ID : MRU_ 436261 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

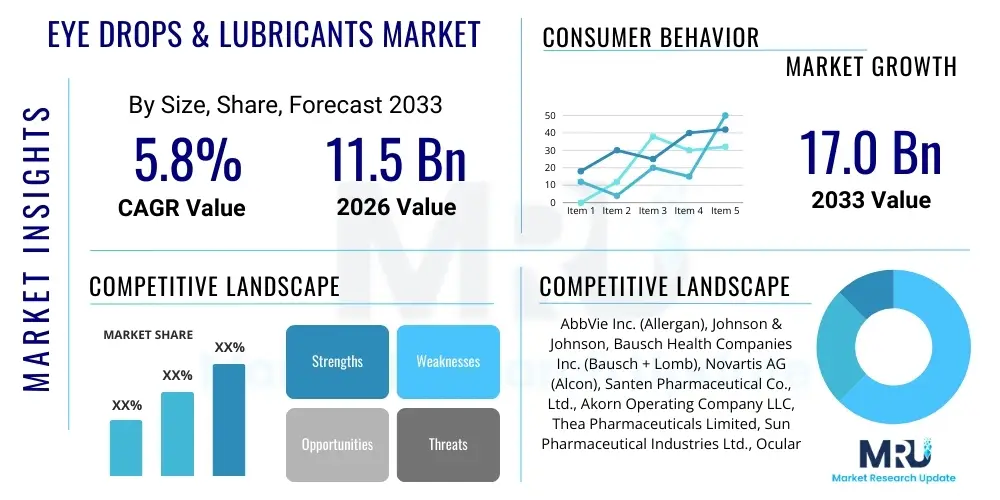

The Eye Drops & Lubricants Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 11.5 billion in 2026 and is projected to reach USD 17.0 billion by the end of the forecast period in 2033. This substantial growth trajectory is underpinned by the rising global prevalence of chronic ocular conditions, the expanding aging demographic requiring consistent vision support, and the increasing usage of digital devices leading to higher incidence of dry eye syndrome (DES). Technological advancements focused on enhanced drug delivery mechanisms, such as sustained-release formulations and preservative-free solutions, are further fueling market expansion by improving patient adherence and therapeutic efficacy.

The Eye Drops & Lubricants Market encompasses a diverse range of sterile ophthalmic preparations designed to treat, manage, or alleviate symptoms associated with various eye conditions, ranging from simple dryness and irritation to complex diseases like glaucoma and chronic infections. These products include artificial tears, therapeutic drops (antibiotics, steroids, anti-allergics), and highly specialized solutions used post-surgery or for managing severe ocular surface diseases. The primary function of eye lubricants, specifically, is to restore and maintain the natural moisture balance and viscoelasticity of the tear film, protecting the delicate corneal and conjunctival surfaces from environmental stressors and inflammation. As global healthcare awareness increases, coupled with improved access to ophthalmic care in developing regions, the demand for these essential ocular healthcare products is accelerating significantly.

Major applications for eye drops extend across several therapeutic areas, including the management of dry eye disease (DED), allergic conjunctivitis, bacterial and viral infections, and the reduction of intraocular pressure (IOP) in glaucoma patients. The benefits of using these products are critical, offering symptomatic relief, preventing potential vision loss from untreated infections or high IOP, and enhancing overall quality of life by mitigating discomfort and visual disturbances. Driving factors for this robust market growth include the ubiquitous adoption of digital screens, which exacerbates DED; the demographic shift toward an older population inherently prone to ocular diseases; and continuous innovation in formulation chemistry, yielding more effective, comfortable, and longer-lasting relief options for consumers and patients globally.

The global Eye Drops & Lubricants Market is experiencing robust expansion driven by converging business trends, including a strong shift toward specialized and prescription-based products, particularly anti-inflammatory agents targeting the underlying causes of chronic dry eye, rather than merely treating symptoms. Key industry players are heavily investing in mergers and acquisitions and strategic collaborations to integrate advanced drug delivery technologies, such as nano-emulsions and liposomal systems, ensuring superior bioavailability and sustained ocular residence time. Furthermore, the market is capitalizing on the growing consumer preference for preservative-free formulations, addressing concerns related to potential long-term toxicity and irritation associated with traditional preservatives, which is pushing manufacturers to adopt innovative multi-dose and unit-dose packaging solutions.

Regionally, North America maintains its dominance due to high healthcare expenditure, established reimbursement policies, and a high rate of adoption of premium, specialized ophthalmic solutions. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate, fueled by improving access to healthcare, rising pollution levels contributing to ocular irritation, and the sheer volume of its aging population. Segment trends highlight that the Prescription segment is gaining significant traction over the Over-The-Counter (OTC) segment, primarily due to the increasing diagnosis of severe or chronic conditions requiring pharmacological intervention, such as cyclosporine or lifitegrast for dry eye treatment. Lubricants and artificial tears remain the largest product category, but the therapeutic segment, encompassing anti-allergic and anti-infective drops, is exhibiting accelerated expansion due to seasonal allergy spikes and higher incidence rates of ocular infections in dense urban environments.

User queries regarding AI's influence in the ophthalmic domain frequently center on how machine learning algorithms can enhance the diagnosis of dry eye disease (DED) severity, predict patient response to specific therapeutic eye drops, and optimize the drug development lifecycle. Users are particularly interested in AI's role in processing vast datasets from clinical trials to identify biomarkers for novel drop formulations, accelerating the time-to-market for specialized lubricants and medications. Furthermore, significant concern and interest are directed towards AI-powered teleophthalmology platforms, which could increase access to timely prescriptions for eye drops, potentially disrupting traditional physician-patient consultation models. Overall, the collective expectation is that AI will streamline R&D, personalize treatment regimens based on genetic and lifestyle data, and improve manufacturing efficiency, particularly in quality control for sterile ophthalmic products.

The Eye Drops & Lubricants Market is shaped by a critical interplay of strong demographic and technological drivers counterbalanced by stringent regulatory hurdles and cost constraints, defining the overall market trajectory. The primary drivers stem from the global increase in screen time and digital device usage across all age groups, leading to widespread ocular fatigue and exacerbating symptoms of dry eye disease. This trend is compounded by the substantial growth of the elderly population, who naturally experience reduced tear production and increased susceptibility to chronic ocular diseases like glaucoma, necessitating long-term therapeutic drop usage. Furthermore, continuous advancements in pharmaceutical technology, particularly the development of superior preservative-free formulas and sustained-release systems that enhance patient comfort and compliance, act as potent growth accelerators.

Conversely, the market faces significant restraints, including the high development and manufacturing costs associated with producing sterile, specialized, and preservative-free solutions, which often translate into elevated end-user prices, impacting accessibility in low- and middle-income regions. The stringent regulatory approval process imposed by bodies like the FDA and EMA for novel ophthalmic drugs, requiring extensive clinical validation, can delay market entry and increase investment risk. Moreover, the over-the-counter (OTC) segment is characterized by intense price competition and saturation with generic artificial tear products, which sometimes confuses consumers and limits the penetration of premium, specialized lubricants.

Opportunities for expansion are abundant, particularly in emerging economies where rising disposable incomes and improving healthcare infrastructure facilitate greater access to specialized ocular care. The market is also poised to benefit significantly from the integration of personalized medicine approaches, where eye drops are formulated or prescribed based on individual tear film characteristics and genetic profiles, maximizing therapeutic outcomes. The development of advanced combination therapies—such as drops pairing a lubricating agent with an anti-inflammatory component—and the utilization of smart packaging solutions for dosing compliance represent key avenues for future innovation and market capture. These dynamics collectively define the impact forces, pushing the market toward specialized, high-efficacy, and consumer-friendly products.

The Eye Drops & Lubricants Market is meticulously segmented based on product type, formulation, application, prescription type, and distribution channel, reflecting the varied clinical needs and commercial pathways within the ophthalmic industry. Analyzing these segments provides strategic insights into consumer preferences and areas of high growth potential. The market is primarily divided between therapeutic (prescription) and moisturizing (OTC) solutions, with the therapeutic segment showing faster value growth due to the rising prevalence of chronic conditions requiring physician intervention. Furthermore, the segmentation by formulation (e.g., solution, suspension, emulsion, gel) is crucial, as patients often prioritize comfort and the duration of action provided by the product, driving demand for advanced viscoelastic gels and nano-emulsion systems which offer prolonged retention on the ocular surface.

The value chain for the Eye Drops & Lubricants Market begins with the highly specialized upstream analysis involving the sourcing and synthesis of pharmaceutical grade active pharmaceutical ingredients (APIs), excipients, and proprietary stabilizing agents, particularly high-quality hyaluronic acid or carboxymethylcellulose. Research and Development activities at this stage focus intensely on formulation science, ensuring stability, sterility, and optimal pH balance for ocular comfort. Due to the stringent requirements for sterility and low endotoxin levels, the quality control throughout the manufacturing phase is rigorous and costly, often requiring specialized cleanroom facilities. Key upstream suppliers are focused on providing novel preservation systems or unique packaging materials, such as blow-fill-seal unit-dose vials or multi-dose preservative-free bottles, which are essential for market differentiation.

The midstream phase involves the primary manufacturing and packaging of the final product, followed by secondary packaging and labeling compliant with diverse global regulatory standards. Downstream analysis focuses on the efficient movement of finished products to end-users. The distribution channel is multifaceted, comprising direct sales to large hospital groups for surgical and inpatient use, and indirect distribution through wholesalers, distributors, and third-party logistics providers (3PLs) who manage supply to retail and online pharmacies. Retail pharmacies, including major drug store chains, represent the largest indirect route for OTC products, benefiting from consumer self-selection and pharmacist recommendations. The rapid expansion of the online pharmacy channel, especially for recurring purchases of artificial tears, is reshaping downstream dynamics by offering greater convenience and often competitive pricing, challenging traditional brick-and-mortar retail dominance and expanding geographical reach.

The potential customer base for the Eye Drops & Lubricants Market is vast and highly diverse, segmented broadly into individuals requiring maintenance care for chronic conditions and those seeking symptomatic relief for acute issues. Primary end-users include the geriatric population (aged 65 and above) who inherently suffer from age-related ocular conditions such as chronic dry eye and glaucoma, requiring daily, long-term therapeutic drops. Another significant buyer segment comprises individuals who experience ocular surface irritation due to prolonged use of digital devices, contact lens wear, or exposure to environmental irritants like pollution and low humidity. This segment often purchases high-volume, over-the-counter artificial tears and lubricants.

Institutional buyers, such as hospitals, ambulatory surgical centers (ASCs), and specialized eye clinics, represent crucial purchasers, particularly for post-operative care drops, specialized anti-infectives, and high-cost therapeutic agents administered under direct medical supervision. Furthermore, the growing global population diagnosed with systemic diseases that manifest in ocular symptoms, such as Sjögren’s syndrome and diabetes, constitute a specialized but high-value customer group requiring complex and often prescription-only formulations. Targeted marketing and product innovation efforts are increasingly focused on these distinct buyer profiles to ensure product differentiation and maximize market penetration across both the consumer self-care and medical prescription pathways.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 billion |

| Market Forecast in 2033 | USD 17.0 billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AbbVie Inc. (Allergan), Johnson & Johnson, Bausch Health Companies Inc. (Bausch + Lomb), Novartis AG (Alcon), Santen Pharmaceutical Co., Ltd., Akorn Operating Company LLC, Thea Pharmaceuticals Limited, Sun Pharmaceutical Industries Ltd., Ocular Therapeutix, Inc., Kala Pharmaceuticals, Inc., Otsuka Pharmaceutical Co., Ltd., Dompé farmaceutici S.p.A., Sentiss Pharma Pvt. Ltd., Prestige Consumer Healthcare Inc., Aspen Pharmacare Holdings Limited, Takeda Pharmaceutical Company Limited, Cipla Ltd., SIFI S.p.A., Aerie Pharmaceuticals, Inc., Glaukos Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Eye Drops & Lubricants Market is continually evolving, driven by significant technological breakthroughs aimed at improving drug delivery efficacy, reducing side effects, and enhancing patient convenience. A crucial area of innovation is the development of sustained-release drug delivery systems, which aim to increase the duration the active ingredients remain on the ocular surface, reducing the need for frequent dosing and improving patient compliance, a long-standing challenge in treating chronic conditions like glaucoma. Technologies such as nanomicellar formulations, liposomal encapsulation, and hydrogel-forming systems are now extensively utilized to ensure APIs penetrate the ocular barrier more effectively and are released slowly over several hours, maintaining stable therapeutic concentrations. This shift moves beyond traditional simple aqueous solutions toward complex, engineered delivery vehicles.

Another fundamental technological advancement is the widespread adoption of preservative-free packaging solutions. Benzalkonium chloride (BAK), a common preservative, is increasingly recognized for causing ocular surface toxicity and exacerbating dry eye symptoms with chronic use. To mitigate this, manufacturers are employing advanced packaging technologies such as the OSD (Ophthalmic Squeeze Dispenser) system or specialized multi-dose bottles that incorporate filtration or silver ion technology to maintain sterility without chemical preservatives. Furthermore, the incorporation of advanced biological components, such as high molecular weight hyaluronic acid and specific osmolarity-regulating agents, is improving the intrinsic quality of artificial tears, making them closer in composition and function to natural human tears, thereby providing superior comfort and healing properties.

The integration of smart technology is also beginning to impact the market landscape. This includes connected dosing devices and smart caps designed to track patient adherence to complex therapeutic regimens, particularly important for glaucoma patients whose treatment efficacy relies heavily on consistent, accurate dosing. Ongoing research is exploring wearable diagnostic technologies that monitor tear film metrics in real-time, providing feedback that could inform the optimal type and frequency of eye drop usage, moving the market closer to truly personalized and adaptive ocular care solutions. These technological thrusts collectively promise to significantly elevate the standard of care available to patients globally and sustain the market's high-value growth.

The global Eye Drops & Lubricants Market demonstrates significant geographical variations in terms of consumption patterns, regulatory environments, and underlying disease burden, necessitating region-specific market strategies. North America, comprising the United States and Canada, currently holds the largest market share globally. This dominance is attributed to high per capita healthcare spending, the early adoption of advanced pharmaceutical technologies, particularly complex prescription-based dry eye treatments, and the strong presence of major pharmaceutical companies and specialized R&D centers. The high prevalence of DED, driven by intensive digital use and favorable reimbursement policies for specialized treatments, ensures sustained demand for both OTC lubricants and high-value therapeutic drops in this region.

Europe represents a mature market characterized by stringent quality control standards and a high proportion of aging citizens, particularly in Western European countries like Germany, France, and the UK, driving consistent demand for anti-glaucoma and specialized post-operative drops. The regulatory focus in Europe strongly favors preservative-free formulations, accelerating the shift among local manufacturers toward advanced packaging and unit-dose formats to meet these environmental and safety standards. Furthermore, the prevalence of seasonal allergies in certain European regions ensures a steady requirement for anti-allergic eye drop medications, supporting the growth of the therapeutic segment.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market globally throughout the forecast period. This rapid growth is fueled by massive populations, improving economic conditions leading to greater accessibility to private healthcare, and increasing awareness regarding ocular health. Significant urbanization, coupled with high levels of industrial pollution, is increasing the incidence of allergic conjunctivitis and environmental dry eye. Countries such as China, India, and South Korea are witnessing substantial investment in healthcare infrastructure and local manufacturing capabilities, making them attractive targets for market expansion, particularly for mass-market OTC products and affordable generics.

Latin America and the Middle East & Africa (MEA) currently hold smaller but rapidly developing market shares. Growth in Latin America is driven by rising chronic disease burdens and improving government healthcare initiatives, though market penetration remains challenged by economic volatility and limited reimbursement. In the MEA region, the market is characterized by increasing urbanization, high exposure to arid climates contributing to DED, and significant, albeit concentrated, healthcare expenditure in Gulf Cooperation Council (GCC) countries, which are adopting advanced ophthalmic treatments at a rapid pace, albeit often relying on imports from Western markets.

The primary driver is the increased clinical and consumer awareness regarding the potential long-term toxicity and ocular surface irritation caused by traditional chemical preservatives like Benzalkonium Chloride (BAK). Preservative-free formulations are essential for chronic users, post-operative patients, and individuals with severe dry eye disease, leading to greater comfort and improved treatment adherence.

Excessive digital screen time significantly reduces the blink rate, leading to increased tear film evaporation and higher incidence of Dry Eye Syndrome (DES). This has substantially amplified the demand for lubricating eye drops (artificial tears) globally, making the ‘digital eye strain’ demographic a key growth engine for the OTC segment.

The most critical technological advancement is the development of sustained-release drug delivery systems, such as nano-emulsions and specialized hydrogels. These technologies minimize the required dosing frequency, increase the duration the medication stays on the ocular surface, and improve overall patient compliance for chronic conditions like glaucoma and advanced DED.

The Prescription (Rx) segment is generally growing faster in value. While OTC lubricants have high volume, the Rx segment includes high-value, specialized anti-inflammatory agents and glaucoma medications, which command premium pricing and are essential for treating the underlying causes of chronic ocular diseases.

Novel formulations face stringent regulatory hurdles, particularly concerning demonstrating long-term sterility, stability over the product lifecycle, and minimizing risk of ocular toxicity. Extensive Phase III clinical trials are often mandated, leading to high R&D costs and lengthy approval timelines, especially for biologic or combination therapies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.