ID : MRU_ 437410 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

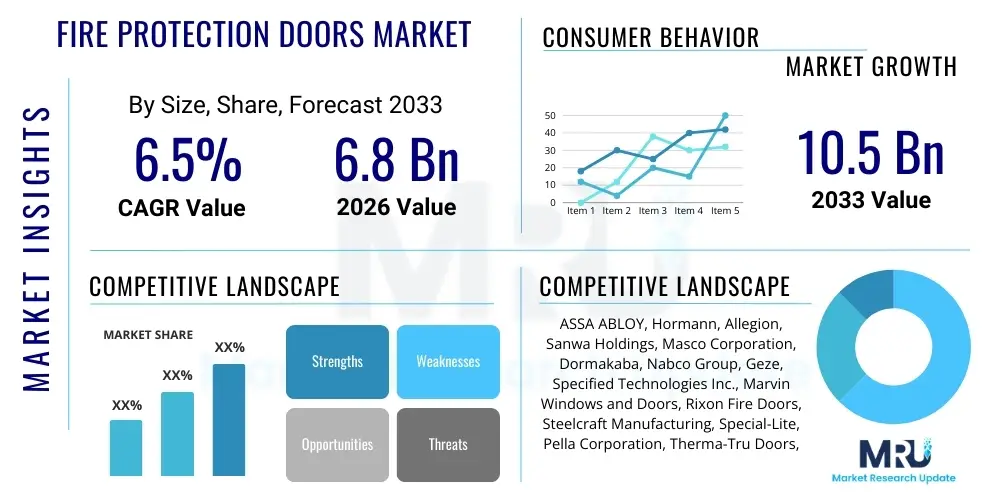

The Fire Protection Doors Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 6.8 Billion in 2026 and is projected to reach USD 10.5 Billion by the end of the forecast period in 2033.

The Fire Protection Doors Market encompasses the design, manufacture, and installation of specialized doors engineered to resist fire and prevent the spread of smoke and heat for a defined period, thereby providing crucial escape time for occupants and protecting assets. These critical safety components are integral parts of passive fire protection systems in modern infrastructure, playing a pivotal role in compartmentalizing buildings to control hazards. The products are highly regulated, requiring stringent certification standards such as UL, NFPA, and EN standards, ensuring reliable performance under extreme conditions. The increasing complexity of architectural designs and the heightened global focus on safety standards in both commercial and residential sectors continue to drive innovation in materials and features, including integrated sealing systems and advanced hardware.

Fire protection doors are fundamentally differentiated by their fire resistance rating, which dictates the duration (e.g., 20 minutes to over 120 minutes) they can withstand fire exposure while maintaining integrity and insulation. Major applications span across highly trafficked commercial buildings, industrial facilities housing valuable equipment or hazardous materials, and multi-family residential complexes where safety protocols are strictly mandated. The primary benefit of these doors lies in their life-saving function, offering compartmentalization that restricts fire spread, limits property damage, and ensures safe evacuation pathways, significantly reducing overall risk exposure for stakeholders and insurance providers.

The market is primarily driven by rigorous updates to global building safety codes and mandatory compliance requirements imposed by governmental and insurance bodies following high-profile fire incidents. The surging global construction industry, particularly the development of high-rise structures and complex industrial parks in emerging economies, contributes significantly to market expansion. Furthermore, the trend toward retrofitting existing commercial and institutional buildings to meet modern fire safety standards acts as a consistent demand catalyst. Innovations focusing on aesthetics, integrating fire resistance into standard door designs, and developing lightweight, high-performance intumescent materials are crucial factors shaping future market dynamics and attracting architectural interest.

The global Fire Protection Doors Market is currently characterized by robust business trends emphasizing sustainability, digitalization, and integration of smart technologies. Manufacturers are increasingly investing in research and development to produce doors with enhanced energy efficiency and lower environmental footprints, aligning with global green building standards. Key business strategies revolve around consolidation, with major players acquiring specialized manufacturers to expand their technological portfolios, particularly in highly sophisticated fire-rated glass and automated door systems. Furthermore, the supply chain is experiencing optimization through the adoption of advanced manufacturing techniques like robotic welding and automated assembly, aimed at improving product quality consistency and reducing lead times in complex customization orders.

Regional trends indicate that Asia Pacific (APAC) is poised for the fastest growth, propelled by massive infrastructure investment, rapid urbanization, and the adoption of stringent international fire safety standards in populous nations like China and India. North America and Europe, while mature, maintain strong market positions driven by compulsory regulatory updates, substantial demand for retrofitting aging commercial structures, and a high consumer willingness to invest in premium, high-rated fire protection solutions. The Middle East and Africa (MEA) region is exhibiting significant growth, fueled by mega-projects in hospitality and commercial real estate sectors, which demand internationally certified, high-performance fire doors, often incorporating complex aesthetic requirements alongside functional safety.

Segment trends reveal that the steel fire protection door segment holds the largest market share due to its superior durability, cost-effectiveness, and ability to achieve the highest fire ratings, making it indispensable in industrial and heavy commercial applications. However, the timber and composite door segments are projected to experience accelerated growth, driven by architectural preferences in residential and luxury commercial sectors where aesthetics and customization are paramount, often integrating advanced core materials for enhanced fire resistance without compromising design. Additionally, the segment for doors rated 90 minutes and 120 minutes is growing rapidly, reflecting the construction trend toward larger, more complex buildings requiring higher levels of compartmentalization security and prolonged safety barriers.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Fire Protection Doors Market frequently center on predictive maintenance capabilities, enhanced security features, and streamlining the design and certification processes. Users are keenly interested in how AI algorithms can monitor the operational status of intelligent fire doors, predict potential hardware failures before they occur, and integrate seamlessly with centralized building management systems (BMS) for optimized safety responses. There is also significant curiosity about AI’s role in automating the complex compliance documentation and ensuring designs adhere instantly to various global fire safety codes (e.g., NFPA, EN), thus reducing human error and expediting project timelines, which summarizes the collective expectation that AI will transition these products from passive safety barriers to integrated, proactive components within smart building ecosystems.

The dynamics of the Fire Protection Doors Market are governed by a complex interplay of Drivers, Restraints, Opportunities, and broader Impact Forces that dictate market direction and investment strategies. Key drivers fundamentally include the stringent enforcement of fire safety regulations globally, particularly in developed economies, making the installation of certified fire doors mandatory in almost all public and commercial construction projects. This regulatory environment, coupled with the increasing global awareness regarding structural safety following catastrophic fire incidents, provides a non-negotiable baseline demand. Furthermore, the rapid growth in global construction activities, especially the proliferation of high-rise commercial, healthcare, and educational facilities, significantly boosts the need for advanced fire compartmentalization solutions, ensuring sustained market expansion throughout the forecast period.

However, the market faces notable restraints, primarily centered around the high initial cost associated with manufacturing, sourcing, and installing highly specialized, certified fire doors, which often include expensive intumescent materials and robust, complex hardware. This elevated cost can sometimes deter adoption in price-sensitive markets or smaller residential projects. Another significant restraint is the complexity and time-consuming nature of the certification and regulatory approval process, which varies widely across geographies, posing challenges for manufacturers operating on a global scale. Additionally, the installation requires highly skilled labor; poor installation practices can compromise the door’s fire rating, leading to potential liability issues and creating barriers to entry for standardized, easy-to-deploy products.

Opportunities for market growth are substantial, particularly through technological advancements such as the integration of smart sensors and IoT capabilities into fire doors, allowing for real-time monitoring and connectivity with central building management systems. This convergence transforms passive safety devices into active components of a security network. The rising trend of renovation and retrofitting of older commercial and industrial buildings presents a lucrative opportunity, as these structures must be upgraded to comply with modern fire codes. Competitive impact forces, driven by increasing competition and the need for product differentiation, push manufacturers toward material innovation, focusing on achieving higher ratings with lighter, more aesthetically pleasing, and sustainable materials like composite cores and advanced fire-rated glass, thereby broadening application scope.

The Fire Protection Doors Market is comprehensively segmented based on material composition, operational type, fire rating duration, and end-user application, providing a granular view of demand patterns across various sectors. Analyzing these segments helps stakeholders understand where growth is concentrated and where technological investment should be prioritized. The segmentation reflects both the technical necessities required by fire codes (rating and material) and the functional demands of building operation (type and end-user), ensuring that specialized product offerings meet specific safety and architectural requirements across the global construction landscape.

The value chain for the Fire Protection Doors Market begins with upstream raw material suppliers, predominantly focusing on steel, specialized core materials (like mineral fiber and gypsum), high-performance intumescent seals, and specialized hardware (hinges, locks, closures). Efficiency and quality control at this stage are paramount, as the integrity of the final product’s fire rating relies heavily on the consistency and performance of these input materials. Manufacturers often establish long-term partnerships with certified material suppliers to ensure compliance and traceability, which is a critical regulatory requirement. Upstream activities are currently focused on sourcing sustainable and lighter core components that can still meet stringent fire-resistance standards, driving material innovation.

Mid-stream activities involve the specialized manufacturing, assembly, and rigorous testing processes. Manufacturers must employ precise fabrication techniques, especially in welding and sealing, to ensure the door assembly maintains its integrity under thermal stress. This stage includes complex procedures like applying intumescent strips and installing certified glazing. Distribution channels play a vital role in connecting manufacturers to the final installation site, utilizing both direct and indirect models. Direct sales are common for large-scale, complex commercial or institutional projects where customization and close consultation with architects and fire safety engineers are required. This ensures that highly specific performance criteria are met and guarantees correct installation procedures.

Downstream activities involve specialized installation and maintenance services. Due to the critical safety function of these products, installation must be performed by certified and trained professionals to avoid compromising the fire rating—a common failure point. Post-sale services, including periodic inspection, maintenance, and certification renewal, form an essential and growing part of the value chain, driven by mandatory inspection protocols. Indirect channels, primarily involving large distributors, wholesalers, and construction material retailers, cater mostly to standard or smaller residential and light commercial projects, prioritizing inventory management and logistical efficiency for standardized products.

The primary potential customers and end-users of fire protection doors span across the entire spectrum of the built environment, driven by regulatory compliance and safety mandates rather than optional utility. The commercial sector, encompassing office towers, retail centers, and hospitality establishments (hotels and restaurants), represents a significant buying bloc. These entities require high-volume, often aesthetically customized fire doors that must integrate seamlessly with interior design while providing ratings typically ranging from 60 to 120 minutes. Purchase decisions in this sector are heavily influenced by architectural specifications, compliance certification records, and the supplier's ability to handle large, complex projects efficiently.

The institutional sector, comprising critical infrastructure such as hospitals, educational facilities (schools and universities), and government buildings, constitutes another crucial customer segment. Hospitals, in particular, require specialized fire doors with high durability, complex access control systems, and often the highest fire ratings (up to 180 minutes) to protect vulnerable populations and critical life-saving equipment. Purchase criteria here prioritize long-term reliability, accessibility features (ADA compliance), strict adherence to local and national codes, and the integration capabilities with sophisticated fire alarm and security systems.

The industrial and residential sectors complete the primary customer landscape. Industrial end-users, including manufacturing plants, chemical storage facilities, and large warehouses, demand heavy-duty steel fire doors designed for maximum ruggedness and high exposure ratings (often 120 minutes and above). Conversely, the residential segment, dominated by multi-family apartment complexes and condominiums, seeks fire doors that balance safety requirements with domestic aesthetics, driving demand for certified timber and composite doors. Buyers in this segment are often developers and property management firms focused on meeting mandatory building codes while minimizing maintenance overhead.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 10.5 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ASSA ABLOY, Hormann, Allegion, Sanwa Holdings, Masco Corporation, Dormakaba, Nabco Group, Geze, Specified Technologies Inc., Marvin Windows and Doors, Rixon Fire Doors, Steelcraft Manufacturing, Special-Lite, Pella Corporation, Therma-Tru Doors, Jeld-Wen, Tyman plc, Gentek Building Products, VT Industries, Halspan, Royal Boon Edam. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Fire Protection Doors Market is evolving rapidly, moving beyond basic materials science into advanced sealing systems, innovative core composition, and smart connectivity. A key technological focus is the development and optimization of intumescent sealing strips. These strips react to heat by expanding rapidly, sealing the gaps between the door frame and the door slab, which is crucial for preventing the passage of hot smoke and flames. Manufacturers are leveraging nanotechnology and specialized chemical compositions to create faster-acting and more durable intumescent materials that can withstand repeated exposure to high temperatures without compromising performance. Furthermore, the use of composite cores, combining materials like mineral wool, gypsum, and high-density fiberboard, is gaining traction to achieve high fire ratings while reducing the overall weight and improving insulation properties of the door.

Another major technological trend is the integration of high-performance fire-rated glass and glazing systems. Modern architectural demands frequently require visibility and natural light, necessitating specialized glass that maintains integrity during a fire event. This involves using multi-layered laminated glass containing intumescent interlayers that become opaque and heat-resistant when exposed to fire. This technology allows doors to satisfy both aesthetic requirements and stringent safety codes, particularly in commercial and institutional settings. Hardware technology is also becoming sophisticated, featuring integrated electronic access control systems, magnetic locks, and sophisticated door closer mechanisms that ensure the door automatically closes and latches securely when a fire alarm is triggered, eliminating human error in securing fire compartmentalization zones.

The most forward-looking aspect of the technology landscape is the adoption of IoT and smart building technology. Modern fire doors are increasingly equipped with embedded sensors that monitor their operational status, including closure verification, latch status, and potential obstruction detection. These sensors connect wirelessly to a central Building Management System (BMS), providing real-time compliance reporting and diagnostics. This connectivity enables predictive maintenance, notifying facility managers if a door mechanism shows signs of degradation that could compromise its fire rating. This shift towards smart, connected fire doors enhances safety management, streamlines inspection processes, and ensures continuous regulatory compliance, adding significant long-term value for end-users.

The Fire Protection Doors Market exhibits distinct growth trajectories across major global regions, influenced by varying regulatory frameworks, construction boom cycles, and levels of technological maturity. North America, characterized by stringent codes like NFPA and highly enforced municipal regulations, represents a mature market with high demand driven primarily by continuous compliance updates and the necessity of retrofitting aging commercial infrastructure. The market here emphasizes high-quality, certified products, often prioritizing doors with advanced security and smart features integration.

Europe mirrors North America in regulatory strictness, relying on harmonized standards like the EN series. Western European countries maintain robust demand for aesthetically pleasing fire-rated timber and glass doors in residential and heritage commercial renovations. Eastern European markets, however, are seeing rapid growth fueled by large-scale commercial and industrial development, driving demand for cost-effective, high-rating steel doors. Innovation in Europe is often centered on sustainable and environmentally compliant manufacturing processes and materials.

Asia Pacific (APAC) is undoubtedly the engine of future market growth. Driven by colossal urbanization projects, unprecedented infrastructure development (high-rises, airports, and healthcare), and the gradual but firm adoption of international fire safety standards in major economies like China, India, and Southeast Asian nations. While the region is price-sensitive, the increasing regulatory oversight and insurance mandates are compelling developers to invest in higher quality, certified fire protection solutions, making APAC the key region for volume sales and new manufacturing investment in the coming decade. Latin America and the Middle East & Africa (MEA) are also experiencing accelerated growth, largely tied to luxury and commercial mega-projects in the hospitality and business hub sectors, demanding premium, internationally certified products.

The primary driver is the continuous and increasingly stringent implementation and enforcement of global building and fire safety codes, such as NFPA standards and regional mandates. These regulations make the installation of certified, high-performance fire doors mandatory across most commercial, institutional, and high-density residential construction projects, ensuring sustained demand irrespective of economic fluctuations in the construction sector.

The fire rating directly correlates with the required level of compartmentalization and safety barrier duration. A higher rating, such as 90 or 120 minutes, indicates the door's capacity to withstand fire and heat for a longer period, making it mandatory for use in critical areas like stairwells, vertical shafts, and industrial facilities where prolonged evacuation time or asset protection is necessary.

Smart technology integrates IoT sensors into fire doors to enable real-time monitoring of operational status, ensuring the door is closed and latched correctly. This connectivity facilitates predictive maintenance, links the door directly to the Building Management System (BMS), and provides automated compliance reporting, transforming the door from a passive barrier to an active safety component.

The steel fire door segment typically holds the largest market share due to its exceptional durability, cost-effectiveness, and inherent strength, allowing it to achieve the highest fire resistance ratings (up to 180 minutes or more). Steel doors are the standard choice for industrial, institutional, and heavy commercial applications where performance and robustness are prioritized over aesthetics.

Globally, key certification standards include those established by Underwriters Laboratories (UL) and the National Fire Protection Association (NFPA) in North America, and the European Norm (EN) standards (such as EN 1634 series) in Europe. Compliance with these standards guarantees that the doors have undergone rigorous testing to verify their integrity and insulation performance under specified fire conditions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.