ID : MRU_ 437008 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

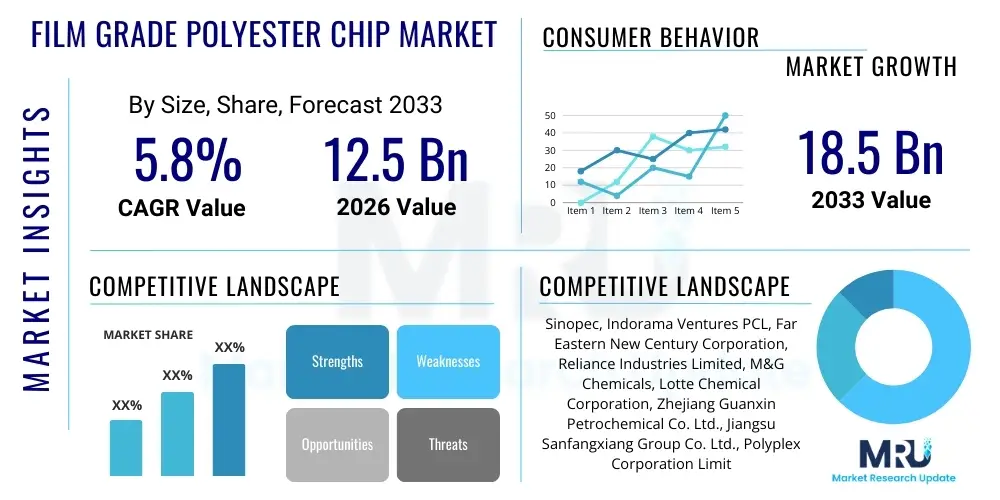

The Film Grade Polyester Chip Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 12.5 Billion in 2026 and is projected to reach USD 18.5 Billion by the end of the forecast period in 2033.

Film Grade Polyester Chip, predominantly Polyethylene Terephthalate (PET) resin, is a high-purity polymer specifically engineered for producing various types of polyester films, including biaxially oriented polyethylene terephthalate (BoPET) films. These chips are characterized by extremely low impurity levels, consistent intrinsic viscosity (IV), and superior thermal stability, which are critical parameters for achieving thin, strong, and highly transparent films necessary for demanding applications. The material’s excellent mechanical strength, chemical resistance, and barrier properties make it indispensable across multiple high-value industries.

The primary applications of film grade polyester chips span consumer packaging, electrical insulation, graphic arts, and specialized industrial uses like solar panel backsheets and flexible electronics. In the packaging sector, BoPET films derived from these chips are favored for their durability and gas barrier properties, extending the shelf life of food products and ensuring product integrity. Furthermore, the rising demand for flexible packaging solutions driven by the growth of e-commerce platforms and urbanization significantly contributes to the consumption volume of these specialized chips globally.

Key driving factors for market expansion include the continuous technological advancements in film manufacturing processes, enabling the production of thinner films without compromising performance, thereby optimizing material usage. The increasing global focus on sustainable packaging solutions is also propelling demand for film grade chips that are compatible with recycling streams or are manufactured using bio-based feedstocks. The benefits of using high-quality polyester films, such as superior printability, high tensile strength, and excellent dimensional stability across varying temperatures, cement the market's trajectory towards robust growth, especially in emerging economies where industrialization and consumer spending are rapidly increasing.

The global market for Film Grade Polyester Chips is currently undergoing significant transformation, primarily driven by robust demand from the Asia Pacific region, which serves as both the largest producer and consumer base due to entrenched downstream manufacturing capabilities, particularly in electronics and flexible packaging. Business trends indicate a strong focus on enhancing sustainability, with major manufacturers investing heavily in chemical recycling technologies and facilities dedicated to producing recycled PET (rPET) chips suitable for high-performance film applications, meeting stringent regulatory demands from key markets like the European Union.

Regional trends highlight that while APAC maintains dominance, North America and Europe are exhibiting high-value growth driven by the shift towards specialty films, such as those used in advanced display technologies (OLED/QLED) and high-barrier food packaging required by modern retail logistics. These developed regions demand premium chips with ultra-high purity and specific intrinsic viscosities, pushing manufacturers towards advanced polymerization techniques like Solid State Polymerization (SSP) to ensure quality consistency and compliance with safety standards, particularly concerning food contact materials.

Segmentation trends reveal that the manufacturing process segment focusing on high-speed continuous polymerization is gaining traction due to efficiency benefits and scale. In terms of application, the electrical and electronic segment is witnessing exponential growth, fueled by the accelerating production of capacitors, insulation tapes, and flexible printed circuits, all of which rely on the dielectric properties and dimensional stability of high-quality polyester film. Overall, the market remains highly competitive, with established integrated petrochemical producers leveraging economies of scale and geographic presence to maintain leadership, while smaller specialized firms focus on niche high-performance grades.

User inquiries regarding AI's impact on the Film Grade Polyester Chip Market frequently center on how artificial intelligence can address core industry challenges: quality variability, optimization of complex polymerization reactions, and prediction of raw material price volatility. Users are keen to understand if AI can significantly reduce batch-to-batch inconsistency, which is crucial for film production purity. There is also substantial interest in AI-driven predictive maintenance for massive polymerization reactors, aiming to minimize costly unplanned downtime and maintain the continuous, high-volume production necessary to meet global demand.

The implementation of machine learning algorithms is profoundly affecting the supply chain and manufacturing efficiency of film grade chips. AI systems are increasingly being utilized to analyze massive datasets related to reactor temperature, pressure, and catalyst dosage in real-time. This real-time analysis allows for minute adjustments to polymerization conditions, leading to optimized reaction kinetics, maximized yield, and, most importantly, enhanced consistency in the final chip properties, such as molecular weight distribution and intrinsic viscosity, directly benefiting the film extrusion process downstream.

Furthermore, AI plays a pivotal role in advanced material inspection and quality control. Traditional methods involve periodic sampling, but AI-powered visual inspection systems, coupled with sensors, can instantaneously detect micro-impurities, gels, and contaminants within the polymer melt or the final chip pellets. This capability ensures that only the highest purity material reaches specialized applications like capacitor films, where even minor defects can lead to product failure. Simultaneously, AI models are aiding procurement by forecasting PTA and MEG price fluctuations, allowing manufacturers to optimize inventory holding and purchasing strategies.

The dynamics of the Film Grade Polyester Chip Market are governed by a complex interplay of internal market demands and external geopolitical and environmental pressures. Key drivers include the relentless global expansion of flexible packaging, fueled by shifting consumer preferences towards convenience, portability, and reduced food waste. Additionally, the proliferation of consumer electronics and electric vehicles necessitates high-performance insulating films, bolstering demand for specific, high-purity chip grades. However, these positive trends are counterbalanced by significant restraints, primarily the extreme price volatility of upstream petrochemical feedstocks, Purified Terephthalic Acid (PTA) and Monoethylene Glycol (MEG), which directly impacts manufacturing costs and profit margins across the value chain. Environmental regulations are acting as both a driver and a restraint, pushing the industry towards sustainability while simultaneously increasing compliance costs.

Opportunities in the market center around the integration of chemically and mechanically recycled PET (rPET) into film applications, allowing manufacturers to capitalize on circular economy initiatives and meet growing brand owner commitments for recycled content. Developing specialized chip grades that offer enhanced barrier properties (oxygen and moisture) and thermal resistance opens new revenue streams, particularly in demanding industrial and medical packaging sectors. Furthermore, geographical diversification of manufacturing capacity, moving beyond the current concentration in Northeast Asia, presents an opportunity to de-risk supply chains and establish regional production hubs closer to major end-use markets, thereby mitigating logistics costs and lead times, though this requires substantial capital expenditure.

The primary impact forces influencing market growth include rapid urbanization in developing regions, which escalates demand for packaged goods, and technological advancements in thin film processing, requiring chips with even higher consistency and lower melt viscosity. Legislative forces, such as bans on single-use plastics and Extended Producer Responsibility (EPR) schemes, are fundamentally reshaping the material sourcing strategies of major film producers. The combined effect of these forces suggests a sustained increase in demand, particularly for premium and sustainable grades, but also points towards significant competitive pressure on pricing and operational efficiency, necessitating continuous process innovation and vertical integration to maintain profitability and market share.

The Film Grade Polyester Chip Market is meticulously segmented based on composition, end-use application, and manufacturing process, allowing suppliers to target specific industry needs with customized products. Segmentation by composition primarily distinguishes between conventional PET chips and co-polyester variations (like PETG or PCTA), which are utilized for specific performance requirements such as lower processing temperature or enhanced clarity. The market structure reflects a tendency towards specialization, where high-volume, standard chips service the general packaging market, while specialty, low-volume chips cater to sensitive applications like medical devices and high-end electronics.

The value chain for the Film Grade Polyester Chip market begins upstream with the procurement of critical raw materials: Purified Terephthalic Acid (PTA) and Monoethylene Glycol (MEG), derived predominantly from crude oil and natural gas. This upstream segment is highly concentrated, involving major petrochemical giants, and heavily influences the final cost structure of the chips. Manufacturers of film grade polyester chips focus on the crucial polymerization and polycondensation stages, often incorporating Solid State Polymerization (SSP) to achieve the necessary high molecular weight and superior intrinsic viscosity required for high-performance film extrusion. The efficiency and energy consumption at this manufacturing stage are vital for determining competitive pricing.

The midstream involves the distribution and logistics of the polyester chips. Distribution channels are varied, including direct sales from large, integrated producers to massive film manufacturers, and sales through regional distributors who manage inventory and specialized smaller orders. Given the bulk nature of the chips and the global nature of the market, robust logistics networks, often involving bulk shipping containers and specialized handling to prevent contamination, are essential. Direct distribution often allows for closer technical collaboration between the chip producer and the film extruder, optimizing the chip specifications for specific downstream machinery and end products.

The downstream segment consists of the film manufacturers (extruders) who convert the chips into biaxially oriented films (BoPET) using processes like stretching and thermal setting. These films are then sold to converters, who process them further into final products such as flexible packaging, metallized films, or electrical insulation tapes. The market is increasingly characterized by demanding end-users who require chips with highly consistent properties, as film quality is directly proportional to the chip quality. Therefore, successful companies in the value chain establish strong, long-term relationships with key downstream players to ensure material specifications meet rigorous application standards, cementing the importance of quality control throughout the entire chain.

The primary customers for Film Grade Polyester Chips are large-scale manufacturers operating high-speed film extrusion lines, specifically those specializing in biaxially oriented films. These customers fall mainly into three high-consumption sectors: the packaging industry, manufacturers of specialized industrial films, and the electrical and electronics sector. Within the packaging domain, major converters and brand owners require chips that ensure optimal clarity, printability, and robust barrier properties for food safety and shelf-life extension. Consistency and compliance with food contact regulations are paramount for these buyers.

Another major customer base includes companies producing high-performance functional films used in industrial and specialized applications. This includes manufacturers of solar photovoltaic backsheets, which require chips with exceptional UV resistance and thermal stability, as well as producers of release liners and thermal transfer ribbons. These technical buyers are less sensitive to minor price fluctuations but place a significantly higher premium on technical specifications, batch uniformity, and consistent supply, often leading to long-term supply contracts based on tailored chip formulations.

The electrical and electronics industry represents the third critical customer segment, demanding ultra-pure, high-dielectric strength chips for manufacturing capacitor films, insulation tapes, and flexible circuit substrates. Customers in this space, such as passive component manufacturers and electronics assemblers, require the highest level of cleanliness and purity in the chips, as any contamination can compromise the dielectric properties essential for device performance. Their purchasing decisions are driven by rigorous certification standards, low defect rates, and the ability of the chip supplier to consistently deliver narrow-specification materials critical for miniaturized and high-voltage applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 18.5 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sinopec, Indorama Ventures PCL, Far Eastern New Century Corporation, Reliance Industries Limited, M&G Chemicals, Lotte Chemical Corporation, Zhejiang Guanxin Petrochemical Co. Ltd., Jiangsu Sanfangxiang Group Co. Ltd., Polyplex Corporation Limited, Nan Ya Plastics Corporation, Alpek S.A.B. de C.V., JBF Industries Ltd., OCTAL, DAK Americas, Thai Polyester Co. Ltd., Sanwa Chemical Industry Co. Ltd., Toray Industries Inc., Kolon Industries Inc., SK Chemical Co. Ltd., Teijin Limited. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing of high-quality Film Grade Polyester Chips relies heavily on sophisticated polymerization technologies designed to ensure maximum purity, optimal molecular weight, and narrow molecular weight distribution. Continuous Polycondensation is the standard industrial process, offering high throughput and economies of scale. However, for specialized film applications demanding superior physical properties, the core technical innovation lies in the integration of Solid State Polymerization (SSP). SSP is a secondary process where already polymerized chips are heated under vacuum or inert gas below the melting point. This step increases the intrinsic viscosity (IV) to levels required for robust film extrusion, minimizes acetaldehyde content, and further reduces volatile contaminants, which is crucial for food contact and electronic films.

Furthermore, advanced filtration techniques and melt pumps are indispensable elements within the technology landscape. High-precision melt filtration systems, often employing sophisticated sintered metal filters, are utilized immediately before the chips are pelletized. These systems remove microscopic impurities, catalyst residues, and insoluble gels that could otherwise cause pinholes or defects in the ultra-thin films. Achieving filter efficiency down to the micron level is mandatory for producing chips suitable for optical and capacitor film grades. The design of the polymerization reactor itself, specifically continuous stir-tank reactors and horizontal reactors, is optimized to achieve excellent mixing and heat transfer, minimizing thermal degradation.

The latest technological trend focuses on incorporating chemical recycling methods (e.g., depolymerization) to feed purified monomers back into the polycondensation process, allowing for the creation of truly circular rPET chips that maintain virgin-like quality. Manufacturers are also implementing advanced process control systems, leveraging data analytics and high-fidelity sensors to monitor reaction parameters in real-time. This level of technical control ensures batch-to-batch consistency and facilitates rapid transitions between different product grades, thereby improving overall operational flexibility and reducing material waste, solidifying the market's trajectory towards precision manufacturing.

Film Grade chips require higher intrinsic viscosity (IV) and exceptional purity with minimal acetaldehyde (AA) and trace metals to ensure high tensile strength and optical clarity necessary for thin film extrusion. Bottle Grade chips prioritize low AA content for beverage safety but typically have a slightly lower IV requirement compared to film grades.

The Packaging Film segment, specifically flexible food and non-food packaging, currently accounts for the largest share of the market volume due to continuous demand for extended shelf life and convenience. However, the Electrical and Electronic segment is demonstrating the highest growth rate due to requirements for high-performance dielectric films.

Volatility in PTA and MEG prices, linked to crude oil markets, is managed through hedging strategies, establishing long-term supply contracts, and optimizing operational efficiencies (e.g., reducing energy consumption through advanced catalysts) to maintain competitive pricing and stable profit margins.

Solid State Polymerization (SSP) is the critical post-polymerization process used to increase the molecular weight and intrinsic viscosity of the chips to the precise level required for ultra-thin, high-strength specialty films like capacitor films, ensuring superior physical properties and purity.

Sustainability is a core growth driver, with mandatory recycled content goals and consumer preferences pushing manufacturers to adopt mechanical and chemical recycling technologies. The future market growth is highly dependent on the successful, scalable integration of high-quality recycled PET (rPET) chips suitable for demanding film applications.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.