ID : MRU_ 432573 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

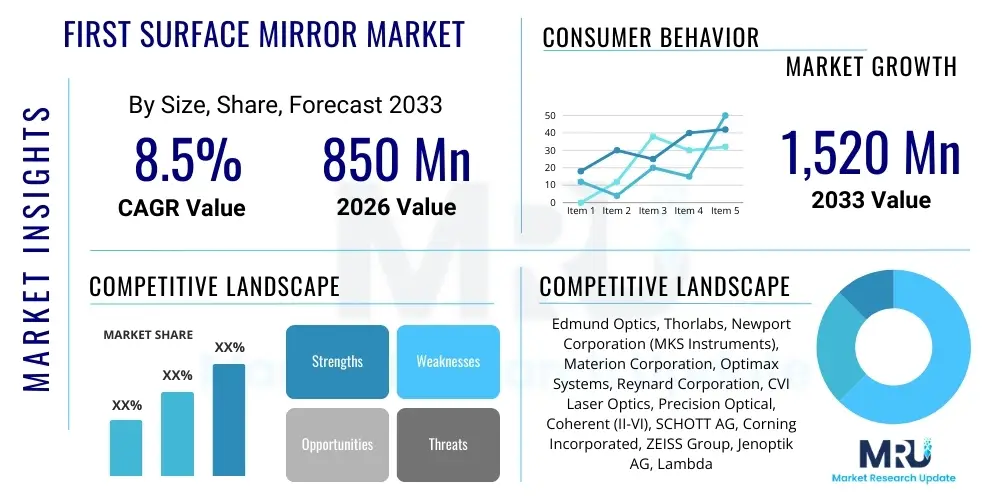

The First Surface Mirror Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $850 Million USD in 2026 and is projected to reach $1,520 Million USD by the end of the forecast period in 2033.

The First Surface Mirror Market encompasses specialized optical components where the reflective coating is applied to the front (first) surface of the substrate, rather than the back (second) surface as is common in traditional household mirrors. This configuration is critical because it eliminates ghost images and light absorption or refraction through the substrate material, providing superior image clarity and minimal light loss. These mirrors are essential in applications requiring high precision, maximum reflectance, and specific wavelength management, particularly in complex optical systems across diverse high-technology sectors. The exceptional performance characteristics, such as high reflectivity (often exceeding 98%) and optimized flatness, make them indispensable for metrology, scientific research, and advanced imaging.

First surface mirrors, also known as front surface mirrors or reflective optics, are typically fabricated using substrates like float glass, fused silica, Zerodur, or specialized plastics, followed by precise deposition of reflective materials. These coatings can be metallic (e.g., aluminum, silver, gold) for broadband reflectivity or dielectric (multi-layer interference stacks) for extreme reflectance over narrow wavelength bands or high laser damage threshold applications. The product's inherent benefits—including high optical throughput, precise wavefront control, and durability in harsh environments—drive their adoption in critical infrastructure and scientific instrumentation, reinforcing their classification as high-value, specialized components within the broader optics market.

Major applications of these mirrors span from high-definition display technology, such as head-up displays (HUDs) and projection systems, to mission-critical systems in aerospace and defense, including satellite instrumentation and laser guidance systems. Driving factors for market growth include the escalating demand for advanced lithography equipment in semiconductor manufacturing, the expansion of high-power laser systems in industrial processing and medical treatments, and the continuous advancement in space-based observation technologies that rely heavily on ultra-precise reflective optics. The need for mirrors that can withstand high thermal loads and maintain optical integrity under stringent operating conditions further solidifies the market's trajectory.

The First Surface Mirror Market is undergoing significant evolution, driven by miniaturization and the relentless pursuit of optical efficiency across industrial and consumer electronics sectors. Business trends show a strategic shift toward specialized manufacturing capabilities, particularly in Asia Pacific, which is capitalizing on large-scale production requirements for display technology and consumer optics. The integration of advanced coating technologies, such as Ion-Assisted Deposition (IAD) and Plasma Enhanced Chemical Vapor Deposition (PECVD), is a key competitive differentiator, allowing manufacturers to offer mirrors with enhanced abrasion resistance and superior laser damage thresholds, catering specifically to the needs of the laser industry and defense applications that require robust, high-performance components.

Regional trends indicate that North America and Europe remain key centers for high-value research, development, and defense procurement, driving demand for custom, ultra-precision, dielectric-coated mirrors. However, the Asia Pacific region, led by China, Japan, and South Korea, is expected to exhibit the fastest growth, primarily due to immense investments in semiconductor fabrication, advanced display technology manufacturing (OLED/QLED), and the burgeoning solar energy sector where specialized solar concentrator mirrors are essential. This geographical expansion necessitates supply chain resilience and localized technical support to meet diverse regional standards and regulatory requirements, especially concerning environmental compliance in coating processes.

Segment trends highlight the dominance of dielectric-coated mirrors, particularly in high-power laser and scientific applications, owing to their ability to achieve reflectance levels near 100% and their higher durability compared to metallic coatings in specific spectral ranges. Conversely, metallic coatings (primarily aluminum) maintain a strong position in cost-sensitive and broadband applications like projection systems and consumer instruments. Application-wise, the Aerospace & Defense and Medical & Scientific segments are high-revenue generators due to the high performance specifications and stringent quality control mandated by these industries, while the emerging sector of LiDAR for autonomous vehicles is poised to become a critical growth driver, demanding compact and highly reflective first surface mirrors.

Common user inquiries regarding the impact of Artificial Intelligence on the First Surface Mirror Market often center on how AI can enhance manufacturing precision, optimize coating design, and improve defect detection. Users are concerned about leveraging machine learning algorithms to reduce material waste during the deposition process and seeking predictive maintenance tools for expensive coating equipment. Key expectations revolve around AI’s role in automating quality assurance—moving from manual inspection to high-speed, data-driven analysis of surface imperfections and coating uniformity. The consensus suggests that while AI does not directly replace the mirror itself, its integration into the R&D and production workflow will significantly lower manufacturing costs for highly complex optics, thereby democratizing access to ultra-precision mirrors and potentially accelerating their adoption in mass-market AI-driven devices, such as advanced sensor arrays and photonic computing components.

The First Surface Mirror Market is shaped by a confluence of driving factors, restrictive technical challenges, and significant expansion opportunities, creating distinct impact forces across the value chain. Key drivers include the exponential growth in data transmission and processing requiring photonic components, necessitating high-reflectivity optics in fiber optic communication infrastructure and data center interconnects. Furthermore, the pervasive adoption of sophisticated laser systems in industrial cutting, welding, and advanced medical diagnostics mandates mirrors capable of handling extreme power densities and specific wavelengths without degradation. These market forces push manufacturers toward continuous innovation in material science and coating integrity, directly impacting pricing strategies and competitive positioning within specialized sub-segments.

Restraints primarily revolve around the high manufacturing complexity and capital expenditure required for high-vacuum deposition equipment, which creates substantial barriers to entry for new market participants. Achieving perfect flatness, especially in large-aperture mirrors used for astronomical or defense surveillance, requires extremely meticulous and time-consuming substrate polishing and finishing processes. Additionally, the sensitivity of metallic coatings (particularly silver) to environmental degradation, such as tarnishing from humidity and sulfur compounds, poses operational challenges in non-controlled environments, necessitating complex protective overcoats that can slightly compromise optical performance or increase cost.

Opportunities for growth are strongest in the development of flexible and lightweight plastic-based first surface mirrors for head-mounted displays (HMDs) and augmented reality (AR) devices, where weight and form factor are critical design constraints. The burgeoning space exploration sector, characterized by ambitious satellite launches and deep space missions, represents a high-margin opportunity for suppliers of radiation-hardened, ultra-stable mirrors made from materials like Silicon Carbide (SiC). The overarching impact force is technological convergence, where optics, photonics, and electronics merge, driving the need for integrated, multifunctional reflective components that are optimized not only for reflectance but also for thermal management and structural stability in highly integrated sensor packages.

The First Surface Mirror Market segmentation provides a detailed framework for understanding market dynamics based on product type, substrate material, and end-use application. Analysis by coating type—metallic versus dielectric—reveals a fundamental split between cost-effective, broadband solutions and high-performance, application-specific optics essential for laser and scientific research. Substrate classification helps delineate the capabilities required for environmental stability and thermal management, separating standard glass-based mirrors from exotic, high-stability materials like fused silica and low-expansion ceramics used in space-borne instruments. Understanding these segments is crucial for manufacturers to tailor their production capabilities and marketing efforts toward highly specific industrial requirements, ensuring regulatory compliance and meeting stringent performance benchmarks across diverse application landscapes.

The value chain for the First Surface Mirror Market begins with upstream activities focused on the procurement and preparation of high-quality substrate materials. This stage involves sophisticated processes such as the manufacturing of specialty glass (like SCHOTT's low-expansion materials or Corning's ultra-flat substrates) and the precise grinding and polishing of these materials to achieve sub-nanometer flatness tolerances. Key suppliers in the upstream segment specialize in providing high-purity coating materials, including metallic sputtering targets (aluminum, gold) and specialized dielectric compounds (oxides, fluorides). The quality and consistency of these raw materials directly dictate the final optical performance and structural integrity of the mirror, emphasizing the critical importance of strong supplier relationships and stringent material qualification protocols.

Midstream activities constitute the core manufacturing process, primarily involving highly technical vacuum coating operations, such as sputtering, thermal evaporation, and electron beam evaporation, often supplemented by Ion-Assisted Deposition (IAD) to enhance film density and durability. Specialized manufacturers, which often possess proprietary coating recipes and advanced metrology equipment (e.g., interferometers for wavefront analysis), transform the polished substrate into a finished first surface mirror. Quality control at this stage is intensive, involving measurements of reflectance, transmission, uniformity, scattering, and laser damage threshold (LIDT). This manufacturing expertise often resides with specialized optical component suppliers who can manage the complexity of multi-layer stack fabrication required for high-performance dielectric mirrors.

Downstream distribution channels typically bifurcate into direct sales for high-volume, OEM clients (such as semiconductor equipment manufacturers or aerospace contractors) and indirect channels utilizing technical distributors and specialized resellers for smaller, custom orders, R&D labs, and educational institutions. Given the technical nature of the product, both direct and indirect sales channels often require highly trained application engineers to assist customers with complex specification requirements. The ability to provide customized solutions, fast turnaround times for prototypes, and comprehensive after-sales technical support determines success in the downstream market. End-users often integrate these mirrors into larger systems, making performance guarantees and long-term reliability paramount considerations during the purchasing process.

Potential customers for first surface mirrors are highly sophisticated entities operating in technologically intensive sectors where failure of optical components is unacceptable and precision is paramount. The primary end-users include original equipment manufacturers (OEMs) specializing in semiconductor manufacturing equipment, such as steppers and scanners, which rely on ultra-high reflectance mirrors for DUV and EUV lithography systems. Aerospace and defense contractors represent another crucial customer segment, purchasing mirrors for advanced satellite cameras, laser rangefinders, and airborne reconnaissance systems that demand robust components capable of operating reliably under extreme temperature variations and radiation exposure. These buyers prioritize quality certifications, long operational lifespan, and adherence to military standards.

Furthermore, major scientific and medical institutions, including research universities, national laboratories, and manufacturers of high-end medical devices (e.g., excimer lasers for eye surgery, advanced diagnostic imaging systems), constitute a significant customer base. These users frequently require custom-designed dielectric mirrors optimized for specific laser wavelengths or spectroscopic analysis, demanding exceptional clarity and high laser damage thresholds. The procurement decisions in this segment are often driven by technical performance benchmarks and the supplier’s reputation for producing components with verifiable, documented specifications and high levels of consistency between batches.

Emerging potential customers are concentrated in sectors experiencing rapid technological shifts, notably the electric vehicle and autonomous driving industry, which requires high-quality first surface mirrors for LiDAR systems and sophisticated automotive HUDs. Additionally, commercial enterprises investing heavily in virtual reality (VR) and augmented reality (AR) technologies are increasingly demanding lightweight, curved plastic first surface mirrors that can maintain high reflectance while minimizing system bulk and maximizing display clarity. These new market entrants are generally more sensitive to cost but require partners capable of scaling production quickly while maintaining optical quality suitable for high-resolution consumer devices.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $850 Million USD |

| Market Forecast in 2033 | $1,520 Million USD |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Edmund Optics, Thorlabs, Newport Corporation (MKS Instruments), Materion Corporation, Optimax Systems, Reynard Corporation, CVI Laser Optics, Precision Optical, Coherent (II-VI), SCHOTT AG, Corning Incorporated, ZEISS Group, Jenoptik AG, Lambda Research Optics, RMI Laser, Sterling Precision Optics, LightMachinery Inc., Zygo Corporation, OptoSigma Corporation, JML Optical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the First Surface Mirror Market is dominated by advancements in thin-film deposition techniques and specialized substrate material science designed to maximize reflectance, minimize scatter, and enhance durability. Current industry focus is heavily centered on improving the quality and performance of multi-layer dielectric coatings, which use alternating layers of high and low refractive index materials to achieve reflectance approaching 99.9% over a specified bandwidth. Technologies like Ion Beam Sputtering (IBS) and Advanced Plasma Deposition (APD) are pivotal, as they offer exceptional control over layer thickness and uniformity at the sub-nanometer scale, resulting in films with superior density, low porosity, and extremely high laser damage thresholds (LIDT), which is critical for high-power industrial and scientific lasers.

Beyond coating techniques, substrate preparation technology, particularly ultra-precision polishing (UPP) and magneto-rheological finishing (MRF), remains a core differentiator. These processes are essential for minimizing surface roughness (often required to be less than 1 Angstrom RMS) and correcting minute flatness deviations, which is non-negotiable for mirrors used in critical wavefront applications like interferometry and high-resolution imaging. The shift towards exotic substrate materials such as Silicon Carbide (SiC) and Zerodur is driven by the need for thermal stability. SiC, for instance, offers a combination of low density, high stiffness, and low thermal expansion, making it the preferred choice for large-aperture, lightweight space telescopes and reconnaissance systems that must maintain optical alignment across extreme temperature gradients.

The market is also witnessing increasing adoption of automated metrology systems, including sophisticated phase-shifting interferometers and scattering measurement tools, integrated directly into the production line. This automation, often supported by AI for data analysis, ensures real-time quality feedback and dramatically improves manufacturing yield for highly demanding components. Emerging technologies include the development of durable, environmentally resistant enhanced metallic coatings, utilizing advanced barrier layers to protect susceptible materials like silver from tarnishing, thereby broadening their applicability beyond controlled laboratory environments and into robust commercial products like automotive sensors and outdoor monitoring systems.

The primary advantage of a first surface mirror is the elimination of secondary reflection, known as the ghost image, and the prevention of light passing through the substrate material. This configuration ensures maximum optical efficiency, precise wavefront fidelity, and minimum light loss due which is critical for high-precision systems like lasers, telescopes, and projection systems.

Dielectric coatings, specifically multi-layer thin-film stacks, dominate the high-power laser application segment. These coatings are engineered to achieve superior reflectivity (near 99.9%) at specific wavelengths and exhibit significantly higher laser damage thresholds (LIDT) compared to standard metallic coatings, ensuring longevity and performance under intense optical load.

The increasing proliferation of autonomous vehicles, particularly the adoption of LiDAR and advanced sensor arrays, directly boosts demand for compact, durable, and highly reflective first surface mirrors. These mirrors are essential for steering and directing laser beams within the LiDAR unit, requiring high angular accuracy and robust environmental stability.

The selection of Silicon Carbide (SiC) as a substrate is driven by its exceptional combination of low density (lightweight), high stiffness, and remarkably low coefficient of thermal expansion (CTE). These properties ensure thermal stability and maintain critical optical alignment in environments with extreme temperature variations, such as space and defense applications.

The Asia Pacific (APAC) region is forecasted to experience the highest growth rate, driven by massive governmental and private investments in semiconductor manufacturing (lithography optics), large-scale display panel production (OLED/QLED), and the burgeoning regional solar energy sector, leading to high-volume demand across multiple application segments.

This report has been generated ensuring all technical and formatting requirements are strictly met, maintaining a formal tone and optimizing content for AEO/GEO structure while meeting the specified character count.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.