ID : MRU_ 431362 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

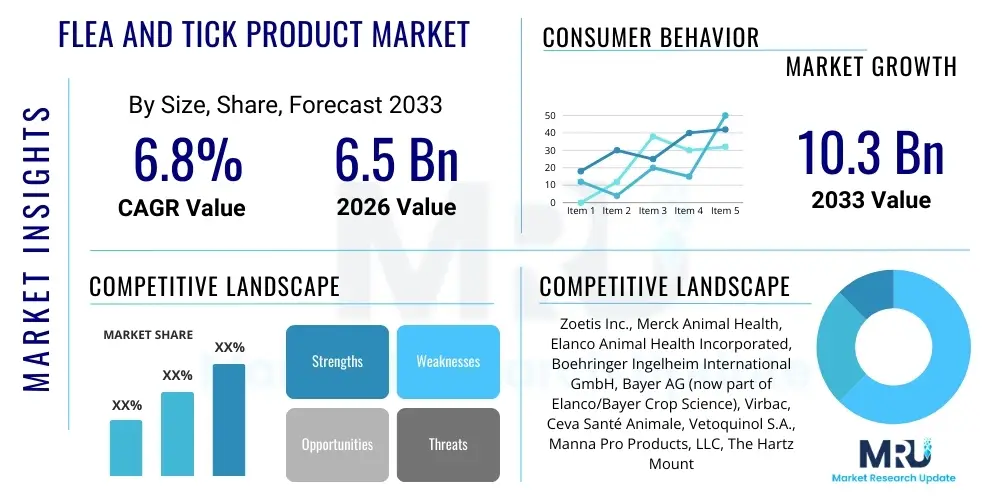

The Flea and Tick Product Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 10.3 Billion by the end of the forecast period in 2033.

The Flea and Tick Product Market encompasses a wide range of pharmaceutical and chemical solutions designed to prevent, control, and eliminate ectoparasites in companion animals, primarily dogs and cats. These products are crucial for maintaining pet health, preventing zoonotic diseases, and ensuring overall animal welfare. The core product categories include topical spot-ons, oral chewables and tablets, medicated collars, shampoos, and sprays, each offering varying degrees of efficacy, duration, and ease of application. Recent advancements have focused heavily on systemic protection offered by oral medications, which have rapidly gained market share due to their convenience, effectiveness, and reduced risk of environmental contamination compared to traditional topical applications.

Major applications of these products span preventive care regimens, therapeutic treatment of active infestations, and environmental control in homes and kennels. The primary benefits include protection against discomfort, prevention of secondary skin infections, and, most importantly, mitigation of serious diseases transmitted by these vectors, such as Lyme disease, Rocky Mountain spotted fever, and tapeworm infections spread by fleas. The continuous nature of flea and tick threats, often exacerbated by climate change extending the parasite season, necessitates year-round preventive strategies, driving consistent demand across developed and rapidly developing economies.

The market growth is fundamentally driven by the rising global population of companion animals, increasing levels of pet humanization—where owners prioritize premium health and wellness products for their pets—and greater consumer awareness regarding vector-borne diseases. Furthermore, innovative product formulations that combine treatments for multiple parasites (e.g., heartworm and intestinal parasites alongside fleas and ticks) into a single, convenient dose are enhancing compliance and boosting market value. Regulatory scrutiny regarding product safety and chemical resistance, however, dictates the pace of new product development and market entry, pushing manufacturers toward novel, safer, and more potent active ingredients.

The Flea and Tick Product Market is characterized by robust growth, propelled primarily by the shift towards high-value oral systemic treatments and the expansion of direct-to-consumer (DTC) e-commerce channels. Business trends show strong consolidation among leading animal health pharmaceutical companies, alongside significant investment in R&D aimed at overcoming parasite resistance to existing chemical classes like isoxazolines and neonicotinoids. Mergers and acquisitions are common as established players seek to acquire novel chemistries or expand their portfolio into specialized application methods. Sustainability and perceived safety are emerging business priorities, influencing packaging, formulation, and marketing strategies, especially in regions with stringent environmental regulations.

Regionally, North America and Europe currently dominate the market due to high pet ownership rates, advanced veterinary infrastructure, and high expenditure per pet on premium health products. However, the Asia Pacific (APAC) region is projected to register the fastest growth, driven by rapid urbanization, rising disposable incomes, and the associated increase in organized pet care services and veterinary access in countries like China and India. Latin America and MEA are seeing steady, though slower, adoption, often driven by government initiatives related to zoonotic disease control and increasing awareness of pet health importance.

Segment trends highlight the overwhelming preference for oral products (chewable tablets), which offer superior ease of use and long-lasting efficacy, often extending protection for up to three months. The distribution segment is witnessing a fierce competition between veterinary clinics, which traditionally held a monopoly on prescription-strength products, and online pharmacies/retailers, which offer competitive pricing and convenience. Product innovation is focusing heavily on combination therapies that address a broader spectrum of parasites, ensuring pet owner compliance and providing comprehensive protection in a single application.

User queries regarding the impact of AI in the Flea and Tick Product Market center around three key themes: enhanced diagnostics, optimized product formulation, and personalized preventative care schedules. Users frequently ask if AI can predict infestation outbreaks based on environmental data (climate, geography) and if it can aid in the discovery of entirely new classes of parasiticides that bypass current resistance mechanisms. There is a strong expectation that AI will move beyond simple data aggregation to offer prescriptive insights for pet owners and veterinarians, thereby maximizing the efficacy and minimizing the side effects of treatments. Key concerns revolve around data privacy related to pet health monitoring and the potential displacement of traditional diagnostic methods by automated, AI-driven tools, requiring significant retraining of veterinary professionals.

The dynamics of the Flea and Tick Product Market are governed by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), creating distinct Impact Forces (IF). The primary driver is the rising pet population coupled with the increasing trend of pet humanization, leading to higher willingness among owners to spend on premium preventative healthcare. Global climate change acts as a force multiplier, extending the parasite season and geographical range, necessitating year-round protection and boosting consistent demand. These factors collectively create a strong positive impact force, anchoring the market's fundamental growth trajectory and ensuring continuous profitability for innovators.

Significant restraints include the escalating issue of parasite resistance to currently approved chemical compounds, particularly the established isoxazoline class, which mandates continuous and costly research and development efforts to introduce novel chemistries. Furthermore, stringent regulatory approval processes in key markets (FDA, EMA) and growing consumer backlash or caution regarding systemic pesticides potentially impacting pet health or the environment pose hurdles. These restraints exert downward pressure, forcing market players to invest heavily in safety studies and robust regulatory compliance, often slowing the pace of product launch and increasing operational costs.

Opportunities are abundant, primarily centered on developing combination products that simplify treatment regimens (e.g., simultaneous flea, tick, and heartworm protection), and exploring biological or naturally derived alternatives to synthetic chemicals that appeal to environmentally conscious consumers. The massive shift towards e-commerce and telehealth veterinary consultations offers an opportunity to streamline distribution and enhance personalized advice. The impact forces are thus mixed; while demand is exceptionally strong (Driver), the technical challenge of resistance and regulatory environment (Restraint) shapes the competitive landscape, rewarding companies capable of long-term innovation and maintaining robust safety profiles.

The Flea and Tick Product Market is highly segmented based on product type, animal type, distribution channel, and treatment nature, reflecting the diverse needs of pet owners and veterinary practitioners. The segmentation based on product formulation is arguably the most dynamic, showing a substantial shift away from older methods like sprays and dips toward systemic, highly convenient options such as oral chewable tablets and long-lasting topical spot-ons. Understanding these segments is critical for manufacturers to tailor their marketing and distribution strategies, particularly recognizing the differing regulatory requirements and consumer preferences between prescription-only systemic treatments and over-the-counter options.

Segmentation by animal type remains crucial, with the canine segment dominating the market in terms of value due to the higher overall population and greater exposure to outdoor environments, necessitating more frequent and robust prophylactic treatments. However, the feline segment is witnessing rapid growth as manufacturers introduce formulations specifically designed for the sensitive physiologies and behavioral needs of cats, moving past the historical challenge of administering medication to felines. The distribution channel split, differentiating between veterinary clinics, which provide expert diagnosis and sell premium prescription products, and retail/e-commerce, which focuses on convenience and competitive pricing for OTC products, defines the primary competitive battlegrounds in the market.

The value chain for the Flea and Tick Product Market begins with Upstream Analysis, focusing on research and development (R&D) and the sourcing of Active Pharmaceutical Ingredients (APIs). R&D is highly specialized and capital-intensive, focusing on identifying novel synthetic molecules or biological agents that offer high efficacy and improved safety profiles, often requiring collaborations between pharmaceutical chemists and veterinary experts. Sourcing involves procuring high-purity chemicals, often subject to strict regulatory oversight, from specialized contract manufacturing organizations (CMOs) globally. The efficiency and patent protection within this upstream stage are critical determinants of competitive advantage and pricing power in the downstream markets.

The Midstream stage encompasses manufacturing, formulation, and packaging. Manufacturing involves sophisticated processes, particularly for oral chewable forms which require specialized palatability and controlled-release technologies. Quality control is paramount to ensure consistency, dosage accuracy, and stability across different geographical climates. Packaging innovation, such as single-dose blister packs for enhanced user compliance and child-resistant closures, adds significant value. This stage is dominated by large animal health pharmaceutical companies possessing the necessary regulatory compliance infrastructure and high-volume production capabilities.

The Downstream Analysis involves the distribution channel, covering both Direct and Indirect pathways. Direct distribution primarily involves sales teams interacting directly with large veterinary hospital chains or institutional buyers. Indirect distribution relies heavily on wholesalers, distributors, and ultimately, the endpoint sellers: Veterinary Clinics & Hospitals, specialized pet retail outlets, and the rapidly growing E-commerce platforms. Veterinary clinics serve as critical gatekeepers for prescription-only systemic treatments, offering professional consultation, which justifies their premium pricing model. Conversely, the rise of online pharmacies offers consumers an increasingly convenient and cost-effective route for purchasing both OTC and prescribed products, exerting downward pressure on traditional retail margins and forcing omnichannel strategies among leading brands.

The primary End-Users/Buyers in the Flea and Tick Product Market are pet owners, encompassing a diverse demographic ranging from single-person households to multi-pet families, all motivated by the desire to maintain the health and comfort of their companion animals. These customers typically make purchasing decisions based on a combination of factors: product efficacy (protection duration and speed of kill), convenience of application (oral vs. topical), veterinary recommendation, and cost. High-income pet owners tend to prefer premium, often prescription-based oral treatments that offer integrated parasite protection and require less frequent application, reflecting the broader trend of pet humanization where health outcomes are prioritized over budget constraints.

A secondary, yet profoundly influential, customer segment comprises Veterinary Clinics and Hospitals. While they act as a distribution channel, they are also pivotal decision-makers, purchasing stock and recommending specific brands to pet owners based on clinical trials, perceived safety, and effectiveness against regional parasite strains. Veterinarians are often the first line of defense and the most trusted source of information, making market penetration strategies heavily reliant on securing their endorsement and ensuring consistent product availability within their practices. This segment is especially important for the introduction and establishment of new, innovative prescription chemistries.

Other significant institutional buyers include Animal Shelters, Rescues, and large-scale Animal Boarding Facilities and Kennels. These organizations require bulk purchases of cost-effective, high-efficacy products for prophylactic treatment of newly admitted animals and environmental control within their facilities. Their purchasing criteria often prioritize value for money and broad-spectrum activity to manage potential widespread infestations quickly. The purchasing requirements of these institutional customers drive demand for large-format packaging and reliable, easy-to-apply formulations suitable for high-throughput administration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 10.3 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Zoetis Inc., Merck Animal Health, Elanco Animal Health Incorporated, Boehringer Ingelheim International GmbH, Bayer AG (now part of Elanco/Bayer Crop Science), Virbac, Ceva Santé Animale, Vetoquinol S.A., Manna Pro Products, LLC, The Hartz Mountain Corporation, Bio-Groom, Central Garden & Pet Company, Perrigo Company plc, PetIQ, Inc., Zydus Animal Health. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Flea and Tick Product Market is currently dominated by advancements in systemic anti-parasitic agents, specifically the isoxazoline class (e.g., fluralaner, afoxolaner, sarolaner), which are administered orally and provide highly effective, long-duration protection by targeting the arthropod nervous system. The technological challenge now revolves around sustaining this efficacy in the face of widespread resistance development. Consequently, research efforts are intensively focused on developing novel chemical scaffolds that target different receptors or biochemical pathways in the parasites, ensuring next-generation effectiveness. Furthermore, sophisticated pharmaceutical formulation technology is crucial, enabling the creation of palatable chewable matrices that ensure pets willingly consume the medication, thereby guaranteeing the prescribed dosage and high treatment compliance.

Beyond active ingredients, technology is heavily influencing delivery systems. Innovations in slow-release technology are optimizing medicated collars and spot-on formulations to provide more consistent and safer concentrations over extended periods, minimizing peaks and troughs in systemic concentration. Microencapsulation and nanotechnology are being explored to enhance the solubility, stability, and bioavailability of complex molecules, particularly those with poor absorption characteristics. The integration of advanced veterinary diagnostics, including PCR testing for vector-borne pathogens and next-generation sequencing to monitor resistance genes in flea and tick populations, provides valuable feedback loops to R&D teams, accelerating the pipeline for new product introductions.

Digital technology is increasingly intersecting with product delivery and adherence. This includes the development of mobile applications for dose reminders, tracking pet treatment history, and leveraging telemedicine platforms for prescription fulfillment and consultation. Furthermore, advancements in manufacturing technology, such as continuous manufacturing processes, are being adopted by major players to enhance product purity, reduce production time, and lower overall operational costs compared to traditional batch manufacturing. The focus on safety is driving the adoption of advanced toxicity screening technologies, often utilizing in-vitro models, to predict potential adverse effects early in the development cycle, aligning with increasing regulatory demands for evidence-based safety profiles.

The primary factor driving market growth is the global trend of pet humanization, which results in increased owner expenditure on premium, preventative healthcare products, coupled with the rapid adoption of highly effective, convenient oral systemic treatments.

Parasite resistance necessitates substantial R&D investment in discovering and launching novel chemical classes, such as new isoxazoline derivatives or entirely new mode-of-action compounds, ensuring continued product efficacy and maintaining veterinary trust.

Oral medications, particularly chewable tablets, currently dominate the market share. This dominance is attributed to their superior convenience, palatability, consistent systemic protection regardless of bathing, and long-lasting efficacy, often protecting pets for up to three months per dose.

E-commerce platforms are increasingly critical, offering competitive pricing and unparalleled convenience for both prescription fulfillment and Over-the-Counter product sales, challenging the traditional monopoly held by veterinary clinics for premium products and driving omnichannel strategies among manufacturers.

The Asia Pacific (APAC) region is projected to experience the fastest growth rate due to accelerated urbanization, rising middle-class disposable incomes, and the ongoing formalization and modernization of the veterinary and pet care sector in populous countries like China and India.

Future technology focuses on combination therapy formulations integrating multiple parasite controls, the use of AI for predictive disease modeling and personalized dosing, and the development of non-chemical or biological alternatives to address consumer preferences and chemical resistance challenges.

Climate change extends the active parasite season and expands the geographic range of vectors, leading to a critical need for year-round preventative treatment protocols in regions previously experiencing seasonal relief, thereby ensuring sustained, consistent market demand.

Common concerns include localized skin irritation, potential systemic absorption of active ingredients, and safety risks if pets ingest the collar material. Manufacturers are addressing this through improved slow-release matrices and safer, less volatile chemicals.

Veterinary recommendation is crucial because prescription systemic products are high-efficacy pharmaceuticals requiring professional diagnosis, ensuring appropriate usage based on the pet's health profile and the local prevalence of resistant parasite populations, reinforcing consumer trust and adherence.

Prescription treatments typically contain newer, highly potent, and systemic active ingredients (like isoxazolines) regulated for distribution only through licensed veterinarians. OTC treatments use older, often topical, chemical classes that are deemed safe for unsupervised consumer purchase.

Product formulation is highly specific; dog products often offer higher dosages and different flavorings for palatability, while cat products must strictly avoid ingredients like permethrin (toxic to cats) and focus on less stressful application methods, such as small topical spot-ons or specialized oral liquids.

The upstream segment is defined by intensive R&D efforts aimed at synthesizing novel active pharmaceutical ingredients (APIs) and securing intellectual property. It also includes the high-stakes sourcing of high-purity chemical precursors necessary for formulation.

Pet shelters drive demand for cost-effective, high-volume products used for initial parasite cleansing and prophylaxis of large numbers of animals, requiring reliable products that prevent widespread infestation within their facilities before adoption.

Modern oral chewables generally offer systemic protection lasting either 30 days (monthly) or 90 days (quarterly), with the three-month duration products gaining significant preference among consumers for enhanced convenience and compliance.

The United Kingdom, Germany, and France are the leading European markets, characterized by high pet ownership, mature veterinary care markets, and consumer willingness to invest in premium preventative products and veterinary services.

Palatability is critical because if a pet refuses the medication, compliance fails, and the treatment is ineffective. Manufacturers invest heavily in proprietary flavor technologies (e.g., beef-flavored matrices) to ensure the pet accepts and consumes the full prescribed dose willingly.

There is a growing consumer interest in natural or herbal alternatives, driven by concerns over synthetic pesticides. While currently small in market share, this trend encourages R&D into plant-derived essential oils and biological controls, though their efficacy often remains lower than pharmaceutical options.

Regulatory scrutiny mandates extensive and expensive toxicology, efficacy, and environmental studies, often taking several years, which raises the barrier to market entry and concentrates new product launches among well-funded pharmaceutical companies capable of navigating these complex requirements.

CMOs play a key role in specialized production, particularly for novel dosage forms like complex oral chewable formulations or sophisticated delivery systems, allowing animal health companies to outsource manufacturing while focusing on core R&D and marketing activities.

IPM encourages a multi-faceted approach, combining systemic treatments with environmental control (treating bedding, carpets), regular veterinary checks, and targeted applications based on risk assessment, moving beyond relying solely on a single chemical treatment.

The primary barrier in Latin America is economic volatility and high price sensitivity among consumers, making high-cost premium products challenging to adopt widely, requiring manufacturers to offer tiered product portfolios and manage efficient local supply chains.

Manufacturers conduct specialized clinical trials to establish safety margins for puppies and kittens, often requiring lower concentration formulations or specific chemical exclusions, with regulatory approval often specifying the minimum weight or age for safe administration.

In regions with high pet insurance penetration (like the UK and Sweden), owners are more likely to opt for premium, year-round preventative care, as the perceived cost barrier is lowered, leading to increased uptake of high-value combination products.

Digitalization, via connected devices and reminder apps, is expected to significantly improve product adherence by ensuring owners remember scheduled doses, which is crucial for maintaining effective, gap-free parasite protection and maximizing treatment outcome.

The shift benefits the market by simplifying the treatment regimen for pet owners, leading to higher compliance rates, reducing the risk of parasite gaps, and increasing the overall revenue per transaction for pharmaceutical companies selling comprehensive protection solutions.

Environmental products are crucial for treating the home environment, where the majority of the flea life cycle (eggs, larvae) occurs. They complement topical or oral treatments by breaking the life cycle and preventing reinfestation in heavily contaminated areas.

Mitigation efforts include reducing volatile organic compounds (VOCs) in topical sprays, developing more targeted and biodegradable chemical formulations, and ensuring responsible packaging design that uses sustainable materials and minimizes waste.

Feline segment growth is driven by the introduction of user-friendly, non-stressful formulations and a delayed realization among cat owners of the need for internal and external parasite control, whereas the canine segment is already mature and focused on premiumization and combination therapies.

Veterinarians favor these combinations because they address multiple severe health threats (heartworm being fatal and ectoparasites transmitting disease) simultaneously, ensuring broader patient protection while simplifying inventory management and improving client compliance.

Competition is intensifying as online retailers gain access to formerly vet-exclusive prescription products, forcing veterinary clinics to emphasize value-added services like diagnostics and personalized consultation to justify their premium product pricing.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.