ID : MRU_ 442677 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

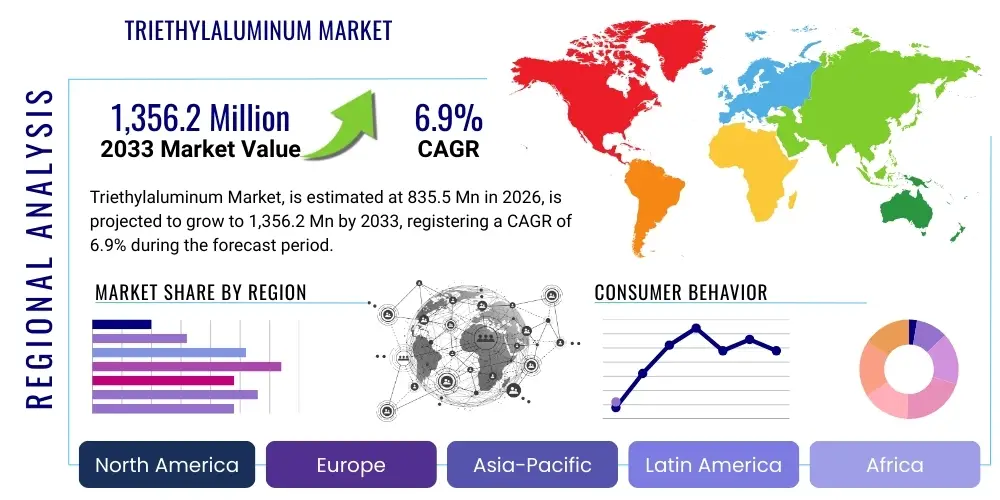

The Triethylaluminum Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.85% between 2026 and 2033. The market is estimated at USD 835.5 Million in 2026 and is projected to reach USD 1,356.2 Million by the end of the forecast period in 2033.

Triethylaluminum (TEA), an organoaluminum compound, is a highly reactive and pyrophoric liquid primarily recognized for its potent reducing and alkylating capabilities. This essential chemical intermediate is synthesized through complex processes, often involving aluminum, ethylene, and hydrogen, necessitating stringent safety protocols due to its tendency to ignite spontaneously upon exposure to air. Its critical role as a co-catalyst in Ziegler-Natta polymerization processes for the manufacture of polyolefins—specifically high-density polyethylene (HDPE), linear low-density polyethylene (LLDPE), and polypropylene (PP)—solidifies its commercial importance, linking its market performance directly to the global plastics industry's expansion and demand for commodity polymers.

Beyond its dominant application in polyolefin production, TEA serves as a vital precursor in the chemical synthesis sector, acting as a reducing agent, alkylating agent, and chain transfer agent. A rapidly growing, albeit smaller, application segment involves its use in the Metal-Organic Chemical Vapor Deposition (MOCVD) process, crucial for manufacturing advanced electronic materials like Gallium Nitride (GaN) and Aluminum Gallium Arsenide (AlGaAs). These materials are fundamental components in high-brightness LEDs (HB-LEDs), solar cells, and high-frequency electronic devices, driving specialized demand for ultra-high purity grades of TEA.

The market expansion is significantly driven by robust growth in packaging, automotive lightweighting initiatives, and the increasing global deployment of renewable energy technologies and advanced display systems. Key benefits associated with the use of TEA in polymerization include enhanced control over polymer molecular weight distribution and improved catalyst efficiency. However, the market faces constraints related to stringent safety regulations governing the transportation and handling of pyrophoric materials, alongside fluctuating raw material costs, particularly aluminum and ethylene feedstocks, which influence overall production economics and market stability.

The global Triethylaluminum market demonstrates dynamic growth, primarily fueled by sustained demand from the thriving polyolefin sector, especially across emerging economies in the Asia Pacific region. Business trends indicate a strategic emphasis among key producers on enhancing safety logistics, optimizing production yield through process automation, and developing specialized, high-purity grades tailored for the expanding semiconductor and optoelectronics industries. Furthermore, integration across the value chain, focusing on secure, localized supply chains and long-term procurement contracts with large-scale polyolefin manufacturers, remains a pivotal competitive strategy aimed at mitigating supply disruptions and stabilizing pricing volatility in this highly consolidated market. Innovation in containment and delivery systems, such as advanced lecture bottle design and customized tank containers, is also driving technological investment among major market participants.

Regional trends highlight the Asia Pacific (APAC) as the undisputed leader in both consumption and production capacity, driven by massive investments in new polymerization facilities, particularly in China and India, catering to burgeoning domestic construction, automotive, and consumer goods markets. North America and Europe, while representing mature markets, exhibit steady demand, primarily driven by replacement cycles, specialization in high-performance polymer grades, and significant uptake in the high-purity TEA segment essential for advanced electronics manufacturing. Regulatory harmonization regarding hazardous material handling across different jurisdictions remains a complex regional challenge influencing distribution costs and market access strategies, prompting localized production or strategic storage hubs to minimize transportation risks.

Segment trends underscore the dominance of the polymerization grade TEA, which accounts for the vast majority of market volume, intrinsically linked to the macroeconomic performance of commodity plastics. However, the high-purity electronic grade TEA, while smaller in volume, is projected to register the fastest growth rate due to its application in revolutionary technologies like 5G infrastructure, advanced display technologies (OLED/MicroLED), and electric vehicle power electronics (SiC/GaN devices). This differentiation compels manufacturers to invest heavily in advanced purification technologies, such as fractional distillation and meticulous quality control protocols, to meet the stringent parts-per-billion (ppb) impurity specifications required by the semiconductor industry, creating a premium market niche with superior profit margins.

User queries regarding AI's impact on the Triethylaluminum market frequently center on three critical areas: enhancing safety and risk management for handling this pyrophoric substance, optimizing the efficiency and yield of the chemical synthesis process, and leveraging predictive analytics to stabilize the volatile supply chain dynamics. Key concerns revolve around whether AI algorithms can effectively predict equipment failure in highly sensitive, inert-atmosphere production environments and if AI-driven process control can reduce the high costs associated with maintaining ultra-low impurity levels for electronic-grade TEA. The consensus expectation is that AI will primarily serve as a powerful tool for operational intelligence, reducing human exposure to risk, minimizing costly batch variations in polymerization, and speeding up the discovery phase for new organometallic catalyst systems, thereby indirectly influencing TEA demand by accelerating material innovation.

The integration of sophisticated AI and Machine Learning (ML) models is transforming traditional TEA manufacturing and downstream usage. In the production phase, predictive maintenance systems, leveraging sensor data from reactors, piping, and specialized storage tanks, are significantly lowering the risk of catastrophic incidents associated with the material’s extreme reactivity. These systems monitor variables like pressure differentials, temperature gradients, and inert gas consumption in real-time, offering actionable insights that prevent unplanned shutdowns and ensure continuous, safe operation. Furthermore, ML algorithms are being applied to refine the reaction kinetics during TEA synthesis, enabling manufacturers to precisely control parameters like feed rate and temperature profiles, which directly enhance product purity and overall batch consistency, especially critical for the demanding electronic grade.

In the application domain, particularly in polyolefin production, AI models are optimizing the complex Ziegler-Natta polymerization process where TEA functions as a co-catalyst. By analyzing vast datasets derived from production runs, including catalyst loading, monomer concentration, residence time, and desired polymer characteristics (e.g., melt flow index, density), AI can dynamically adjust TEA injection rates to achieve optimal reaction yield and polymer properties, minimizing waste and resource utilization. This optimization capability is crucial for large-scale polyolefin plants operating on thin margins. Consequently, the adoption of AI is not replacing TEA but rather making its deployment safer, more efficient, and more precise, thus subtly increasing market demand reliability by improving the economic viability of processes reliant on this critical reagent.

The Triethylaluminum market's trajectory is determined by a complex interplay of robust drivers centered on industrial expansion and stringent restraints related to material inherent properties and regulatory oversight, creating unique opportunities for specialized growth. The primary driving force is the escalating global consumption of polyolefins, fueled by urbanization, industrialization, and the rising middle class in developing nations, particularly for packaging, infrastructure, and automotive components. Simultaneously, the market is severely restrained by the pyrophoric nature of TEA, which mandates extremely high capital expenditure for safety infrastructure, specialized transportation logistics, and highly trained personnel, translating into higher costs compared to less reactive alternatives. These forces collectively propel market expansion while simultaneously limiting the pool of qualified manufacturers and end-users capable of handling the product safely and efficiently.

Opportunities in the TEA market are predominantly concentrated in the non-polymerization sectors, notably the high-growth electronics and aerospace industries. The increasing adoption of 5G technology, the proliferation of solid-state lighting (HB-LEDs), and the demand for efficient power management devices (GaN-based power supplies) are creating a substantial, rapidly growing demand for ultra-high-purity TEA used in MOCVD processes. This high-value segment allows manufacturers to capture premium pricing, offsetting the substantial operational costs. However, major restraints, beyond inherent material hazards, include volatility in the prices of key raw materials like aluminum and ethylene, which are petrochemical and metal commodities subject to global geopolitical and economic fluctuations. These fluctuations impact the stability of long-term supply contracts and necessitate sophisticated hedging strategies for major producers.

The impact forces influencing the market demonstrate a high degree of integration between technological necessity and environmental pressure. The need for advanced, high-performance polymers in applications like lightweight electric vehicles continues to necessitate TEA as an indispensable catalyst component, maintaining its market relevance despite environmental scrutiny over plastic usage. Conversely, global regulatory trends favoring circular economy principles and sustainable materials may indirectly restrain market growth by encouraging the exploration of alternative, non-organometallic catalyst systems or bio-based polymers that do not rely on TEA synthesis. Thus, market players are forced to balance providing essential chemical solutions for high-growth sectors with continuous innovation in safe handling and responsible chemical stewardship.

The Triethylaluminum market is strategically segmented based on factors such as product purity grade, the dominant application area, and the specific function it performs within chemical processes, reflecting the divergence in demand between high-volume commodity industries and niche high-technology sectors. The categorization by grade—Polymerization Grade and Electronic Grade—is the most critical differentiator, as it dictates the complexity of the manufacturing process, the required supply chain safeguards, and the final selling price. Segmentation by application clearly defines market size allocation, showing the massive volume consumed by polyolefin production versus the high growth potential and specialized requirements originating from the MOCVD process in semiconductor manufacturing. Understanding these distinct segments is essential for manufacturers tailoring their production capabilities and marketing strategies.

The Triethylaluminum value chain is characterized by stringent control and high vertical integration, starting with the acquisition and processing of core raw materials: aluminum metal, ethylene, and hydrogen. Upstream analysis highlights that TEA producers must secure reliable, cost-effective supplies of high-purity aluminum and petrochemical-derived ethylene, requiring significant negotiation power and long-term contracts to manage input cost volatility. The synthesis process, often involving the complex two-step process known as the 'Alfol process' or modified direct synthesis methods, takes place in highly specialized, inert-atmosphere reactors, representing the highest capital investment point in the chain due to the rigorous safety requirements necessary to manage the pyrophoric intermediate and final product.

The downstream segment involves the critical steps of purification, packaging, and logistics. For polymerization grade TEA, purification is standard, and packaging usually involves large stainless steel containers or ISO tanks. However, for electronic-grade TEA, ultra-purification via multi-stage distillation or other advanced techniques is mandatory to reach ppb levels of contamination control. Distribution channels for TEA are inherently specialized and predominantly indirect, relying on certified third-party logistics providers who possess expertise and regulatory approval for handling Class 4.2 Dangerous Goods (spontaneously combustible materials). Direct sales are typically reserved for the largest, most strategic polyolefin producers or specialized electronic chemical distributors who manage final delivery to MOCVD fabs.

Consequently, the distribution network is highly constrained and forms a significant barrier to entry, as few logistics firms worldwide are equipped to handle the volumes of pyrophoric chemicals required by the market. Pricing and profit margins vary significantly; standard polymerization grade TEA operates on higher volume and lower margin, while electronic-grade TEA commands a substantial premium reflecting the specialized purification and highly secure delivery mechanisms involved. The efficient management of inert gas blanketing, specialized transfer equipment, and emergency response capabilities across the entire distribution network are non-negotiable elements defining the operational excellence of successful TEA suppliers.

The primary consumers (end-users/buyers) of Triethylaluminum are major petrochemical companies and polymer manufacturers that operate large-scale polyolefin production facilities utilizing Ziegler-Natta or metallocene catalyst systems. These integrated chemical giants require massive, continuous volumes of polymerization grade TEA to serve as the essential co-catalyst responsible for activating and stabilizing the main catalyst, enabling the efficient manufacture of commodity plastics like HDPE, LLDPE, and PP. Their purchasing decisions are critically driven by volume pricing, security of supply, and the supplier's proven track record of safe and compliant delivery, as any interruption in TEA supply can halt multi-million-dollar polymerization lines.

A second, rapidly growing cohort of potential customers consists of specialized electronics manufacturers, particularly those involved in the fabrication of high-performance semiconductor devices, such as LED lighting companies and advanced power electronics producers. These customers exclusively require the ultra-high-purity Electronic Grade TEA for use as a precursor in the MOCVD process to deposit III-V compound semiconductor layers (e.g., GaN). For these buyers, purity specifications—often down to sub-parts-per-billion impurity levels—and the availability of specialized packaging (like standard lecture bottles or bubblers) that interfaces directly with MOCVD equipment are far more important than volume price, reflecting the high value of the final electronic components.

Finally, a smaller but important customer segment includes specialty chemical producers and pharmaceutical intermediates manufacturers. These entities leverage TEA's powerful alkylating and reducing properties for the synthesis of complex organic molecules and fine chemicals. Demand in this sector is highly fragmented, project-based, and requires specialized technical support from TEA suppliers regarding reaction compatibility and handling protocols. The diverse nature of these end-user industries underscores the multifunctional utility of Triethylaluminum, ranging from supporting mass-market plastics to enabling cutting-edge microelectronics.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 835.5 Million |

| Market Forecast in 2033 | USD 1,356.2 Million |

| Growth Rate | 6.85% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Albemarle Corporation, Lanxess AG (Chemtura), Nouryon (AkzoNobel Specialty Chemicals), BASF SE, Jiangsu Wansheng Chemical Co., Ltd., SAFC Hitech, Gulbrandsen Technologies, Inc., Evonik Industries AG, The Dow Chemical Company, Arkema S.A., PCC Rokita SA, Lg Chem, Sumitomo Chemical, Kemira Oyj, Tri-Is Chemical Co., Ltd., Akishima Chemical Industries Co., Ltd., Mitsubishi Chemical Corporation, Specialty Chemical Products Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The key technology landscape of the Triethylaluminum market centers predominantly on two critical areas: highly efficient synthesis methods and advanced handling and purification technologies tailored for hazardous, high-purity materials. The primary industrial production method for TEA involves the reaction of metallic aluminum with hydrogen and ethylene, a technically demanding process that must be meticulously controlled under anhydrous and anaerobic conditions to prevent undesirable side reactions and ensure high yield. Continuous innovation focuses on improving reactor design, optimizing heat dissipation, and minimizing catalyst waste to lower overall production costs while adhering to extremely tight safety tolerances required by regulatory bodies worldwide, especially concerning fugitive emissions and process containment integrity.

For the rapidly expanding electronic grade segment, purification technology is paramount. Standard industrial purification is insufficient; manufacturers utilize sophisticated multi-stage fractional distillation, often performed under high vacuum, to strip impurities down to parts-per-billion (ppb) or even parts-per-trillion (ppt) levels. Specialized analytical techniques, such as inductively coupled plasma mass spectrometry (ICP-MS) and gas chromatography, are essential for rigorous quality control, validating the ultra-high purity required by the semiconductor industry where trace contaminants can severely compromise device performance. The ongoing technological challenge is to scale these purification processes economically without compromising the purity threshold.

Furthermore, technology related to safe storage, transportation, and delivery systems is crucial. This includes specialized packaging like stainless steel cylinders, proprietary transfer systems, and ISO tank containers designed with features such as double-walled construction, integrated inert gas purging systems (typically nitrogen or argon), and robust pressure relief mechanisms. The adoption of advanced remote monitoring technologies—often integrated with AI systems—for tracking container integrity and pressure during transit represents a significant technological investment, aimed at ensuring zero-leak delivery and compliance with international hazardous material transport standards (e.g., ADR, IMO regulations), which is essential for maintaining market access and minimizing liability risks associated with this reactive chemical.

TEA's primary function is serving as a co-catalyst or activator, specifically in Ziegler-Natta and metallocene polymerization processes. This application is crucial for the large-scale industrial manufacturing of commodity plastics, including high-density polyethylene (HDPE), linear low-density polyethylene (LLDPE), and polypropylene (PP), which dominate market volume consumption.

The Electronic Grade TEA segment is projected for rapid growth due to its indispensable role as a Metal-Organic Chemical Vapor Deposition (MOCVD) precursor. It is vital for synthesizing critical semiconductor materials, such as Gallium Nitride (GaN) and Aluminum Gallium Arsenide (AlGaAs), which are foundational for high-efficiency LEDs, 5G components, and advanced power electronics, demanding ultra-high purity grades.

The main risk stems from TEA's pyrophoric nature, meaning it ignites instantly upon contact with air or moisture, necessitating rigorous safety protocols. Specialized equipment, inert gas blanketing (argon/nitrogen), highly trained personnel, and compliance with strict international hazardous goods regulations (Class 4.2) are mandatory for safe production, storage, and transport, significantly increasing logistical complexity and operational costs for market participants.

Raw material price volatility, particularly concerning aluminum metal and ethylene (derived from petrochemicals), directly impacts TEA production costs and market profitability. Since TEA manufacturing is energy-intensive and reliant on stable feedstock supplies, sharp fluctuations require manufacturers to implement long-term supply agreements and complex financial hedging strategies to maintain stable pricing and mitigate margin erosion.

The Asia Pacific (APAC) region currently holds the largest market share for Triethylaluminum consumption. This dominance is driven by the region's massive and rapidly expanding capacities in polyolefin manufacturing (primarily China and India) and its leading position in global semiconductor and LED production, generating strong demand for both polymerization and electronic grades.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.