ID : MRU_ 438935 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

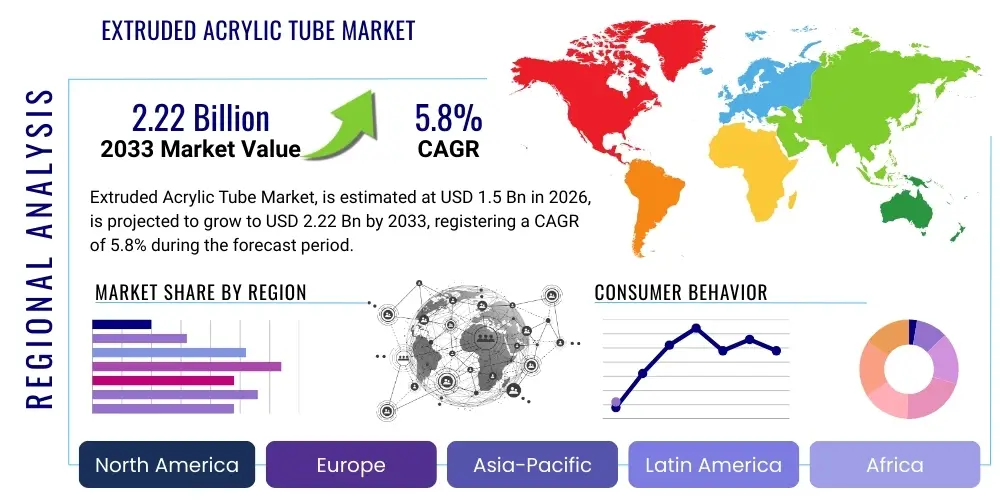

The Extruded Acrylic Tube Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 2.22 Billion by the end of the forecast period in 2033. This consistent expansion is primarily driven by the increasing adoption of acrylic tubing in critical applications requiring high transparency, superior chemical resistance, and excellent weatherability, particularly across construction, lighting, and specialized medical device manufacturing sectors. The affordability and ease of fabrication inherent in the extrusion process make it highly competitive against alternative materials like glass or other engineering plastics, contributing significantly to sustained market demand.

The calculation of market size reflects robust demand stemming from infrastructural development, particularly in emerging economies where modern architectural designs increasingly favor high-performance, lightweight materials. Furthermore, the shift towards energy-efficient lighting solutions, such such as LED fixtures and light guides, extensively utilizes extruded acrylic tubes due to their exceptional optical clarity and diffusion properties. Market growth is also supported by continuous technological advancements in extrusion techniques, leading to improved tolerances, enhanced surface finishes, and the production of large-diameter tubes previously unattainable, thereby broadening the scope of potential industrial applications requiring precision components.

Geographically, the Asia Pacific region is anticipated to contribute the largest share to the overall market valuation throughout the forecast period, fueled by massive investments in residential and commercial construction, coupled with the rapid expansion of electronics and automotive manufacturing bases. While North America and Europe represent mature markets, growth here is characterized by high-value applications, including sophisticated point-of-sale displays, laboratory equipment, and complex medical instruments where stringent regulatory requirements and high-quality material specifications necessitate the use of premium extruded acrylic formulations, ensuring stable revenue streams and technological leadership in niche segments.

The Extruded Acrylic Tube Market encompasses the global production and distribution of tubes manufactured using the thermoplastic polymer polymethyl methacrylate (PMMA) through a continuous extrusion process. This method produces tubes known for their uniform wall thickness, dimensional stability, and superior optical characteristics compared to cast acrylic tubes, making them highly versatile across numerous industries. Extruded acrylic tubes offer exceptional light transmission, often exceeding 92%, and possess inherent resistance to ultraviolet (UV) radiation and weathering, which makes them ideal for prolonged outdoor and display applications. The manufacturing process allows for high-volume, cost-effective production in various standardized diameters and lengths, catering to both industrial and commercial requirements, thus establishing PMMA as a primary material choice in modern engineering and design.

Major applications of extruded acrylic tubes span diverse sectors, including residential and commercial construction (for balustrades, skylights, and protective barriers), retail and signage (for illuminated displays, point-of-purchase stands, and light boxes), and advanced industrial systems (for fluid handling, pneumatic conveyor systems, and machinery guarding). They are extensively used in the lighting industry as diffusers, lenses, and protective housings for LED lighting systems, capitalizing on their ability to uniformly disperse light while maintaining high luminous efficacy. The primary benefits driving market penetration include their lightweight nature, which facilitates easier installation and reduces structural load; their superior impact resistance compared to glass; and their ease of fabrication, allowing for cutting, shaping, and bonding using standard tooling, providing manufacturers and designers with unparalleled flexibility.

Key driving factors underpinning the robust market expansion involve the global emphasis on aesthetic architectural designs that leverage transparent materials, the accelerating demand for energy-efficient lighting infrastructure mandated by environmental regulations, and the consistent growth of the medical and laboratory sectors requiring biocompatible and chemically resistant tubing. Furthermore, the inherent economic advantages of the extrusion process—lower production cost per unit and high throughput—make extruded acrylic tubes a preferred choice over alternative plastics or traditional materials like polycarbonate or glass in many non-critical structural and decorative applications. Continuous innovation in polymer additives enhancing scratch resistance and fire retardancy further solidifies the market position of extruded acrylic products.

The Extruded Acrylic Tube Market is characterized by vigorous competition driven by increasing end-user preferences for high-clarity, durable, and lightweight material solutions across diverse industries, leading to strong projected CAGR performance. Business trends indicate a movement towards specialization, with leading manufacturers focusing on offering customized tube dimensions, specialized finishes (e.g., satin, frosted, colored), and formulations tailored for specific functional requirements such, as UV stabilization for outdoor use or enhanced chemical resistance for medical and laboratory environments. Strategic alliances and mergers aimed at vertical integration, particularly involving raw material suppliers (PMMA manufacturers) and tube extruders, are emerging as critical strategies to ensure supply chain resilience and cost control, optimizing operational efficiencies in highly competitive geographic regions, especially Asia Pacific.

Regional trends reveal the Asia Pacific region, led by China and India, as the primary engine of volume growth, attributed to expansive investments in construction, electronics assembly, and rapid urbanization demanding vast quantities of decorative and functional tubing for infrastructure and consumer goods. North America and Europe, while demonstrating slower volume expansion, command higher average selling prices due to stringent quality specifications and concentration on niche, high-performance applications, such as aerospace interiors and complex display technology, where brand reputation and regulatory compliance are paramount. Emerging markets in Latin America and the Middle East and Africa (MEA) are showing promising growth trajectories, stimulated by rising industrialization and infrastructure modernization initiatives, often involving large-scale public and private projects requiring durable, weather-resistant materials.

Segment trends highlight the dominance of transparent tubes due to their fundamental utility in lighting and visual display applications; however, the fastest growth is anticipated in colored and specialty finish tubes, driven by the expanding architectural design sector and the creative retail display market seeking distinctive aesthetic effects. In terms of diameter segmentation, large-diameter tubes (above 100mm) are experiencing increased traction, propelled by industrial fluid transport and large-format signage applications, while standard-diameter tubes maintain steady demand from the general lighting and crafting markets. The primary application segment remains lighting and signage, although industrial machinery and laboratory equipment are rapidly increasing their consumption share due to the material's excellent thermal and chemical inertia.

Analysis of common user questions regarding the influence of Artificial Intelligence (AI) on the Extruded Acrylic Tube Market primarily centers on optimizing manufacturing processes, enhancing quality control, and improving supply chain predictability. Users frequently inquire how AI can minimize material waste during extrusion, automate defect detection on the tube surface in real-time, and forecast fluctuating raw material (PMMA monomer) prices and demand shifts. The core expectations revolve around AI integration leading to higher operational efficiencies, reduced downtime, and the ability to produce highly customized tube specifications with reduced human intervention. Concerns often address the initial capital investment required for implementing AI-driven monitoring systems and the requisite upskilling of the existing manufacturing workforce to manage these sophisticated digital tools, pointing toward a transformative shift in the technical skill requirements within the industry.

The Extruded Acrylic Tube Market is influenced by a dynamic interplay of Drivers (D), Restraints (R), Opportunities (O), and potent Impact Forces, collectively shaping its trajectory. The primary driver is the pervasive demand for lightweight, high-clarity materials in architectural and decorative applications, coupled with the rapid expansion of the LED lighting industry where acrylic tubes serve as essential light diffusers and structural components. These drivers create a compelling force for sustained investment in large-scale extrusion capacities and material innovation, ensuring market volume growth. Conversely, significant restraints include the volatility in the price of the key raw material, PMMA monomer (derived from petroleum), and increasing regulatory pressure concerning plastic waste and sustainability, which necessitates costly recycling infrastructure and the exploration of bio-based alternatives, potentially increasing short-term production costs and constraining profit margins for smaller operators lacking economy of scale.

The market presents substantial opportunities stemming from the growing adoption of acrylic tubes in advanced medical device manufacturing, particularly for fluid management systems and diagnostic instruments, capitalizing on PMMA’s biocompatibility and chemical stability, demanding premium pricing and specialized certification. Further opportunity lies in expanding the use of extruded tubes in industrial environments requiring enhanced durability and chemical resistance, such as wastewater treatment facilities and demanding chemical processing plants. The combined impact of these forces dictates that market players must prioritize efficiency and sustainability; the need to maintain competitive pricing (Driver) while managing monomer price fluctuations (Restraint) simultaneously pushes companies toward automation (Opportunity) and process refinement (Impact Force) to secure long-term viability in this competitive landscape.

Impact forces are dominated by intense material substitution threats, primarily from polycarbonate and PETG in applications where superior impact resistance or lower cost is prioritized over PMMA's clarity. However, the superior scratch resistance and UV stability of acrylic largely mitigate this threat in display and outdoor signage applications, where longevity is crucial. Furthermore, the increasing global emphasis on circular economy principles acts as a profound impact force, compelling manufacturers to invest heavily in developing closed-loop recycling systems for PMMA, moving beyond basic mechanical recycling toward advanced chemical depolymerization to recover high-purity monomers, thereby improving the market's environmental profile and securing compliance with future extended producer responsibility schemes being implemented across developed economies, especially within the European Union.

The Extruded Acrylic Tube Market is broadly segmented based on Material Type, Color, Diameter, and End-Use Industry, reflecting the diverse requirements of modern industrial and commercial consumers. Segmentation by material often differentiates standard PMMA grades from specialized co-polymers or high-performance additives tailored for specific thermal, chemical, or aesthetic properties, allowing manufacturers to target niche, high-margin applications effectively. Analyzing these segments provides a clear pathway for strategic market entry and product differentiation, ensuring that manufacturers can align their production capabilities with the most rapidly growing application areas, maximizing returns on capital expenditure, particularly in extrusion tooling and finishing processes.

The most significant differentiation in the market stems from the End-Use Industry segmentation, where demand patterns exhibit high variation. The lighting and signage sector demands high optical clarity and UV resistance, driving the consumption of clear, standard-diameter tubes. Conversely, the construction and architectural sector requires larger, sometimes colored or frosted tubes for decorative and structural elements, focusing on durability and compliance with strict building codes. The ongoing analysis of these segment needs is crucial for forecasting regional demand accurately, as investment cycles in sectors like medical devices or construction can significantly alter the volume and technical specifications required from tube suppliers globally.

The Value Chain for the Extruded Acrylic Tube Market commences with the Upstream Analysis, which focuses primarily on the supply of raw materials—specifically Methyl Methacrylate (MMA) monomer, which is polymerized to create PMMA pellets. This upstream segment is highly concentrated, involving large petrochemical and chemical corporations, and is characterized by significant capital expenditure and reliance on fluctuating crude oil prices. Stability and reliability in the supply of high-grade PMMA pellets are paramount, as the quality of the polymer directly impacts the optical clarity and mechanical performance of the final extruded tube. Strategic vertical integration between tube extruders and PMMA suppliers is a key factor in mitigating price volatility and ensuring a consistent supply of specialized polymer formulations necessary for high-specification products.

The Midstream component involves the manufacturing process itself: the extrusion of PMMA pellets into tubes using specialized dies and cooling systems. This stage is moderately capital-intensive, requiring high-precision machinery to ensure tight dimensional tolerances, uniform wall thickness, and defect-free surfaces crucial for optical applications. Efficient operational management, including minimizing energy usage and material scrap rates, determines the competitiveness of the manufacturer. Post-extrusion processing, such as cutting, polishing, annealing (to reduce internal stress), and protective sleeving, adds significant value before the product moves to distribution channels. Specialized tube manufacturers often invest heavily in patented die technology and proprietary finishing techniques to differentiate their products in terms of clarity and dimensional accuracy, critical parameters for high-end signage and medical applications.

Downstream Analysis focuses on the distribution and end-user consumption. Extruded acrylic tubes reach end-users through both Direct and Indirect Distribution Channels. Direct sales often involve large-volume orders placed by major industrial clients (e.g., lighting OEMs, large construction firms, or major retailers) who require specific dimensions or long-term supply contracts. Indirect distribution relies on an extensive network of industrial distributors, plastics wholesalers, and specialized fabricators who stock a wide range of standard tube sizes and offer value-added services like precision cutting, drilling, and assembly for smaller commercial or consumer projects. The effectiveness of the indirect channel is essential for market penetration and serving the fragmented small and medium-sized enterprise (SME) market, requiring strong logistical capabilities and regional warehousing infrastructure to minimize delivery lead times.

Potential customers for extruded acrylic tubes are broadly categorized by their need for aesthetic appeal, light transmission capabilities, and material durability, positioning end-users across industrial, commercial, and consumer sectors. The most significant segment of buyers comprises Original Equipment Manufacturers (OEMs) within the lighting industry, who purchase tubes in bulk for manufacturing specialized linear LED fixtures, decorative light installations, and light guide components. These customers prioritize high optical quality, UV stability, and consistency in light diffusion properties, making them reliable, high-volume purchasers dependent on the continuous supply of specialized transparent and frosted tubes.

Another major category includes architectural and construction companies, as well as specialized metal and plastics fabricators who integrate acrylic tubes into interior and exterior building designs, such as stair railings, protective barriers, decorative columns, and specialized skylight elements. These buyers often seek large-diameter tubes with excellent weather resistance and compliance with regional fire and safety codes. Retail display manufacturers and visual merchandisers form a third critical customer base, relying on acrylic tubes for constructing dynamic, attractive point-of-sale (POS) displays, mannequins, and retail fixtures where aesthetics, scratch resistance, and ease of assembly are paramount purchasing considerations, driving demand for colored and satin-finished varieties.

Finally, specialized technical sectors, including biomedical laboratories, chemical processing plants, and industrial machinery manufacturers, represent high-value potential customers. In these environments, extruded acrylic tubes are used for complex fluid handling, pneumatic conveying systems, and protective machine guards. These technical buyers require superior chemical resistance, specific thermal performance characteristics, and extremely tight dimensional tolerances, often necessitating custom extrusion runs and rigorous quality certifications, providing opportunities for manufacturers focusing on specialized high-performance PMMA formulations and adherence to industry standards like FDA or specific laboratory compliance protocols.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.22 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Altuglas International (Arkema Group), Acrilex Inc., A&C Plastics Inc., Plaskolite LLC (Rowmark), ASTARIGLAS (PT. ASTARI NIAGARA INTERNASIONAL), Polycasa (Schweizer Group), Extrudex Plastics, Inc., Pexco LLC, Spartech LLC, Lucite International (Mitsubishi Chemical), 3A Composites, Asia Poly Industrial Sdn Bhd, Shanghai Acrylic Chemical Co., Ltd., Sumitomo Chemical, Reynolds Polymer Technology, Inc., Regal Plastics, GEM Plastic Co., Ltd., Elite Extrusion Technology, Inc., Sanmu Group, Perspex International. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Extruded Acrylic Tube Market is defined by continuous innovation focused on enhancing production efficiency, improving material performance, and achieving tighter dimensional control, essential for high-precision applications. A cornerstone technology is the use of specialized, multi-zoned temperature-controlled extrusion dies, often featuring proprietary designs that ensure uniform melt flow and prevent the formation of localized stress points within the emerging tube. Modern extruders are equipped with sophisticated gear pumps to maintain consistent volumetric throughput, directly translating to uniform wall thickness and minimizing the variations inherent in traditional single-screw extrusion processes. Furthermore, continuous process monitoring utilizing advanced sensors and feedback loops allows for immediate adjustments to variables like puller speed and cooling bath temperature, crucial for achieving the superior optical quality demanded by high-end consumers in the display and lighting sectors.

Advanced material science plays a crucial role, encompassing the development of specialty PMMA formulations. Key technological advancements include incorporating targeted UV stabilizers and anti-yellowing agents to extend the operational life of tubes in prolonged outdoor exposure, critical for signage and architectural uses. Manufacturers are also developing co-extrusion techniques that allow for the layering of different material properties—such as a base layer for mechanical strength and an outer layer for enhanced scratch or chemical resistance—in a single continuous process. This technological approach expands the application scope of extruded acrylic tubes into harsher industrial environments where monolithic PMMA might otherwise fail, broadening the addressable market for high-performance specialty profiles and complex geometrical shapes beyond simple circular tubes, requiring specialized tooling and precise thermal management during forming.

Automation and digitalization are becoming increasingly influential in the technology landscape. The implementation of high-speed, non-contact laser and optical micrometers integrated into the production line allows for immediate, accurate measurement of outer diameter, inner diameter, and eccentricity. This data is often fed back into the process control system, enabling closed-loop tolerance adjustments, minimizing waste, and guaranteeing compliance with rigorous quality standards, thereby enhancing overall production throughput and reducing labor costs associated with manual quality checks. The shift towards large-scale, automated production facilities globally necessitates investments in these cutting-edge monitoring and control systems to maintain a competitive edge, driving the industry toward highly digitized, precision manufacturing paradigms that maximize material yield and decrease cycle times for continuous, high-volume orders.

Regional dynamics play a crucial role in shaping the Extruded Acrylic Tube Market, influenced by varying levels of industrialization, infrastructure spending, and regional regulatory frameworks concerning materials and environmental sustainability. The market is currently dominated by Asia Pacific (APAC), which exhibits the highest volume consumption globally. This dominance is attributable to the region's robust manufacturing sector, including massive production hubs for electronics, automotive components, and the relentless pace of urbanization requiring acrylic tubing for architectural elements and energy-efficient lighting installations in rapidly expanding metropolitan centers. Countries such as China, India, and Southeast Asian nations are undergoing massive infrastructural developments, providing sustained, large-scale demand for cost-effective, durable acrylic products, often leading to competitive pricing structures and high utilization rates among local extrusion firms.

North America and Europe represent mature markets characterized by stable but slower growth, primarily focused on high-value, specialized applications that demand premium quality and certification. In these regions, growth is driven by regulatory pushes towards energy efficiency, boosting the demand for advanced LED lighting systems using high-clarity acrylic diffusers, and stringent quality requirements in the medical, aerospace, and high-end retail display sectors. European manufacturers, in particular, face increasingly demanding environmental regulations (e.g., REACH), compelling them to invest in sustainable manufacturing processes and explore bio-based or recycled acrylic feedstocks. This focus on premiumization and sustainability supports higher average selling prices compared to the APAC volume market, prioritizing product innovation and strict adherence to specific industry certifications over pure cost competition.

Latin America (LATAM) and the Middle East and Africa (MEA) are emerging regions offering significant future potential, though currently holding smaller market shares. In LATAM, growth is tied to local economic stability and investments in commercial construction and retail infrastructure, particularly in Brazil and Mexico, creating a growing need for modern display materials and architectural elements. The MEA region, particularly the Gulf Cooperation Council (GCC) countries, is experiencing substantial government-led investment in large-scale infrastructure projects, tourism, and real estate development (such as smart city initiatives), fueling demand for high-performance, weather-resistant acrylic tubes suitable for harsh desert climates, notably for outdoor signage and specialized architectural installations where material longevity and resistance to extreme temperatures and UV radiation are paramount engineering requirements for material selection and design specification, ensuring a high-quality finished product.

Extruded acrylic tubes offer superior dimensional stability, tighter thickness tolerances, and are significantly more cost-effective for high-volume production due to the continuous manufacturing process. While cast acrylic often provides higher optical clarity and chemical resistance in very thick forms, extruded tubes are preferred for standardized applications requiring consistency, such as linear lighting diffusers and protective sleeves. The extrusion process allows for longer continuous lengths and generally exhibits better bonding characteristics for fabrication processes.

Profitability is highly sensitive to the fluctuation of Methyl Methacrylate (MMA) monomer prices, as it constitutes the largest proportion of raw material cost. Price volatility, often linked to global petroleum prices and upstream chemical manufacturing constraints, compresses margins, especially for manufacturers without strong vertical integration or long-term fixed-price contracts. Companies mitigate this by optimizing extrusion efficiency, maintaining lean inventories, and utilizing advanced risk management strategies like forward contracts to stabilize input costs and ensure predictable operational budgets despite the inherent instability of the petrochemical supply chain.

Demand for large-diameter extruded acrylic tubes is primarily driven by industrial and architectural applications requiring robust, transparent structural components. These include large format outdoor and indoor signage (requiring superior weatherability), specialized fluid or air conveyance systems in industrial settings (demanding smooth inner walls and chemical compatibility), and high-end architectural elements like columns, decorative lighting fixtures, and display cases where impact strength and high aesthetic quality are critical design prerequisites. Technological advancements in extrusion machinery have made the production of these large, thick-walled profiles technically and economically viable for high-volume markets.

The Lighting and Signage industry segment consistently accounts for the highest global consumption of extruded acrylic tubes. Acrylic's exceptional optical clarity (up to 92% light transmission), combined with its UV stability and lightweight characteristics, makes it the material of choice for LED light diffusers, protective housings, fluorescent fixture covers, and large-scale backlit sign boxes. The rapid global transition to energy-efficient LED technology, driven by regulatory mandates and consumer energy savings, ensures sustained, high-volume demand from this crucial end-use sector, far surpassing consumption in construction or medical segments.

Yes, sustainability is an increasing focus. PMMA is fully recyclable, and two primary methods exist. Mechanical recycling involves grinding and re-extruding clean scrap, suitable for non-critical applications. More importantly, chemical recycling (depolymerization) breaks the PMMA polymer chain back down into its original high-purity MMA monomer. This advanced process allows the recovered monomer to be used in producing new, optically clear acrylic tubes without loss of quality, supporting circular economy initiatives and meeting stringent environmental targets mandated by international bodies and large corporate consumers seeking verified sustainable material sourcing documentation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.