ID : MRU_ 443731 | Date : Feb, 2026 | Pages : 248 | Region : Global | Publisher : MRU

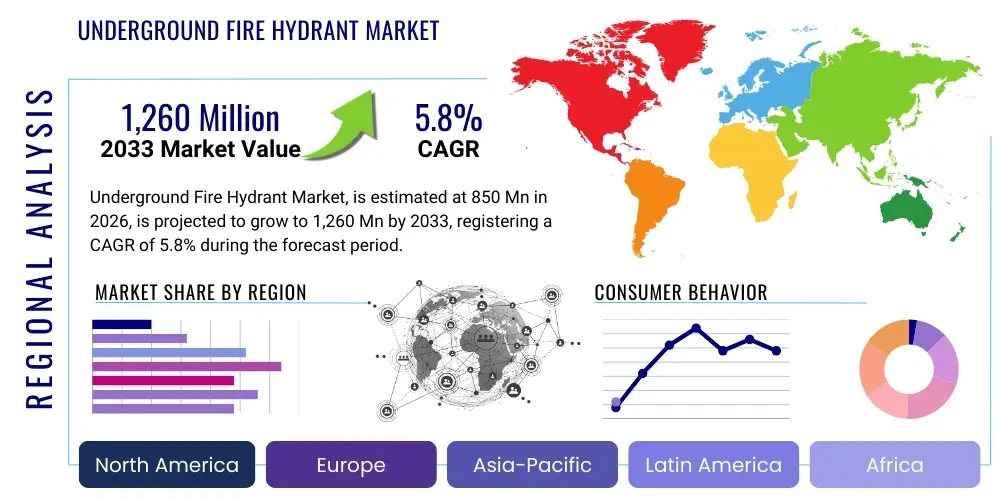

The Underground Fire Hydrant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $850 Million in 2026 and is projected to reach $1,260 Million by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by increasing urbanization rates globally, strict adherence to national and international fire safety codes, and substantial infrastructure investments aimed at upgrading aging water distribution networks, particularly in established municipal areas across North America and Europe, and rapidly expanding metropolitan centers in Asia Pacific.

The Underground Fire Hydrant Market encompasses the manufacturing, distribution, and installation of specialized fixtures designed to provide a readily accessible connection point to a pressurized water supply for firefighting operations. These critical safety components are typically installed below ground level, offering protection from traffic damage, vandalism, and freezing conditions, thereby ensuring operational reliability, especially in densely populated urban environments where aesthetic considerations and minimizing street clutter are prioritized. Unlike their above-ground counterparts, underground hydrants require a surface box or cover to access the valve and outlets, necessitating meticulous engineering to guarantee quick and effective access during emergencies.

The primary products within this market include dry barrel hydrants, predominantly utilized in regions susceptible to freezing temperatures, where the main valve is located below the frost line, and wet barrel hydrants, common in warmer climates, featuring pressurized water immediately available up to the barrel. Major applications span municipal waterworks, large-scale industrial complexes (such as petrochemical plants and manufacturing facilities), commercial developments (including shopping centers and high-rise offices), and critical infrastructure projects. The inherent benefits of underground systems—such as enhanced durability, reduced visual impact, and superior protection against external stressors—drive their continuous adoption, particularly in areas undergoing significant public utility infrastructure modernization.

Key driving factors accelerating market expansion include stringent government mandates related to building safety standards and mandatory fire suppression infrastructure in new constructions, coupled with the need for immediate replacement of decades-old, corroded cast iron hydrants that fail to meet modern flow rate and pressure requirements. Furthermore, population density increases demand for highly reliable public safety equipment, pushing municipalities toward investing in resilient, low-maintenance underground systems that integrate seamlessly with smart city initiatives for remote monitoring and predictive maintenance. This shift towards modernization ensures long-term operational efficiency and adherence to elevated safety protocols across global utility landscapes.

The Underground Fire Hydrant Market is characterized by stable demand driven by non-discretionary public safety requirements and prolonged asset life cycles, exhibiting steady growth across all geographical regions. Current business trends emphasize material innovation, specifically the increasing adoption of ductile iron, stainless steel, and advanced polymer coatings to enhance corrosion resistance and extend product longevity, thereby reducing total cost of ownership for municipal end-users. There is a notable trend towards integrating sensor technology within hydrant components to allow for real-time monitoring of pressure, temperature, and usage, paving the way for predictive maintenance programs that minimize downtime and enhance emergency response capabilities. Strategic mergers and acquisitions among established global players are consolidating market share and facilitating faster entry into high-growth emerging economies where infrastructure development is accelerating.

Regionally, North America and Europe maintain dominance due to legacy infrastructure replacement programs and strict adherence to established safety standards like NFPA guidelines. However, the Asia Pacific region is forecast to demonstrate the highest CAGR, primarily fueled by massive infrastructure investments in China, India, and Southeast Asian nations aimed at supporting unprecedented urban expansion and industrialization. These regions are prioritizing the installation of modern fire suppression systems in new smart city developments, often bypassing traditional above-ground models in favor of resilient underground setups. Latin America and MEA are experiencing growth tied to oil and gas exploration projects and rapid urbanization, demanding robust industrial and municipal-grade fire safety solutions, respectively, though growth rates may be subject to regional political and economic stability.

Segment trends indicate that the dry barrel hydrant type will continue to hold a significant market share, driven by its necessity in cold climates and its superior reliability under fluctuating environmental conditions, while the wet barrel segment sees steady, reliable demand in tropical and subtropical zones. The municipal segment remains the largest end-user, accounting for the vast majority of installed units, but the industrial segment, particularly heavy manufacturing and logistics hubs, is showing faster growth due to the high-pressure, high-volume flow requirements unique to these facilities. Furthermore, the market for ancillary equipment, such as connection fittings, surface boxes, and specialized wrenches, is experiencing growth proportional to new installations and maintenance requirements across all primary geographical segments, underscoring a holistic expansion across the value chain.

User queries regarding AI’s influence on the Underground Fire Hydrant Market predominantly focus on three core areas: predictive maintenance capabilities, optimization of deployment strategy, and integration with broader smart city infrastructure. Users are particularly interested in how Artificial Intelligence can leverage historical data (e.g., pressure fluctuations, water quality data, maintenance records) to anticipate potential failures, such as corrosion breaches or valve malfunctions, before they escalate into critical issues. There is also significant curiosity about utilizing AI algorithms for optimizing the physical placement of new hydrants to ensure optimal coverage and response times based on demographic data, building density, and historical fire incident mapping. Concerns often revolve around data security, the initial investment cost for implementing sensor networks and AI platforms, and the necessary upskilling of municipal utility personnel to manage these complex, integrated systems effectively. Overall, the expectation is that AI will transform reactive maintenance models into proactive, highly efficient asset management programs.

The Underground Fire Hydrant Market is fundamentally shaped by powerful regulatory drivers and significant infrastructure investment cycles, counterbalanced by long product life cycles and initial high installation costs. Drivers (D) include globally tightening fire safety regulations and rapid urbanization, which mandate resilient, high-capacity water access points. Restraints (R) primarily involve the substantial capital outlay required for initial installation, including excavation and complex connection to main water lines, and the long replacement cycles typical of municipal assets, which inherently limit annual market growth for new installations. Opportunities (O) arise from the expanding scope of smart infrastructure projects, especially the integration of IoT sensors for remote monitoring, and the vast potential for infrastructure modernization and replacement in mature markets like North America and Western Europe, where systems are nearing the end of their operational lifespan. These forces combine to create a market characterized by stable, predictable demand governed heavily by public sector procurement processes.

The market faces several critical impact forces that determine profitability and strategic direction. The bargaining power of buyers, predominantly municipal utility districts and government bodies, is high due to standardization, large volume procurement, and rigorous tendering processes that demand competitive pricing and proven reliability. The bargaining power of suppliers, however, is moderate; while raw material suppliers (especially for ductile iron and brass) exert some influence, the standardized nature of components allows manufacturers to mitigate price volatility through diversified sourcing. The threat of new entrants is relatively low due to high regulatory barriers, the necessity for robust certification (e.g., UL, FM approved), and the established, long-standing relationships incumbent companies hold with municipal clients, requiring significant financial and technical resources to overcome. Substitutes, primarily dry risers in tall buildings or mobile water sources, pose a low threat to the core municipal market but may impact specific industrial or commercial applications.

Overall market dynamics are highly influenced by governmental infrastructure spending and macroeconomic health. In periods of economic growth, municipalities allocate substantial budgets towards infrastructure upgrades and safety enhancements, directly benefiting the market. Conversely, economic downturns can lead to deferred maintenance and postponed replacement projects, creating cyclical demand fluctuations. The increasing focus on water conservation and leakage reduction also impacts product development, driving demand for innovative sealing technologies and robust valve designs that minimize water loss—a critical factor for utility buyers seeking enhanced system efficiency and environmental compliance. These intricate dependencies highlight the specialized nature of market penetration, requiring significant technical expertise and regulatory compliance rigor from all participants.

The Underground Fire Hydrant Market is meticulously segmented based on product type, operational mechanism, material composition, and the diverse range of end-user applications, allowing for precise market targeting and strategic analysis. Segmentation based on type differentiates between dry barrel and wet barrel hydrants, reflecting global climate diversity and specific operational requirements. Further segmentation by operation mechanism typically involves various valve types, such as sluice gate or compression valves, which dictate flow control and maintenance ease. The diverse structure of end-users—ranging from government-owned utilities to private industrial complexes—highlights distinct purchasing behaviors and performance specifications required across the market landscape.

The value chain for the Underground Fire Hydrant Market begins with upstream activities centered on raw material procurement, dominated by ferrous metals (iron, steel) and non-ferrous alloys (brass, bronze) for internal mechanisms and fittings. Key raw material suppliers, often global commodity producers, significantly influence initial manufacturing costs. This is followed by core manufacturing, which includes casting, machining, protective coating application (e.g., epoxy), and final assembly, where component quality and adherence to regulatory standards (like AWWA or ISO) are paramount. Efficiency gains in this stage are often achieved through advanced automation and standardized production lines to manage diverse product specifications required by various international markets. Intellectual property surrounding valve design and sealing technologies is a major competitive differentiator at this stage.

Midstream activities involve sophisticated distribution channels necessary to move heavy, specialized equipment efficiently. Distribution is highly segmented: Direct distribution is common for large-scale municipal bids, allowing manufacturers to maintain direct control over pricing, installation specifications, and aftermarket service agreements. Indirect distribution utilizes specialized wholesalers, plumbing supply houses, and construction material distributors who possess established relationships with smaller contractors and regional municipalities. These intermediary partners often provide localized inventory, technical support, and logistical flexibility, which is crucial for timely delivery in infrastructure projects.

The downstream segment focuses on installation and maintenance. Professional engineering firms and certified utility contractors perform the complex civil engineering and connection work required for subterranean installation. Post-installation, the value chain shifts to maintenance, repair, and overhaul (MRO), which constitutes a stable, long-term revenue stream driven by mandatory annual inspection protocols. The introduction of IoT-enabled hydrants is reshaping the downstream, favoring companies that can offer integrated hardware, software, and data analytics services to enhance asset management efficiency. This service layer is becoming an increasingly important source of profitability and customer retention throughout the lengthy operational lifespan of the hydrant.

The primary customers for underground fire hydrants are governmental entities and utility providers responsible for maintaining public safety infrastructure, supplemented by large private organizations with significant fire protection requirements. Municipal water departments and public works agencies represent the core demand base, consistently purchasing high volumes for new installations, expansion of utility lines, and replacement of existing aging stock. These buyers prioritize product longevity, compliance with local fire codes (flow and pressure requirements), ease of maintenance, and competitive pricing realized through lengthy, detailed tender processes and established supplier relationships.

Beyond municipal buyers, the industrial sector constitutes a rapidly growing end-user segment. Companies operating high-risk facilities such as petroleum refineries, chemical processing plants, power generation stations, and massive logistics and warehousing complexes require specialized, often high-pressure, underground fire suppression access points. These customers are driven by extremely strict insurance requirements and internal safety protocols, demanding specialized materials and high-capacity units that often exceed standard municipal specifications, creating opportunities for premium product sales and custom engineering solutions. Reliability and compliance are non-negotiable in these critical operational environments.

Furthermore, commercial infrastructure developers and private property management companies represent key buyers in large-scale residential developments, planned communities, and extensive commercial zones like university campuses or sprawling corporate parks. While often adhering to municipal standards, these private sector buyers are increasingly interested in smart hydrant technology that facilitates remote monitoring and integration with private security systems, optimizing operational expenditure and insurance liability management. The convergence of municipal and private sector demands for advanced, resilient, and efficiently manageable infrastructure is shaping future product development across the market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $850 Million |

| Market Forecast in 2033 | $1,260 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AVK Holding A/S, Hawle Austria Group, Saint-Gobain, Talis Group, TYCO (Johnson Controls), Mueller Water Products, McWane, Inc., Cimberio, Adams Valves, KSB Group, CSA S.r.l., VAG-Armaturen GmbH, Kennedy Valve, Z&J Technologies GmbH, ERHARD GmbH, Clow Valve Company, Cla-Val, Victaulic, Nibco Inc., APOLLO Valves |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Underground Fire Hydrant Market is rapidly evolving from traditional mechanical components to integrated, intelligent systems, although the fundamental hydraulics remain constant. Current advancements are heavily focused on material science and digital integration. Material innovation centers on the use of advanced epoxy coatings and linings, particularly fusion-bonded epoxy (FBE), to provide superior resistance against corrosion and tuberculation, significantly extending the service life of ductile iron bodies and ensuring consistent water quality and flow characteristics over decades. Furthermore, the adoption of specialized elastomers for O-rings and sealing components has improved the leak integrity and durability of valve mechanisms, reducing the frequency and complexity of underground maintenance procedures, a critical factor for utility operators seeking operational efficiency.

The most significant shift is the proliferation of Internet of Things (IoT) technology integration. New generations of underground hydrants are increasingly being equipped with embedded sensors capable of measuring critical parameters such as internal pressure, temperature, water hammer effects, and even unauthorized usage or tampering. These sensors communicate wirelessly via cellular networks or LoRaWAN protocols to a central data management platform. This technological enhancement enables utilities to transition from scheduled, reactive maintenance to proactive, condition-based maintenance strategies, allowing for real-time diagnostics and rapid identification of system anomalies, which is crucial for maintaining regulatory compliance and system reliability, especially in large metropolitan networks where manual inspection is resource-intensive.

Another crucial area is the optimization of design for ease of installation and reduced street disturbance. Manufacturers are developing lighter-weight, modular designs that facilitate easier handling and faster connection to existing water mains, often utilizing specialized flanged or mechanical joint connections that minimize the need for extensive welding or specialized pipe work in the field. Furthermore, advanced hydraulic modeling software is being utilized during the design phase to optimize internal flow paths, minimizing head loss and turbulence, thereby ensuring that the hydrant can deliver maximum rated flow and pressure under emergency conditions, a vital aspect for meeting modern fire suppression standards in high-density areas. This confluence of material, digital, and design optimization defines the competitive edge in the current market environment.

Global demand for underground fire hydrants exhibits distinct regional characteristics influenced by climate, regulatory framework, and infrastructure maturity.

The Underground Fire Hydrant Market is anticipated to grow at a Compound Annual Growth Rate (CAGR) of 5.8% from 2026 through 2033, driven by global urbanization and mandatory fire safety infrastructure upgrades in municipal and industrial sectors.

Dry barrel hydrants are designed for freezing climates; the main valve is situated below the frost line, keeping the barrel dry until use. Wet barrel hydrants are used in warmer regions, where water is consistently pressurized within the barrel up to the outlet nozzles, providing immediate flow access.

Technology, particularly IoT sensors and AI-driven predictive analytics, allows utilities to remotely monitor hydrant pressure, flow, and usage. This transition to condition-based monitoring significantly reduces unexpected failures, optimizes maintenance scheduling, and extends the operational lifespan of the buried assets.

The Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR due to massive infrastructure development, rapid urbanization, and increased regulatory enforcement of modern fire safety standards across countries like China, India, and Southeast Asia.

High-quality underground fire hydrants primarily utilize ductile iron bodies for strength and longevity, often protected by fusion-bonded epoxy (FBE) coatings for superior corrosion resistance, while internal components and fittings frequently use non-ferrous alloys such as brass and bronze for precision and corrosion integrity.

The Underground Fire Hydrant Market is a highly specialized segment within the broader water infrastructure and fire safety industry, characterized by stringent regulatory oversight and long-term investment cycles. The critical function these products serve in public safety means that quality, certification, and reliability override cost in most procurement decisions, especially within the dominant municipal end-user segment. Manufacturers are continually challenged to innovate within the confines of established standards, leading to incremental but crucial advancements in materials science, anti-corrosion techniques, and, most recently, digital integration. The market's future expansion is inextricably linked to global urbanization trends and the financial capacity of governments and utilities to undertake essential infrastructure replacement projects. Key strategic considerations for market participants include navigating complex international certification requirements, securing long-term government contracts, and investing in localized distribution networks capable of supporting extensive maintenance and repair needs.

Furthermore, sustainability and environmental considerations are playing an increasing role in market demand. Utilities are prioritizing hydrants and associated components that minimize water leakage, ensuring compliance with conservation mandates and reducing non-revenue water loss, which can be significant in older systems. This preference is driving demand for precision-engineered valves and advanced sealing mechanisms. Companies that successfully integrate robust sustainability features alongside smart monitoring capabilities will be strategically positioned to capture market share in environmentally conscious markets, particularly in Europe and North America. The competitive landscape remains dominated by a few large, globally established players who leverage deep technical expertise and brand trust built over decades of reliable supply to utility sectors worldwide, making market penetration difficult for smaller, uncertified entities.

The long-term outlook for the Underground Fire Hydrant Market is positive and stable, underpinned by non-negotiable safety requirements. While high initial capital expenditure acts as a continuous restraint, the indispensable nature of fire suppression infrastructure guarantees sustained demand for both new installations in emerging markets and crucial system replacements in mature economies. Strategic market players must focus on achieving operational excellence, leveraging digital solutions for asset intelligence, and maintaining uncompromising quality control to meet the demanding specifications of municipal and industrial buyers, ensuring resilient growth throughout the forecast period and beyond, making this an attractive sector for patient, long-term investors focused on essential utility services.

As smart city initiatives gain momentum globally, the role of the underground fire hydrant is evolving from a purely mechanical device to a connected node in a larger public safety and water management network. This integration is creating new requirements for interoperability and standardized communication protocols. Successful vendors must pivot their offerings to include not just the hardware but also the necessary software platforms and connectivity solutions that enable utilities to harness the data generated by these smart hydrants. This transformation requires expertise in areas traditionally outside of hydraulic engineering, such as cybersecurity and cloud computing, reflecting the increasing sophistication of the infrastructure market. Investment in R&D focusing on low-power, long-range wireless communication for buried assets is a priority for leading firms seeking technological differentiation and long-term competitive advantage in the increasingly digitized utility landscape.

The regulatory environment, particularly in highly regulated markets like the United States (AWWA, UL, FM standards) and Germany (DIN standards), necessitates strict adherence to performance metrics, including minimum flow rates and pressure testing capabilities. Non-compliance is not an option, making the certification process a significant barrier to entry and a foundational element of quality assurance. Furthermore, procurement cycles are often extended, involving detailed technical specifications and multi-year supply contracts. This stable, yet challenging, environment favors companies with proven financial stability, extensive testing capabilities, and the logistical infrastructure to support nationwide or international deployment and ongoing maintenance service contracts. Future growth will rely on how effectively manufacturers can optimize their supply chains to absorb fluctuating raw material costs while continuing to meet these elevated performance expectations under stringent public contracting terms.

Finally, the growing threat of climate change and extreme weather events is subtly influencing product design. In regions facing increased flood risks or prolonged drought, the resilience and longevity of buried infrastructure become even more critical. Manufacturers are responding by developing highly resilient components designed to withstand seismic activity, extreme temperature variations, and prolonged submersion, ensuring that critical fire suppression access remains viable even after natural disasters. This focus on climate resilience underscores the market's fundamental commitment to public safety and its adaptation to evolving global environmental challenges, driving continuous, albeit incremental, product improvement across all segments, ensuring the Underground Fire Hydrant Market remains a vital and dynamic sector of the global infrastructure economy.

The deployment strategy for underground fire hydrants is also being refined through sophisticated Geographic Information Systems (GIS) mapping and hydraulic modeling. Municipalities are increasingly utilizing these tools to assess optimal placement, considering factors such as terrain elevation, pressure zones, building height, and potential fire load risks. This data-driven approach moves away from simple linear spacing and towards risk-based deployment, enhancing the overall efficiency and effectiveness of the fire fighting network. The ability of manufacturers to provide consultative services, integrating their product specifications directly into the client’s GIS and modeling efforts, adds significant value and strengthens client relationships, moving the supplier role beyond mere equipment provision into strategic infrastructure partnership. This service-oriented trend is particularly visible in high-value, complex projects, such as airport expansions or nuclear facility development, where bespoke safety solutions are required.

Furthermore, the maintenance segment of the market is becoming highly competitive, with a focus on ease of repair and standardization of parts. Since underground hydrants are inherently difficult and costly to access, utilities prioritize designs that minimize required excavation for routine maintenance. Manufacturers are developing modular components, such as easily removable operating nuts and nozzle caps, and standardized internal mechanisms that allow field technicians to perform repairs efficiently. This focus on minimizing operational disruption and reducing labor costs associated with maintenance is a major selling point. The aftermarket segment for specialized tools, parts, and accredited training for utility personnel represents a stable and high-margin revenue stream that often complements the initial equipment sale, cementing long-term manufacturer-client bonds and reinforcing the overall market structure.

In terms of specific material selection trends, there is a gradual shift away from traditional brass components towards high-strength, dezincification-resistant alloys and specialized polymers in certain non-load-bearing internal parts. This shift is driven by concerns over lead content in potable water systems, even though fire hydrants are primarily non-potable access points, and the need to mitigate the effects of aggressive water chemistry often found in aging distribution networks. Compliance with strict public health standards, such as those governing components in contact with drinking water, even tangentially, is becoming essential, particularly in North America and Europe, forcing manufacturers to innovate in material composition while maintaining the robust mechanical performance required for emergency use. This alignment of public safety and public health mandates underscores the comprehensive regulatory environment governing market operations.

The competitive landscape is further influenced by intellectual property rights surrounding specialized valve technology, particularly those relating to anti-tamper mechanisms and non-reverse flow check valves, which are crucial for system security and preventing backflow contamination. Companies continuously invest in patenting advanced features that enhance usability, durability, and safety, creating distinct technological niches. For instance, proprietary sealing technologies that guarantee zero leakage over prolonged periods contribute significantly to brand differentiation and justify premium pricing, particularly important when bidding for sophisticated municipal contracts where performance guarantees are critical. The global market, therefore, rewards innovation that solves fundamental utility problems related to water loss and maintenance difficulty.

Finally, global standardization efforts, such as the increasing harmonization of regional standards (e.g., movement towards EN standards in Europe or increased adoption of ISO certifications globally), are gradually facilitating cross-border trade and manufacturing efficiency. While regional variations (like nozzle thread sizes and operating nut designs) persist due to historical infrastructure legacy, the core performance requirements are converging, streamlining production for global manufacturers. This trend allows leading companies to leverage economies of scale and offer consistent quality across diverse geographical markets, reinforcing the dominance of established multinational entities in the global Underground Fire Hydrant Market. The strategic management of these diverse regulatory and technical requirements defines success in this mature yet technologically evolving industry segment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.