ID : MRU_ 435106 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

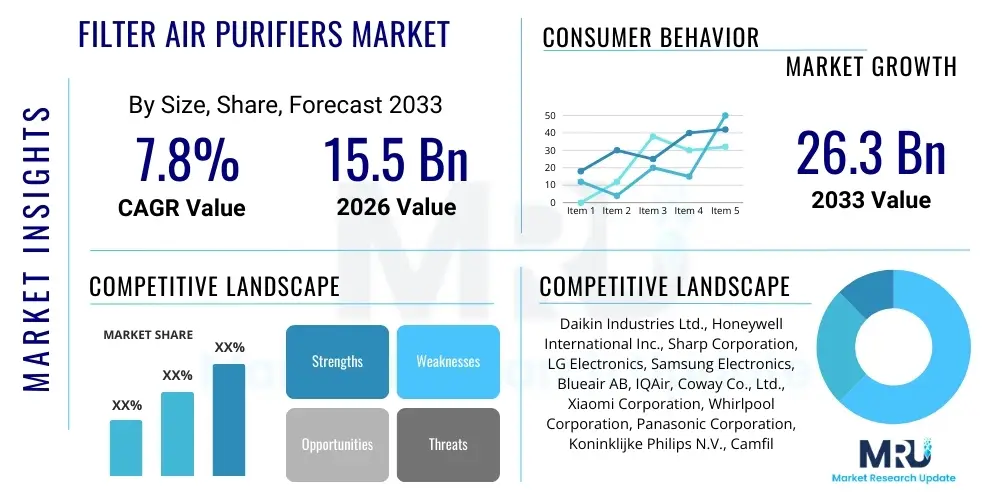

The Filter Air Purifiers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 15.5 Billion in 2026 and is projected to reach USD 26.3 Billion by the end of the forecast period in 2033.

The Filter Air Purifiers Market encompasses devices designed to remove contaminants, pollutants, and allergens from the air within enclosed spaces through the use of mechanical and chemical filtration media. These systems operate by drawing in ambient air, passing it through various layers of filters—such as High-Efficiency Particulate Air (HEPA) filters, activated carbon filters, and pre-filters—to capture particles ranging from dust and pet dander to volatile organic compounds (VOCs) and smoke. The primary product offering includes standalone units for residential use, commercial-grade systems for offices and retail environments, and high-capacity industrial units for manufacturing and cleanroom applications. Filter-based purification remains the dominant technology due to its proven efficacy and reliability in capturing a broad spectrum of airborne contaminants, making it a critical component of indoor air quality (IAQ) management.

Major applications of filter air purifiers span health and comfort environments, driven by rising public awareness concerning the detrimental effects of both outdoor pollution infiltration and indoor sources like mold, chemicals, and cooking fumes. Residential adoption is accelerating due to the increased prevalence of respiratory allergies and asthma, particularly in urban areas experiencing poor air quality. Commercial applications include hospitals, schools, hotels, and corporate offices, where maintaining a healthy environment is paramount for employee productivity and customer well-being. The inherent benefits of filter air purifiers include reduced respiratory illness incidence, odor removal, and the creation of healthier living and working spaces, contributing significantly to improved quality of life.

The market is fundamentally driven by several macro-environmental factors, chief among them the escalating levels of global air pollution, especially in rapidly industrializing economies in the Asia Pacific region. Furthermore, stringent regulatory standards imposed by governmental bodies on IAQ, coupled with technological advancements leading to smart, energy-efficient, and aesthetically appealing devices, fuel consumer uptake. The COVID-19 pandemic also served as a catalyst, permanently shifting consumer perceptions toward the importance of air sanitation, thereby solidifying the air purifier as a standard household and commercial appliance rather than a niche health product. Continuous innovation in filter media and integration with smart home ecosystems are key factors propelling sustained market expansion throughout the forecast period.

The Filter Air Purifiers Market is characterized by robust growth, largely fueled by persistent global air quality crises and heightened consumer health consciousness following global health events. Key business trends indicate a strong move toward product digitalization, with manufacturers integrating IoT capabilities, AI-driven sensor technology, and mobile connectivity to offer proactive monitoring and automated purification adjustments. This integration is boosting premium segment growth and fostering brand loyalty. Furthermore, sustainability is emerging as a critical competitive factor; companies are focusing on developing long-lasting, recyclable filter materials and energy-efficient motors to address environmental concerns and meet consumer demand for eco-friendly appliances. Supply chain resilience, particularly concerning the sourcing of specialized filter media like advanced HEPA material, remains a strategic focus for major market players to mitigate geopolitical risks and ensure stable production.

Regionally, the Asia Pacific (APAC) market maintains its dominance, driven by dense populations, rapid urbanization, and severe air pollution issues in countries such as China and India, making air purification a necessity rather than a luxury. However, North America and Europe demonstrate significant growth in the premium and smart segments, benefiting from high disposable incomes and high penetration of smart home technologies. European markets, in particular, are focusing on energy efficiency standards and advanced filtration capabilities targeting indoor chemical contaminants and allergens. The Middle East and Africa (MEA) and Latin America represent emerging opportunities, spurred by infrastructure development and increasing awareness campaigns regarding IAQ, though market penetration rates remain comparatively lower, offering substantial room for future expansion.

Segment trends reveal that the HEPA filter category continues to hold the largest market share due to its scientifically proven effectiveness against fine particulate matter (PM2.5 and PM10), which are major components of smog and urban pollution. Within applications, the residential segment accounts for the largest volume, benefiting from high unit sales and the trend toward multi-unit deployment per household. However, the commercial segment, particularly healthcare and educational facilities, is expected to exhibit the fastest growth rate, driven by institutional spending aimed at creating safer environments post-pandemic. The shift in distribution channels emphasizes the rapid expansion of online retail, which provides consumers with detailed product comparisons, easy access, and competitive pricing, complementing the traditional role of specialized retail stores in consumer education.

User queries regarding the intersection of AI and Filter Air Purifiers primarily revolve around device autonomy, personalization of filtration, and predictive maintenance. Consumers frequently ask: "How does AI make air purifiers smarter?" "Can AI optimize filtration based on real-time pollution data?" and "Will AI integration reduce filter replacement costs?" The core themes center on expectations for air purifiers to transition from reactive devices to proactive, intelligent air management systems. Users anticipate AI will enable precise particulate and contaminant identification, leading to tailored filtration schedules, enhanced energy efficiency by avoiding unnecessary high-power operation, and timely, automated alerts for filter replacement based on actual usage and degradation, rather than fixed time intervals. The consensus suggests AI is viewed as the necessary evolution to unlock true performance optimization and convenience in IAQ management.

The integration of Artificial Intelligence transforms traditional filter air purifiers into sophisticated, responsive environmental control hubs. AI algorithms process data streams from multi-sensor arrays (detecting PM, VOCs, humidity, and temperature) and external sources (local air quality index, weather patterns). This enables the device to predict upcoming air quality degradation—such as pollution spikes during rush hour or increased indoor VOCs during cooking—and automatically pre-emptively adjust fan speed and filtration intensity. Furthermore, machine learning models analyze user habits and historical indoor air patterns to create personalized purification profiles, ensuring optimal air quality maintenance with minimal manual intervention. This level of predictive maintenance significantly extends filter lifespan and maximizes energy efficiency, addressing key consumer concerns about operational cost and device intelligence.

Consequently, the application of AI is driving the next wave of product differentiation. Leading manufacturers are embedding neural networks locally within the devices (edge computing) to ensure quick decision-making without constant cloud connectivity, enhancing data privacy and operational reliability. AI also facilitates seamless integration into wider smart home ecosystems, allowing air purifiers to collaborate with HVAC systems and smart vents for holistic environmental management. This sophistication elevates the value proposition of filter air purifiers, moving them beyond simple mechanical appliances to essential, intelligent components of modern, healthy living infrastructure, thereby increasing market valuation and expanding the target demographic to include technology enthusiasts.

The Filter Air Purifiers Market is significantly influenced by a dynamic interplay of Drivers, Restraints, and Opportunities, which collectively determine the market trajectory and competitive landscape. The primary Drivers, such as worsening global air quality and heightened consumer health awareness, create continuous demand across residential and commercial sectors. However, the market faces structural Restraints, notably the high initial cost of premium filtration units and the recurring expense associated with proprietary filter replacements, which can deter price-sensitive consumers. Opportunities lie primarily in technological advancements, including the development of advanced photocatalytic oxidation (PCO) hybrid systems and filters with longer lifespans, alongside aggressive expansion into untapped emerging economies. These forces exert pressure on manufacturers to innovate rapidly, optimize supply chains, and differentiate products based on verified efficacy and long-term cost of ownership.

Drivers: The most prominent driver is the escalating prevalence of airborne diseases and respiratory conditions globally, directly correlating with the increase in particulate matter (PM) and smog in densely populated urban centers. Government initiatives and public health campaigns promoting indoor air quality awareness are accelerating adoption. Moreover, the integration of air purifiers into smart home platforms enhances user convenience and control, appealing to technologically savvy demographics. Corporate and institutional demands for compliance with health and safety standards in enclosed public spaces further solidify market growth. The demonstrable link between clean air and improved cognitive function and productivity is increasingly convincing commercial buyers to invest in high-performance filtration solutions, viewing them as essential workplace assets rather than discretionary expenses.

Restraints: The market’s expansion is constrained by several factors. The significant cost of certified HEPA and advanced carbon filters often results in a high total cost of ownership over the product lifespan, posing a barrier to entry for lower-income households. Furthermore, consumer skepticism regarding the genuine effectiveness and misleading marketing claims (e.g., unproven ionization technologies) in a fragmented market can erode trust. A key technical restraint involves the energy consumption of high-efficiency purifiers, especially when operating at maximum fan speed, leading to concern over electricity bills, although modern units are striving for Energy Star compliance. Finally, the bulky design of high-capacity units can sometimes conflict with modern aesthetic preferences, creating a functional trade-off that manufacturers must address through design innovation.

Opportunities: Significant market opportunities stem from the untapped potential in developing economies where IAQ standards are emerging but penetration rates are low. There is a substantial opportunity for manufacturers to innovate filter technology, focusing on washable, reusable, or self-cleaning filters to alleviate the recurring maintenance cost barrier. The growing emphasis on environmental sustainability provides an opportunity for the development and marketing of eco-friendly and biodegradable filter materials. Additionally, specialized air purification systems tailored for niche applications, such as medical facilities, laboratories requiring ultra-fine filtration, and vehicles, offer high-margin expansion pathways. Collaborative partnerships with residential developers and HVAC companies to integrate whole-house filtration systems present a major avenue for long-term growth and market saturation.

The Filter Air Purifiers Market is comprehensively segmented based on Filter Type, Application, and Distribution Channel, allowing for detailed analysis of consumer preferences and market dynamics across various use cases. Segmentation by filter type is crucial as it dictates the device's efficacy against specific contaminants, with HEPA technology dominating due to its efficiency against fine particulate matter, while activated carbon addresses odors and VOCs. The application segmentation clearly distinguishes between high-volume residential demand and the high-value, stringent requirements of commercial and industrial settings. Analyzing these segments provides strategic insights into R&D focus, pricing strategies, and regional marketing efforts, ensuring products meet the specific needs of their target end-users effectively. This structured market view is essential for identifying both mature segments and high-growth niches.

The residential segment continues to drive volume sales, propelled by heightened individual focus on home health and comfort, favoring compact and aesthetically pleasing units. Conversely, the commercial segment, encompassing healthcare, hospitality, and corporate offices, demands robust performance, certification, and integration with building management systems, translating into higher average selling prices (ASPs). The selection of the distribution channel, particularly the rapid growth of the online segment, reflects modern purchasing habits where product comparison and user reviews heavily influence purchasing decisions, demanding strong digital marketing and logistics capabilities from market players. Understanding the interplay between these segments enables targeted product development, for instance, designing multi-stage filtration systems that combine HEPA, activated carbon, and specialized features like UV-C or ionizers to cater to diverse contamination profiles.

Future growth within segmentations is expected to be dictated by regulatory pressure and technological integration. For instance, increased scrutiny on VOCs and chemical contaminants will boost demand for advanced carbon filtration and PCO technologies, potentially challenging the traditional dominance of pure HEPA filters. The rise of interconnected smart homes will further cement the distinction between basic mechanical purifiers and premium, IoT-enabled devices, creating a clear two-tier market structure within the residential segment. Similarly, in the commercial sphere, customization for large spaces and integration into HVAC infrastructure for whole-building filtration represent key areas of strategic investment, moving beyond standalone unit deployment. This continuous evolution necessitates dynamic adaptation of product portfolios by leading companies to maintain market relevance.

The value chain of the Filter Air Purifiers Market begins with upstream activities focused on raw material procurement, particularly specialized materials like borosilicate glass fibers for HEPA media, high-grade granular activated carbon, and sensor components. Suppliers of these raw materials, often niche chemical and textile manufacturers, wield moderate bargaining power, especially for certified, high-efficiency media. Manufacturing involves sophisticated assembly processes, blending industrial design with precision engineering for fan motors and air sealing mechanisms. Key activities include R&D for filter efficiency and longevity, software integration for smart features, and rigorous quality control testing to achieve performance certifications (e.g., AHAM Verifide, Energy Star). Efficient upstream management is critical for cost containment and maintaining product performance consistency.

Downstream activities center on distribution, sales, and aftermarket services. Distribution channels are bifurcated into direct and indirect routes. Direct distribution often involves sales through company-owned e-commerce platforms or corporate sales teams targeting large commercial contracts. Indirect channels rely heavily on retail partners—both brick-and-mortar specialty electronics stores and mass-market hypermarkets—and increasingly on global e-commerce giants. Marketing and consumer education play a vital role downstream, as product efficacy and filter replacement schedules are complex concepts requiring clear communication. The provision of robust after-sales service, including convenient filter subscription models and technical support, significantly influences customer satisfaction and recurring revenue streams.

The distribution network complexity varies geographically. In developed markets, the influence of online retail (e-commerce) is paramount, offering extensive reach and competitive price transparency, often bypassing traditional middlemen. However, in developing markets, brick-and-mortar retail and local distributors remain essential for demonstration, trust-building, and localized logistics. Successful value chain management requires optimizing logistics for timely delivery of both the initial product and replacement filters. Furthermore, vertical integration in manufacturing, particularly controlling the production of proprietary filter media, provides a strategic advantage, ensuring supply stability and mitigating costs associated with reliance on external, specialized suppliers.

Potential customers for filter air purifiers are broadly categorized into three major segments: residential end-users, commercial entities, and industrial operators, each possessing distinct purchase motivations and technical requirements. Residential buyers, the largest volume segment, are typically individuals or families motivated by health concerns, such as managing allergies, asthma, or general wellness, and improving the odor profile of their homes, often seeking mid-range to premium, aesthetically pleasing, and user-friendly devices with smart capabilities. This group is highly influenced by medical advice, online reviews, and performance certifications, often purchasing through online channels for convenience and price comparison.

The commercial segment encompasses a diverse group of buyers including hospitals and healthcare facilities, educational institutions (schools, universities), hospitality venues (hotels, restaurants), and corporate offices. These buyers are driven by regulatory compliance, the desire to ensure employee and customer health safety (especially post-pandemic), and the recognized link between IAQ and productivity. Their requirements focus on high-capacity, heavy-duty purification systems, low noise output, energy efficiency, and systems that can integrate seamlessly with existing HVAC infrastructure and facility management protocols. Purchase decisions are typically made by procurement departments or facility managers, prioritizing total cost of ownership (TCO) and certified performance data.

Industrial customers, while representing a smaller volume, purchase high-value, specialized filtration equipment designed for demanding environments. This segment includes manufacturing plants, cleanrooms, laboratories, and processing facilities where control over airborne contaminants is critical for product quality, process integrity, or worker safety. Their needs are highly specialized, often requiring ULPA (Ultra-Low Penetration Air) or specialized chemical filtration media, robust construction, and adherence to strict industry standards (e.g., FDA, ISO). Buying decisions are highly technical and are usually driven by engineering and safety compliance teams, focusing on performance guarantees and long-term reliability under severe operating conditions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 26.3 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Daikin Industries Ltd., Honeywell International Inc., Sharp Corporation, LG Electronics, Samsung Electronics, Blueair AB, IQAir, Coway Co., Ltd., Xiaomi Corporation, Whirlpool Corporation, Panasonic Corporation, Koninklijke Philips N.V., Camfil AB, 3M Company, Carrier Global Corporation, Electrolux AB, Austin Air Systems, Levoit, Winix Inc., Haier Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology landscape of the Filter Air Purifiers Market revolves around the efficiency and combination of various filtration media. High-Efficiency Particulate Air (HEPA) filtration remains the gold standard, capable of capturing 99.97% of airborne particles 0.3 microns in size, forming the bedrock of most premium purification units. Technological advancements are focused on enhancing HEPA media by integrating anti-microbial coatings or developing proprietary fibers that improve airflow without sacrificing efficiency. Complementary technology includes Activated Carbon filters, which use adsorption to neutralize odors, smoke, and Volatile Organic Compounds (VOCs). The trend is toward hybrid filtration systems that integrate multiple stages—such as a washable pre-filter, HEPA, and a dense carbon bed—to address a comprehensive range of pollutants efficiently.

Beyond passive filtration, the landscape is increasingly adopting active purification technologies to augment the filter process. These include UV-C light sterilization, used to inactivate viruses and bacteria trapped on the filter media or passing through the air stream, although its effectiveness is debated based on exposure time. Another notable technology is Photocatalytic Oxidation (PCO), which utilizes a UV light source combined with a titanium dioxide (TiO2) catalyst to chemically decompose gaseous pollutants like VOCs into harmless byproducts. While PCO does not rely on physical filters, it is often marketed as a high-end feature in filter-based purifiers, positioning the product as a complete air sanitation solution.

The most significant technological shift is the integration of Internet of Things (IoT) and advanced sensor technology. Modern filter air purifiers are equipped with highly sensitive laser-based sensors for PM2.5 detection and electrochemical sensors for specific VOCs (e.g., formaldehyde, ozone). This sensor data fuels the device’s intelligence, allowing for real-time adjustments and smart operation. Cloud connectivity enables remote control, diagnostics, and subscription management for filters, enhancing user experience and driving recurring service revenue. Future technological focus will concentrate on creating silent, powerful, and aesthetically integrated units with highly specific filtration capabilities tailored to unique urban and indoor environmental challenges, leveraging AI for optimization.

The Asia Pacific region commands the largest share of the Filter Air Purifiers Market and is projected to exhibit the highest growth rate during the forecast period. This dominance is intrinsically linked to severe and chronic air quality issues prevalent across densely populated and rapidly industrializing countries such as China, India, and Southeast Asian nations. The high incidence of respiratory diseases, coupled with substantial public awareness driven by media coverage of pollution events (e.g., winter smog), positions air purification as a household necessity. Governments in the region are increasingly investing in public IAQ initiatives, although household consumption remains the primary driver.

Key market characteristics in APAC include a strong emphasis on affordability in the mass market segment, often led by domestic giants and international brands offering entry-level models. However, the premium segment is also expanding rapidly, particularly in tier-one cities in China and South Korea, where consumers demand high-capacity units with advanced features like multi-stage filtration, smart connectivity (IoT), and aesthetic design. The competitive landscape is intensely localized, requiring manufacturers to tailor product specifications, pricing, and distribution strategies to diverse cultural and economic landscapes, with online sales serving as a major distribution channel.

The future trajectory of the APAC market is expected to be characterized by continued innovation in filter technology to combat unique regional pollutants (e.g., industrial dust, agricultural burning smoke) and a significant push towards integrating air purification capabilities into centralized HVAC systems in new commercial and residential developments. Regulatory bodies are expected to tighten IAQ standards, further institutionalizing the need for high-efficiency filtration solutions across all sectors, ensuring sustained, aggressive market expansion.

North America holds a substantial share of the global market, characterized by high disposable income, strong health consciousness, and high adoption rates of smart home technology. Market growth is primarily driven by concerns over allergies, pet dander, and increasingly, airborne contaminants resulting from frequent wildfire smoke events across the continent. Consumers in this region prioritize certified performance (e.g., Clean Air Delivery Rate - CADR), low noise levels, and seamless integration with existing smart ecosystems (Amazon Alexa, Google Home). The market structure is highly polarized, with strong demand for both entry-level personal purifiers and high-end, high-capacity, designer units.

The competitive environment in North America is highly active, featuring strong presence from established global electronics brands and specialized IAQ companies. Marketing emphasizes verified efficacy, product durability, and ease of filter subscription services to manage the recurring cost component. A significant trend is the increasing demand for whole-house filtration solutions, where purifiers are either integrated into the HVAC system or high-CADR units are strategically deployed to cover large residential footprints. Furthermore, stringent building codes and workplace safety standards bolster the commercial segment, particularly in sectors like healthcare and data centers.

Future growth will be sustained by continuous technological upgrades, specifically in sensor technology (to detect ultra-fine particles and a broader range of VOCs) and AI-driven automation. Education campaigns targeting the health risks associated with chronic exposure to indoor pollutants, such as mold and chemical off-gassing, will continue to convert new users. The focus remains heavily on the premiumization of the product, linking air purification not just to health, but to overall wellness and sophisticated home management.

The European market for filter air purifiers is marked by robust regulatory frameworks concerning health and energy efficiency. While general outdoor air pollution varies across the continent, indoor air quality is a significant concern, driven by tightly sealed, energy-efficient buildings that can trap and concentrate indoor contaminants like radon, mold spores, and building material off-gassing. Consequently, European consumers and commercial buyers place a high premium on products that offer verifiable filtration efficiency, particularly against allergens and VOCs, while strictly adhering to European energy consumption standards (e.g., ERP directives).

Market penetration is solid, particularly in Western European nations like Germany, the UK, and France. Key drivers include the aging population susceptible to respiratory issues, and high public awareness campaigns regarding the source of indoor pollution. The distribution landscape is mature, combining traditional electronics retail with a strong e-commerce presence. Companies often emphasize sleek, minimalist design that aligns with contemporary European aesthetics, making the purifier an acceptable piece of home furniture rather than a utility appliance.

Future expansion is anticipated to be fueled by mandatory IAQ standards in public buildings and schools, creating a stable growth environment for the commercial segment. Furthermore, innovation will center on creating sustainable filter solutions, minimizing plastic waste, and developing highly energy-efficient motors and fan systems. The focus on low noise operation is also paramount, reflecting consumer demand for unobtrusive technology within their living and working spaces. Eastern European markets offer growth potential as economic development continues to improve disposable incomes and raise health awareness.

The Latin American region represents an emerging market for filter air purifiers, with growth accelerating due to rapid urbanization, increasing industrialization, and subsequent deterioration of air quality in major metropolitan centers such as São Paulo, Mexico City, and Santiago. While historical market penetration has been low due to economic volatility and prioritizing essential durable goods, rising middle-class disposable incomes and increased access to information regarding global health trends are shifting consumer behavior.

Current demand is price-sensitive, often favoring mid-range and basic HEPA purification units. However, high-end demand is concentrated among affluent urban populations concerned with respiratory health and status. The market relies heavily on traditional retail channels and localized distributors, although e-commerce is rapidly gaining traction, particularly in Brazil and Mexico. Education remains a critical factor, as many consumers are still learning about the specific benefits of filter-based air purification versus simpler air conditioning units.

Opportunities for growth are vast, driven by improving economic stability and a focus on public infrastructure modernization. Manufacturers entering the LATAM market must focus on building strong local distribution partnerships, offering flexible payment options, and providing clear, culturally relevant education on the long-term health benefits of IAQ management. The commercial sector, particularly new hotel and corporate office developments, offers early opportunities for high-capacity unit sales, setting the stage for wider consumer adoption.

The MEA region presents a unique market environment influenced by extreme climatic conditions, including frequent sandstorms and high levels of dust (particulate matter), alongside significant infrastructure investment, particularly in the Gulf Cooperation Council (GCC) countries. The demand for air purification in this region is driven both by outdoor environmental challenges necessitating robust filtration (especially pre-filters and HEPA) and by the high construction rates leading to increased indoor dust and VOC exposure in new buildings. The commercial sector, particularly high-end hospitality, retail complexes, and medical facilities, serves as a major consumer of advanced purification systems to maintain high standards for patrons.

The market in the Middle East is characterized by a demand for premium, high-capacity, and durable units capable of operating reliably in high-temperature environments, often requiring specialized motors and filtration structures. In contrast, the African continent is highly fragmented, with strong growth potential in wealthier nations (e.g., South Africa, Nigeria) but generally lower overall penetration. Challenges include distribution logistics, affordability issues, and low awareness in many sub-Saharan African countries.

Future growth will be significantly impacted by sustained government investment in healthcare infrastructure and smart city development across the GCC states, promoting the mandated use of advanced IAQ systems in public and commercial facilities. For the African segment, growth is contingent on rising economic stability and targeted campaigns addressing localized pollution issues. Manufacturers should prioritize products with durable components and effective multi-stage filtration to combat the high load of coarse and fine dust prevalent in the region.

The Filter Air Purifiers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033, driven by increasing air pollution and consumer health awareness globally.

HEPA (High-Efficiency Particulate Air) filtration dominates the market because it is proven to capture 99.97% of particles as small as 0.3 microns, including fine particulate matter (PM2.5), which is a major health concern worldwide.

AI integration enables air purifiers to operate proactively by using advanced sensors and machine learning to predict pollution spikes, automatically adjust filtration settings, optimize energy usage, and accurately predict filter replacement timing based on actual usage.

The Asia Pacific (APAC) region is expected to demonstrate the fastest growth rate, fueled by severe urbanization, chronic air pollution issues in major cities, and the rapidly increasing disposable incomes of the middle class across the region.

The main restraints are the high total cost of ownership (TCO) due to the recurring expense of proprietary filter replacements, along with consumer confusion and skepticism regarding the effectiveness of various filtration and supplementary technologies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.