ID : MRU_ 433681 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

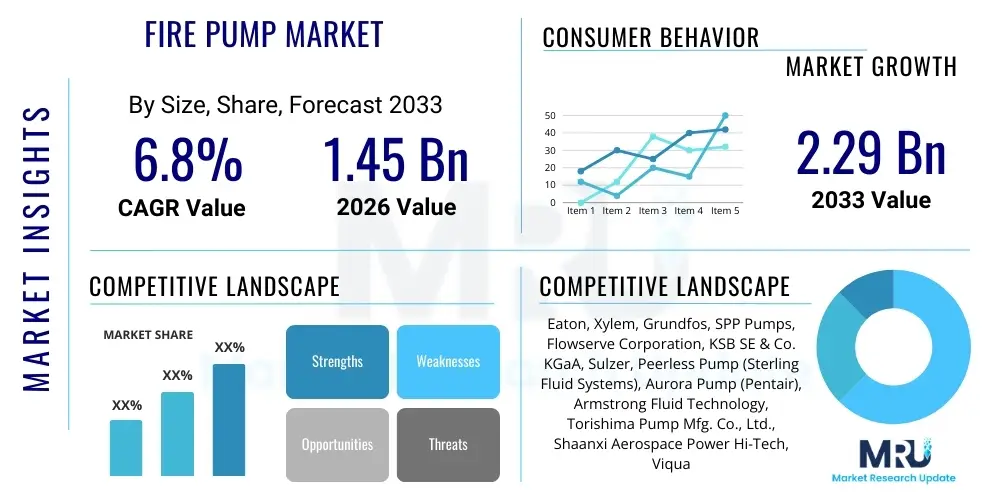

The Fire Pump Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.45 Billion in 2026 and is projected to reach USD 2.29 Billion by the end of the forecast period in 2033.

The Fire Pump Market encompasses the manufacturing, sales, and servicing of pumps specifically designed to increase water pressure within a fire suppression system, ensuring sufficient flow and pressure to extinguish fires effectively. These pumps are critical components of fire protection infrastructure in commercial, industrial, residential, and institutional buildings globally. Driven by stringent regulatory mandates, particularly NFPA (National Fire Protection Association) standards and local building codes, the demand for reliable and high-performance fire pumps is consistently strong. Key product offerings include horizontal split case, vertical in-line, end suction, and vertical turbine fire pumps, powered primarily by electric motors or diesel engines.

Major applications of fire pumps span across high-risk environments such as petrochemical plants, data centers, airports, high-rise buildings, and large-scale manufacturing facilities where system reliability is paramount. The primary benefit these systems offer is maintaining consistent water pressure required for sprinkler systems and standpipes, thereby mitigating property damage and ensuring life safety during a fire event. As urbanization accelerates and infrastructure development increases in emerging economies, the necessity for robust fire safety measures fuels the market expansion, making fire pumps indispensable safety assets.

The driving factors for market growth are manifold, including heightened global awareness regarding fire safety, rapid expansion of construction activities in Asia Pacific, and mandatory adherence to global insurance standards which often require certified fire suppression systems. Technological advancements, such as integration with IoT platforms for remote monitoring and predictive maintenance, are further enhancing the value proposition of modern fire pump systems, contributing positively to market dynamics and adoption rates across various end-user sectors.

The global Fire Pump Market is currently characterized by moderate growth, primarily driven by regulatory compulsion and ongoing modernization of existing fire safety infrastructure across developed nations. Key business trends indicate a strong shift toward sustainable and energy-efficient electric fire pumps, although diesel-driven pumps remain dominant in regions with unreliable power grids or applications requiring maximum operational autonomy. Furthermore, industry consolidation is evident, with major players focusing on comprehensive service contracts, integrating advanced diagnostics, and expanding their distribution networks, particularly targeting specialized industrial sectors like mining and marine applications where unique operational constraints exist.

Regionally, Asia Pacific is emerging as the fastest-growing market due to massive investment in infrastructure and the mandatory implementation of new safety codes in countries like China, India, and Southeast Asia. North America and Europe, while mature, maintain dominance in terms of technological adoption and adherence to the strictest certification standards (e.g., UL, FM). These mature markets are focusing on aftermarket services, retrofit projects, and the deployment of smart fire pump monitoring solutions that comply with Industry 4.0 standards, ensuring high system uptime and minimizing false activations.

Segment trends highlight the continued dominance of the electric motor segment due to lower long-term operational costs and reduced emissions, especially in urban environments. However, in terms of pump type, horizontal split case pumps hold the largest market share owing to their high flow capacity and ease of maintenance. The commercial segment, including offices, hotels, and hospitals, represents a substantial application base, although the oil & gas and power generation sectors offer the highest growth potential for specialized, high-pressure fire pump configurations requiring bespoke engineering and certification.

Common user questions regarding AI's influence on the Fire Pump Market revolve around predictive maintenance capabilities, the integration of AI with building management systems (BMS), and its role in improving response times and system reliability. Users frequently inquire about how AI algorithms can analyze vibration patterns, pressure fluctuations, and motor performance data in real-time to predict mechanical failures before they occur, thus moving from reactive to proactive maintenance schedules. There is also significant user interest in utilizing machine learning for optimizing pump operation based on historical fire risk data and environmental factors, ensuring that the system is always in peak operational readiness while minimizing unnecessary energy consumption and testing cycles. Key themes summarize the expectation that AI will transform fire pump management into a highly automated, data-driven discipline focused on maximizing system longevity and compliance.

AI's initial impact is focused on enhancing the diagnostics and monitoring phase of the fire pump lifecycle. Machine learning models can process vast amounts of sensor data collected from integrated monitoring systems (IoT sensors measuring pressure, temperature, vibration, and current draw). By establishing comprehensive baseline operational parameters, AI can quickly identify subtle anomalies that human operators might miss, such as minor bearing degradation or incipient cavitation. This shift enables condition-based monitoring, reducing the reliance on time-based maintenance schedules, which are often inefficient or insufficient for mission-critical safety equipment.

Furthermore, AI facilitates integration with broader smart city and smart building infrastructure. When fire pump status is dynamically linked to a central AI-powered platform, it can coordinate operational decisions—such as diverting power or alerting maintenance staff automatically—faster and more reliably than traditional, siloed systems. This integration significantly improves overall system resilience and allows regulatory bodies to maintain digital records of compliance tests and system performance, streamlining auditing processes and ensuring greater adherence to standards like NFPA 25 (Standard for the Inspection, Testing, and Maintenance of Water-Based Fire Protection Systems).

The Fire Pump Market is driven predominantly by stringent global safety regulations and rapid infrastructure growth, particularly in developing economies, which necessitates mandatory installation in all large construction projects. Key drivers include the revision of NFPA standards and ISO regulations that mandate higher performance and reliability criteria for fire suppression equipment. However, the market faces significant restraints, primarily stemming from the high initial capital expenditure associated with purchasing, installing, and certifying fire pump systems, coupled with fluctuating raw material costs (especially steel and copper) which impact manufacturing economics. The availability of opportunities lies primarily in emerging regions where regulatory frameworks are being strengthened, creating new mandatory installation markets, and in the aftermarket sector, specifically through digitization and provision of advanced predictive maintenance contracts.

The impact forces influencing the market trajectory are multi-layered. Regulatory force remains the most substantial, as compliance is non-negotiable for obtaining occupancy permits, thereby ensuring a baseline demand regardless of economic cycles. Economic forces, such as global GDP growth and investment in large infrastructure projects (e.g., data centers, transportation hubs), directly correlate with fire pump sales volume. Technological forces, characterized by the move toward smarter, more efficient variable-speed drive (VSD) pumps and the adoption of IoT for monitoring, are transforming product design and service offerings, adding significant value and potentially offsetting the high initial cost barrier.

Furthermore, competitive rivalry is high, driven by the presence of several established global manufacturers and regional specialists, leading to continuous innovation in pump efficiency and compact design. The primary strategic focus for major players involves optimizing their supply chains and securing long-term contracts with large engineering, procurement, and construction (EPC) firms. Overall, while the high costs and complexity of installation serve as moderate restraints, the powerful impetus of mandated safety standards and industrial expansion ensures the market's positive momentum throughout the forecast period.

The Fire Pump Market is meticulously segmented based on key functional and technical attributes including Type, Power Source, Capacity, End-User, and Regional Geography. Analyzing these segments provides a granular view of market dynamics, enabling stakeholders to identify high-growth niches and tailor their product development and marketing strategies accordingly. The dominance of specific segments, such as horizontal split case pumps and the industrial end-user sector, reflects the ongoing need for high-capacity, heavy-duty fire protection solutions critical for safeguarding vital infrastructure and mitigating catastrophic risks associated with large-scale industrial operations. Regional segmentation confirms Asia Pacific's burgeoning role as the principal demand center, driven by unprecedented construction and regulatory enforcement efforts.

Detailed evaluation reveals that the Power Source segmentation holds particular significance, with the ongoing global energy transition influencing purchasing decisions. While diesel remains crucial for redundancy in high-risk environments, the push for green building certifications and reduced carbon footprints is accelerating the shift toward electric fire pumps, especially in commercial and residential developments where power reliability is generally high. Capacity segmentation, ranging from low to high flow rates, directly correlates with the type of facility being protected; small commercial buildings typically require lower capacity systems, whereas large industrial complexes, such as power plants or chemical refineries, necessitate complex, high-pressure setups.

Understanding the End-User landscape is vital for specialized manufacturers. The industrial segment, encompassing sectors like oil & gas, manufacturing, and utilities, demands highly customized, explosion-proof, and certified systems, often representing the highest average transaction value. Conversely, the commercial and residential segments, while volume-driven, prioritize ease of installation, compliance with basic building codes, and integration with standardized sprinkler systems. These segmented insights are essential for accurate forecasting and strategic penetration across diverse application environments globally.

The value chain for the Fire Pump Market begins with upstream activities, predominantly focused on the sourcing and processing of critical raw materials, namely high-grade cast iron, stainless steel, bronze, and specialized alloys required for pump casings, impellers, and shafts. This phase also includes the manufacturing of specialized components such as certified electric motors, diesel engines, couplings, and control panels compliant with NFPA 20 standards. Efficiency in this initial stage is vital, as material cost volatility and compliance with stringent material specifications directly impact the final product cost and certification eligibility. Key relationships in the upstream segment involve long-term procurement contracts with metal foundries and specialized motor manufacturers.

Midstream activities involve the core manufacturing process, including precision machining, assembly, hydraulic testing, and critical certification by bodies like UL (Underwriters Laboratories) and FM Global. Manufacturers add value through proprietary hydraulic design expertise, ensuring optimal performance curves and reliability. Distribution channels are highly influential, relying heavily on specialized fire protection distributors, wholesalers, and professional system integrators who possess the technical expertise required for complex system design and installation. Direct sales channels are typically reserved for very large, customized industrial projects, whereas indirect channels dominate the commercial and residential segments.

Downstream activities focus on installation, commissioning, maintenance, and mandatory testing (as per NFPA 25). The downstream segment is highly localized and service-intensive, requiring trained technicians to ensure pumps are correctly integrated into the broader fire suppression system. Aftermarket services, including spare parts supply, routine testing, and preventative maintenance contracts, represent a significant revenue stream and a critical link in maintaining system integrity and long-term customer satisfaction. The efficiency of the indirect distribution channel, acting as the primary point of contact with end-users, directly influences market reach and service quality.

Potential customers for fire pump systems are diverse, extending across nearly every sector requiring substantial infrastructure and adherence to safety codes. The largest category of buyers includes EPC (Engineering, Procurement, and Construction) companies and general contractors involved in the development of new high-rise commercial buildings, industrial facilities, and municipal infrastructure projects. These entities are responsible for integrating the fire pump system into the overall building design and ensuring compliance prior to handover, typically prioritizing reliability, certification, and integration capability.

A second major customer segment comprises end-users who operate high-value or high-risk assets, necessitating premium fire suppression solutions. This includes owners and operators in the Oil & Gas sector (refineries, terminals), Power Generation (nuclear, thermal, renewable energy plants), and large-scale manufacturing (automotive, aerospace, pharmaceuticals). These customers demand highly resilient, often customized fire pump solutions with diesel backups, focused heavily on minimizing operational downtime and catastrophic loss protection. Their purchasing decisions are primarily governed by risk assessment and insurance requirements.

Finally, institutional and public sector buyers constitute a stable customer base, including governmental organizations, military bases, large healthcare facilities (hospitals), educational campuses, and vital infrastructure like airports and water treatment centers. These entities often procure fire pumps through mandated public tenders, prioritizing longevity, adherence to specific governmental standards, and comprehensive service contracts. The residential sector, specifically developers of high-density, multi-story residential towers, also represents a growing customer base driven by mandatory life safety codes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.45 Billion |

| Market Forecast in 2033 | USD 2.29 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Eaton, Xylem, Grundfos, SPP Pumps, Flowserve Corporation, KSB SE & Co. KGaA, Sulzer, Peerless Pump (Sterling Fluid Systems), Aurora Pump (Pentair), Armstrong Fluid Technology, Torishima Pump Mfg. Co., Ltd., Shaanxi Aerospace Power Hi-Tech, Viqua Pumps, Wilo Group, ITT Inc., CNP Pumps. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Fire Pump Market is increasingly centered on digitization, energy efficiency, and remote diagnostics, moving beyond traditional mechanical engineering. The most prominent technological shift involves the integration of Variable Speed Drives (VSDs) and sophisticated control panels. VSDs allow the pump motor speed to be modulated in response to real-time system demand, offering significant energy savings and reducing unnecessary wear and tear compared to fixed-speed pumps. This technology is critical for minimizing water hammer effects and maintaining precise pressure control, adhering to modern safety standards that emphasize system longevity and efficiency.

Another crucial technological area is the deployment of Internet of Things (IoT) sensors and connectivity modules. Modern fire pump systems are often equipped with sensors to monitor vital parameters such as suction pressure, discharge pressure, vibration levels, bearing temperatures, and motor current draw. This data is transmitted via secure networks to cloud-based monitoring platforms, enabling continuous, real-time performance assessment. This IoT integration facilitates predictive maintenance, allowing maintenance teams to anticipate and address potential component failures, thereby drastically increasing the reliability of mission-critical fire safety systems and ensuring compliance with mandatory testing procedures.

Furthermore, the materials science sector contributes significantly to the market, focusing on developing corrosion-resistant alloys and composite materials for pump components, particularly for applications in harsh environments such as marine or chemical processing facilities. Advances in hydraulic modeling and Computational Fluid Dynamics (CFD) are also utilized by leading manufacturers to optimize impeller and casing designs, maximizing hydraulic efficiency and reducing the overall footprint of the pump unit. The convergence of these technologies ensures fire pumps are not only compliant but also optimized for minimal operational cost and maximum responsiveness.

The geographical analysis of the Fire Pump Market reveals distinct growth trajectories and maturity levels across key regions, primarily influenced by local regulatory stringency, construction activity, and economic development levels. North America and Europe currently represent mature markets characterized by high compliance rates, established infrastructure, and a significant focus on retrofit projects and advanced monitoring technologies. The demand here is driven by the need to upgrade aging systems to meet newer energy efficiency and digital integration standards, creating robust opportunities for aftermarket services and sophisticated VSD pump solutions.

Asia Pacific (APAC) stands out as the primary engine of global market growth. Rapid urbanization, massive investment in industrial parks, data centers, and high-rise commercial structures in countries like China, India, and Southeast Asian nations are fueling unprecedented demand. Crucially, many governments in APAC are standardizing and rigorously enforcing building safety codes, mirroring global standards (such as NFPA), which mandates the installation of certified fire pump systems in virtually all new large-scale construction projects. This environment supports high-volume sales and manufacturing expansion within the region.

The Middle East and Africa (MEA), particularly the GCC states (Saudi Arabia, UAE), exhibit strong demand driven by large infrastructure and mega-project investments (e.g., NEOM, Dubai Expo developments). Due to the high value of assets and the often challenging environmental conditions (high temperatures, arid climate), there is a strong preference for high-quality, diesel-driven pumps and complex water systems requiring substantial capacity. Latin America also presents moderate growth, tied closely to economic stability and investment in infrastructure, though often constrained by varying levels of regulatory enforcement across different countries.

The market growth is primarily driven by rigorous enforcement of global fire safety standards, such as NFPA codes, and the accelerated pace of infrastructure development and urbanization, particularly in the Asia Pacific region, mandating the installation of certified fire suppression systems.

NFPA standards, particularly NFPA 20, govern the selection, design, and installation of fire pumps, ensuring minimum performance requirements (flow and pressure), reliability, and mandatory component specifications (motors, controllers). Compliance is mandatory for obtaining necessary building certifications.

Horizontal split case pumps typically hold the largest market share due to their high flow capacity, relatively simple maintenance access, and reliable performance across a wide range of industrial and large commercial applications requiring high volume water delivery.

IoT sensors facilitate real-time monitoring of pump parameters (vibration, pressure, temperature), enabling predictive maintenance algorithms to identify potential failures proactively. This reduces unexpected downtime, increases system reliability, and optimizes service schedules according to NFPA 25 testing requirements.

Yes, there is a distinct shift toward electric fire pumps in commercial and urban settings due to lower emissions, reduced maintenance complexity, and higher energy efficiency. However, diesel pumps remain essential in industrial, high-risk, and remote environments where power grid reliability is a concern or where mandated by safety redundancy requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.