ID : MRU_ 431499 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

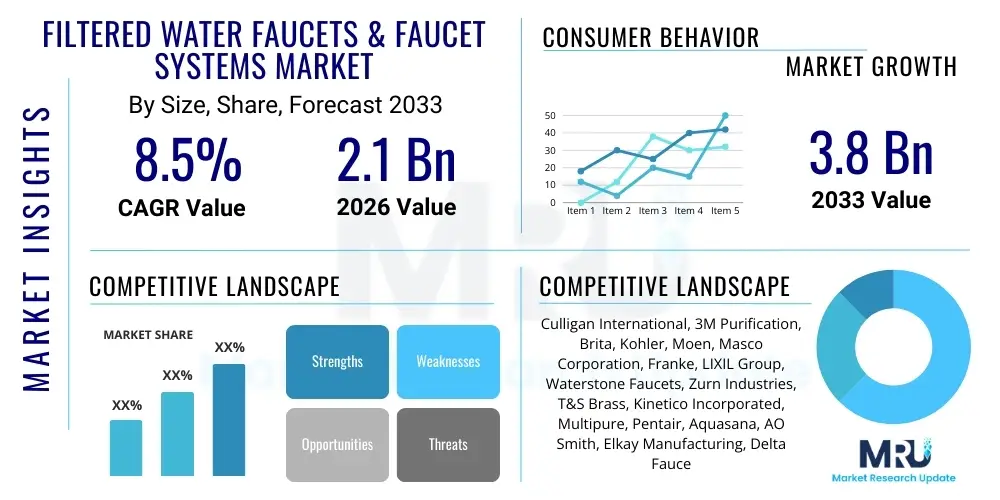

The Filtered Water Faucets & Faucet Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $2.1 Billion in 2026 and is projected to reach $3.8 Billion by the end of the forecast period in 2033.

The Filtered Water Faucets & Faucet Systems Market encompasses specialized plumbing fixtures designed to dispense purified or filtered drinking water directly at the point of use, typically integrated within kitchen sinks. These systems often include under-sink filtration units utilizing technologies such as activated carbon, reverse osmosis (RO), ultrafiltration (UF), or a combination of these methods, linked to dedicated, often secondary, faucets or integrated pull-down units. The primary objective is to enhance water quality by removing contaminants like chlorine, sediment, heavy metals, pesticides, and microbial cysts, thereby improving taste, odor, and safety for consumption.

Major applications span both residential and commercial sectors. In residential settings, they are foundational components of modern kitchens focused on health and wellness, providing an accessible alternative to bottled water. Commercially, they are utilized in offices, hospitality venues, healthcare facilities, and educational institutions to provide high-quality drinking water for employees and guests. The benefits derived from these systems are substantial, including reduced plastic waste associated with bottled water, cost savings over time, and immediate access to safer, better-tasting water, which directly addresses growing consumer concern regarding municipal water infrastructure degradation and contaminants.

Driving factors propelling market expansion include increasingly stringent health standards adopted globally, greater public awareness regarding waterborne illnesses and contaminants, and rapid urbanization leading to greater strain on existing water treatment facilities. Furthermore, technological advancements have significantly improved the efficiency, footprint, and longevity of filtration cartridges, making these systems more attractive for modern living spaces. The integration of smart features, such as filter replacement indicators and flow monitoring, further catalyzes adoption, positioning filtered water systems as essential household amenities rather than mere luxury items.

The Filtered Water Faucets & Faucet Systems Market is undergoing robust growth driven by converging trends in consumer health prioritization and sustainable living practices. Business trends show a distinct shift toward integrated smart systems that offer seamless user experience and remote diagnostics, increasing the complexity and value proposition of market offerings. Key players are focusing heavily on mergers and acquisitions to consolidate distribution channels and secure proprietary filtration technologies, particularly in the Reverse Osmosis and Ultrafiltration segments, aiming for higher efficiency and lower maintenance requirements. Furthermore, the expansion of direct-to-consumer (D2C) online sales channels has lowered entry barriers for innovative startups offering modular and easy-to-install filtration kits, intensifying competitive dynamics across established brands.

Regionally, North America and Europe currently represent the largest revenue streams, characterized by high disposable incomes and a mature awareness of water quality issues, driving demand for premium, certified filtration systems. However, the Asia Pacific (APAC) region is poised for the highest growth rate, fueled by rapid infrastructural development, escalating levels of water pollution in highly populated urban centers, and the burgeoning middle class demanding reliable home solutions. Governments in countries like China and India are also promoting infrastructure upgrades and health standards, indirectly supporting the adoption of point-of-use filtration systems, thereby transforming APAC into a critical strategic growth area for manufacturers.

Segment trends highlight the dominance of under-sink multi-stage filtration units, particularly those employing RO technology, which offer the highest degree of purification, despite requiring slightly more complex installation. The residential end-user segment remains the primary revenue driver, though the commercial sector, especially the hospitality and food service industries, is increasingly adopting sophisticated systems to meet consumer expectations for quality beverages and food preparation. In terms of distribution, large home improvement retail chains and specialized plumbing distributors continue to dominate, but the strategic importance of e-commerce platforms for educating consumers and facilitating replacement filter sales is rapidly accelerating.

Common user inquiries regarding AI's influence in the Filtered Water Faucets & Faucet Systems Market frequently revolve around predictive maintenance capabilities, water quality monitoring accuracy, and the integration of filtration systems into broader smart home ecosystems. Users are primarily concerned with how AI can minimize system downtime by predicting filter degradation or component failure, thereby ensuring consistent water quality without manual checks. There is also significant interest in AI-driven water analysis that could dynamically adjust filtration stages based on real-time municipal water reports or in-pipe sensor data, optimizing performance and prolonging the life of expensive RO membranes. Expectations center on systems becoming fully autonomous, providing alerts only when action is immediately required, moving beyond simple timer-based reminders, and enabling personalized consumption pattern analysis to optimize water usage efficiency.

The application of Artificial Intelligence within this domain is fundamentally transforming system efficiency and consumer engagement. AI algorithms process data streams from integrated sensors—monitoring flow rates, total dissolved solids (TDS), and pressure—to create highly accurate degradation models for filter media. This allows manufacturers to provide Just-in-Time (JIT) maintenance notifications and automate consumable reordering, dramatically improving the customer lifecycle experience and fostering brand loyalty. Furthermore, AI-powered systems facilitate advanced diagnostics during installation or troubleshooting, reducing reliance on expensive human technical support and allowing for faster resolution of operational issues, which is a significant factor in consumer satisfaction for complex plumbing products.

Beyond operational improvements, AI also contributes to product development and customization. By analyzing aggregated consumption data across a vast network of installed units, manufacturers gain invaluable insights into regional variations in water quality and typical household usage patterns. This data informs the R&D process, leading to the creation of more robust and targeted filtration cartridges designed to specifically address prevalent local contaminants, such as lead in older infrastructure zones or high mineral content in specific geographical areas. This personalized approach to filtration, facilitated by machine learning, is key to developing next-generation water treatment solutions that are both highly effective and economically efficient for the end-user.

The dynamics of the Filtered Water Faucets & Faucet Systems Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), amplified by critical Impact Forces. A primary driver is the widespread concern over aging public water infrastructure and instances of contamination (e.g., lead or PFAS exposure), compelling consumers to seek dependable point-of-use protection. This health-driven demand is compounded by the strong governmental push for environmental sustainability, positioning filtration systems as a superior, low-waste alternative to single-use plastic bottled water, aligning perfectly with consumer environmental consciousness. However, the market faces significant restraints, notably the relatively high initial capital outlay for advanced RO systems and the perceived inconvenience of required filter changes and system maintenance, which can deter budget-conscious consumers or those prioritizing instant convenience.

Opportunities are abundant, particularly in leveraging the burgeoning Internet of Things (IoT) landscape. Integrating filtration systems with smart home networks allows for unprecedented levels of monitoring, automation, and user engagement, potentially mitigating the "inconvenience" restraint. Developing countries, especially those undergoing rapid industrialization and experiencing commensurate water quality degradation, represent vast, untapped markets where water safety is a growing priority. Furthermore, manufacturers are exploring sustainable and chemical-free filtration methods, such as enhanced UV sterilization or electro-adsorption technologies, which offer differentiating factors in a crowded market and appeal to environmentally sensitive customers.

The Impact Forces governing market trajectory are centered on regulatory standards and consumer perception. Strict certifications (like NSF/ANSI standards) act as powerful barriers to entry but significantly boost consumer confidence in certified products. Increased disposable income globally directly correlates with the ability of households to invest in permanent, high-quality water solutions over cheaper temporary alternatives. Most critically, the accelerating consumer preference for convenience dictates that future systems must not only be efficient but also aesthetically pleasing, space-saving, and offer minimal user intervention, pushing R&D towards compact, integrated faucet designs that conceal the underlying complex filtration technology, making the user experience paramount to market success.

The Filtered Water Faucets & Faucet Systems Market is segmented based on product type, filtration technology, end-user, and distribution channel, providing a granular view of market dynamics and targeted opportunities. Understanding these segments is crucial for manufacturers to tailor their offerings, distribution strategies, and marketing efforts effectively. The segmentation reflects the diverse needs of consumers, ranging from basic taste and odor improvement to comprehensive removal of microscopic contaminants, influencing the complexity and price points of the various systems available.

The technology segment reveals shifting preferences toward multi-stage filtration and highly effective methods like Reverse Osmosis (RO) due to increasing concerns about contaminants not addressed by basic carbon filters. Concurrently, the rise of smart faucets integrated directly into filtration systems (Smart Faucets) addresses the growing demand for convenience, real-time data, and seamless design integration in modern kitchens. Geographically, market maturity varies significantly, requiring manufacturers to adapt product specifications—such as flow rate capacity and contaminant removal specifics—to local water quality profiles and regulatory environments.

The value chain for the Filtered Water Faucets & Faucet Systems Market begins with upstream activities focused heavily on specialized material sourcing and component manufacturing. This stage involves the procurement of highly engineered materials for filtration membranes (e.g., polyamide materials for RO membranes, specialized resins for carbon blocks) and sophisticated electronic components for smart systems, including sensors, microcontrollers, and wireless communication modules. Key upstream stakeholders include specialty chemical suppliers, membrane technology companies, and component manufacturers who adhere to strict quality controls to ensure compliance with drinking water safety standards (e.g., NSF/ANSI). Efficiency and innovation in this segment, particularly regarding membrane lifespan and contaminant rejection rates, directly determine the final product’s performance and cost structure.

Midstream activities encompass the actual manufacturing, assembly, and branding of the finished faucet and filtration unit. Leading manufacturers invest heavily in precision engineering to ensure the longevity and leak-proof nature of both the faucet hardware (e.g., corrosion-resistant finishes, solid brass construction) and the filtration housing. Direct distribution channels, where manufacturers sell directly to large contractors or via proprietary e-commerce sites, allow for greater control over branding and pricing, while indirect distribution relies on established networks of plumbing wholesalers, large home improvement retailers (e.g., Lowe’s, Home Depot), and specialized kitchen and bath showrooms. The choice of channel often depends on the complexity of the product; high-end, professionally installed systems favor plumbing wholesalers, while DIY-friendly systems dominate retail shelves.

Downstream activities center on installation, maintenance, and ongoing customer support, which are critical for long-term revenue generation through recurring filter media sales. Professional plumbers and installation technicians play a vital role in ensuring system integrity and performance, especially for complex RO systems requiring drain line connections and pressure adjustments. The recurring revenue stream derived from replacement filters is a defining characteristic of this market, emphasizing the importance of robust customer relationship management (CRM) and streamlined supply chains for consumables. Effective post-sale service and automated reorder reminders through smart system integration significantly enhance customer lifetime value and reinforce market dominance for companies with extensive service networks.

The primary customer base for Filtered Water Faucets & Faucet Systems is broadly categorized into two major segments: residential homeowners and commercial enterprises. Within the residential sector, the ideal customer profile often includes middle to high-income households residing in urban or suburban areas, typically individuals aged 30 to 55, who are highly health-conscious, environmentally aware, and value modern kitchen aesthetics. These customers prioritize the safety of their drinking water, often driven by familial health concerns (e.g., for young children or elderly relatives) or a desire to eliminate the environmental footprint and logistic burden associated with purchasing bottled water. They are actively searching for permanent, integrated solutions that seamlessly blend high performance purification with premium kitchen design.

A secondary, rapidly growing group within the residential segment includes apartment dwellers and renters, increasingly targeted by manufacturers with compact, easy-to-install countertop or simple under-sink systems that require minimal modification to existing plumbing. These systems cater to customers seeking improved water quality without the long-term commitment or high cost of professional installation, broadening the accessibility of filtered water. Furthermore, affluent consumers embarking on kitchen renovations are prime targets for integrated smart faucet systems, where the filtration unit is incorporated into the overall design plan by interior designers and custom home builders, indicating a strong influence from the professional services sector.

In the commercial sector, the largest buyers include the hospitality industry (hotels and restaurants), corporate offices, and institutional settings like hospitals and universities. Hotels and high-end restaurants adopt these systems to ensure high-quality water for beverages, ice production, and cooking, directly impacting the quality of their service offering. Corporate offices utilize filtered water systems as an employee amenity, often replacing bulk water coolers with centralized, plumbed-in systems for efficiency and environmental reasons. Healthcare facilities, meanwhile, require robust, certified filtration to meet stringent hygiene and patient care standards, making them critical buyers of highly reliable, often institution-specific, RO and UF systems.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $2.1 Billion |

| Market Forecast in 2033 | $3.8 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Culligan International, 3M Purification, Brita, Kohler, Moen, Masco Corporation, Franke, LIXIL Group, Waterstone Faucets, Zurn Industries, T&S Brass, Kinetico Incorporated, Multipure, Pentair, Aquasana, AO Smith, Elkay Manufacturing, Delta Faucet Company, Everpure (Pentair), InSinkErator |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological evolution of the Filtered Water Faucets & Faucet Systems market is characterized by a drive toward higher purification efficacy, reduced operational footprint, and enhanced user connectivity. Activated Carbon remains the foundational technology for improving taste and odor, but modern systems often utilize compressed carbon block technology to enhance contaminant absorption surface area while maintaining high flow rates. The major technological frontier involves Reverse Osmosis (RO), which has seen significant innovation focused on minimizing wastewater generation and increasing membrane lifespan. Newer RO systems now incorporate booster pumps and non-electric gravity flow systems to overcome pressure limitations and improve efficiency, addressing the traditional drawback of high water waste associated with older RO models, thereby making them more environmentally acceptable to a wider consumer base.

Beyond traditional mechanical filtration, the integration of smart technologies is defining the premium segment. These systems feature embedded sensors that continuously monitor Total Dissolved Solids (TDS) levels, filter usage, and flow rate. This data is transmitted via Wi-Fi or Bluetooth to dedicated smartphone applications, providing real-time quality assurance and predictive maintenance alerts. Furthermore, some high-end systems incorporate UV sterilization technology as a final stage, providing a chemical-free defense against bacteria and viruses, which is particularly appealing in areas where microbial contamination is a concern, enhancing the robustness of the "system" concept beyond mere filtration.

Material science also plays a crucial role, particularly in the longevity and safety of the faucet hardware itself. Manufacturers are increasingly utilizing lead-free brass and high-grade stainless steel with specialized finishes that resist tarnish and corrosion, ensuring compliance with strict health regulations and aesthetic durability. The move towards quick-connect mechanisms for filter cartridges minimizes the mess and difficulty of maintenance, facilitating DIY replacements and lowering the total cost of ownership. This continuous refinement in both the purification mechanics and the user interface design confirms that innovation is occurring across the entire product ecosystem, from the under-sink unit to the visible faucet fixture.

The most comprehensive filtration technology is Reverse Osmosis (RO), which removes up to 99% of total dissolved solids (TDS), including heavy metals, chemical residues, and microorganisms. However, modern multi-stage systems combining Activated Carbon and Ultrafiltration (UF) offer high effectiveness with better flow rates and less water waste compared to traditional RO units.

Filter replacement frequency is highly dependent on the filtration technology used, local water quality (hardness/sediment), and daily water consumption volume. Activated carbon filters typically require replacement every six months to one year, while high-performance RO membranes can last two to three years. Smart systems often provide automated, real-time indicators based on flow monitoring to optimize replacement timing.

Yes, most under-sink filtered water faucet systems are designed for standard home plumbing setups. Installation usually requires a connection to the cold water line beneath the sink and either a dedicated hole for the secondary faucet or integration into a replacement main faucet. While basic systems are DIY-friendly, complex RO systems often require professional installation due to the necessity of connecting to the drain line.

Conventional filtered faucet systems utilize a separate, dedicated small faucet installed next to the main sink faucet solely for dispensing filtered water. Integrated systems, conversely, incorporate the filtration dispensing mechanism directly into the main kitchen faucet, often using a lever or button to switch between unpurified and filtered water flow, offering superior aesthetic integration and counter space saving.

Smart systems, while having a higher initial purchase price, can potentially lower the long-term cost of ownership by optimizing maintenance schedules. By using AI to accurately monitor filter life based on actual usage and water quality, they prevent premature filter changes and ensure maximum efficiency from expensive cartridges, offsetting the initial investment through optimized consumable usage and reduced service calls.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.