ID : MRU_ 433971 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

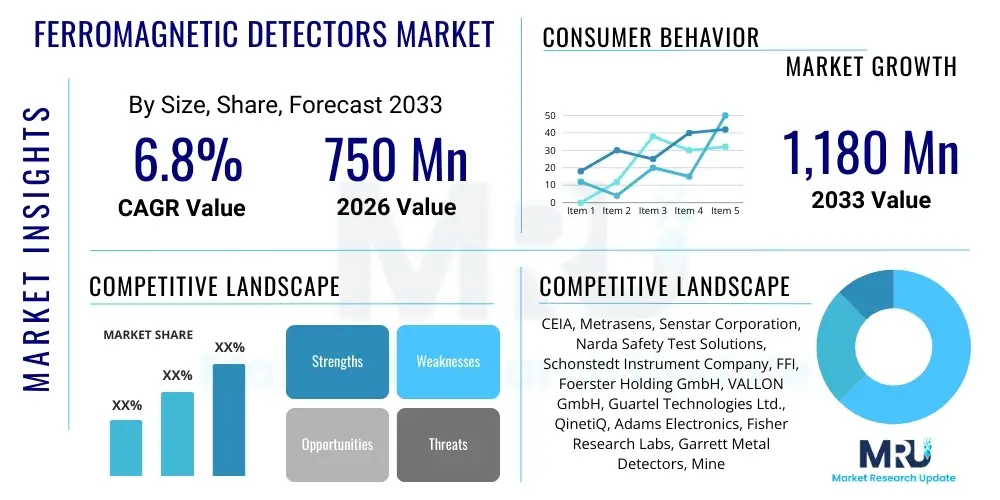

The Ferromagnetic Detectors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $750 Million in 2026 and is projected to reach $1,180 Million by the end of the forecast period in 2033.

The Ferromagnetic Detectors Market encompasses sophisticated devices designed to identify and localize objects containing ferrous materials by measuring disturbances in the local magnetic field. These detectors are instrumental in maintaining safety and security across various high-stakes environments, fundamentally differing from standard metal detectors by focusing specifically on materials susceptible to strong magnetic fields. The primary function is to prevent catastrophic failure or injury, especially in highly sensitive areas like Magnetic Resonance Imaging (MRI) suites, where projectile hazards pose a significant risk.

Ferromagnetic detectors (FMDs) are gaining prominence due to stringent safety regulations and the increasing deployment of high-field magnetic systems globally. Key applications span across medical safety screening, where FMDs prevent patients and staff from carrying dangerous ferromagnetic items into the strong static magnetic field of an MRI scanner, and security sectors, particularly for detecting weapons in highly regulated access points. The inherent benefits of these systems include high sensitivity to ferrous metals, quick detection times, and the ability to operate effectively even when the object is small or concealed.

The market growth is primarily driven by the expansion of healthcare infrastructure, specifically the rise in MRI installations worldwide, coupled with enhanced security requirements in critical national infrastructure and transportation hubs. Furthermore, the specialized use of FMDs in environmental remediation, such as the detection of unexploded ordnance (UXO), contributes significantly to market expansion. Technological advancements, focusing on miniaturization, enhanced sensor sensitivity, and improved user interface, are further accelerating the adoption rate across emerging economies.

The Ferromagnetic Detectors Market demonstrates robust growth, propelled by non-discretionary safety mandates, particularly within the healthcare sector concerning MRI safety protocols. Business trends indicate a strong focus on integration capabilities, where FMDs are increasingly incorporated into comprehensive screening systems alongside traditional metal detectors and body scanners to provide layered security solutions. Leading manufacturers are investing heavily in research and development to improve detection algorithms that minimize false alarms while maintaining maximal sensitivity, thereby enhancing operational efficiency for end-users. The trend toward portable and handheld FMD devices is also accelerating, catering to dynamic security environments and emergency applications.

Regionally, North America and Europe currently dominate the market due to the stringent implementation of medical safety standards (e.g., ACR Guidance) and high expenditure on advanced security technologies. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest Compound Annual Growth Rate (CAGR), driven by rapid expansion of public and private healthcare facilities, increasing infrastructure development, and a growing emphasis on national security and defense capabilities in countries like China, India, and Japan. Latin America and the Middle East and Africa (MEA) are also showing promising potential, mainly through government initiatives focused on enhancing airport security and hospital accreditation standards.

Segment trends reveal that the medical end-use segment holds the largest market share, directly correlated with the global increase in diagnostic imaging procedures utilizing MRI technology. In terms of product type, portal-based detectors (gate systems) remain dominant for high-throughput screening, whereas handheld detectors are gaining traction due to their flexibility and precision for targeted searching. The ongoing technological evolution is shifting consumer preference towards software-defined detectors that offer remote diagnostics, maintenance, and periodic updates to detection protocols, further solidifying market segments based on technological sophistication.

Common user questions regarding AI’s impact on Ferromagnetic Detectors often revolve around two central themes: how AI can eliminate false positives and whether AI can enhance the detection of smaller, less obvious threats. Users seek assurance that AI-driven analysis will improve the accuracy and speed of screening processes, especially in high-volume settings like airports or busy MRI suites, where operational flow is critical. Key concerns include the training data reliability for diverse ferromagnetic objects and the cost implication of integrating sophisticated AI algorithms into existing hardware infrastructure. Expectations are high for AI to provide predictive maintenance alerts and improve the adaptability of FMDs to environmental interference, ensuring continuous, reliable operation.

The integration of Artificial Intelligence, specifically machine learning (ML) and deep learning (DL), is transforming the effectiveness of Ferromagnetic Detection systems. AI algorithms are employed to analyze vast datasets of magnetic signatures generated by various ferrous objects, allowing the system to differentiate benign personal items (like keys or non-ferrous electronics) from actual threats (weapons or high-risk medical implants) with unprecedented accuracy. This leads to a significant reduction in nuisance alarms, a major operational pain point for end-users, thereby increasing screening throughput and reducing reliance on manual secondary checks.

Furthermore, AI-driven analytics are being used to optimize the sensitivity settings of FMDs dynamically based on environmental factors, crowd density, and historical data patterns unique to a specific installation. This predictive capability allows the detector to learn the ambient magnetic noise profile of its location and filter out persistent interference, maintaining high performance under variable conditions. While current FMD systems are predominantly hardware-centric, future market competitiveness will heavily depend on incorporating advanced software intelligence for improved threat discrimination and remote operational management.

The Ferromagnetic Detectors Market is primarily driven by mandatory safety protocols in the medical sector and increasing global security concerns, balanced against high installation costs and technological complexity. Opportunities lie in expanding applications in environmental and industrial safety, coupled with ongoing technological improvements in sensor technology and AI integration. These factors collectively exert moderate to high impact forces, pushing the market towards necessary upgrades and broader adoption.

Drivers

The paramount driver for the Ferromagnetic Detectors market is the globally recognized necessity for MRI safety screening. MRI machines utilize extremely powerful magnetic fields, and any unintended introduction of ferromagnetic materials can result in severe patient injury or damage to costly equipment. Regulatory bodies worldwide, including health organizations and hospital accreditation committees, are making FMD screening protocols mandatory, fueling consistent demand for reliable detection systems. Beyond healthcare, escalating geopolitical tensions and the rising threat of domestic security incidents necessitate advanced screening technology in government facilities, airports, and correctional institutions. This demand for non-invasive, high-precision security checks further solidifies the market base.

A secondary, yet significant, driver is the increasing complexity of infrastructure projects and environmental remediation efforts. FMDs are essential tools in detecting Unexploded Ordnance (UXO) during construction or clean-up operations in former conflict zones or military testing grounds. The expansion of oil and gas pipelines, railway networks, and large-scale industrial sites requires pre-screening for buried ferrous anomalies, contributing substantially to the market growth, particularly in developing regions undergoing rapid infrastructure expansion. This necessity for preemptive hazard detection provides a stable growth trajectory independent of immediate security crises.

Restraints

Despite strong drivers, the market faces significant restraints, chiefly the high initial capital expenditure associated with purchasing and installing advanced FMD systems. High-sensitivity detectors, especially those integrated into full portal systems, involve sophisticated sensor arrays and complex shielding mechanisms, making them significantly more expensive than standard metal detectors. This cost often proves prohibitive for smaller hospitals or facilities with limited budgets, particularly in lower-income countries. Additionally, the operational complexity and the need for specialized training for staff to correctly interpret alerts and maintain calibration pose ongoing challenges.

Another crucial restraint involves the issue of false positives and system calibration complexities. While modern systems strive for accuracy, environmental magnetic noise (e.g., proximity to heavy machinery, power lines, or structural steel) can frequently trigger nuisance alarms. Over-reliance on FMDs that frequently generate false alerts can lead to operational bottlenecks and reduced staff compliance with screening protocols, potentially undermining the safety benefits. Furthermore, the market faces technical hurdles related to detecting deep-seated or highly shielded ferromagnetic objects, limiting the complete scope of potential applications.

Opportunities

The primary opportunity lies in the burgeoning market for specialized industrial safety and forensic applications. FMDs can be adapted for use in manufacturing environments to detect internal defects in non-ferrous materials or for quality control processes. Furthermore, there is a strong opportunity for integrating FMD technology with advanced imaging systems, creating multi-modal security checkpoints that offer a complete profile of concealed objects. This fusion capability will be crucial for the next generation of high-throughput security solutions.

The second major opportunity is geographical expansion, specifically targeting emerging markets in APAC and MEA. As these regions modernize healthcare infrastructure and increase their focus on patient safety accreditation, the demand for mandatory MRI safety screening systems will skyrocket. Developing affordable, scalable FMD solutions tailored for these markets, alongside strong local distribution and maintenance support, presents a substantial avenue for market penetration and sustained revenue growth over the forecast period.

The Ferromagnetic Detectors Market is segmented primarily based on Product Type (Portal Detectors, Handheld Detectors), End-User (Medical & Healthcare, Security & Defense, Others), and Application (MRI Safety Screening, General Security Screening, UXO Detection). This segmentation helps in understanding the varying demands across different sectors, with medical applications dominating in terms of value due to stringent safety requirements, while security applications drive volume demand, particularly for portal systems. The ongoing trend is towards tailored solutions optimized for specific environments, such as ultra-high sensitivity models for detecting tiny metallic fragments in medical settings.

The value chain for the Ferromagnetic Detectors Market begins with the sourcing of highly specialized raw materials, predominantly advanced magnetic sensors (such as Fluxgate magnetometers or SQUID systems), precision electronics components, and high-grade materials for housing and shielding. The upstream activities are concentrated among a few specialized sensor manufacturers globally, meaning input costs and component availability can significantly influence the final product price and production timelines. Research and development activities, which involve complex electromagnetic modeling and algorithm design, are critical at this stage, dictating the detection accuracy and system reliability, which are key differentiators in the market.

The midstream activities involve the design, assembly, and rigorous calibration of the detector systems. Manufacturing complexity is high, especially for portal-based systems that require numerous synchronized sensors and sophisticated signal processing units. Key players often maintain proprietary assembly processes to ensure system integrity and maintain regulatory compliance, particularly for medical devices. Distribution channels are varied: direct sales are common for large government or high-value medical contracts, ensuring specialized installation and training. Indirect channels, utilizing specialized security distributors or medical equipment providers, are leveraged for smaller installations and regional market access, providing localized support.

Downstream analysis focuses heavily on after-sales service, installation, maintenance, and system upgrades. Given the safety-critical nature of FMDs (especially in MRI safety), end-users demand continuous performance assurance, making long-term service contracts highly valuable revenue streams for manufacturers. Direct distribution channels facilitate better control over service quality and adherence to strict regulatory standards, while specialized systems integrators often manage the complex integration of FMDs into broader security or facility management networks, completing the value chain by ensuring optimal system functionality and regulatory compliance for the end-user.

Potential customers for Ferromagnetic Detectors are primarily institutions operating environments where strong magnetic fields pose risks, or where the detection of concealed ferrous threats is paramount for public safety and operational continuity. The largest segment of buyers consists of large hospital networks, specialized diagnostic imaging centers, and private clinics globally that operate high-field MRI scanners. These customers purchase FMDs not only for regulatory compliance but as a fundamental component of patient and staff safety protocols, demanding high reliability and minimal workflow disruption.

The second major cohort of buyers includes governmental entities, encompassing national defense organizations, security agencies, civil aviation authorities, and correctional facilities. These customers require robust, high-throughput FMD systems for screening personnel and visitors at sensitive entry points, military bases, and secure government buildings. Their purchasing decisions are often driven by national security mandates, requiring proven detection capabilities against diverse threat profiles and resilience against operational environments.

A growing segment of potential customers includes companies involved in environmental and infrastructure development, such as civil engineering firms, mining operations, and energy utility companies. These entities utilize FMDs for specialized tasks like locating buried pipelines, geological mapping, and crucial Unexploded Ordnance (UXO) clearance before construction begins. For these industrial buyers, the key purchasing factors are ruggedness, depth penetration capabilities, and data accuracy for precise localization, signifying a broader diversification of end-user requirements beyond traditional security applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $750 Million |

| Market Forecast in 2033 | $1,180 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | CEIA, Metrasens, Senstar Corporation, Narda Safety Test Solutions, Schonstedt Instrument Company, FFI, Foerster Holding GmbH, VALLON GmbH, Guartel Technologies Ltd., QinetiQ, Adams Electronics, Fisher Research Labs, Garrett Metal Detectors, Minelab International, OSI Systems. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Ferromagnetic Detectors market is defined by advancements in highly sensitive magnetic sensor technology, signal processing algorithms, and robust system integration. Core technologies employed include Fluxgate Magnetometers, which measure minute changes in the Earth's magnetic field caused by the presence of ferrous objects, offering high sensitivity crucial for medical screening. Another key area is Superconducting Quantum Interference Devices (SQUIDs), although less common due to complexity and cooling requirements, they represent the peak of magnetic detection sensitivity and are primarily used in high-end research or military applications where ultra-deep detection is necessary.

Recent innovations are focusing heavily on developing multichannel sensor arrays combined with sophisticated digital signal processing (DSP). By utilizing multiple sensors (e.g., in a walk-through portal), systems can accurately pinpoint the location and approximate size of the ferromagnetic object, drastically improving threat resolution and reducing the likelihood of false alarms compared to older single-sensor systems. Furthermore, the development of specialized shielding materials and calibration techniques is essential to allow FMDs to operate reliably in electrically noisy environments typical of hospitals or industrial zones, enhancing overall device robustness and utility.

The future of FMD technology is intrinsically linked to software and connectivity. The implementation of Internet of Things (IoT) capabilities allows for remote monitoring, diagnostic checks, and centralized data management across multiple installed units. Furthermore, the increasing adoption of Artificial Intelligence and machine learning frameworks is allowing detectors to become "smarter," continuously learning new magnetic signatures and self-calibrating for optimal performance. This shift from purely hardware-centric detection to integrated smart sensing systems represents the most significant technological evolution expected during the forecast period.

Regional analysis indicates a mature yet consistently growing market across developed economies, with explosive growth potential concentrated in developing regions. North America currently leads the global Ferromagnetic Detectors market, largely attributed to strict enforcement of MRI safety standards (driven by organizations like the American College of Radiology), high healthcare expenditure, and the presence of major technology providers. The high rate of adoption of advanced portal systems in airports and critical infrastructure following updated security mandates further strengthens this dominance. Demand is consistent and focused on replacing older equipment with newer, AI-enhanced models boasting superior discrimination capabilities.

Europe follows closely, benefiting from high standards of public safety and a highly regulated medical device market. Countries such as Germany, the UK, and France are significant contributors, with the adoption driven by both civilian security needs and widespread military ordnance disposal projects, particularly in Central and Eastern Europe. European manufacturers often specialize in robust, high-precision detection equipment suitable for both medical and environmental field use, often integrating robust data logging capabilities mandated by EU regulations. The market here is characterized by sustained investments in technological refinement rather than sheer volume growth.

The Asia Pacific (APAC) region is poised to be the fastest-growing market segment. Rapid urbanization, massive infrastructure development, and substantial investment in healthcare expansion—especially the construction of new hospitals and diagnostic centers in China, India, and Southeast Asia—are fueling demand for FMDs, particularly for mandatory MRI safety screening. While budget constraints are sometimes a factor, the increasing awareness of international safety standards and the large-scale military/remediation efforts (UXO detection) provide significant untapped potential, encouraging aggressive market entry strategies from global manufacturers seeking high-volume regional sales.

FMDs are specialized instruments designed to detect objects possessing magnetic permeability (ferrous materials) by measuring localized disturbances in the magnetic field, making them highly effective near high-field magnets like MRI machines. Standard metal detectors utilize electromagnetic induction to detect all types of conductive metals (both ferrous and non-ferrous).

The market is projected to grow at a robust CAGR of 6.8% between 2026 and 2033, driven primarily by increasing global regulatory requirements for MRI safety and rising investment in security infrastructure worldwide.

The Medical and Healthcare segment currently holds the largest market share, dominated by the demand for advanced FMD systems necessary for screening patients and staff before entering high-field Magnetic Resonance Imaging (MRI) environments to prevent dangerous projectile incidents.

AI, through machine learning algorithms, significantly improves FMD accuracy by analyzing complex magnetic signatures, enabling systems to better discriminate between high-risk threats and benign personal ferrous items, thereby minimizing operational downtime caused by false alarms.

The Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate, fueled by substantial investment in new healthcare infrastructure, particularly MRI installations, and rising implementation of standardized safety protocols across developing economies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.