

Furthermore, auxiliary markets such as event management companies, airport authorities, warehousing and logistics firms, and educational institutions constitute specialized customer groups. Event organizers require temporary demarcation for parking and crowd movement, while logistics centers use cones for defining internal traffic routes and hazardous material zones. These end-users typically value ease of storage (collapsible cones) and custom branding options, demonstrating the broad, indispensable nature of traffic cones across virtually every major economic sector involved in physical operations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $550 Million |

| Market Forecast in 2033 | $815 Million |

| Growth Rate | CAGR 5.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | JBC Safety Products, Cortina Safety Products, Poly-Line Corporation, Radians, Trident Safety, A-Safe, Roadway Safety, TrafFix Devices, PEXCO, Plasticade, 3M (Reflective Materials), Honeywell Safety Products, Zizah Safety, Qwick Kurb, Emedco |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Traffic Cone Market is focused less on radical disruption of the product form itself, and more on enhancing material science, durability, and data integration capabilities. Advanced material technologies are central, specifically the development of higher-grade PVC and synthetic rubber compounds that offer superior UV resistance, cold-weather flexibility, and resistance to impact stress. Manufacturers are utilizing sophisticated formulations to ensure that the bright colors (e.g., fluorescent orange, lime green) remain visible and do not fade prematurely under prolonged sun exposure, which is a critical failure point impacting regulatory compliance. The focus is also shifting towards using recycled materials and bio-based plastics to meet environmental sustainability targets being set by municipal and government procurement processes globally.

Reflectivity technology is another key area of innovation. While standard reflective collars are common, the trend is moving toward high-intensity prismatic sheeting (HIP) and micro-prismatic technology, which significantly enhances nighttime visibility and conspicuity, exceeding minimum MUTCD (Manual on Uniform Traffic Control Devices) standards. Furthermore, active lighting integration is emerging, where LED lights or solar-powered strobes are incorporated into the cone structure itself. These active safety elements provide an extra layer of visibility in low-light conditions or during extreme weather, crucial for high-speed highway applications where early warning is paramount to preventing accidents. The technology ensures the cones actively draw attention rather than relying solely on ambient light reflection.

The most forward-looking technological development is the incorporation of Internet of Things (IoT) sensors and RFID tags. These devices transform the passive cone into a "smart" asset capable of transmitting critical data. IoT integration allows asset managers to track the exact GPS location of cones, monitor tilt status (to detect if a cone has been knocked over), and transmit environmental data. This capability significantly improves inventory management, reduces losses from theft or misplacement, and most importantly, enhances safety compliance by providing immediate alerts if a crucial traffic control point is compromised. This fusion of physical safety hardware with digital monitoring capabilities represents the future direction of premium segments within the Traffic Cone Market.

Regional dynamics play a crucial role in shaping the Traffic Cone Market, primarily due to differing infrastructure spending patterns, regulatory maturity, and climate variations that dictate material requirements. North America, driven by the United States and Canada, represents a high-value market characterized by stringent safety compliance (mandating specific cone heights, weights, and retroreflectivity levels) and continuous investment in highway modernization. The demand here is stable and focused on high-durability, premium cones, often favoring heavy, weighted bases to withstand high-speed traffic wind shear. The prevalence of robust state-level DOT requirements ensures ongoing replacement cycles and strong demand for specialized products adhering to specific regional transportation guidelines.

Europe exhibits steady growth, heavily influenced by EU directives and national safety standards, with a strong emphasis on sustainability. European markets are rapidly adopting cones made from recycled or environmentally certified materials, often prioritizing modular designs for easier storage and deployment. Western European countries, with dense urban centers, generate high demand for smaller, more manageable cones for urban street work and utility maintenance, whereas Eastern Europe's expanding highway networks fuel large-scale bulk procurement. Regulatory harmonization across the EU simplifies market entry for manufacturers but necessitates a strong focus on certification and adherence to material provenance standards.

The Asia Pacific (APAC) region is projected to experience the highest growth rate, fueled by unprecedented investments in railway, highway, and urban infrastructure development, particularly in China, India, and Indonesia. While price sensitivity remains high in this region, the sheer volume of construction activity generates massive demand. The market here is rapidly maturing, moving away from low-quality substitutes towards regulatory-compliant products, especially as global construction giants enter the market, enforcing international safety standards. This transition offers significant expansion opportunities for international manufacturers capable of offering cost-competitive yet compliant safety solutions tailored to diverse climatic extremes.

The primary governing standard in the US is the Manual on Uniform Traffic Control Devices (MUTCD), which specifies minimum height (e.g., 28 inches for high-speed roadways) and requires specific levels of retroreflectivity for collars. Globally, standards are set by regional bodies like EN 13422 in Europe or specific national transportation agencies, all focused on ensuring conspicuity and stability.

The volatility in petrochemical prices directly affects the cost of PVC and HDPE resins, the main raw materials for cones. Manufacturers typically manage this by implementing strategic long-term supply contracts, improving material efficiency in molding processes, and passing on selective cost increases to end-users, especially for commodity-grade products, thereby pressuring profit margins.

Sustainability is driven by the use of high-percentage recycled PVC and recycled rubber, reducing reliance on virgin plastics. Further advancements include bio-based polymers and specialized compounds designed for extended lifespan and ease of recycling at the end of the product cycle, which appeals strongly to government procurement offices focused on environmental mandates.

While not universally mandatory, smart cones equipped with GPS/IoT sensors are gaining traction, particularly in complex, high-liability construction zones and smart city initiatives. They are highly valued for asset management, theft prevention, and providing real-time compliance status, offering enhanced data capabilities that traditional cones cannot match, thus becoming preferred technology in premium segments.

The Asia Pacific (APAC) region, specifically the Construction & Public Works application segment, is expected to exhibit the highest growth rate. This is due to massive, ongoing national infrastructure modernization programs and rapidly increasing regulatory enforcement of safety standards across developing Asian economies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.