ID : MRU_ 436200 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

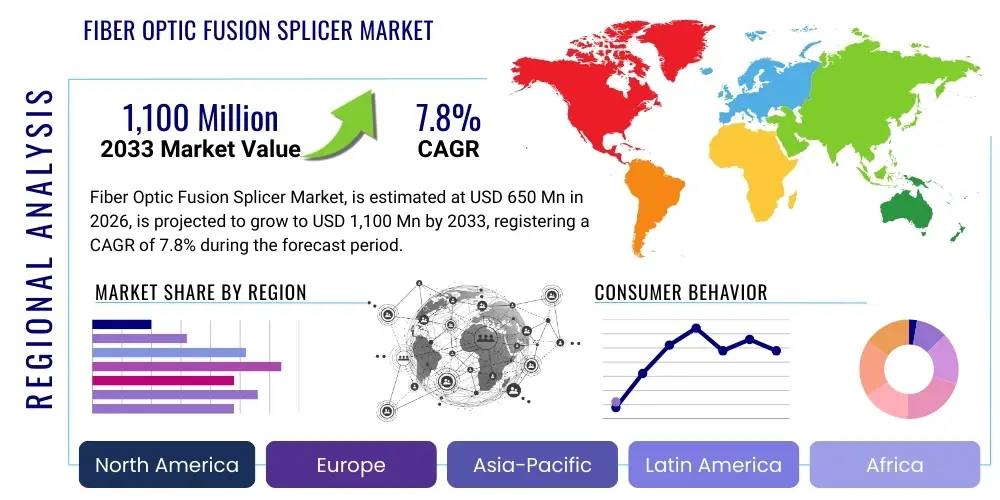

The Fiber Optic Fusion Splicer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 650 Million in 2026 and is projected to reach USD 1,100 Million by the end of the forecast period in 2033.

The Fiber Optic Fusion Splicer Market encompasses advanced electronic devices used to permanently join two optical fibers end-to-end, creating a seamless, low-loss connection that facilitates high-speed data transmission. These devices operate by utilizing an electric arc to melt and fuse the glass ends together, ensuring minimal light signal reflection and attenuation. Fusion splicing is recognized as the standard technique for establishing reliable, long-distance, and high-bandwidth optical networks, making the splicer an indispensable tool in modern telecommunication infrastructure deployment, maintenance, and upgrade cycles globally.

The primary applications driving the demand for fusion splicers include the proliferation of 5G networks, expansion of Fiber to the Home (FTTH) infrastructure, establishment of hyperscale data centers requiring complex internal optical connectivity, and ongoing submarine cable projects. Fusion splicers offer unparalleled benefits, such as extremely low splice loss (typically below 0.02 dB), high mechanical strength, and long-term stability, which are critical for meeting the Quality of Service (QoS) demands of modern bandwidth-intensive applications. Furthermore, the evolution of splicer technology towards ruggedized, highly automated, and compact designs has broadened their applicability across various challenging field environments.

Key driving factors accelerating market growth involve massive governmental and private investments in digital infrastructure worldwide, particularly across emerging economies seeking universal broadband access. The transition from legacy copper infrastructure to fiber optics is a global trend, necessitating continuous procurement of high-precision splicing equipment. Technological advancements, such as automatic core-to-core alignment systems, faster splicing cycles, and enhanced battery life, contribute significantly to operational efficiency, further solidifying the market's trajectory towards robust expansion throughout the forecast period.

The global Fiber Optic Fusion Splicer Market is experiencing robust growth driven predominantly by aggressive 5G infrastructure deployment and the pervasive rollout of FTTH networks, particularly in the Asia Pacific region. Business trends indicate a shift towards high-precision core alignment splicers, demanded by hyperscale data centers and demanding telecommunication backbones requiring ultra-low signal loss. Key manufacturers are focusing heavily on developing intelligent, cloud-connected splicers featuring predictive maintenance capabilities and enhanced automation to improve field technician efficiency and reduce operational expenditure (OPEX) for network operators.

Regionally, the Asia Pacific (APAC) stands out as the dominant growth engine, fueled by vast infrastructure projects in China, India, and Southeast Asia aimed at achieving national digital transformation goals. North America and Europe maintain strong demand, characterized by continuous network upgrades, migration to higher fiber count ribbon cables, and significant investment in underwater cable maintenance fleets. Segment trends reveal that the Core Alignment splicer segment retains market leadership due to its superior precision, although the cladding alignment segment remains crucial for cost-sensitive short-haul installations and quick repair operations in less critical environments.

Overall, the market landscape is moderately competitive, with established Japanese and US manufacturers competing against increasingly sophisticated Asian players who offer competitive pricing models and feature-rich devices. Strategic emphasis is placed on innovation in mass fusion capabilities and the integration of Internet of Things (IoT) connectivity into splicers for real-time monitoring of splicing parameters and performance analytics. This strategic focus ensures that the market remains aligned with the exponential increase in global data traffic requirements and the associated need for flawless optical connectivity solutions.

Common user questions regarding AI’s impact on the Fiber Optic Fusion Splicer Market center on automation improvements, predictive maintenance of equipment, and enhanced splice loss estimation accuracy. Users frequently inquire about how AI algorithms can optimize arc discharge settings dynamically based on fiber type, environmental conditions (like temperature and humidity), and fiber end-face quality, thereby minimizing technician intervention and increasing first-time splice success rates. Furthermore, interest lies in leveraging machine learning to analyze vast datasets of splicing records to identify recurrent issues or suboptimal performance trends across a network, facilitating proactive equipment calibration and training module refinement.

The integration of Artificial Intelligence and Machine Learning (AI/ML) is fundamentally transforming the operational paradigm of fiber optic fusion splicing, moving the process beyond mere automation toward true intelligence. AI enables real-time, adaptive control over complex physical processes within the splicer, such as optimizing electrode wear compensation and automatically identifying unique fiber profiles, which is crucial for handling mixed network environments containing diverse fiber types (e.g., G.652, G.655, G.657). This sophisticated level of process control ensures consistent, laboratory-grade splice quality even when performed by less-experienced field personnel under challenging conditions, significantly reducing rework rates and associated costs.

Moreover, AI contributes significantly to the maintenance and logistical management of the splicer fleet. By analyzing usage patterns, component performance (like motor alignment reliability or cleaver blade degradation), and environmental stress factors, AI-driven predictive maintenance systems can accurately forecast potential equipment failures. This capability allows service providers to schedule proactive maintenance or calibration before a catastrophic failure occurs in the field, maximizing equipment uptime, improving service reliability, and streamlining inventory management of crucial spare parts like electrodes and cleaver blades. This transition toward smart, self-optimizing splicing tools represents the future operational standard for large-scale fiber deployments.

The Fiber Optic Fusion Splicer Market is propelled by the global imperative for ultra-high-speed connectivity, countered by high initial investment costs and reliance on highly trained technicians. The principal drivers include the pervasive deployment of 5G infrastructure, exponential growth in data consumption demanding faster backbones, and governmental initiatives supporting universal fiber broadband access. Restraints largely center around the significant capital expenditure required for high-precision core alignment machines and the recurring need for meticulous calibration and maintenance, often requiring specialized vendor expertise. Opportunities lie in expanding into niche applications like specialized aerospace and defense communications, developing highly durable, cost-effective mid-range splicers for emerging markets, and integrating AI/IoT features to enhance remote diagnostics and operational efficiency. The confluence of these forces dictates market trajectory, strongly favoring innovative and user-friendly splicing solutions that can meet mass deployment requirements.

Key drivers are deeply intertwined with technological evolution in related fields. For example, the increasing adoption of high-density fiber cables (e.g., 200/400/600 micron fiber count cables) used in data center interconnects and dense urban environments necessitates highly efficient mass fusion splicers, which can simultaneously fuse 8, 12, or even 16 fibers. This technological necessity directly stimulates market demand for advanced, multi-fiber capable equipment. Furthermore, the commitment of major telecommunication companies to phasing out legacy networks and migrating all services—voice, video, and data—onto unified fiber platforms acts as a consistent, long-term demand stabilizer for high-quality splicing tools across all geographic regions.

Conversely, market restraints present persistent challenges. Beyond the high capital cost, the market faces constraints related to the sensitive nature of the equipment; fusion splicers require a clean environment and careful handling, making field operations in harsh climates challenging. Regulatory hurdles and standardization challenges, particularly concerning the interoperability of specialty fibers and the subsequent need for specialized splicing recipes, can occasionally slow adoption rates. However, the opportunity landscape, particularly in developing robust, ruggedized equipment tailored for rapid deployment in last-mile FTTH projects and remote industrial settings, offers substantial potential for market participants seeking competitive differentiation through specialization and durability.

The Fiber Optic Fusion Splicer Market is systematically segmented based on technology type, application, and end-user, allowing for precise market analysis and strategic targeting. The technology segmentation differentiates between high-precision Core Alignment splicers, which use advanced profile detection and movement systems for optimal performance, and cost-effective Cladding Alignment splicers, which prioritize speed and ease of use in environments where slightly higher splice loss is tolerable. Application segmentation highlights the diverse utilization spectrum, ranging from demanding long-haul telecommunication backbones to localized industrial control networks and tactical military communication systems. End-user categorization distinguishes demand patterns between large service providers (telcos), enterprise networks, and governmental entities, revealing varying preferences regarding automation levels, ruggedness, and splicing speed requirements.

The Core Alignment segment generally commands the highest revenue share globally due to the increasing requirement for ultra-low loss connections in 400G and 800G optical networks, where cumulative attenuation must be rigorously managed to maintain link integrity and performance margin. Manufacturers in this segment focus on enhancing features like automatic fiber identification, precise magnification systems, and environmental compensation capabilities. Meanwhile, the Telecommunication & Data Communication application segment remains the undisputed leader in market size, directly benefiting from massive global investments in 5G transmission infrastructure, metropolitan area networks (MANs), and expansive international undersea cable systems. The need for reliable, high-volume splicing within these sectors solidifies their demand dominance.

Geographical segmentation reveals that APAC continues to be the most lucrative market, driven by accelerated urbanization and government mandates promoting digital inclusion. Key players strategically localize manufacturing and distribution in this region to benefit from lower operational costs and better access high-volume demand from large-scale FTTH deployments. The ongoing trend toward automation and miniaturization across all segments suggests future market growth will be heavily concentrated in devices offering superior portability, faster cycle times, and robust data management features, directly catering to the field technician's need for efficiency and ease of compliance reporting.

The value chain for the Fiber Optic Fusion Splicer Market begins with upstream activities focused on securing high-precision electronic components, micro-optics, specialized motors, and advanced software necessary for controlling the highly sensitive arc-fusion process. Key suppliers provide crucial items like electrode assemblies, V-groove ceramics, and highly specialized image processing sensors essential for fiber alignment. Manufacturing and assembly involve meticulous calibration and quality control, as the performance of the final product—measured by splice loss and reliability—is extremely sensitive to minute tolerances. Manufacturers must invest heavily in R&D to maintain technological parity, focusing on optimizing arc discharge algorithms and enhancing battery life for portability.

Midstream activities involve sophisticated distribution channels. Direct channels are often preferred by major manufacturers when dealing with Tier 1 telecommunication companies and defense entities, facilitating complex equipment training, specialized technical support, and negotiated bulk purchases. Indirect distribution, leveraging regional distributors, resellers, and systems integrators, is vital for reaching smaller installation contractors, utility companies, and educational institutions globally. These intermediaries are critical for providing localized sales support, equipment rental services, and rapid field calibration services, particularly in geographically dispersed markets.

Downstream analysis focuses heavily on the end-user interaction, encompassing installation, operation, and maintenance. Due to the high investment and precision of fusion splicers, post-sales support, calibration services, and comprehensive training are critical components of the value proposition. The market is increasingly influenced by the "total cost of ownership" (TCO), where the longevity, ease of maintenance (e.g., field-replaceable electrodes), and availability of local service centers often outweigh marginal differences in initial purchase price. The robustness of the service network is a key competitive differentiator, particularly for high-volume service providers operating across large geographic areas.

Potential customers for Fiber Optic Fusion Splicers are predominantly entities involved in the deployment, maintenance, and upgrade of optical fiber networks across varying scales and complexity levels. The largest segment comprises Telecommunication Service Providers—including fixed-line carriers, mobile network operators (MNOs), and internet service providers (ISPs)—who rely on splicers daily for connecting central offices, deploying FTTH lines, and maintaining their extensive backbone infrastructure. These buyers prioritize core alignment technology, high throughput (speed), automated features, and extensive technical support warranties due to their mission-critical applications.

Another major customer group consists of hyperscale Data Center Operators and Enterprise Network Managers. For these customers, fusion splicers are essential for creating the internal fiber spine interconnecting servers and storage area networks (SANs) where extremely high data rates (400G+) necessitate near-zero splice loss. The focus here is often on mass fusion splicing capabilities to handle ribbon fiber efficiently, minimizing installation time for massive infrastructure projects. Reliability and integration with network management systems are key buying criteria for this sophisticated clientele.

Niche but high-value customers include governmental defense organizations and specialized utility companies (power grids, oil and gas pipelines). Defense customers require ruggedized, tactical splicers capable of operating reliably under extreme environmental conditions for temporary and permanent field communication links. Utility companies use splicers for connecting proprietary Supervisory Control and Data Acquisition (SCADA) systems and fiber sensors along vast infrastructure networks, demanding high durability and resistance to electromagnetic interference. These end-users often seek specific, customized splicing solutions that meet stringent industry or military standards.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650 Million |

| Market Forecast in 2033 | USD 1,100 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Fujikura Ltd., Sumitomo Electric Lightwave Corp., Furukawa Electric Co., Ltd. (Fitel), INNO Instrument Inc., AFL (America Fujikura Ltd.), Jiangsu Jilong Optical Communication Co., Ltd., Shenzhen Ruiyan Communication Equipment Co., Ltd. (Signal Fire), Darkhorse Technologies, Comway, Ilsintech Co., Ltd., Techwin Co., Ltd., ShinewayTech, 3M, CKT Technology, Ruidian Communication. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Fiber Optic Fusion Splicer Market is dominated by advancements aimed at increasing speed, precision, and automation while reducing the overall size and power consumption of the equipment. Modern splicers employ sophisticated Profile Alignment System (PAS) technology, which utilizes highly sensitive cameras and image processing software to precisely align the fiber cores before fusion, minimizing splice loss to levels often below the theoretical limit of the fiber itself. A significant innovation is the refinement of arc discharge control mechanisms, which dynamically adjust the arc temperature and duration based on real-time feedback regarding fiber material and atmospheric conditions, enhancing consistency in various field environments.

The shift towards specialized splicing techniques is also prominent, particularly the widespread adoption of Mass Fusion Splicing for ribbon fiber cables, which is essential for hyperscale data centers and high-density FTTx backbones. These advanced machines feature highly accurate V-grooves and optimized heating ovens for simultaneous fusion and protection of multiple fibers (typically 4, 8, or 12 fibers). Furthermore, manufacturers are incorporating Internet of Things (IoT) connectivity into splicers, enabling remote software updates, cloud-based data backup of splice reports, and integration with broader inventory and workforce management systems. This connectivity is vital for large telecommunication companies managing dispersed assets and ensuring regulatory compliance.

Emerging technologies focus on enhancing durability and user interface. Ruggedization techniques ensure the equipment can withstand dust, moisture, and vibration, expanding applicability in demanding outdoor and industrial settings. Advancements in battery technology, offering extended operational life, and highly intuitive Graphical User Interfaces (GUIs) are simplifying operation for less experienced technicians. Additionally, manufacturers are heavily researching alternative splicing methods and improved fiber cleaving technologies, such as plasma cutting, to further reduce physical preparation steps and improve the yield of successful, low-loss splices, cementing the market’s trajectory toward self-sufficient, highly intelligent splicing units.

The global Fiber Optic Fusion Splicer Market exhibits distinct regional dynamics driven by varying levels of digital infrastructure maturity, governmental investment policies, and population density demanding high-speed connectivity. Asia Pacific (APAC) currently holds the dominant position in terms of market volume and growth rate. This leadership is primarily attributed to monumental governmental investment in national broadband programs, particularly in China and India, aiming to expand Fiber-to-the-Home (FTTH) infrastructure across vast rural and urban landscapes. The rapid rollout of 5G networks in countries like South Korea, Japan, and the ASEAN nations further necessitates continuous deployment and maintenance of fiber backbones, creating sustained high demand for both core and cladding alignment splicers.

North America and Europe represent mature, high-value markets characterized by demand for sophisticated, high-precision Core Alignment and Mass Fusion Splicers, driven by ongoing network upgrades (e.g., replacement of older GPON networks with XGS-PON) and the continuous expansion of hyperscale and edge data centers. These regions emphasize quality, ruggedness, and advanced data reporting capabilities. While the volume growth may be slower compared to APAC, the Average Selling Price (ASP) of fusion splicers remains high, reflecting the preference for premium brands and advanced technological features essential for handling complex, high-fiber count cables and specialized applications.

Latin America, the Middle East, and Africa (MEA) are emerging as high-potential growth territories. Latin American nations are accelerating their fiber deployments to meet rising consumer demand for faster internet, spurred by competitive local loop unbundling policies. The Middle East benefits from state-led digital transformation initiatives and smart city projects, leading to substantial investment in ultra-modern fiber infrastructure requiring precision equipment. Africa's market growth, while currently lower in volume, is accelerating due to international aid and private sector investment focusing on backbone connectivity and connecting underserved populations, primarily favoring durable, user-friendly, and cost-effective cladding alignment models for initial deployments.

Core alignment splicers, utilizing Profile Alignment Systems (PAS), precisely align the actual fiber cores using advanced optics and motorized movements, resulting in ultra-low splice loss (typically 0.02 dB or less). Cladding alignment splicers align the fibers based on their outer diameter (cladding), offering faster splicing and lower cost, but generally yielding slightly higher splice losses, making them suitable for FTTX last-mile and less critical installations.

5G expansion fundamentally requires dense fiber optic backhaul infrastructure to support high-bandwidth small cells and massive MIMO arrays. This necessitates high-volume fiber deployment and maintenance, directly increasing demand for automated, high-speed, and reliable fusion splicers capable of handling ribbon fibers and ensuring the stringent low-loss connections required for modern high-frequency radio architectures.

The Total Cost of Ownership (TCO) includes the high initial capital cost of the unit, periodic calibration fees (usually annually), and recurring consumables such as replacement electrodes (which degrade over several thousand splices) and cleaver blades. Proper maintenance and regular calibration are essential to preserving low splice loss performance and maximizing the equipment's lifespan.

The Asia Pacific (APAC) region, driven by extensive governmental and private investments in Fiber-to-the-Home (FTTH) and 5G rollout initiatives across China, India, and Southeast Asia, is currently the fastest-growing and largest market for fusion splicers in terms of unit volume.

Mass fusion splicers are essential for applications involving high-count ribbon fiber cables (8 to 12 fibers fused simultaneously), commonly used in data center interconnects, major backbone routes, and dense urban metropolitan networks. For standard single-fiber connections or simple repairs (patch cables, drops), single-fiber core alignment splicers are typically sufficient and more practical.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.