ID : MRU_ 443590 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

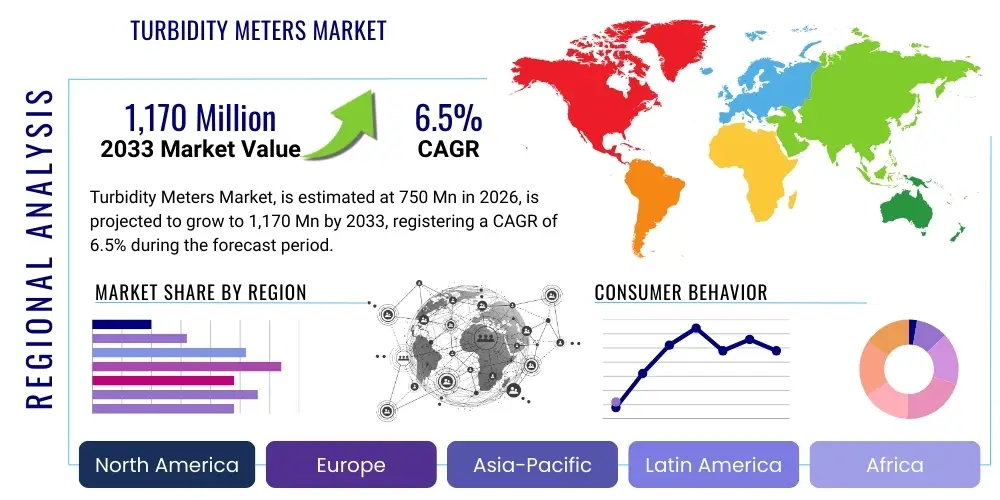

The Turbidity Meters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at $750 Million in 2026 and is projected to reach $1,170 Million by the end of the forecast period in 2033. This consistent expansion is predominantly driven by increasingly stringent global regulatory frameworks governing water quality and the necessity for enhanced process control across various industrial sectors, particularly municipal water treatment and food and beverage manufacturing. The transition towards continuous, real-time monitoring solutions further underpins this substantial market trajectory.

Turbidity meters, also known as turbidimeters or nephelometers, are precision analytical instruments designed to measure the clarity of liquids by quantifying the concentration of suspended particulate matter. The measurement principle typically involves passing a light beam through the liquid sample and measuring the amount of light scattered (nephelometric method, usually at 90 degrees) or the light attenuated (absorbed/scattered). These instruments are indispensable for ensuring compliance with international water quality standards, such as those set by the U.S. Environmental Protection Agency (EPA 180.1) and the International Organization for Standardization (ISO 7027), which mandate low turbidity levels for potable water.

The core product portfolio includes benchtop models for laboratory analysis, portable devices for field testing, and advanced in-line (or process) instruments for continuous monitoring within industrial pipelines and treatment facilities. Major applications span municipal water and wastewater treatment, where turbidity serves as a primary indicator of filtration efficiency and pathogen risk; environmental monitoring of rivers and reservoirs; and quality control in industrial processes, notably brewing, pharmaceuticals, and chemical manufacturing. The primary benefit derived from these meters is immediate insight into process performance, enabling rapid corrective action and minimizing public health risks associated with contaminated water sources.

Market growth is fundamentally driven by a confluence of factors, including population growth escalating the demand for clean water infrastructure, continuous urbanization leading to complex wastewater management challenges, and the global trend toward automated, real-time data collection in process industries. Furthermore, the rising awareness regarding microplastic pollution and sediment transport in ecological systems is creating novel demands for highly sensitive turbidimetry techniques, particularly in environmental research and remediation projects.

The Turbidity Meters Market is poised for robust expansion, characterized by a significant shift from traditional laboratory-based testing towards sophisticated, continuous monitoring systems. Business trends indicate strong investment in sensor technology, favoring compact, robust, and low-maintenance in-line turbidimeters capable of integration into Industrial Internet of Things (IIoT) platforms. Key market competitors are focusing on developing multi-parameter instruments that combine turbidity measurement with pH, dissolved oxygen, or conductivity, offering comprehensive water quality analysis solutions to streamline operational expenditure for end-users. Regulatory compliance remains the most potent market driver, especially in North America and Europe, mandating high-frequency testing and reporting, which naturally elevates the adoption rate of automated solutions.

Regionally, the market exhibits a bifurcated growth pattern. Developed economies in North America and Europe demonstrate mature demand driven by technological upgrades, replacement cycles, and adherence to extremely strict regulatory thresholds for potable water. Conversely, the Asia Pacific (APAC) region is projected to register the fastest growth rate, fueled by massive governmental investments in developing and modernizing water and wastewater treatment infrastructure to support rapid industrialization and burgeoning populations. The operational segment landscape shows that the in-line category is rapidly gaining dominance over portable and benchtop meters due to its capacity for generating continuous, high-resolution data streams critical for modern plant operations and predictive maintenance protocols.

Furthermore, segmentation trends highlight that the Water and Wastewater application segment holds the dominant market share, essential for public health protection and infrastructure reliability. However, high growth rates are anticipated in the Food and Beverage sector, where turbidity measurement is vital for ensuring product clarity, consistency, and compliance in processes like filtration and mixing. The strategic focus of manufacturers is increasingly directed towards enhancing sensor longevity, minimizing calibration frequency, and ensuring data reliability in harsh operating environments, catering directly to the needs of large-scale industrial and municipal treatment plants.

Users frequently inquire about how Artificial Intelligence (AI) and Machine Learning (ML) can enhance the reliability, automation, and predictive capabilities of existing turbidity monitoring systems. Common questions revolve around AI’s role in anomaly detection, predictive failure analysis of sensor components, optimizing chemical dosing based on real-time turbidity fluctuations, and establishing complex correlations between raw water turbidity and upstream environmental factors. The analysis reveals a consensus that AI is transforming passive data collection into active, actionable intelligence. Key themes center on leveraging ML algorithms to filter out noise, compensate for fouling (a major concern for in-line meters), and provide early warnings of treatment process instability long before catastrophic failure occurs. Expectations are high regarding the integration of AI-powered diagnostic tools that can remotely assess sensor health and recommend automated maintenance schedules, thereby drastically reducing human intervention and operational downtime.

The impact of AI fundamentally shifts turbidity measurement from merely providing a data point to generating predictive insights across the water treatment lifecycle. AI models, trained on historical turbidity data alongside variables like flow rate, pH, temperature, and chemical addition rates, are proving instrumental in optimizing coagulant and flocculant dosages. This optimization is crucial for achieving cost savings and improving effluent quality consistency. Moreover, sophisticated ML techniques are being developed to interpret multi-sensor data streams, allowing operators to distinguish genuine turbidity events from measurement artifacts (like air bubbles or localized flow disturbances), enhancing the accuracy and robustness of the entire monitoring system. This transition accelerates the adoption of smart water networks, positioning the turbidimeter as a critical data node rather than a standalone measurement tool.

The future trajectory involves integrating edge computing capabilities directly into the turbidimeter hardware. This allows for immediate, localized processing of data and rapid decision-making without reliance on centralized cloud systems, which is vital for remote or critical infrastructure applications. AI also addresses the challenge of sensor drift and calibration complexity. By constantly analyzing the meter's performance profile against known standards and environmental variables, ML algorithms can virtually recalibrate or flag instruments requiring physical maintenance, ensuring sustained accuracy and reducing the necessity for frequent manual interventions, which often disrupt process flow and incur labor costs.

The Turbidity Meters Market is fundamentally shaped by stringent environmental and public health regulations, acting as the primary driver. Global standards for drinking water quality, particularly the zero-tolerance approach to pathogenic contamination often correlated with high turbidity, force municipalities and industries to invest heavily in reliable monitoring equipment. Restraints include the high initial capital expenditure associated with advanced in-line turbidimeters, especially those featuring self-cleaning mechanisms, and the complexity of maintenance requirements in specific industrial environments where fouling or corrosion is prevalent. Opportunities are abundant in emerging economies undergoing rapid infrastructure development and in the food and beverage industry focusing on brand protection and highly controlled production standards. These forces collectively dictate market adoption rates, pricing strategies, and technological innovation cycles.

Drivers: The most significant driver is the globally increasing scarcity of fresh water, which necessitates recycling and advanced purification processes where real-time turbidity monitoring is crucial. Moreover, governmental emphasis on enforcing discharge permits for industrial effluent ensures that companies must continuously monitor and record compliance data using accredited instruments. The continuous innovation in sensor technology, leading to more robust, accurate, and lower-maintenance instruments (such as those using contactless measurement principles), further stimulates market growth by reducing the total cost of ownership for end-users. The rising adoption of automated systems in manufacturing processes globally also creates a pull demand for integrated process turbidimeters.

Restraints: Despite technological advancements, achieving consistent accuracy in harsh, high-solids environments remains a technical restraint, often requiring frequent manual cleaning or specialized, high-cost accessories. Furthermore, the variability in regulatory standards across different geographical regions can complicate global market penetration and instrument standardization efforts for manufacturers. In budget-constrained regions, there is a tendency to rely on less sophisticated, less reliable laboratory methods instead of investing in continuous in-line monitoring systems, thereby slowing the adoption of premium products.

Opportunities: The expansion of smart cities and the establishment of smart water infrastructure represent major untapped opportunities, where integration of networked turbidity sensors provides foundational data for optimized resource management. The food and beverage sector, encompassing dairy, breweries, and soft drinks, offers substantial growth potential as manufacturers seek to enhance filtration efficiency, reduce product losses, and ensure visual clarity, which is directly tied to consumer perception and product value. Furthermore, the growing focus on environmental monitoring for sediment runoff, algal blooms, and climate change impact assessment opens specialized niches for high-precision, low-power portable and submersible turbidimeters.

The Turbidity Meters Market is comprehensively segmented based on Type, Technology, and Application, reflecting the diverse operational environments and precision requirements across end-user industries. Segmentation by Type reveals a market dominated by the convenience and robustness of in-line process analyzers, essential for uninterrupted monitoring, followed closely by versatile portable meters used for fieldwork and spot-checking, and traditional benchtop models confined largely to certified laboratory environments for high-accuracy standard verification. Understanding these segments is crucial for manufacturers to tailor product specifications regarding robustness, connectivity, and measurement range to specific end-user needs.

From a technological standpoint, the market relies heavily on Nephelometric measurement (90-degree scattered light) due to its high sensitivity at low turbidity levels (critical for drinking water) and its acceptance by key regulatory bodies like the EPA. However, alternative technologies, such as attenuation-based systems or ratio turbidimeters, find relevance in high-solids applications like raw sewage or sludge processing where standard nephelometry might be overwhelmed. Application segmentation clearly highlights the dominance of the Water and Wastewater segment, which is the foundational user base, but strong growth in the Food and Beverage sector, particularly those requiring final product clarity (e.g., beer, juices), is reshaping strategic focus for market players.

The value chain for the Turbidity Meters Market begins with upstream activities involving the sourcing of highly specialized components, primarily high-precision optical sensors, light sources (LEDs or lasers), sophisticated microprocessors, and ruggedized housing materials. Reliability of the measurement is highly dependent on the quality and calibration stability of the sensor components, making supplier relationships critical. Manufacturing involves complex calibration and quality assurance processes to meet stringent regulatory certifications (e.g., CE, UL, ISO compliance). The intellectual property surrounding calibration techniques and automatic cleaning systems represents a significant value addition at the manufacturing stage. Component sourcing is often globally distributed, with sensors frequently originating from specialized providers, and final assembly often occurring in centers focused on analytical instrument production.

Downstream activities involve specialized distribution and high-value service provision. Unlike mass-market electronics, turbidity meters often require technical pre-sales consultation to ensure the correct instrument is selected for the specific application environment (e.g., high pressure, corrosive media, low flow). The distribution channel relies heavily on established global distributors and local authorized representatives who possess the technical expertise to install, calibrate, and service these precision instruments. Direct sales channels are typically reserved for large-scale municipal contracts or high-volume global accounts, ensuring direct manufacturer support and seamless integration into plant control systems (SCADA/DCS).

A critical element of the downstream value chain is the provision of after-sales service, encompassing routine maintenance, traceable calibration using primary standards (like Formazin), and periodic sensor replacement. This service segment often represents a recurring and high-margin revenue stream for both manufacturers and specialized distributors, establishing long-term customer relationships. Effective distribution channels must also efficiently handle the supply of consumables, such as calibration standards and spare parts, ensuring minimal downtime for critical continuous monitoring applications. The value extracted is maximized when the manufacturer provides comprehensive data integration and remote diagnostic capabilities, linking the physical instrument to the end-user’s operational intelligence systems.

Potential customers for turbidity meters span a wide spectrum of industrial, governmental, and environmental entities that prioritize liquid quality and process integrity. The primary end-user/buyer segment is undoubtedly municipal water and wastewater treatment plants, which utilize these instruments at every stage of the treatment process—from raw water intake monitoring and flocculation optimization to final effluent quality verification before discharge or distribution. These entities demand high accuracy, ruggedness, and instruments that comply strictly with national and international health regulations, making them reliable, high-volume purchasers of both in-line and benchtop models.

Secondary high-value customers include the global Food and Beverage industry, where process turbidimetry is vital for quality control. Specific applications include checking the clarity of filtered beverages (beer, wine, sodas), monitoring pasteurization efficiency in dairy, and managing solid suspension in juice production. In the Pharmaceutical and Biotechnology sectors, high-purity water systems require ultra-low-level turbidity monitoring to ensure compliance with pharmacopeia standards, necessitating specialized, high-sensitivity instruments. Chemical processing plants and power generation facilities (for monitoring boiler feed water purity) also represent significant customer segments, where equipment protection and process optimization are paramount concerns.

Beyond industrial and municipal users, environmental agencies, academic research institutions, and hydrological survey organizations constitute a growing customer base, often requiring highly portable, durable, and submersible meters for monitoring natural water bodies, sediment transport studies, and pollution tracking. These buyers typically focus on instruments capable of providing accurate measurements in challenging field conditions and often prioritize instruments with low power consumption and robust data logging capabilities for extended remote deployment periods.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $750 Million |

| Market Forecast in 2033 | $1,170 Million |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Hach Company (Danaher), Thermo Fisher Scientific, Xylem Inc., Emerson Electric Co., Hanna Instruments, LaMotte Company, Tintometer GmbH, Mettler-Toledo International Inc., GF Piping Systems, Swan Analytical Instruments, PCE Instruments, Merck KGaA, Endress+Hauser, WTW (Xylem Brand), Palintest Ltd., Yokogawa Electric Corporation, KROHNE Messtechnik, Horiba Scientific, Insite Instrumentation Group, EUTECH Instruments. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Turbidity Meters Market is centered around optical measurement principles, primarily focusing on scattering and transmission characteristics of light passing through the sample. The dominant technology remains Nephelometry, which measures the scattered light at a 90-degree angle to the incident beam, providing superior sensitivity for detecting fine, dispersed particles typical of low-turbidity applications like finished drinking water. Regulatory bodies heavily endorse nephelometric methods, often specifying the use of a tungsten lamp (EPA 180.1) or an 860 nm infrared LED (ISO 7027) depending on the required color compensation. Modern nephelometers incorporate advanced algorithms to compensate for color interference and employ sophisticated optics to minimize internal stray light, thereby boosting accuracy, particularly in the critical 0 to 1 NTU range.

A crucial technological advancement is the widespread adoption of Ratio Turbidimetry, which enhances accuracy by compensating for various light attenuation factors, including color and large particle interference, by simultaneously measuring scattered light (usually at 90 degrees) and transmitted light. This technique is particularly valuable in samples where particle size distribution is highly variable. Furthermore, the push towards continuous monitoring has driven innovation in sensor design, including the use of non-contact or ultrasonic cleaning mechanisms built directly into the probe. These integrated cleaning systems significantly mitigate sensor fouling, which is a leading cause of measurement drift and high maintenance costs in long-term deployment environments such as wastewater treatment or high-solids industrial slurries.

The latest generation of turbidimeters incorporates digital communication protocols (e.g., Modbus, HART, Profibus) and utilizes smart sensor technology, enabling plug-and-play functionality and remote diagnostics within IIoT frameworks. Fiber optic technology is also gaining traction, particularly for submersible or highly remote applications, allowing the light source and detector electronics to be separated from the sensor head immersed in the sample, enhancing robustness and ease of maintenance. Future technological evolution is expected to focus on miniaturization, utilizing micro-electro-mechanical systems (MEMS) for compact, cost-effective sensors, and developing multi-beam systems that provide enhanced particle size and shape differentiation alongside turbidity measurement, offering more comprehensive water quality profiles.

The regional analysis of the Turbidity Meters Market reveals distinct market maturity, regulatory impetus, and growth potential across major geographical areas. North America and Europe currently dominate the market value due to stringent environmental regulations, extensive historical investments in water infrastructure, and high adoption rates of advanced, in-line monitoring systems. However, the Asia Pacific region is anticipated to exhibit the most accelerated growth over the forecast period, driven by unparalleled infrastructure development and escalating demands for industrial water quality control.

The primary drivers are stringent regulatory requirements demanding continuous, real-time monitoring of treated water quality (e.g., EPA and ISO mandates), the need for automated process control in industrial facilities (like filtration optimization), and the operational efficiency gained by minimizing manual sampling and laboratory testing.

Nephelometric turbidimetry measures the light scattered by particles, typically at a 90-degree angle, making it highly sensitive and ideal for low-turbidity applications like drinking water. Attenuation technology measures the decrease in transmitted light, which is more effective for high-turbidity applications (e.g., sludge or raw sewage) where scattered light signals might be too complex or overloaded.

Sensor fouling, caused by bio-growth or particle deposition, drastically reduces measurement accuracy and increases maintenance costs. Technological solutions include integrated mechanical wiping systems, ultrasonic cleaning devices, and non-contact measurement probes, often coupled with advanced AI algorithms to correct for baseline drift caused by residual fouling.

The Water and Wastewater Treatment segment consistently holds the largest market share. Turbidity measurement is a critical, mandated parameter throughout municipal treatment processes, ensuring the efficacy of coagulation, flocculation, sedimentation, and filtration, directly safeguarding public health.

The Asia Pacific region is projected to be the fastest-growing market due to massive government infrastructure spending on water supply modernization, rapid industrialization, and urgent needs for pollution control and safe drinking water access for its large, growing population. This drives significant new procurement of both process and laboratory instruments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.