ID : MRU_ 442831 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

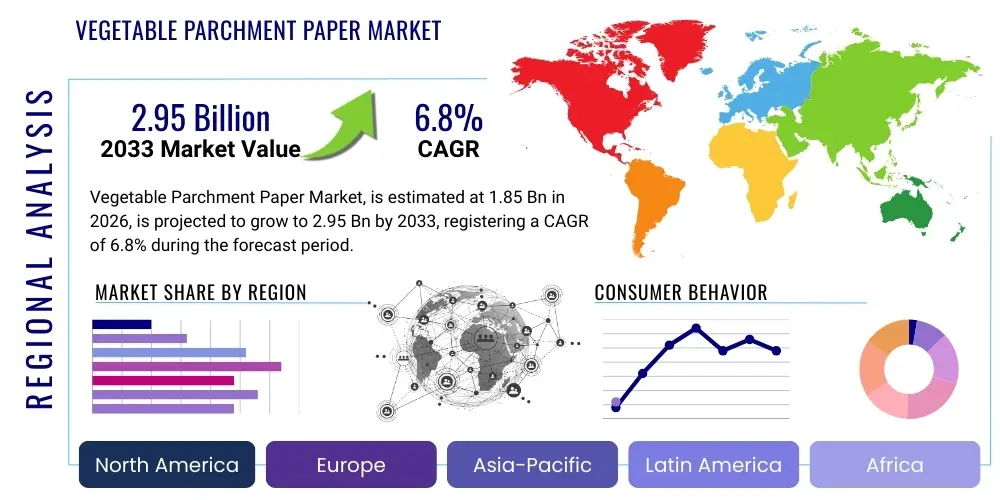

The Vegetable Parchment Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 2.95 Billion by the end of the forecast period in 2033.

The Vegetable Parchment Paper Market encompasses the global production and consumption landscape of chemically treated cellulose-based specialty paper, which is critically utilized across various high-demand sectors due to its distinctive performance attributes. This material is manufactured through the highly controlled parchmentization process, wherein high-purity cellulose sheets are rapidly immersed in a bath of sulfuric acid, followed immediately by extensive washing and drying. This chemical reaction, known as gelatinization, permanently alters the fibrous structure of the paper, resulting in a dense, homogenous, and non-porous matrix that is resistant to grease, moisture, and high temperatures, fundamentally differentiating it from standard papers or simple greaseproof alternatives. The inherent purity and non-leaching characteristics of vegetable parchment paper position it as a premium material essential for direct food contact applications where safety and performance cannot be compromised.

The primary applications driving market volume include its indispensable role in the food preparation industry, particularly as a reliable non-stick liner for commercial baking, roasting, and grilling applications. Additionally, its superior barrier properties make it a favored material for specialized food packaging, especially for high-fat content items such as butter, cheese, and processed meats, where preventing grease penetration and maintaining product integrity during storage and transportation is crucial. Beyond the culinary sector, vegetable parchment paper finds specialized use in medical and pharmaceutical contexts, serving as sterile packaging and sterilization wraps due to its breathability under steam and ability to maintain a sterile barrier. The core benefits promoting widespread adoption include its natural origin, verifiable biodegradability, and the fact that high-quality parchment often requires minimal or no chemical coatings to achieve non-stick functionality, appealing strongly to increasingly eco-conscious consumers and regulatory bodies.

Market expansion is fundamentally driven by the accelerating global transition away from single-use plastic films, fueled by stringent regulatory mandates across North America and Europe. This shift has necessitated the rapid development and deployment of high-performance, sustainable paper-based alternatives, where vegetable parchment paper excels. Furthermore, the robust growth of the global food service sector, including the proliferation of commercial bakeries, ghost kitchens, and meal kit delivery services, significantly increases demand for reliable, high-temperature-tolerant cooking and wrapping materials. Continuous technological innovation focused on improving the wet-strength characteristics and developing fully compostable barrier coatings without sacrificing product safety or performance ensures sustained market dynamism and reinforces the material's competitive position against conventional packaging solutions.

The Vegetable Parchment Paper Market is currently experiencing a dynamic phase of sustained expansion, underscored by critical business trends focused on optimizing sustainable sourcing and improving manufacturing efficiency. Leading market players are prioritizing vertical integration to secure stable access to FSC-certified wood pulp, mitigating supply chain risks associated with raw material volatility. There is a perceptible trend toward modular production systems that allow for rapid switching between standard and specialty grades (such as silicone-coated or highly calendered variants), responding quickly to differentiated end-user demands from institutional clients. Strategic investment is heavily skewed towards modernizing existing production facilities with advanced chemical recovery and wastewater treatment systems, aligning operational practices with global circular economy goals and enhancing the market positioning of manufacturers as responsible corporate entities.

In terms of geographical dynamics, regional trends confirm that while the mature markets of Europe and North America retain high per capita consumption and drive premiumization trends, the most significant future growth opportunity lies within the Asia Pacific (APAC) region. This APAC acceleration is attributable to massive demographic shifts, rising disposable incomes, and the modernization of cold chain and packaged food infrastructure across densely populated markets like China, India, and Southeast Asia. Regulatory environments in these developing economies are starting to catch up with Western standards regarding food safety and environmental impact, creating a powerful market pull for safe, imported, and domestically produced vegetable parchment paper. Conversely, Europe continues to lead in technological adoption, particularly concerning bio-based and non-fluorinated grease-resistant treatments that push the envelope of sustainability without compromising the paper's integral barrier function.

Analysis of segment trends reveals that the Application category of Baking and Cooking Liners maintains the largest market share, driven by widespread domestic and commercial use. However, the fastest Compound Annual Growth Rate is projected within the specialized Food Packaging segment, particularly for customized interleaving papers used in high-speed industrial packaging lines for meat and dairy products. Furthermore, the High-Density Grade parchment, due to its exceptional resistance to tearing and strong barrier function, is increasingly capturing demand within the non-food sectors, including specialized industrial separators and medical sterilization wraps. Overall, the market remains moderately consolidated, with major players competing intensively through product certification, global distribution networks, and the ability to offer highly customized product formats tailored to specific client automation requirements and rigorous international safety standards.

Analysis of common inquiries surrounding the intersection of Artificial Intelligence (AI) and the Vegetable Parchment Paper Market highlights user interest in leveraging cognitive technologies to overcome traditional manufacturing challenges, particularly those related to precision and resource management. Users are critically interested in how AI and machine learning algorithms can be employed to optimize the highly sensitive chemical parameters of the parchmentization bath—specifically, maintaining the ideal sulfuric acid concentration, temperature, and exposure time to achieve consistent gelatinization without compromising fiber integrity. A significant concern revolves around using AI for predictive quality modeling, anticipating material defects such as uneven opacity or poor wet strength before substantial production waste is generated. Furthermore, stakeholders seek solutions for integrating real-time sensor data from the production floor with AI-driven inventory and logistics planning to minimize storage costs for bulky paper rolls and enhance the predictability of high-quality pulp sourcing amidst volatile commodity markets. The overall user expectation is that AI systems will transition the specialized parchment paper manufacturing process from relying heavily on empirical operator knowledge to a highly efficient, data-driven, and resource-optimized industrial operation, directly addressing the pressure points of cost and consistency.

Advanced computational models are also expected to play a crucial role in product innovation, particularly in predicting the performance characteristics of new bio-based coatings designed to enhance barrier properties. By simulating molecular interactions and evaluating the potential success rate of novel non-toxic release agents before pilot production, AI significantly accelerates the R&D cycle for specialty parchment grades. This predictive capability reduces the substantial time and cost associated with traditional empirical testing, allowing manufacturers to quickly bring sustainable, high-performance products to market. For instance, AI can model the long-term degradation rates of fully compostable parchment in diverse environmental conditions, providing verifiable data to back up marketing claims and ensuring compliance with emerging global composting standards, a key competitive advantage.

The application of AI extends into the commercial and risk management aspects of the vegetable parchment industry. Machine learning is being utilized to analyze large datasets encompassing regional sales volumes, seasonal demand fluctuations (e.g., peak baking seasons), competitor pricing strategies, and macroeconomic indicators like GDP growth and commodity futures. This deep-level analysis allows manufacturers to dynamically adjust pricing, optimize production scheduling, and strategically manage inventory deployment across global distribution hubs. Furthermore, AI systems are instrumental in regulatory compliance monitoring, flagging potential deviations in production records that might violate strict food contact material guidelines (like FDA or EU regulations), thereby mitigating substantial legal and reputational risk inherent in this safety-critical sector.

The market trajectory for Vegetable Parchment Paper is strongly guided by powerful macro-environmental drivers and opportunities, yet constrained by inherent material and cost limitations, creating a complex operating environment. Primary drivers include the overwhelming global policy impetus, particularly the phasing out of non-recyclable plastic packaging in direct food contact, which structurally benefits natural, fiber-based solutions like parchment paper. This regulatory tailwind is augmented by the profound shift in consumer behavior, evidenced by increased willingness to pay a premium for products packaged in sustainable, biodegradable, and perceived "cleaner" materials, especially in the premium artisanal and organic food segments. Furthermore, the relentless growth and expansion of the prepared food and meal kit industry across all major geographical regions necessitate large volumes of high-performance, non-stick liners that can withstand both preparation and transportation conditions, acting as a constant demand generator for the industry.

Restraints exerting pressure on market expansion include the substantial capital investment and technical complexity involved in the parchmentization process itself, which relies on handling hazardous chemicals (sulfuric acid), raising both operational costs and environmental compliance requirements, particularly regarding water treatment. Economically, the market remains highly sensitive to the global pricing cycles and supply stability of high-quality, long-fiber wood pulp, the essential feedstock. Competitive restraints manifest in the form of substitute materials, primarily standard greaseproof papers and specialized silicone-treated baking papers, which often offer a lower-cost alternative, although they may lack the superior wet strength and non-leaching characteristics of genuine vegetable parchment. Sustained efforts are required to educate end-users on the distinct performance value proposition that justifies the higher cost base of true parchment paper.

Key opportunities for future market capture revolve around technological breakthroughs in sustainable barrier technologies. Developing bio-based, fully compostable coatings that provide enhanced resistance to oxygen and moisture vapor—approaching the performance of specialized plastic films—would unlock massive potential in modified atmosphere packaging (MAP) for perishable goods. Geographically, scaling up production and distribution infrastructure within fast-growing APAC markets, where local sourcing reduces import costs and lead times, presents a significant strategic pathway. Moreover, diversification into high-specification non-food applications, such as specialized release liners for composite manufacturing or advanced sterilization packaging for reusable medical instruments, offers insulation against cyclical swings in the food sector. The market's impact forces are dominated by intense regulatory scrutiny regarding chemical residue and overall environmental footprint, ensuring that sustainable sourcing and clean manufacturing processes are not just market differentiators but essential prerequisites for global competitiveness and market access in developed economies.

Detailed segmentation of the Vegetable Parchment Paper Market provides a comprehensive framework for understanding the diverse forces driving demand, enabling manufacturers to strategically target specific functional needs across various end-user environments. Segmentation by Grade reflects the technical requirements of the application, with Standard Grade serving general baking and wrapping needs, while High-Density Grade is mandated for applications requiring superior durability, extreme wet strength, and enhanced barrier function, often used in industrial interleaving or medical sterilization packaging. Specialty Coated Grades, frequently treated with non-toxic release agents like silicone, cater specifically to the high-volume commercial baking industry where maximum non-stick performance is critical for automated processes and rapid turnaround times.

The segmentation by Application clearly delineates the primary consumption centers. The Baking and Cooking Liners application, encompassing household and commercial uses, remains the volume leader, benefiting from global culinary trends and health consciousness. However, the Food Packaging segment is strategically vital, capturing growth from specialized areas such as cheese, butter, and processed meat wraps, where the paper’s inherent resistance to grease migration ensures product quality and shelf stability. The rapid emergence of the Medical and Sterilization Wrap segment is noteworthy, driven by the expanding healthcare sector’s need for packaging materials that meet stringent sterilization protocols (e.g., steam autoclaving) while maintaining aseptic conditions until point of use, showcasing the technical versatility of the parchment material.

Segmentation by End-Use Industry helps in profiling the purchasing behavior and quantity requirements of core clients. The Food Service and Commercial Bakeries segment requires reliability and high-throughput capacity, often demanding customized, pre-cut formats. In contrast, Pharmaceutical and Medical buyers prioritize certifications, sterility assurance, and strict batch traceability, making purchasing criteria highly technical and regulatory-driven. Recognizing these distinct needs allows marketing and R&D efforts to be precisely tailored, ensuring that product development—whether focusing on enhanced release characteristics for bakeries or specific sterilization compatibility for hospitals—is aligned with maximum commercial utility and adherence to sector-specific compliance mandates, optimizing resource allocation across the entire competitive landscape.

The Vegetable Parchment Paper value chain is initiated in the upstream segment, dominated by the procurement of certified virgin wood pulp, primarily long-fiber chemical pulp selected for its high cellulose content necessary for effective gelatinization. This raw material phase is critically linked to global sustainable forestry practices; thus, major manufacturers mandate adherence to certifications such as FSC or PEFC, which add complexity and cost but ensure market access in eco-sensitive regions. The primary transformation occurs at the manufacturing stage, involving the highly technical parchmentization process. This stage is characterized by high fixed costs related to specialized machinery and stringent environmental compliance, specifically managing and recycling the sulfuric acid solution and treating industrial effluent to meet strict regulatory discharge limits. Efficient execution of this step is paramount, as the precise control over chemical parameters directly dictates the final paper's quality attributes, including its density, wet strength, and barrier performance.

The midstream involves the conversion process, where the large parent rolls of parchment paper are transferred to converters for sheeting, cutting, die-cutting, or specialized coating application. This conversion step adds substantial value by transforming the base material into the precise formats required by end-users, such as oven-ready baking circles, specific interleaving shapes for meat slicers, or pre-printed branded wraps. Many manufacturers are partially vertically integrated, performing basic slitting and sheeting, but specialized coating (e.g., non-toxic silicone) is often outsourced to expert converters capable of ensuring uniform application at high speeds. Distribution channels are essential for market reach; direct channels manage high-volume sales to institutional clients (e.g., large-scale food processors, hospital purchasing groups) requiring technical specifications and guaranteed batch traceability. These direct relationships often involve customized product development and technical support services.

Conversely, indirect distribution relies on a network of regional wholesalers, food service distributors, and mass-market retailers to deliver smaller volumes to commercial bakeries, small businesses, and household consumers. The rapid expansion of e-commerce has revitalized this indirect channel, enabling niche parchment products (e.g., unique colored parchment, specialty medical grades) to reach targeted customer groups globally with greater efficiency. Maintaining transparency across the entire value chain is a growing imperative; traceability systems, often utilizing digital tracking technologies, are increasingly necessary to comply with international standards like BRC Global Standards for packaging materials and ISO certifications, particularly in segments related to food contact and medical device manufacturing. Successfully navigating the value chain requires strategic partnerships at both the upstream (pulp suppliers) and downstream (specialty converters and global logistics providers) ends to ensure consistent, compliant, and cost-effective delivery of this specialized paper product.

The demographic of potential customers for Vegetable Parchment Paper is fundamentally defined by industries requiring a material that offers high performance in contact with heat, grease, and moisture, while simultaneously adhering to strict hygiene and sustainability standards. The largest consumer base resides within the Food Service and Institutional Catering segment, including major hotel chains, large industrial kitchens, and regional catering companies. These buyers rely on parchment paper for efficient, non-stick cooking, reducing cleanup time and ensuring that baked goods and prepared meals are consistently released intact. Their purchasing criteria are centered on certified food safety, consistency of non-stick properties under varying temperature conditions, and the availability of large, standardized formats for industrial ovens and tray liners.

A high-volume, precision-focused segment consists of Packaged Food Manufacturers, specifically those producing high-fat, high-moisture, or sticky processed goods. This includes large-scale producers of dairy products (cream cheese, butter), frozen baked goods, and confectionery. For these industrial users, vegetable parchment paper serves as a critical interleaving layer, preventing adhesion and allowing for automated sorting and packaging without tearing or transferring grease. These customers demand exceptionally consistent thickness, guaranteed grease resistance, and often require specific non-silicone or specialty coatings that comply with their specific product formulation requirements. The increasing global regulatory focus on minimizing mineral oil migration from packaging also directs these producers toward high-purity parchment solutions.

Furthermore, the Pharmaceutical and Medical Device industry represents a high-value customer niche. Potential buyers include manufacturers of sterilized medical kits, hospitals, and surgical centers utilizing steam or ethylene oxide sterilization methods. They require medical-grade parchment paper to function as sterile wraps, which must allow sterilizing agents to penetrate while creating a microbial barrier after the process is complete. These customers prioritize vendors who can provide rigorous compliance documentation, including full traceability, batch-specific quality assurance reports, and adherence to ISO 11607 standards for terminal sterilization packaging. The dynamic growth of e-commerce meal preparation and ready-to-eat food delivery services also identifies them as emerging potential customers, seeking custom-printed, aesthetically pleasing, and highly functional parchment sheets to enhance brand presentation and maintain food integrity during final mile delivery.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.95 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Delfort Group, Ahlstrom-Munksjö, Pudumjee Paper Products, Nordic Paper, Glatfelter Corporation, Domtar Corporation, KRPA Paper, Schweitzer-Mauduit International (SWM), KapStone Paper and Packaging, Twin Rivers Paper Company, Georgia-Pacific, Mondi Group, Smurfit Kappa, International Paper, Packaging Corporation of America (PCA), WestRock, Tembec Inc., Suzano Papel e Celulose, Resolute Forest Products, BillerudKorsnäs |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology underpinning the Vegetable Parchment Paper Market remains the highly specialized acid bath parchmentization process, a mature yet continuously refined technology. Modern technological advancements in this area are primarily focused on enhancing the sustainability and efficiency of this chemical transformation. Specifically, manufacturers are implementing sophisticated process control systems utilizing digital sensors and closed-loop circulation to precisely manage the strength and temperature of the sulfuric acid bath. This precision minimizes chemical usage, ensures consistent paper quality parameters such as uniform density and optimal gelatinization, and critically, facilitates the recovery and reuse of the acid, substantially reducing environmental discharge and lowering variable operating costs. Furthermore, investment in highly efficient washing and drying sections of the paper machine is essential, as these steps determine the final product’s purity, wet strength, and dimensional stability, which are non-negotiable requirements for high-speed automated processing equipment used by industrial clients.

A significant area of technological focus involves proprietary surface modification and barrier enhancement technologies. While traditional parchment is naturally grease resistant, market demand for greater resistance to moisture vapor and oxygen—crucial for extended food shelf life—is driving innovation in non-toxic coating formulations. Key R&D efforts are centered on replacing fluorochemicals (PFAS/PFOA) and traditional silicone with environmentally benign, bio-based barrier agents, often derived from starches, natural gums, or proprietary biodegradable polymer formulations. The successful application of these sustainable coatings, often done inline during the conversion process, must be flawless, ensuring that the paper maintains its inherent biodegradability and compostability while significantly improving its performance metrics to compete effectively against flexible plastic packaging in specialized applications like frozen food wraps or long-term food storage interleaving.

Beyond material science, digitization and automation are reshaping the manufacturing and distribution landscape. Modern converting facilities leverage high-precision laser cutting, advanced die-cutting techniques, and automated packaging systems capable of handling the inherent stiffness and rigidity of high-density parchment paper, minimizing material waste and maximizing output speed. Additionally, digital printing technologies are being integrated to allow for customized branding, color coding, and serialization of parchment products, crucial for both consumer appeal and strict regulatory traceability in the medical sector. The integration of Industry 4.0 principles, including comprehensive data analytics and IoT devices across the production line, enables real-time monitoring of quality control and equipment health, ensuring that manufacturers meet the rising global demand for certified, high-performance, and consistently reproducible vegetable parchment paper products efficiently and sustainably.

The global distribution and consumption patterns for Vegetable Parchment Paper are diverse, driven by regional economic development levels, regulatory frameworks concerning packaging, and cultural food preparation habits.

Vegetable parchment paper undergoes a specific chemical treatment (parchmentization using sulfuric acid) that gelatinizes the cellulose, rendering the paper highly dense, non-porous, and conferring superior wet strength, heat resistance, and grease impermeability, features absent or significantly weaker in standard greaseproof paper.

Yes, genuine vegetable parchment paper, being made purely of cellulose fibers without added chemical coatings or plastic layers, is inherently biodegradable, compostable, and often sourced from certified sustainable forests (FSC/PEFC), making it a preferred sustainable packaging choice.

The primary driver is stringent global regulatory pressure, particularly in North America and Europe, to reduce the reliance on single-use plastic packaging in food contact applications, compelling food manufacturers and service providers to adopt natural, high-performance paper alternatives like vegetable parchment.

High-Density Grade parchment paper is predominantly utilized in specialized industrial packaging, such as interleaving sheets for highly abrasive materials or high-fat dairy products (butter blocks), and in the medical sector for robust sterilization wraps requiring superior barrier and tear strength.

The reliance on high-quality wood pulp means market manufacturers are highly susceptible to fluctuations in global pulp commodity prices. This volatility impacts production costs and profit margins, often leading companies to secure long-term contracts or invest in vertical integration to stabilize supply chains.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.