ID : MRU_ 434587 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

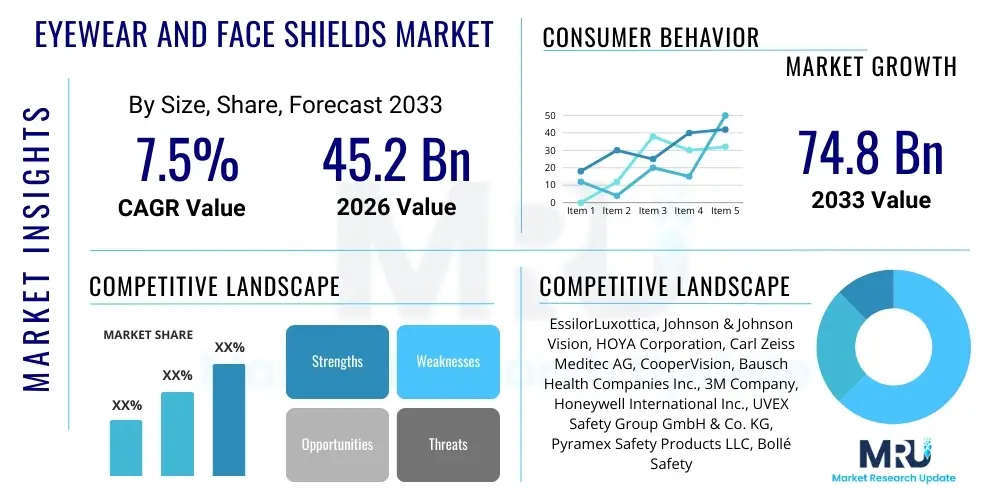

The Eyewear and Face Shields Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 45.2 Billion in 2026 and is projected to reach USD 74.8 Billion by the end of the forecast period in 2033.

The Eyewear and Face Shields Market encompasses a broad spectrum of products crucial for both vision correction, fashion aesthetics, and personal protective equipment (PPE). This expansive market includes prescription spectacles, contact lenses, sunglasses, and specialized safety products like industrial goggles, protective safety glasses, and medical-grade face shields. The foundational driving factors include the global rise in vision disorders such as myopia and presbyopia, requiring corrective lenses, alongside burgeoning consumer demand for aesthetically pleasing, branded, and technologically advanced eyewear. Furthermore, stringent occupational safety regulations across industries like manufacturing, construction, and healthcare necessitate the mandatory use of high-quality protective eyewear and face shields, ensuring employee welfare and compliance with established workplace standards.

Products within this domain serve dual critical roles: enhancing daily life through improved vision and protecting individuals from physical, chemical, and biological hazards. Eyewear benefits range from superior optical clarity and UV protection to integration of smart technologies like augmented reality (AR) and blue-light filtering capabilities. Face shields, particularly their increased prominence following global health crises, provide critical barrier protection against splashes, droplets, and particulate matter, complementing other forms of PPE. The synergy between consumer optics and safety equipment segments creates a resilient market structure, capitalizing on both elective purchases driven by fashion cycles and mandatory purchases dictated by regulatory mandates.

Key driving factors propelling market expansion include the rapid aging of the global population, which consistently increases the demand for multifocal and progressive lenses, and the growing awareness regarding eye health associated with prolonged digital screen usage. Technological advancements in lens materials, coating techniques (such as anti-fog and scratch-resistant layers), and the miniaturization of electronic components in smart glasses are continually opening new application avenues. Major applications span retail optical stores, e-commerce platforms, hospitals, clinics, manufacturing facilities, laboratories, and specialized environments like cleanrooms, confirming the ubiquity and essential nature of these products across the modern economy.

The Eyewear and Face Shields Market is characterized by robust growth, driven primarily by evolving consumer lifestyles, stringent safety legislation, and rapid technological integration. Business trends indicate a significant shift towards omni-channel distribution models, combining the personalized service of traditional brick-and-mortar stores with the convenience and competitive pricing of online platforms. The luxury segment is witnessing increased consolidation, focusing on exclusive materials and design partnerships, while the mass market emphasizes affordability and rapid supply chain responses. A key operational trend is the adoption of automated lens manufacturing and 3D printing technologies, allowing for faster customization and reduced production lead times, particularly benefiting the highly fragmented corrective lenses segment and enabling precise, tailored protective equipment designs. Furthermore, sustainability and ethical sourcing of materials (e.g., bio-based plastics) are becoming crucial competitive differentiators, influencing consumer purchasing decisions globally.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, fueled by its immense population base, increasing incidence of myopia (especially among younger demographics), rising disposable incomes in economies like China and India, and expanding industrial infrastructure that mandates occupational safety gear. North America and Europe maintain leading positions in terms of technological adoption, high average selling prices, and dominance in the smart eyewear and luxury segments. Emerging markets in Latin America and MEA are experiencing accelerating demand, primarily driven by improved healthcare access and stricter implementation of industrial safety protocols. Regional trends also reflect geopolitical influences on supply chains; diversification of manufacturing capabilities away from single regions is becoming a strategic priority for multinational corporations.

Segment trends highlight the significant penetration of polycarbonate materials due to their impact resistance, crucial for both sports eyewear and safety shields. In terms of product type, contact lenses, particularly daily disposables, are experiencing the fastest growth due to enhanced hygiene and user convenience. The face shields segment, while experiencing normalization post-peak pandemic demand, remains structurally larger than historical levels, sustained by permanent changes in hygiene practices within healthcare and specific high-risk industrial environments. The smart eyewear segment, though nascent, is rapidly gaining traction in enterprise applications (e.g., remote assistance and training) and is expected to revolutionize consumer engagement by integrating health monitoring and seamless digital connectivity, transitioning eyewear from a necessity or accessory into a functional computing platform.

User queries regarding the influence of Artificial Intelligence (AI) on the Eyewear and Face Shields market generally revolve around customization, diagnostics, supply chain efficiency, and the capabilities of smart eyewear. Key themes include the use of AI for personalized lens prescriptions derived from complex ophthalmic data, the role of machine learning in optimizing supply chain logistics and reducing inventory waste, and the potential for AI algorithms embedded in smart glasses to enhance user experience through contextual awareness and advanced real-time data analysis. There is significant user expectation regarding AI assisting in rapid quality control during manufacturing and optimizing the ergonomic design of face shields for extended wear comfort, suggesting a shift towards highly individualized and digitally optimized products.

The dynamics of the Eyewear and Face Shields Market are significantly shaped by a confluence of accelerating drivers, structural restraints, and emerging opportunities, collectively defining the impact forces influencing market trajectories. A primary driver is the global increase in occupational safety mandates, particularly the tightening of OSHA and EN standards requiring high-impact protective gear in industrial settings, which perpetually sustains demand for robust safety eyewear and face shields. Simultaneously, demographic shifts, specifically the rapidly aging population worldwide and the escalating global prevalence of digital eye strain and myopia, create an undeniable, systemic demand for corrective lenses and associated blue-light protection technology. These demand-side pressures are complemented by continuous advancements in material science, which enable the production of lighter, durable, and aesthetically superior products, thus encouraging consumer adoption and trade-up purchases in the elective segment of the market.

However, the market faces several restraining forces that moderate growth. The relatively high cost associated with advanced vision solutions, such as progressive lenses, specialized coatings, and cutting-edge smart glasses technology, acts as a significant barrier to entry or widespread adoption in price-sensitive developing regions. Furthermore, the optical sector struggles with a persistent issue of counterfeit and low-quality products, which not only erode manufacturer profitability but also pose significant safety risks, particularly in the protective equipment subsegment, necessitating constant vigilance and investment in intellectual property protection. The complexity and highly regulated nature of medical device classification for certain contact lenses and surgical protective gear also introduce time-consuming and expensive approval processes, hindering rapid market entry for innovative products.

Opportunities for exponential growth are concentrated in the commercialization of smart eyewear for specialized applications, moving beyond novelty into high-utility enterprise solutions (e.g., logistics, field service). The expansion of tele-optometry and remote diagnostics presents a novel opportunity to increase access to eye care services in underserved rural areas, thereby expanding the potential customer base for prescription eyewear. The integration of enhanced features such as self-cleaning coatings, photochromic lens technology that reacts instantly to light changes, and sophisticated anti-fog mechanisms for face shields represent immediate opportunities for product differentiation and premium pricing. The overarching impact force is the permanent integration of safety consciousness into daily life post-pandemic, ensuring that the demand for readily available, high-quality facial protection remains significantly elevated compared to pre-2020 levels, shifting face shields from niche industrial items to broader public health accessories.

The Eyewear and Face Shields market is highly fragmented, segmented comprehensively across product type, material, application (end-user), and distribution channel to reflect the diversity in consumer needs and regulatory requirements. The segmentation allows stakeholders to accurately gauge demand variations between high-fashion corrective lenses and mandatory industrial protective gear. Product types differentiate between vision correction tools (spectacles, contact lenses) and protection/accessory items (sunglasses, safety goggles, face shields). Material segmentation focuses on performance characteristics such as impact resistance, clarity, and weight, primarily differentiating between various plastics (polycarbonate, acrylic, CR-39) and traditional glass. The application segmentation is critical, dividing demand between the highly regulated healthcare sector, the robust industrial safety segment, and the dynamic, consumer-driven retail segment, each characterized by distinct purchasing behaviors and compliance requirements.

The value chain for the Eyewear and Face Shields Market is complex, beginning with raw material sourcing and culminating in the highly specialized distribution to end-users, encompassing both medical-grade products and fast-moving consumer goods. Upstream analysis focuses heavily on the procurement of specialized raw materials, including high-grade optical polymers (like polycarbonate and various high-index plastics), metal alloys (titanium, stainless steel) for frames, and specific chemical components for lens coatings and cleaning solutions. Key upstream suppliers must meet stringent quality control standards, especially for materials destined for medical or high-impact safety applications. Pricing volatility and sustainability certifications regarding these base materials are major concerns at this stage. Manufacturers often engage in long-term supply contracts to ensure consistent quality and availability, given the high barrier to entry for producing optical-grade resins.

The midstream phase involves manufacturing, which is highly technological and capital-intensive, covering lens molding, grinding, polishing, coating application (anti-reflective, anti-scratch, UV protection), frame fabrication, and the assembly of face shield components. Direct manufacturing focuses on integrated processes where large corporations control raw material refinement to finished product assembly, allowing for maximized control over quality and cost. Downstream activities are dominated by specialized logistics and comprehensive marketing strategies tailored to distinct market segments. Distribution channels are varied: direct channels dominate the highly regulated industrial safety and medical segments (selling directly to hospitals or large corporations), ensuring compliance and bulk purchasing efficiencies. This requires deep product knowledge from the sales team and robust traceability systems.

The indirect distribution channel is prevalent in the consumer eyewear segment, utilizing a vast network of wholesale distributors, independent optometrists, major retail chains, and rapidly growing e-commerce platforms. E-commerce platforms, characterized by simplified purchasing and virtual try-on technology, are reshaping consumer interaction. The final stage involves the dispensing professional (optometrist or ophthalmologist) for prescription eyewear, who provides essential diagnostic and fitting services, adding significant value and technical expertise to the final delivery of the product. For face shields, industrial distributors act as crucial intermediaries, ensuring quick, localized supply of safety-compliant products to high-demand worksites.

Potential customers for the Eyewear and Face Shields Market span a diverse range of end-users, broadly categorized into individual consumers requiring vision correction or fashion accessories, and institutional buyers adhering to safety and health regulations. The consumer segment is the largest volumetric market, encompassing individuals across all age groups who purchase spectacles, contact lenses, and sunglasses driven by necessity (poor vision), lifestyle needs (digital strain), or fashion trends. Specifically, the elderly population (60+) represents a critical and expanding customer base due to the increasing incidence of presbyopia, cataracts, and other age-related vision impairments, necessitating frequent updates to prescription lenses and specialized lens types, such as progressive lenses. Younger demographics, including millennials and Gen Z, drive demand for fashionable frames, blue light filtering lenses, and convenient daily disposable contact lenses, leveraging social media and direct-to-consumer brand influence.

The institutional buyer base consists primarily of the industrial and healthcare sectors, where purchasing decisions are mandated by safety compliance and regulatory oversight rather than personal preference. Industrial customers include large multinational corporations operating in construction, heavy manufacturing, automotive production, oil and gas extraction, and mining, where stringent Personal Protective Equipment (PPE) standards necessitate high-impact safety glasses and heavy-duty face shields designed to protect against physical hazards, intense heat, or chemical exposure. Procurement in this sector is highly sensitive to product certifications (e.g., ANSI Z87.1 standards) and bulk pricing, favoring established industrial distributors capable of managing large, recurring orders and providing safety training support.

Healthcare facilities, encompassing hospitals, clinics, surgical centers, and research laboratories, represent another crucial institutional customer segment. These entities require medical-grade protective eyewear, including specialized surgical loupes, anti-fog safety goggles, and sterile face shields that offer protection against infectious agents and biological fluids. The purchasing cycles here are often driven by government funding, epidemic preparedness needs, and adherence to infection control protocols. Other niche customers include professional athletes, military personnel, and specialized vocational workers (e.g., welders, painters) who require highly specialized, performance-enhancing protective gear designed to withstand extreme conditions, often driving demand for advanced materials like Trivex and ballistic-rated polycarbonate.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 45.2 Billion |

| Market Forecast in 2033 | USD 74.8 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | EssilorLuxottica, Johnson & Johnson Vision, HOYA Corporation, Carl Zeiss Meditec AG, CooperVision, Bausch Health Companies Inc., 3M Company, Honeywell International Inc., UVEX Safety Group GmbH & Co. KG, Pyramex Safety Products LLC, Bollé Safety, Zenni Optical, Warby Parker, Marcolin S.p.A., Safilo Group S.p.A., PPG Industries, Rodenstock GmbH, Fielmann AG, Silhouette International Schmied AG, ClearVision Optical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Eyewear and Face Shields Market is undergoing continuous innovation, driven by material science breakthroughs, advanced manufacturing processes, and the integration of digital capabilities. A cornerstone of modern eyewear manufacturing is Free-Form Technology, which enables highly precise, complex curvatures on the back surface of lenses, drastically improving optical clarity and field of vision, especially for progressive lenses. This precision milling, often guided by proprietary algorithms, allows for maximum personalization based on frame geometry, prescription strength, and patient habits. Furthermore, the development of High-Index Materials (plastics with refractive indices up to 1.74) allows for significantly thinner and lighter lenses, catering to high-prescription users seeking aesthetic improvements and comfort. For protective gear, the advancement in anti-fog and anti-scratch coatings, often utilizing nanotechnology to create microscopic surface structures, is paramount, ensuring continuous visibility and extended product lifespan in demanding industrial and medical environments, thus mitigating user temptation to remove essential PPE.

Another major technological thrust involves Smart Eyewear and Augmented Reality (AR) integration. While consumer adoption remains slow, the enterprise segment is rapidly deploying smart glasses equipped with micro-displays, integrated cameras, and sensors (like gyroscopes and accelerometers). These devices utilize wave-guide technology and micro-projection systems to overlay digital information onto the user's field of vision, facilitating applications such as hands-free maintenance instructions, inventory management, and remote expert assistance in complex assembly operations. This technological convergence is blurring the lines between standard protective equipment and sophisticated computing platforms, offering unprecedented efficiency gains in industrial and logistics settings. Energy efficiency and battery miniaturization remain key challenges for further mass market penetration of consumer smart glasses.

In the domain of face shield manufacturing, technological advancements focus heavily on ergonomic design and material optimization. The use of advanced computational fluid dynamics (CFD) modeling helps engineers design optimal curvature and venting systems to maximize airflow and minimize fogging without compromising protection efficacy. The adoption of 3D printing (additive manufacturing) is becoming increasingly significant, especially for customized safety frames and specialized face shield brackets tailored for integration with other PPE, such as helmets or respirators. Moreover, the emergence of photochromic face shields that automatically adjust tint based on UV exposure, offering transitional protection, is enhancing usability in outdoor industrial applications. These technological investments underscore the industry’s commitment to not only protecting the user but also maximizing comfort and functionality for prolonged usage, directly impacting compliance rates in safety-critical sectors.

The market growth is primarily driven by three factors: the demographic increase in age-related vision defects (presbyopia and cataracts), stricter global occupational safety regulations mandating high-impact protective gear (ANSI, EN standards), and rising digital screen time, fueling demand for blue-light filtering and anti-fatigue corrective lenses.

E-commerce is a highly significant and rapidly growing distribution channel, especially for standardized products like sunglasses, reading glasses, and daily disposable contact lenses. It offers price competitiveness and convenience, augmented by technology like virtual try-ons, although prescription eyewear still often requires physical fitting and verification by an optical professional.

The most influential technological advancement is the widespread use of high-performance anti-fog and scratch-resistant coatings, often utilizing nanotechnology. These coatings significantly enhance the usability and longevity of safety glasses and face shields, crucial for maintaining user compliance in challenging, high-humidity, or dusty industrial and medical settings.

Asia Pacific (APAC) represents the most substantial growth opportunity, driven by its massive population base, increasing affluence leading to higher consumer spending on premium and corrective vision care, and the urgent need to address the rising prevalence of myopia among its younger generations.

Smart glasses are currently transforming the enterprise sector, offering critical applications in industrial maintenance, logistics, and field service through hands-free computing and augmented reality overlays. While still a niche segment of the overall market, their growing adoption in specialized occupational environments indicates a substantial, high-value future revenue stream, shifting eyewear towards functional utility.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.