ID : MRU_ 444541 | Date : Feb, 2026 | Pages : 242 | Region : Global | Publisher : MRU

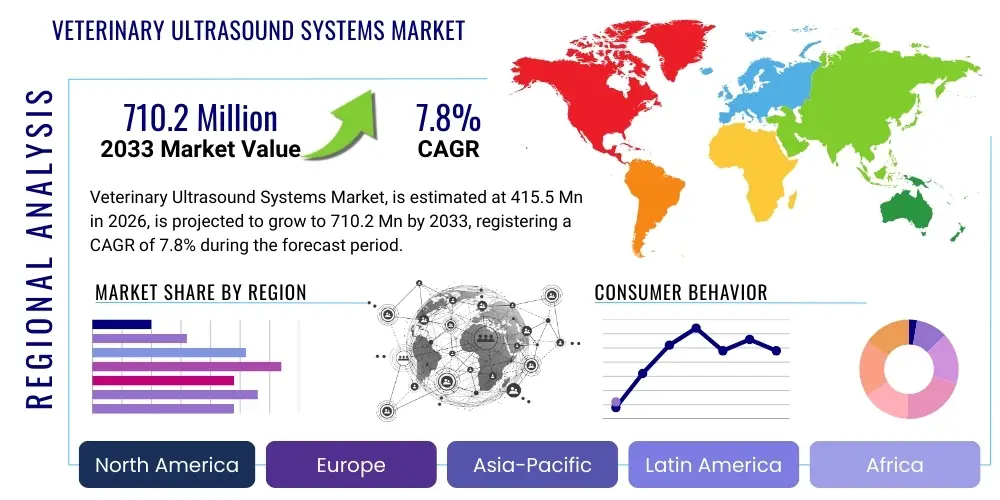

The Veterinary Ultrasound Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 415.5 Million in 2026 and is projected to reach USD 710.2 Million by the end of the forecast period in 2033. This growth trajectory underscores the increasing global investment in animal health diagnostics, driven by a burgeoning companion animal population and a heightened emphasis on advanced veterinary care practices. The consistent expansion of the market reflects both the technological advancements in imaging capabilities and the rising willingness of pet owners and livestock producers to adopt sophisticated diagnostic tools for disease prevention, early detection, and effective treatment strategies. The market's robust expansion is further supported by the expanding applications of ultrasound technology across various animal species and clinical scenarios, ensuring its indispensable role in modern veterinary medicine.

The Veterinary Ultrasound Systems Market encompasses the manufacturing, distribution, and utilization of medical imaging devices designed specifically for diagnostic purposes in animals. These systems employ high-frequency sound waves to generate real-time images of internal body structures, providing veterinarians with crucial insights into the health status of various animal species, ranging from companion animals to livestock and exotic animals. The escalating humanization of pets, coupled with an increased awareness regarding animal welfare and productivity in agricultural settings, has significantly propelled the demand for sophisticated, non-invasive diagnostic tools. This market segment is characterized by continuous innovation aimed at improving image resolution, portability, and ease of use, thereby enhancing diagnostic accuracy and facilitating broader adoption across diverse veterinary settings.

Products within this market range from compact, handheld devices ideal for field diagnostics and mobile veterinary practices to advanced cart-based systems equipped with extensive features for specialized veterinary hospitals and research institutions. Major applications span across cardiology, obstetrics, abdominal imaging, musculoskeletal diagnostics, and even guided interventions, offering a versatile tool for a wide array of clinical conditions. The inherent benefits of veterinary ultrasound systems, such as their non-ionizing radiation nature, real-time imaging capabilities, and ability to differentiate soft tissues effectively, make them a preferred choice over other imaging modalities for numerous diagnostic challenges. These advantages are particularly critical in sensitive animal patients where minimizing discomfort and risk is paramount, establishing ultrasound as a cornerstone diagnostic technology.

Several pivotal factors are driving the substantial growth of the veterinary ultrasound systems market. Foremost among these is the global surge in pet ownership and the increasing financial investment by owners in the health and well-being of their animals, treating them as integral family members. This trend necessitates access to advanced diagnostic services. Furthermore, ongoing technological advancements, including the development of higher-frequency transducers, improved image processing algorithms, and the integration of artificial intelligence, are making ultrasound systems more efficient, accurate, and user-friendly. The rising incidence of zoonotic diseases and chronic conditions in animals also fuels the demand for early and precise diagnostic methods, reinforcing the essential role of ultrasound in maintaining animal health and public safety. These combined forces are creating a fertile ground for sustained market expansion.

The Veterinary Ultrasound Systems Market is currently experiencing dynamic shifts driven by a confluence of evolving business trends, regional growth patterns, and segment-specific innovations. A prominent business trend involves strategic consolidations and mergers & acquisitions among key market players, aimed at expanding product portfolios, enhancing technological capabilities, and increasing market reach. There is also a discernible focus on developing more portable and user-friendly devices, catering to the growing demand from general practitioners and mobile veterinary services who require diagnostic tools that offer both flexibility and high performance. Furthermore, the integration of advanced technologies like artificial intelligence and cloud connectivity into new generation ultrasound systems is a critical trend, promising to revolutionize diagnostic workflows and data management, thereby offering enhanced efficiency and diagnostic precision in veterinary practice.

From a regional perspective, North America and Europe continue to dominate the market, primarily due to high pet adoption rates, well-established veterinary healthcare infrastructures, and significant investments in research and development activities. These regions benefit from a high degree of awareness among veterinarians and pet owners regarding advanced diagnostic modalities. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by increasing disposable incomes, a burgeoning middle class leading to greater pet ownership, and the gradual improvement of veterinary services infrastructure in countries like China and India. Latin America, the Middle East, and Africa are also showing promising growth potential, albeit from a lower base, as awareness grows and access to advanced veterinary care expands, facilitated by government initiatives and international collaborations focused on animal health.

Segmentation trends reveal significant advancements across various product types, animal categories, applications, and end-user segments. In terms of product, there is an increasing adoption of handheld and portable ultrasound systems due to their versatility and cost-effectiveness, particularly in remote or emergency settings. The demand for color Doppler capabilities, which provide detailed information on blood flow, is consistently growing across all system types, reflecting a need for more comprehensive cardiac and vascular diagnostics. Furthermore, the livestock segment is witnessing increased application of ultrasound for reproductive management and general health assessment, driven by economic incentives for herd optimization. Specialized probes for specific animal anatomies and clinical applications are also becoming more prevalent, underscoring a trend towards tailored diagnostic solutions that enhance accuracy and efficiency for diverse veterinary needs.

User inquiries concerning the impact of Artificial Intelligence on the Veterinary Ultrasound Systems Market predominantly revolve around the potential for improved diagnostic accuracy, the automation of routine tasks, and the implications for veterinary workflow efficiency. Common questions include whether AI will make diagnoses more precise, how it can assist veterinarians with complex cases, the ethical considerations of AI in animal healthcare, and the cost-benefit analysis of adopting AI-powered systems. There is a strong interest in understanding how AI can integrate seamlessly with existing ultrasound platforms, the learning curve associated with new AI functionalities, and the extent to which these technologies might reduce the need for highly specialized interpretation, thereby democratizing access to advanced diagnostics. Users are also concerned about data privacy and the security of patient information when AI algorithms are processing sensitive diagnostic images, highlighting a need for robust data governance frameworks.

Based on this analysis, the key themes, concerns, and expectations users have about AI's influence in the veterinary ultrasound domain center on the transformative potential of AI to elevate diagnostic standards. Users anticipate that AI will significantly enhance image interpretation through automated detection of anomalies, measurement calculations, and disease pattern recognition, which could lead to earlier and more accurate diagnoses. The expectation is that AI will act as a powerful assistive tool, reducing diagnostic fatigue and improving inter-observer variability, rather than replacing the veterinarian's critical role. However, concerns regarding the initial investment required for AI-integrated systems, the need for continuous software updates, and the robust validation of AI algorithms in diverse real-world veterinary scenarios remain pertinent. Users also seek clarity on regulatory pathways and standards for AI in veterinary medicine to ensure safe and effective deployment.

The overarching sentiment is one of cautious optimism, with a clear understanding that AI holds immense promise for refining veterinary ultrasound capabilities. Users expect AI to streamline workflows, allowing veterinarians to focus more on patient care and clinical decision-making by automating time-consuming analytical tasks. There is also a strong expectation that AI will facilitate better training for new veterinarians by providing real-time feedback and diagnostic support. The integration of AI is seen as a crucial step towards personalized veterinary medicine, enabling more tailored treatment plans based on objective, AI-assisted diagnostic insights. Ultimately, the market is poised to embrace AI as an evolutionary force, driving advancements in precision, efficiency, and accessibility within veterinary diagnostic imaging, provided that ethical, cost, and integration challenges are effectively addressed by manufacturers and practitioners alike.

The Veterinary Ultrasound Systems Market is significantly shaped by a complex interplay of various Drivers, Restraints, and Opportunities, which collectively constitute the Impact Forces influencing its growth trajectory. Key drivers include the ever-growing global pet population and the increasing trend of pet humanization, leading to greater owner willingness to invest in advanced veterinary care and diagnostic services. Technological advancements in ultrasound imaging, such as improved resolution, portability, and specialized applications, further stimulate market expansion by offering more effective and accessible diagnostic solutions. Additionally, the rising incidence of chronic and zoonotic diseases in animals, coupled with a heightened focus on early disease detection and prevention for both animal welfare and public health, significantly boosts the demand for reliable diagnostic tools like ultrasound. The economic importance of livestock health and reproductive management also contributes to market growth, particularly in agricultural regions where ultrasound is vital for herd health optimization.

Despite robust growth drivers, the market faces several notable restraints. The high initial cost of advanced veterinary ultrasound systems, particularly cart-based units with premium features, can be a significant barrier to adoption for smaller clinics or veterinarians in developing regions with limited budgets. This is often exacerbated by the associated costs of maintenance, software upgrades, and specialized probes. Furthermore, the scarcity of adequately trained and skilled veterinary professionals capable of performing and interpreting complex ultrasound examinations effectively poses a considerable challenge. The steep learning curve for mastering advanced ultrasound techniques means that a lack of expertise can limit the full utilization of these sophisticated devices. Regulatory complexities and varying standards across different geographical regions for device approval and clinical practice can also create hurdles for manufacturers and hinder market penetration, adding layers of cost and time to product deployment.

However, these challenges are counterbalanced by substantial opportunities that promise to drive future market expansion. The emergence of developing economies, particularly in Asia Pacific and Latin America, presents vast untapped markets with increasing disposable incomes and a burgeoning demand for advanced veterinary services. The rapid expansion of tele-veterinary services and mobile veterinary clinics creates a fertile ground for the adoption of portable and handheld ultrasound systems, enabling diagnostics in remote or underserved areas. Moreover, the ongoing integration of artificial intelligence and machine learning into ultrasound technology offers transformative opportunities for enhancing diagnostic accuracy, automating image analysis, and improving workflow efficiency, thereby broadening the capabilities and appeal of these systems. Strategic partnerships between technology developers and veterinary equipment manufacturers, alongside increased research and development efforts in novel transducer technologies and imaging modalities, are also key avenues for future growth and market innovation.

The Veterinary Ultrasound Systems Market is comprehensively segmented across various dimensions including product type, animal type, application, and end-user, providing a granular understanding of market dynamics and catering to the diverse needs within the animal health sector. This segmentation reflects the varied technological capabilities, target species, clinical uses, and operational environments, allowing for a tailored approach to market analysis and strategic planning. Each segment exhibits unique growth patterns and competitive landscapes, driven by specific demands and technological advancements relevant to that particular niche. The careful dissection of the market into these segments allows stakeholders to identify high-potential areas, understand market penetration, and develop specialized product offerings and marketing strategies that resonate with specific customer groups, optimizing resource allocation and maximizing market share in the rapidly evolving veterinary diagnostics space.

The value chain for the Veterinary Ultrasound Systems Market is a complex network involving various stages, from the sourcing of raw materials to the ultimate delivery and support of diagnostic equipment to end-users. This chain begins with upstream activities, focusing on the procurement of specialized components and technologies critical for ultrasound device functionality. Key upstream suppliers include manufacturers of transducers, high-performance processors, imaging software components, display screens, and ergonomic chassis materials. These suppliers play a vital role in dictating the quality, innovation, and cost-efficiency of the final product, often engaging in extensive research and development to create next-generation imaging elements. The intricate nature of these components necessitates specialized manufacturing processes and stringent quality control, forming the foundational layer of the value chain. Strategic partnerships with these upstream providers are crucial for ensuring a steady supply of advanced and reliable materials, directly impacting the manufacturing capabilities and competitive edge of ultrasound system producers.

Following the manufacturing phase, which involves assembly, integration of software, and rigorous testing, the value chain transitions to downstream activities, primarily focused on the distribution and sales of finished veterinary ultrasound systems. This stage involves a sophisticated network of distributors, agents, and direct sales teams responsible for reaching diverse end-users such as veterinary hospitals, specialized clinics, general practitioners, and animal research centers. Effective downstream management is paramount for market penetration and customer satisfaction, encompassing logistics, inventory management, and technical support. The choice of distribution channels—whether direct or indirect—significantly impacts market reach and customer service responsiveness. Post-sales support, including installation, training, maintenance, and repairs, forms a critical part of the downstream value chain, directly influencing customer loyalty and repeat purchases. A robust service infrastructure is essential for ensuring the longevity and optimal performance of these high-value diagnostic instruments in clinical settings.

Distribution channels in the veterinary ultrasound market are typically multifaceted, incorporating both direct and indirect sales approaches to cater to a wide range of customer needs and geographical areas. Direct distribution involves manufacturers selling directly to large veterinary hospital networks, universities, or government institutions, often providing personalized consultation, customized solutions, and extensive training programs. This approach allows for closer customer relationships and direct feedback channels. Conversely, indirect distribution relies on a network of third-party distributors, regional resellers, and veterinary equipment suppliers who facilitate market access to smaller clinics, individual practitioners, and international markets where manufacturers may not have a direct presence. These indirect channels leverage local expertise, established sales networks, and streamlined logistics to effectively distribute products. The selection of the optimal distribution strategy often depends on market maturity, regulatory environment, and the specific target customer segment, with many manufacturers employing a hybrid model to maximize reach and efficiency.

The primary potential customers and end-users of veterinary ultrasound systems are diverse, reflecting the broad spectrum of animal healthcare providers and research institutions. At the forefront are veterinary hospitals, which often serve as comprehensive care centers offering a wide range of diagnostic services. These facilities require advanced, often cart-based ultrasound systems with multiple probe options and sophisticated imaging capabilities to handle complex cases across various animal species, from routine check-ups to specialized surgical planning and critical care monitoring. Their demand is driven by a high patient volume, the need for detailed diagnostics, and the capacity to integrate ultrasound findings with other imaging modalities and laboratory results, thus demanding systems that offer both high performance and extensive features for comprehensive diagnostic workups. The investment capacity of these larger institutions allows for the adoption of premium equipment, driving a significant portion of the market's high-end segment.

Following veterinary hospitals, specialized veterinary clinics, such as cardiology clinics, oncology centers, or reproductive clinics, represent another crucial customer segment. These clinics require ultrasound systems tailored to their specific areas of expertise, emphasizing features like high-frequency transducers for detailed cardiac imaging or specialized probes for reproductive diagnostics in livestock. General veterinary practitioners and small animal clinics constitute a vast segment, often preferring more portable, user-friendly, and cost-effective ultrasound units that can be easily moved between examination rooms or used for mobile veterinary services. These practitioners prioritize systems that offer good image quality for common applications such as abdominal scans and pregnancy checks, providing essential diagnostic capabilities without the need for highly specialized or expensive features. Additionally, animal research laboratories, universities, and zoological parks also represent significant end-users, requiring robust and versatile ultrasound systems for research studies, academic training, and the health management of diverse and sometimes exotic animal populations, often demanding highly specialized imaging modalities for unique anatomical structures or research protocols.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 415.5 Million |

| Market Forecast in 2033 | USD 710.2 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | FUJIFILM SonoSite Inc., Mindray Medical International Limited, Esaote S.p.A., GE Healthcare, Siemens Healthineers AG, Canon Medical Systems Corporation, Hitachi, Ltd., Samsung Medison Co., Ltd., BCF Technology Ltd. (now IMV Imaging), Clarius Mobile Health, Draminski S.A., Shenzhen Kezhong Medical Instrument Co., Ltd., Sonoscape Medical Corp., Kaixin Electric Co., Ltd., CHISON Medical Technologies Co., Ltd., LANDWIND Medical, Echo-Son S.A., Concure Oncology |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Veterinary Ultrasound Systems Market is characterized by continuous innovation aimed at enhancing image clarity, system portability, and diagnostic capabilities, thereby improving overall veterinary care. Advanced imaging modes such as 2D, 3D, and 4D ultrasound are becoming standard, offering comprehensive views of anatomical structures and dynamic processes. Doppler ultrasound, including Color Doppler, Power Doppler, and Pulsed Wave Doppler, has become indispensable for evaluating blood flow dynamics, crucial for cardiology and vascular diagnostics in animals. Harmonic imaging techniques are widely adopted to reduce artifacts and improve image resolution in challenging patients, providing clearer visualization of deep structures and subtle lesions. These core technologies form the backbone of modern veterinary ultrasound, enabling veterinarians to make more accurate and timely diagnoses across a wide array of clinical presentations and animal species.

Beyond fundamental imaging modes, the market is rapidly integrating more sophisticated technologies that elevate diagnostic precision and user experience. Advanced transducer technologies, such as matrix arrays and single crystal transducers, are being developed to offer superior penetration, bandwidth, and sensitivity, allowing for better visualization of both superficial and deep tissues with exceptional detail. Elastography, an emerging technique that measures tissue stiffness, is gaining traction for the non-invasive assessment of liver fibrosis, tumor characterization, and musculoskeletal pathology in animals, providing quantitative data that complements conventional B-mode imaging. Furthermore, the development of miniaturized and wireless transducers has revolutionized portability, enabling veterinarians to perform scans in virtually any location, from remote farm fields to the examination room, significantly expanding access to diagnostic imaging services and improving workflow efficiency for mobile practices. These innovations underscore a clear trend towards more versatile, precise, and accessible ultrasound solutions.

The integration of digital technologies, particularly artificial intelligence (AI) and cloud computing, is profoundly shaping the future of veterinary ultrasound. AI-powered image analysis algorithms are being developed to assist veterinarians in automatically detecting abnormalities, performing measurements, and even generating preliminary diagnostic reports, thereby reducing examination time and enhancing diagnostic consistency. Cloud connectivity facilitates remote access to images, tele-consultations, and seamless sharing of data for collaborative diagnostics and educational purposes, breaking down geographical barriers to specialized care. Advanced post-processing software tools, often embedded within the ultrasound system or available as standalone workstations, offer capabilities for detailed image manipulation, quantification, and reporting. These technological advancements are not only improving diagnostic outcomes but also transforming veterinary workflows, making ultrasound systems more intelligent, connected, and integral to the modern veterinary practice, ultimately contributing to better animal health management and scientific research.

A veterinary ultrasound system is a non-invasive medical imaging device specifically designed for diagnostic purposes in animals. It operates by emitting high-frequency sound waves from a transducer into the animal's body. These sound waves travel through tissues and organs, and when they encounter different densities or interfaces, they bounce back as echoes. The transducer then captures these echoes, and the system's sophisticated software processes them to construct real-time, two-dimensional or even three-dimensional images on a display screen. This technology allows veterinarians to visualize internal anatomical structures, assess organ health, detect abnormalities, evaluate blood flow, and monitor physiological processes in real-time, without using ionizing radiation, making it a safe and versatile diagnostic tool for a wide range of animal species, from small pets to large livestock. Its core principle relies on the reflection of sound waves, similar to how bats navigate, providing detailed insights into soft tissue structures that might not be visible with X-rays. The functionality is further enhanced by various imaging modes, such as B-mode for structural views and Doppler modes for assessing blood flow, enabling comprehensive diagnostic evaluations in clinical settings.

Artificial Intelligence significantly enhances veterinary ultrasound diagnostics by bringing a new level of precision, efficiency, and analytical capability to image interpretation and workflow management. AI algorithms can be trained on vast datasets of ultrasound images to automatically detect subtle abnormalities, measure anatomical structures, and identify disease patterns with remarkable accuracy, often surpassing the human eye in consistency and speed. This capability helps veterinarians reduce diagnostic fatigue, improve inter-observer variability, and expedite the diagnostic process, leading to quicker treatment decisions. AI can also automate tedious tasks such as image annotation, report generation, and even provide real-time guidance during examinations, assisting less experienced practitioners. Furthermore, AI-powered systems can integrate with patient records to offer predictive analytics, helping to forecast disease progression or treatment responses. Cloud-based AI solutions extend these capabilities, enabling remote diagnostics, collaborative case reviews, and continuous learning from a global pool of data, thereby democratizing access to specialized diagnostic insights and driving advancements towards more personalized and precise animal healthcare. The integration of AI transforms ultrasound from merely an imaging tool into an intelligent diagnostic assistant.

Veterinary ultrasound systems have a broad spectrum of primary applications across various animal species and clinical specializations, making them an indispensable tool in modern veterinary medicine. One of the most common applications is in abdominal imaging, where it is used to evaluate organs such as the liver, kidneys, spleen, gastrointestinal tract, and bladder for conditions like tumors, inflammation, stones, or fluid accumulation. Another critical area is cardiology, where ultrasound (echocardiography) allows for detailed assessment of heart structure, function, and blood flow, diagnosing congenital heart defects, valvular diseases, and myocardial conditions. Obstetrics and gynecology applications include pregnancy detection, fetal viability assessment, monitoring fetal development, and evaluating reproductive organ health in both companion and livestock animals, which is vital for breeding management and reproductive success. Furthermore, ultrasound is extensively used in musculoskeletal imaging to diagnose soft tissue injuries such as tendonitis, ligament tears, and muscle strains, particularly in athletic animals like horses. Other notable applications include ophthalmology for eye examinations, guided biopsies for precise tissue sampling, and emergency diagnostics for rapid assessment of trauma or acute conditions, showcasing the versatility and breadth of its utility in enhancing animal health and welfare.

Several key factors are significantly driving the robust growth of the Veterinary Ultrasound Systems Market. Foremost among these is the global surge in pet ownership and the increasing trend of pet humanization, where pets are regarded as integral family members, leading to greater owner willingness to invest in advanced veterinary diagnostic and treatment services. This emotional connection translates directly into increased demand for sophisticated healthcare. Secondly, continuous technological advancements in ultrasound imaging, including improvements in image resolution, portability (e.g., handheld devices), advanced imaging modes (e.g., 3D/4D, Doppler), and specialized probes, are making these systems more effective, versatile, and accessible for diverse clinical needs and settings. Thirdly, the rising incidence of chronic and zoonotic diseases in animals necessitates early and accurate diagnosis, for which ultrasound is a critical tool, ensuring timely intervention and public health protection. Fourthly, there's a growing awareness and preference for non-invasive diagnostic procedures that minimize stress and discomfort for animals, positioning ultrasound as a preferred alternative to more invasive methods. Lastly, the economic importance of livestock health and reproductive management, driven by demand for food security and animal productivity, stimulates the adoption of ultrasound for pregnancy diagnosis, fetal assessment, and herd health monitoring in agricultural sectors globally. These converging factors collectively underpin the sustained expansion and innovation within the veterinary ultrasound market.

The latest technological advancements in veterinary ultrasound systems are dramatically enhancing diagnostic capabilities and user experience, making these devices more powerful and user-friendly. A significant advancement is the development of high-frequency and wide-bandwidth transducers, which provide superior image resolution and penetration, allowing for clearer visualization of both superficial and deep anatomical structures across a wide range of animal sizes. The integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms is a game-changer, enabling automated image analysis, anomaly detection, precise measurements, and even preliminary diagnostic suggestions, which significantly improves diagnostic accuracy and workflow efficiency. Another key innovation is the proliferation of handheld and wireless ultrasound devices, often powered by smartphone or tablet connectivity, offering unparalleled portability and accessibility for field veterinarians, emergency situations, and mobile practices. Furthermore, advanced imaging modes like elastography, which measures tissue stiffness, are gaining traction for non-invasive assessment of conditions like liver fibrosis or tumor characteristics. The incorporation of cloud-based data management and tele-ultrasound capabilities allows for remote image sharing, expert consultations, and streamlined data storage, fostering collaboration and extending diagnostic reach. These advancements collectively underscore a market moving towards smarter, more connected, and highly efficient diagnostic solutions in animal healthcare.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.