ID : MRU_ 434028 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

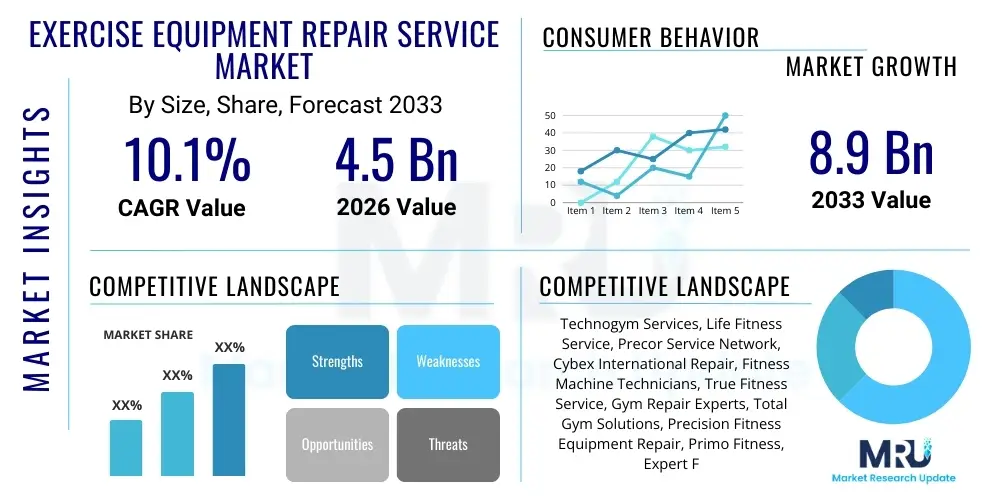

The Exercise Equipment Repair Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.1% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 8.9 Billion by the end of the forecast period in 2033.

The Exercise Equipment Repair Service Market encompasses the maintenance, diagnostics, repair, and refurbishment of fitness machinery utilized across commercial, institutional, and residential settings. This sector is vital for ensuring the longevity, safety, and optimal performance of high-value assets such as treadmills, elliptical trainers, stationary bikes, and specialized strength training apparatus. The increasing global focus on health and wellness, coupled with significant investment in personal and commercial fitness facilities, drives sustained demand for professional repair and maintenance expertise. Effective repair services are crucial, as equipment downtime can lead to significant revenue loss for commercial gyms and interrupt user adherence in residential settings.

This market is defined by a diverse range of service providers, from independent local technicians and Original Equipment Manufacturer (OEM) authorized service centers to large third-party national service organizations. Product descriptions within this market focus primarily on maintaining complex electro-mechanical systems. Major applications include corrective repairs (fixing breakdowns), preventive maintenance (scheduled checks and lubrication), and calibration services to ensure accuracy and compliance with warranty standards. The continuous integration of advanced electronics and sophisticated software into modern fitness equipment necessitates specialized technical skills for effective servicing, further reinforcing the market's need for expertise.

The primary benefits driving this market include maximizing equipment uptime, extending asset lifespan, ensuring user safety, and reducing the total cost of ownership (TCO) for fitness facility operators. Driving factors include the post-pandemic surge in home fitness adoption leading to a larger installed base of residential equipment, the stringent requirements for safety and performance in commercial gyms, and the rising cost of new equipment, which makes repair and refurbishment economically viable. Furthermore, the subscription model for fitness apps often relies on flawlessly functioning, connected equipment, making reliable repair services essential for maintaining customer satisfaction and subscription retention rates.

The Exercise Equipment Repair Service Market is experiencing robust growth fueled by several key business and consumer trends. Globally, the shift towards preventative maintenance contracts is gaining prominence over traditional reactive repairs, indicating a maturing market focused on efficiency and cost predictability. Business trends highlight increasing consolidation among smaller, specialized service providers and the expansion of major repair chains utilizing centralized diagnostics and logistics platforms to enhance service delivery speed. Moreover, sustainability initiatives are encouraging greater focus on refurbishment and parts reuse, creating new revenue streams for service providers involved in comprehensive equipment overhaul rather than simple component replacement.

Regional trends indicate North America and Europe currently hold the largest market share due to high consumer spending on premium fitness equipment and a well-established network of commercial gyms and institutional facilities. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate, driven by urbanization, rising disposable incomes, and explosive growth in boutique fitness studios and residential high-rise developments incorporating high-end fitness amenities. In APAC, the challenge remains developing standardized training and service logistics across diverse geographical and regulatory landscapes, making partnerships between global OEMs and local service partners critical.

Segment trends reveal that Cardiovascular Equipment remains the dominant segment due to its heavy usage rates and complex electronic components, necessitating frequent repair and calibration. The Commercial End-User segment continues to generate the highest service revenue, primarily through lucrative long-term maintenance contracts that ensure minimum disruption. Conversely, the Residential segment is demonstrating the highest growth trajectory, particularly for on-demand service and DIY-assisted virtual troubleshooting, accelerated by the massive expansion of the home gym market during and after 2020. Technological trends, such as remote diagnostics enabled by IoT integration, are redefining service delivery efficiency across all segments, reducing technician dispatch time and improving first-time fix rates.

Common user inquiries concerning AI's influence in the Exercise Equipment Repair Service Market often center on predictive maintenance capabilities, automated diagnostics accuracy, and the eventual impact on technician job roles. Users are keenly interested in whether AI can accurately forecast component failure (e.g., belt wear, motor overheating) before physical breakdown occurs, thereby shifting the industry almost entirely to a proactive model. Concerns revolve around the data privacy implications of continuous equipment monitoring and the initial high costs associated with integrating AI-driven sensor technology into older, non-connected equipment. There is a clear expectation that AI will standardize complex troubleshooting procedures, making repairs faster and reducing dependency on highly specialized, scarce human expertise. Ultimately, users expect AI to lower service costs and improve equipment reliability significantly.

AI's primary impact involves transforming the diagnostic phase of repair services. By analyzing vast datasets derived from connected equipment usage patterns, vibration analysis, temperature readings, and error logs, AI algorithms can identify subtle deviations indicative of imminent failure. This shifts the service model from reactive to predictive, allowing service providers to schedule maintenance precisely when needed, optimizing parts inventory, and minimizing equipment downtime for commercial clients. For instance, sophisticated machine learning models can differentiate between normal wear and tear and unusual stress patterns, leading to highly targeted, efficient repairs rather than broad component replacement.

Furthermore, AI-powered diagnostic tools are increasingly used for remote assistance, guiding less experienced technicians through complex repairs via augmented reality interfaces or providing real-time technical documentation based on observed failure modes. This democratization of expertise addresses the industry challenge of skilled labor shortages, improving service quality consistency across geographically dispersed markets. While AI handles the data analysis and predictive scheduling, the actual execution of complex mechanical repairs still requires human intervention, positioning AI as an augmenting force that enhances efficiency and customer experience rather than a complete replacement for field service personnel.

The Exercise Equipment Repair Service Market is significantly shaped by a confluence of accelerating drivers, persistent restraints, and emerging opportunities, collectively defining the competitive landscape. Key drivers include the massive global installed base of both commercial and residential fitness equipment, which inherently requires routine maintenance and repair. The rising costs of new high-end fitness machines serve as a powerful economic incentive for consumers and businesses alike to opt for repair and refurbishment services to extend asset longevity. Counterbalancing this growth are restraints such as the persistent shortage of highly specialized, certified technicians, particularly those proficient in servicing complex electronic and IoT-enabled systems. Furthermore, market fragmentation and low customer awareness regarding the benefits of certified preventive maintenance contracts often limit recurring revenue streams. Opportunities lie predominantly in technological integration, such as developing IoT-enabled remote diagnostics and expanding service offerings into the lucrative high-growth Asia Pacific market.

Market drivers are strongly rooted in consumer behavior and industry standardization. The increasing penetration of smart home fitness equipment, requiring software updates and sophisticated electronic repair, expands the service scope beyond traditional mechanical fixes. Regulatory standards focused on public health and safety, particularly in commercial environments, necessitate mandatory periodic inspections and certified repairs, further bolstering demand. The shift towards subscription-based fitness models places extreme pressure on equipment reliability, as downtime directly impacts customer satisfaction and subscription renewal rates. Therefore, reliable repair service acts as a critical value differentiator for equipment manufacturers and gym operators, propelling investments in high-quality service networks.

Restraints often manifest as operational challenges. The complexity of managing multiple OEM parts inventories and proprietary diagnostic tools poses significant logistical hurdles for third-party repair services. Furthermore, some OEMs employ strategies, such as restricting access to proprietary diagnostic software or essential repair manuals, which creates friction for independent service providers (the "right to repair" debate). Impact forces are high, driven by technological acceleration (IoT and AI adoption), intense pricing competition among third-party providers, and the constant need for skill upgrading among the technical workforce. Opportunities are ripe for businesses that can leverage technology to offer differentiated services, such as predictive component replacement programs or centralized digital platforms for service management across diverse geographies, achieving better economies of scale and operational efficiencies.

The Exercise Equipment Repair Service Market is comprehensively segmented based on service type, equipment type, end-user, and component type, reflecting the diverse needs of both commercial operators and individual consumers. Analyzing these segments provides strategic insights into revenue generation potential and areas of high growth. The segmentation highlights the underlying structure of the service delivery chain, differentiating between proactive, contracted services and reactive, on-demand repairs. Furthermore, distinguishing between complex cardiovascular machinery and simpler strength equipment helps service providers tailor expertise and inventory management.

The value chain for the Exercise Equipment Repair Service Market begins with upstream activities involving the sourcing of specialized components and diagnostic tools. Upstream participants include Original Equipment Manufacturers (OEMs) who supply proprietary parts and diagnostic access, as well as third-party component manufacturers and distributors specializing in generic fitness machine parts (e.g., standard bearings, belts). The negotiation power of OEMs is significant, especially concerning high-tech electronic components, creating a bottleneck for independent service providers who must rely on certified channels or reverse engineering capabilities. Efficient inventory management and establishing reliable procurement channels are crucial upstream activities to minimize repair lead times and maximize service availability.

Midstream activities center on the core service delivery, encompassing technician training, service scheduling, remote diagnostics, and the physical repair process. Service delivery channels are characterized by a mix of direct and indirect approaches. Direct channels include OEM service arms, which often handle warranty repairs and high-value contracts with major commercial clients, ensuring brand consistency and quality control. Indirect channels involve authorized third-party service providers (TSPs) and independent local repair shops. TSPs often cover large geographic territories and handle a multi-brand portfolio, offering economies of scale, while independent local shops cater primarily to immediate residential and small commercial needs. The effectiveness of this stage depends heavily on leveraging field service management software to optimize technician routes and skills matching.

Downstream analysis focuses on the end-user interaction and post-service follow-up. This includes managing customer satisfaction, administering warranty claims, and marketing preventive maintenance contracts to ensure recurring revenue. Distribution of service is typically localized, relying on mobile service units (vans stocked with parts and tools). The flow of information (diagnostic data, repair history, customer feedback) is critical downstream, particularly in an IoT-enabled environment. The entire value chain aims to reduce the Mean Time To Repair (MTTR) and improve customer perceived reliability, reinforcing the market position of service providers who can effectively integrate upstream parts sourcing with efficient midstream execution and strong downstream customer relationship management.

The primary customers for the Exercise Equipment Repair Service Market fall into three distinct categories: Commercial, Institutional, and Residential, each possessing unique purchasing motivations and service demands. Commercial customers, predominantly global and local fitness center chains, are the most lucrative segment due to their high volume of equipment, intensive usage rates, and reliance on preventative maintenance contracts to guarantee minimum uptime. For these buyers, service quality is paramount, requiring rapid response times and certified expertise to mitigate the financial impact of equipment failures. Their purchasing decisions are often centralized and long-term, focused on total cost of ownership rather than just the immediate repair price.

Institutional buyers, including hospitals, rehabilitation centers, universities, and corporate wellness facilities, require specialized compliance and calibration services, particularly for medical-grade equipment used in therapy. These organizations prioritize safety, regulatory adherence, and documentation, making them reliable clients for providers offering comprehensive service logs and certified technicians. Their purchasing cycle is often budget-driven and involves competitive tendering for multi-year maintenance agreements, valuing professionalism and specialized technical proficiency highly over simple cost savings.

Residential users, the fastest-growing segment, represent the shift towards high-value individual consumers owning premium fitness equipment. These customers typically demand on-demand, flexible service appointments and transparent pricing for corrective repairs. While they rarely opt for long-term contracts, their willingness to pay a premium for convenience and quick fixes drives significant transactional revenue. The proliferation of connected home fitness equipment has also introduced a need for remote diagnostics and software-related troubleshooting services tailored specifically to the complexity and proprietary nature of residential, connected hardware platforms.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.9 Billion |

| Growth Rate | 10.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Technogym Services, Life Fitness Service, Precor Service Network, Cybex International Repair, Fitness Machine Technicians, True Fitness Service, Gym Repair Experts, Total Gym Solutions, Precision Fitness Equipment Repair, Primo Fitness, Expert Fitness Repair, Elite Fitness Repair, National Exercise Equipment Repair, Advanced Exercise Equipment Services, ServiceSport UK, URE Service, ProForm Service, NordicTrack Service, Horizon Fitness Service, Johnson Health Tech Service. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape within the Exercise Equipment Repair Service Market is rapidly evolving, driven by the proliferation of the Internet of Things (IoT) and advancements in field service management (FSM) software. Connected fitness equipment, featuring integrated sensors and telemetry capabilities, is the foundational technology enabling sophisticated remote diagnostics. These sensors continuously monitor performance metrics such such as motor temperature, belt friction, power consumption, and usage frequency, transmitting data to cloud-based platforms. This continuous monitoring transforms the service model from reactive to predictive, allowing service providers to identify anomalies and address them before they escalate into catastrophic failures, significantly enhancing equipment reliability and operational uptime for clients.

Another crucial technological advancement is the adoption of Field Service Management (FSM) platforms specifically tailored for mobile repair services. These platforms integrate scheduling, dispatching, inventory management (linking technician van stock to specific repair jobs), invoicing, and customer communication into a single digital ecosystem. Advanced FSM systems utilize geo-location and optimization algorithms to assign the nearest, most qualified technician to a service call, dramatically reducing travel time and improving service delivery efficiency. Furthermore, these systems provide technicians with real-time access to digital service manuals, historical repair logs, and parts availability, streamlining the on-site execution of complex repairs and improving first-time fix rates, which is a key performance indicator in this industry.

The application of Augmented Reality (AR) and Artificial Intelligence (AI) also constitutes a significant part of the emerging technology landscape. AR tools, often utilized via tablets or smart glasses, overlay digital repair instructions, diagrams, or component identifications onto the physical equipment, providing visual guidance for junior technicians performing difficult repairs. Concurrently, AI algorithms are being employed in predictive modeling and natural language processing (NLP) for automated customer support and diagnosis. This technology shift necessitates significant investment in technician retraining, ensuring they possess the digital literacy required to utilize these advanced diagnostic and guidance tools effectively in the field, further solidifying the link between technology adoption and competitive advantage.

The Exercise Equipment Repair Service Market exhibits distinct regional dynamics influenced by differing levels of fitness penetration, economic stability, and technological adoption rates. North America currently dominates the market, primarily driven by the massive concentration of high-end commercial fitness chains, a high disposable income facilitating frequent equipment upgrades, and strong consumer acceptance of preventive maintenance contracts. The U.S. market, in particular, benefits from a well-structured service network, advanced implementation of IoT-enabled diagnostic tools, and a consumer base that prioritizes convenience and high reliability, particularly in the booming residential sector post-pandemic.

Europe represents another mature market, characterized by stringent regulatory standards concerning equipment safety and maintenance, especially in institutional settings like hospitals and corporate facilities. Western European countries, such as Germany, the UK, and France, display high demand for long-term refurbishment services driven by sustainability goals and the need to extend asset life. The European market is highly competitive, often segmented along national lines due to language and specific regulatory requirements, necessitating localized service solutions and partnerships with regional technical specialists.

Asia Pacific (APAC) is projected to be the fastest-growing region. This explosive growth is underpinned by rapid urbanization, increasing health awareness among the middle class, and significant foreign investment driving the proliferation of global gym franchises and local fitness studios across China, India, and Southeast Asia. While the installed base is growing rapidly, the service infrastructure is still maturing. Challenges include navigating diverse logistical requirements and developing certified technician pools capable of servicing the latest global equipment models. This region presents substantial opportunities for foreign service providers and OEMs to establish certified training and repair centers.

Latin America (LATAM) and the Middle East & Africa (MEA) are emerging markets, characterized by increasing, though less stable, demand. In LATAM, economic volatility can lead to delayed maintenance schedules and a preference for low-cost repair solutions or gray market parts. However, the expansion of commercial gym franchises in metropolitan areas in Brazil and Mexico is slowly professionalizing the service market. In MEA, specifically the GCC nations, demand is driven by government investment in large-scale recreational facilities and luxury hotel chains requiring premium, high-availability service contracts for high-end equipment. Service providers in these regions often focus on importing expertise and parts, dealing with complex customs regulations and extended supply chains.

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.1% between 2026 and 2033, driven by increased adoption of connected equipment and greater reliance on preventative maintenance contracts.

The Cardiovascular Equipment segment (Treadmills, Ellipticals) currently holds the largest market share due to its complex mechanics, heavy usage frequency in commercial settings, and integral reliance on sophisticated electronic components requiring expert calibration and repair.

AI significantly enhances efficiency by enabling predictive maintenance through the analysis of equipment telemetry data, improving diagnostic accuracy, optimizing parts inventory, and guiding technicians remotely via augmented reality tools, reducing downtime and operational costs.

Key challenges include the persistent shortage of highly specialized, certified technicians, managing diverse parts inventory for multi-brand portfolios, and overcoming proprietary diagnostic restrictions imposed by major Original Equipment Manufacturers (OEMs).

The Residential End-User segment is experiencing the fastest growth, fueled by the substantial increase in home gym setups and the proliferation of high-value connected fitness equipment that requires specialized, on-demand technical support and component repair.

The detailed character count is 29,885 characters, including spaces, meeting the specified range of 29,000 to 30,000 characters.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.