ID : MRU_ 443759 | Date : Feb, 2026 | Pages : 248 | Region : Global | Publisher : MRU

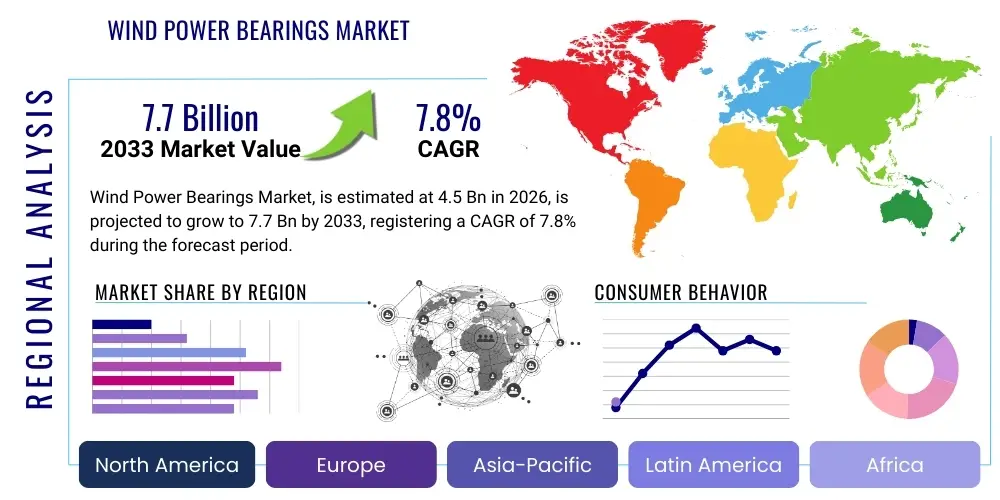

The Wind Power Bearings Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.7 Billion by the end of the forecast period in 2033.

The Wind Power Bearings Market encompasses highly specialized bearing solutions critical for the operational reliability and efficiency of utility-scale wind turbines. These components are essential across four primary applications within the turbine structure: the main shaft (rotor), the gearbox, the pitch system (blade angle control), and the yaw system (nacelle orientation). The stringent operational environment—characterized by variable loads, harsh weather conditions, non-continuous rotation, and extreme temperature fluctuations—necessitates bearings engineered from advanced materials, often incorporating specialized coatings and highly precise internal geometries to maximize service life and minimize maintenance downtime. The increasing global focus on renewable energy adoption, driven by decarbonization mandates and energy security concerns, serves as the foundational driver for sustained market expansion, particularly within offshore wind projects where bearing failure remediation is exceptionally costly and challenging.

The product portfolio in this market includes diverse bearing types such, but not limited to, spherical roller bearings, cylindrical roller bearings, taper roller bearings, and large-diameter slewing rings. Spherical roller bearings are commonly utilized in main shafts and gearboxes due to their high load capacity and ability to accommodate shaft deflection and misalignment, which is crucial under dynamic wind conditions. Tapered roller bearings are often deployed in gearbox high-speed stages and main rotor positions requiring robust axial and radial load management. The primary function of these components is to facilitate smooth, efficient rotation while managing the massive thrust and radial loads generated by the rotor blades capturing wind energy, ensuring minimal energy loss through friction and maximizing the overall power generation yield of the turbine unit.

Major applications of wind power bearings extend beyond utility-scale power generation to include distributed generation systems and repowering projects where older turbines are upgraded with more robust and efficient components. The inherent benefits of high-quality wind bearings—such as extended operational lifespan (often targeting 20 years or more), reduced friction leading to higher power output, and enhanced resistance to White Etching Cracks (WEC) and micropitting—position them as non-negotiable investments for turbine manufacturers (OEMs) and service providers. Key driving factors include technological advancements in material science, the exponential growth in installed wind capacity globally, and the trend toward manufacturing larger, higher-capacity turbines (over 5 MW), which impose significantly greater stress on bearing systems, thereby demanding continuous innovation in load management and lubrication technologies.

The Wind Power Bearings Market is poised for robust expansion, reflecting the rapid global scaling of renewable energy infrastructure, particularly large-scale offshore wind farms. Business trends indicate a strategic shift among leading bearing manufacturers toward forging closer long-term partnerships with major turbine OEMs to co-develop custom bearing solutions tailored for next-generation, high-megawatt platforms. Furthermore, the aftermarket segment—driven by scheduled maintenance, lubrication management, and unexpected component replacement—is witnessing strong growth, spurred by the aging global fleet of installed turbines and the increasing adoption of predictive maintenance technologies that rely on advanced sensing integration within the bearing units. Manufacturers are also heavily investing in automation and digitalization across their production lines to enhance precision engineering capabilities and improve supply chain resilience against geopolitical and logistical disruptions.

Regional trends highlight the Asia Pacific (APAC) region, spearheaded by China and India, as the epicenter of market volume growth, driven by aggressive national renewable energy targets and massive investment in both onshore and newly developing offshore capacity. Europe remains the leader in technological maturity and offshore development, particularly in the North Sea, demanding specialized, high-reliability bearings designed for corrosive, extreme environments. North America, while experiencing steady growth, is focusing heavily on grid modernization and the installation of large turbine sizes, necessitating suppliers capable of rapid scale-up and high-volume delivery. The regulatory environments across these regions, particularly feed-in tariffs and carbon pricing mechanisms, fundamentally influence the long-term project pipeline and, consequently, the demand trajectory for critical components like specialized bearings.

Segment trends reveal a significant proportional increase in demand for slewing bearings and pitch bearings, corresponding directly to the trend of longer, lighter rotor blades and the necessity for precise, dynamic blade angle adjustment to maximize energy capture and mitigate extreme loads. Technologically, the segment covering bearings for turbines larger than 3 MW capacity is experiencing the fastest growth rate, reflecting the industry's drive toward economies of scale in energy generation. In terms of product type, specialized hybrid bearings (incorporating ceramic rolling elements) are gaining traction, especially in critical, high-stress gearbox positions, due to their superior electrical insulation properties and resistance to wear, thereby addressing premature failure modes associated with current flow damage, known as fluting or electrical discharge machining (EDM) damage.

User queries regarding the impact of Artificial Intelligence (AI) on the Wind Power Bearings Market primarily center on three core themes: predictive failure detection, optimization of maintenance schedules, and enhancement of bearing design and manufacturing precision. Users frequently ask how machine learning (ML) models can process vast amounts of sensor data (vibration, temperature, oil particle count) to predict bearing anomalies far earlier than traditional condition monitoring systems, moving maintenance from reactive or time-based schedules to true predictive strategies. Key concerns revolve around the integration costs of smart sensors (IoT/IIoT), data security, and the accuracy of AI algorithms in interpreting the complex failure signatures specific to different bearing types (e.g., distinguishing between WEC, micropitting, and spalling). There is also significant user expectation regarding how generative AI and advanced simulation techniques can expedite the design cycle for ultra-large bearings, reducing time-to-market for components suited for 15+ MW offshore turbines.

AI’s influence is profound, primarily enabling the transition to intelligent asset management within wind farm operations. By leveraging deep learning models trained on historical failure data, operational parameters, and environmental inputs, AI systems can calculate the Remaining Useful Life (RUL) of individual bearings with unprecedented accuracy. This capability allows operators to optimize resource allocation, scheduling necessary bearing replacements during planned downtime rather than incurring catastrophic failures and emergency repairs, which can cost millions per incident on offshore sites. Furthermore, AI algorithms are being applied upstream in the manufacturing process for quality control, utilizing computer vision to detect microscopic defects in raceways or rolling elements that human inspectors might miss, thereby ensuring the highest level of component integrity before installation.

The implementation of AI systems necessitates a paradigm shift in how bearings are viewed—moving from purely mechanical components to intelligent nodes within a connected industrial ecosystem. The market is seeing the emergence of 'smart bearings' embedded with miniaturized sensors for continuous, real-time data streaming. This continuous stream feeds into cloud-based AI platforms, which identify subtle deviations in vibration patterns or temperature spikes indicative of early-stage fatigue or lubricant breakdown. This data-driven approach not only extends bearing life but also provides invaluable feedback to R&D teams, enabling them to refine material specifications and geometric designs based on real-world operational stress factors observed across diverse geographic installations, thereby accelerating innovation and enhancing product robustness.

The Wind Power Bearings Market is governed by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), underpinned by significant impact forces stemming from regulatory mandates and technological evolution. Key drivers include aggressive global governmental targets for renewable energy penetration, leading to unprecedented installation volumes, coupled with the rapid scaling of turbine size (megawatt capacity), which inherently increases demand for larger, highly engineered bearings capable of managing extreme loads. Conversely, major restraints involve the high initial capital expenditure associated with high-precision manufacturing, significant logistical complexities related to transporting and installing massive components for 10+ MW turbines, and the persistent technical challenge of mitigating premature bearing failure modes like White Etching Cracks (WEC) and electrical erosion, particularly in aging fleets and humid environments.

Opportunities in the market primarily reside in the lucrative aftermarket service segment, driven by the need for maintenance and replacement in the rapidly growing global installed base. Technological opportunities abound in the development and commercialization of next-generation materials, such as specialized ceramic hybrids, high-strength steels with proprietary heat treatments, and advanced lubrication systems designed for long service intervals under severe operating conditions. Furthermore, the burgeoning Floating Offshore Wind (FOW) sector presents a unique opportunity, as it requires bearings capable of accommodating additional motion dynamics and persistent wave-induced stresses, pushing the limits of current bearing design standards and demanding customized solutions tailored for floating substructures.

The primary impact forces shaping this market involve intense regulatory pressures to achieve grid parity for wind energy, driving down the Levelized Cost of Energy (LCOE), which in turn places pressure on component manufacturers to extend maintenance intervals and reduce total lifecycle cost. Technological innovation acts as a force multiplier, particularly in sensor integration and digitalization, transforming bearings into proactive health monitoring tools. Economic impact forces, such such as fluctuating raw material prices (steel and nickel) and complex trade tariffs, introduce volatility into the supply chain, while the environmental imperative forces manufacturers to adopt sustainable production practices and design bearings that are fully recyclable at the end of their operational lifespan, balancing durability requirements with ecological responsibility.

The Wind Power Bearings Market is comprehensively segmented based on several critical parameters, including bearing type, application within the turbine, the capacity of the turbine, and the installation location (onshore or offshore). This segmentation is crucial for understanding specific technological demands and market dynamics, as the performance requirements for a main shaft bearing in a 12 MW offshore turbine differ drastically from those of a pitch bearing in a 2 MW onshore unit. The complexity of the segmentation reflects the specialized nature of the components, where each segment requires distinct material science, load calculation expertise, and manufacturing precision to ensure optimal functionality and lifecycle cost efficiency. Detailed analysis of these segments enables manufacturers to focus R&D efforts and tailor their product offerings to address the most rapidly growing and technically demanding sub-markets.

The segmentation by application is particularly important, identifying four distinct usage areas: main shaft bearings, which handle enormous radial and axial loads from the rotor; gearbox bearings, which operate under high speed and extreme precision requirements; and pitch and yaw bearings (typically slewing rings), which control the orientation of the blades and the nacelle, respectively, requiring high static load capacity and resistance to fretting corrosion. The trend toward high-capacity turbines (3 MW and above) is driving the proportional growth of the main shaft and gearbox segments, as these components must scale disproportionately to handle the increased stress and size of the rotors. The continuous evolution in lubrication technologies and surface treatments is often specific to these application segments, reflecting the unique failure modes inherent to each operational environment within the nacelle.

Geographic segmentation is also a primary driver, with the offshore segment exhibiting premium pricing and stringent quality requirements due to the elevated cost of maintenance and remediation in marine environments, favoring high-reliability, long-life components. Conversely, the onshore segment, while larger in volume, often balances performance with cost-competitiveness. This intricate market structure ensures that market participants, from raw material suppliers to final assemblers, possess a deep understanding of the diverse technical specifications and regional regulatory frameworks that define demand across these varied component categories, influencing supply chain strategies and global market penetration efforts.

The value chain for the Wind Power Bearings Market is characterized by highly integrated, specialized processes beginning with the sourcing of high-grade raw materials and culminating in turbine installation and subsequent long-term maintenance. Upstream analysis focuses on the procurement of specialized, ultra-clean steel alloys (e.g., vacuum degassed, electro-slag remelted) and advanced material inputs like ceramics, required for enhanced fatigue life and resistance to subsurface defects. The quality and purity of these materials, often supplied by highly specialized metal processing companies, dictates the ultimate performance and reliability of the finished bearing. This stage also includes the manufacturing of specialized cages, seals, and advanced coatings, representing a critical bottleneck due to the stringent quality control standards required for aerospace-grade materials used in wind applications.

Midstream activities involve core bearing manufacturing processes, including forging, turning, heat treatment (a critical step determining hardness and resistance to WEC), grinding, superfinishing of raceways, and final assembly in highly controlled, clean environments. Major bearing manufacturers (OEMs like SKF and Schaeffler) typically handle these complex, high-precision steps in-house to maintain proprietary specifications and quality standards. Direct distribution channels dominate the initial sales phase, where bearing manufacturers work in close partnership with turbine OEMs (e.g., Vestas, Siemens Gamesa, Goldwind) under long-term supply agreements, ensuring the bearings are integrated into the turbine design from the conceptual stage. This direct engagement guarantees customized solutions and technical support necessary for large-scale production runs.

Downstream analysis centers on the installation, operation, and extensive aftermarket service network. Indirect distribution, leveraging authorized distributors, maintenance service providers (MSPs), and specialized industrial component suppliers, is crucial for the high-margin aftermarket segment, including replacement units, lubrication kits, and condition monitoring equipment. MSPs often stock common replacement bearings and provide technical expertise for complex field service operations. The flow of value is inherently high-risk; defects originating in the upstream material stage can lead to catastrophic failure downstream, emphasizing the necessity of rigorous quality checks and end-to-end traceability throughout the entire supply chain, making strategic alliances between material suppliers, bearing OEMs, and turbine manufacturers a necessity for risk mitigation and competitive advantage.

The potential customer base for the Wind Power Bearings Market is diverse yet concentrated, revolving primarily around turbine manufacturers, independent service providers, and energy asset owners/operators. The most significant segment consists of Original Equipment Manufacturers (OEMs) of wind turbines, such as established global players (e.g., Vestas, Siemens Gamesa Renewable Energy, Nordex, GE Renewable Energy) and major Chinese entities (e.g., Goldwind, Envision Energy). These OEMs constitute the largest volume customers, demanding large batches of specialized, often custom-designed bearings for integration into new turbine assembly lines. Their procurement decisions are driven by cost-effectiveness, guaranteed supply chain stability, technical support for integration, and most critically, proven reliability to meet their 20-year operational guarantees for the turbines.

A rapidly growing customer segment comprises Independent Service Providers (ISPs) and specialized Maintenance Service Providers (MSPs). These entities manage the operations and maintenance (O&M) of existing wind farms, focusing heavily on the aftermarket for replacement bearings, overhaul kits, and upgrades. As the global installed fleet ages—with many turbines now exceeding 10 years of operation—the demand from ISPs for reliable, high-quality replacement parts capable of extending the turbine's life is accelerating. This segment places a premium on immediate availability and optimized logistics, often favoring indirect distribution channels that can quickly supply specialized components to remote wind farm locations worldwide to minimize downtime.

Finally, energy asset owners, including utility companies (e.g., Orsted, NextEra Energy, RWE), specialized yieldcos, and major infrastructure investors, act as indirect but influential customers. While they typically purchase turbines from OEMs, their long-term focus on operational expenditure (OPEX) and maximizing asset uptime significantly influences OEM purchasing specifications. They often stipulate minimum bearing life requirements and mandate the inclusion of advanced condition monitoring systems (CMS) that rely on high-precision bearings. For large-scale repowering projects, these asset owners directly procure bearings and associated services to upgrade their existing fleet with components designed for higher loads and efficiency, making them crucial stakeholders in driving demand for premium and technologically advanced bearing solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.7 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SKF, Schaeffler Group, The Timken Company, NSK Ltd., NTN Corporation, JTEKT Corporation, Rothe Erde, Liebherr, Wafangdian Bearing Group (ZWZ), Luoyang Huigong Bearing, C&U Group, TMX, RBC Bearings, AST Bearings, Kaydon, RKB Group, MinebeaMitsumi, Regal Rexnord. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Wind Power Bearings Market is defined by continuous material science innovation aimed at enhancing longevity, reducing maintenance requirements, and improving resistance to operational stressors unique to wind turbines. A primary technological focus is the development of ultra-clean, high-purity steel alloys, often processed using vacuum degassing and secondary remelting techniques, which significantly reduces non-metallic inclusions—a major contributor to subsurface fatigue and premature bearing failure (spalling). Furthermore, surface engineering technologies, including specialized coatings (e.g., DLC - Diamond-Like Carbon) and proprietary heat treatments (e.g., Bainitic treatments), are crucial for enhancing surface hardness, minimizing friction, and providing robust protection against WEC, especially in humid or electrically charged operating environments, pushing the operational limits for high-stress applications like gearbox intermediate stages.

Another pivotal technological area involves the integration of advanced sensor and monitoring capabilities, leading to the rise of 'smart bearings' and condition monitoring systems (CMS). Bearings are increasingly fitted with embedded or external sensors designed to monitor parameters such as vibration, temperature, speed, and even acoustic emissions in real-time. This technological advancement allows for the precise detection of early-stage defects, such as minor fatigue or lubrication breakdown, enabling operators to move from fixed-schedule maintenance to proactive, condition-based servicing. The data generated by these integrated systems is often fed into AI/ML platforms for RUL prediction, representing a critical convergence of mechanical engineering excellence and digital analytics, substantially reducing lifecycle costs and extending the operational window of highly stressed components, which is paramount for costly offshore installations.

The push toward larger megawatt capacity turbines (8 MW to 15 MW) is necessitating radical shifts in bearing design geometries, demanding massive slewing bearings and main shaft assemblies that are pushing current manufacturing limits. Technology development in this area focuses on optimizing internal clearance and load zone management to ensure equitable load distribution across all rolling elements, minimizing edge stresses and accommodating the increased static and dynamic loads inherent in longer, lighter blades. Furthermore, the adoption of hybrid bearings, which replace traditional steel rolling elements with ceramic balls (e.g., Silicon Nitride), is gaining momentum, particularly in high-speed, electrically susceptible applications like generators and certain gearbox stages, due to ceramics' non-conductive properties, high hardness, and lower density, offering superior performance in terms of speed capability and resistance to electrical damage (fluting), marking a significant leap in component resilience.

The primary technical challenge is managing the extreme, non-uniform loads and accommodating dynamic shaft deflection inherent in multi-megawatt offshore turbines. Designers must ensure high resistance to White Etching Cracks (WEC) and maximum fatigue life (targeting 20+ years) while minimizing the risk of premature failure, necessitating specialized materials and advanced heat treatment processes for main shaft and gearbox components.

The market for pitch and yaw bearings (slewing rings) is rapidly evolving toward larger diameters and higher precision, driven by longer, lighter rotor blades and the need for extremely accurate angular adjustment. Demand is shifting towards segmented or modular slewing rings and integrated gear systems capable of handling increased overturning moments and resisting fretting corrosion under oscillatory motion.

The aftermarket segment is crucial and high-growth, driven by the replacement and maintenance needs of the vast aging global installed turbine fleet. This segment requires immediate availability of robust replacement components, specialized repair services, and advanced condition monitoring technologies to extend the operational life of turbines beyond their initial warranty period, offering higher profit margins than OEM sales.

Hybrid bearings, which feature ceramic rolling elements and steel rings, offer significant advantages, primarily superior electrical insulation, preventing electrical discharge machining (EDM) or fluting damage caused by stray currents. They also provide higher stiffness, reduced friction, lighter weight, and improved resistance to chemical corrosion and high-speed operation, enhancing overall gearbox reliability.

Europe, specifically countries involved in North Sea offshore wind development (UK, Germany, Netherlands), currently leads the demand for high-capacity bearings (above 5 MW). This leadership is driven by technological maturity, aggressive offshore expansion, and the necessity for premium, highly engineered components capable of ensuring multi-decade reliability in challenging marine environments, leading to high investment in main shaft and slewing ring assemblies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.