ID : MRU_ 432233 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

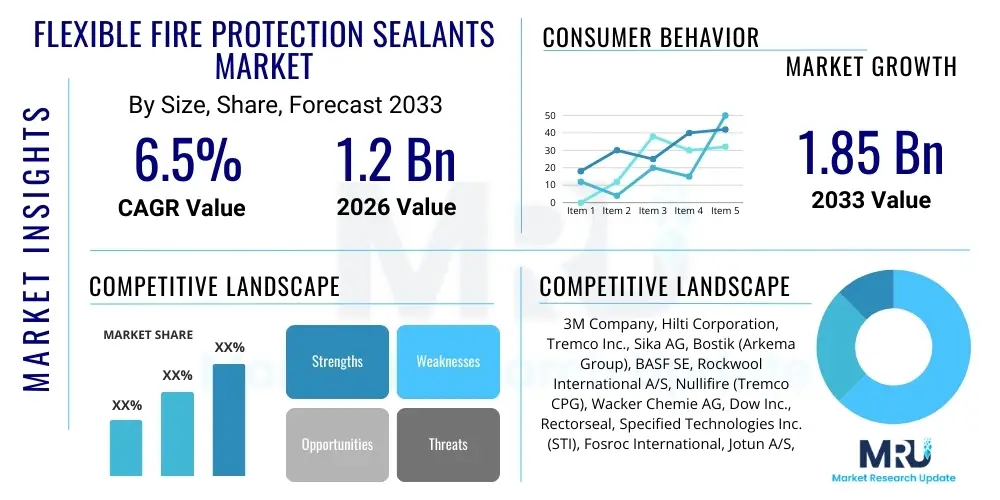

The Flexible Fire Protection Sealants Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 1.85 Billion by the end of the forecast period in 2033.

The Flexible Fire Protection Sealants Market encompasses specialized chemical formulations designed to prevent the passage of fire, smoke, and toxic gases through gaps, joints, and penetrations in fire-rated constructions. These sealants are crucial components within passive fire protection systems, maintaining the integrity of fire compartments by accommodating movement within building structures—a key differentiation from rigid firestopping materials. The core functionality relies on intumescent properties, where the sealant expands significantly when exposed to high temperatures, creating a robust, insulating char layer that seals the breach. This performance is governed by stringent international building codes, including standards set by organizations such as ASTM, UL, and EN, ensuring reliability in critical life safety applications across various structural typologies.

Product categories primarily include acrylic, silicone, polyurethane, and hybrid polymer sealants, each optimized for specific applications based on substrate compatibility, joint movement requirements, and required fire resistance rating. Acrylic firestopping sealants are generally cost-effective and suitable for less movement-intensive joints, whereas silicone sealants offer superior flexibility, UV resistance, and longevity, making them ideal for exterior facades and high-performance environments. The major applications span critical infrastructure, commercial buildings, residential complexes, and industrial facilities, particularly where electrical or mechanical services penetrate fire-rated walls and floors, or where expansion joints necessitate dynamic firestopping solutions.

The principal driving factors fueling market expansion are the escalating global focus on fire safety compliance, particularly in developing economies experiencing rapid urbanization and regulatory tightening, and the increasing complexity of modern building designs that incorporate lightweight materials and extensive service penetrations. Furthermore, the undeniable benefits these sealants offer—including life preservation, asset protection, and compliance assurance—cement their indispensable role in the construction industry. Manufacturers are continuously innovating to improve ease of application, reduce Volatile Organic Compound (VOC) emissions, and enhance long-term performance stability, meeting the dual demands of sustainability and robust safety standards.

The Flexible Fire Protection Sealants Market is poised for sustained growth, driven fundamentally by robust global construction spending, particularly in the commercial and residential sectors, coupled with increasingly strict governmental mandates regarding passive fire protection. A defining business trend is the shift toward high-performance, environmentally friendly formulations, emphasizing low-VOC and halogen-free products to meet evolving green building certifications and enhance installer safety. Strategic mergers, acquisitions, and partnerships are common as key players seek to broaden their product portfolios, secure distribution channels, and gain access to specialized technologies, particularly in hybrid sealant chemistry which combines the best attributes of silicones and polyurethanes for versatile application.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, fueled by massive infrastructure investments in countries like China, India, and Southeast Asian nations, where adherence to modern fire codes is rapidly improving. North America and Europe, characterized by established regulatory frameworks and high labor costs, prioritize premium, pre-qualified, and easy-to-install systems, including innovative packaging like foil packs and specialized application guns that improve installation efficiency and reduce material waste. European market growth is particularly sensitive to rigorous CE marking and Euroclass fire performance standards, driving demand for products tested under realistic end-use conditions. The Middle East and Africa (MEA) region shows strong potential, spurred by large-scale commercial and residential construction projects requiring sophisticated passive fire protection solutions to comply with international insurer requirements and local municipal codes.

Segment trends highlight the dominance of silicone-based sealants in terms of value, owing to their superior longevity, movement capability, and stability, essential for high-rise and seismic zones. However, the fastest growth trajectory is anticipated in the hybrid/specialty polymer segment, favored for its balanced performance and better adhesion to complex modern substrates. The commercial construction end-use sector remains the largest consumer, driven by extensive compartmentation requirements in hospitals, schools, and office towers. Furthermore, the specialized industrial sector, particularly oil and gas facilities and chemical processing plants, demands high-specification sealants resistant to harsh environmental conditions and explosive risks, commanding premium pricing and stringent qualification procedures.

User inquiries regarding the influence of Artificial Intelligence (AI) on the Flexible Fire Protection Sealants Market frequently center on how AI can enhance regulatory compliance, optimize material formulation, and revolutionize inspection and maintenance procedures. Common themes involve the potential for AI-driven predictive modeling to anticipate material degradation under various environmental stresses, the use of computer vision for automated quality control during manufacturing, and leveraging machine learning algorithms to optimize supply chain logistics and inventory management for complex firestopping projects. Concerns often revolve around the initial investment required for digitalization and the necessity of standardizing digital inputs (e.g., BIM data) across the fragmented construction industry to realize AI's full benefits.

AI is expected to significantly accelerate the research and development pipeline for new sealant materials. By analyzing vast databases of chemical structures, thermal properties, and fire test results, machine learning models can predict the performance of novel intumescent compounds, reducing the time and cost associated with iterative physical testing. Furthermore, in the operational phase of construction, AI tools integrated with Building Information Modeling (BIM) platforms can automatically verify that sealant specifications meet project requirements and local codes, ensuring accurate material selection and placement validation before physical installation, thereby minimizing human error and potential regulatory pitfalls during final certification. This shift elevates the role of digital compliance and intelligent system management within the passive fire protection domain.

Beyond material science and design integration, AI-powered tools are transforming post-installation asset management. Drones and robotic systems equipped with high-resolution imaging and AI analytics can perform rapid, comprehensive inspections of installed firestopping systems in inaccessible areas. These systems identify defects, gaps, or signs of material aging with greater precision and speed than manual inspection, generating automated compliance reports and scheduling proactive maintenance interventions. This transition towards 'smart' passive fire protection reduces lifetime operating costs, enhances system reliability, and ensures continuous compliance throughout the building's lifecycle, addressing a critical pain point for facility managers and regulatory bodies.

The Flexible Fire Protection Sealants Market is predominantly shaped by stringent regulatory landscapes and the inherent demands of building safety, which serve as foundational drivers. The primary driving force is the universal adoption and continuous updating of international and regional building codes that mandate specific fire resistance ratings and compartmentation strategies for all new and renovated structures. This regulatory pressure ensures sustained demand regardless of immediate economic fluctuations. Conversely, a major restraint is the volatility in the cost and supply of key raw materials, particularly specialty polymers like silicone and certain intumescent additives, which are often petrochemical derivatives or rely on complex manufacturing processes, introducing cost pressure across the value chain. Opportunities lie in the rapidly expanding retrofit and renovation markets in mature economies, where aging infrastructure requires upgrades to meet modern fire safety standards, providing a continuous secondary revenue stream beyond new construction.

The impact forces within this market are significant and interconnected. Technological advancements play a critical role; the continuous introduction of sealants offering superior adhesion to difficult substrates (e.g., cross-laminated timber, specialized plastics) and those with ultra-low-VOC content creates competitive differentiation and drives price premiums for high-quality products. Economic forces, such as fluctuating interest rates and overall construction activity, directly influence market volume, but the regulatory necessity of firestopping acts as a buffer against severe downturns. Social forces, particularly increasing public awareness regarding fire safety and indoor air quality, accelerate the adoption of non-toxic, sustainable sealant alternatives, pushing manufacturers towards greener chemistry and reduced environmental footprint, reinforcing the opportunity segment related to sustainable building practices and certifications like LEED.

Furthermore, substitution risk remains a persistent, albeit moderate, impact force. While flexible sealants are indispensable for dynamic joints and complex penetrations, competition exists from rigid firestopping mortars, pre-formed collars, and specialized composite boards in certain static applications, necessitating continuous product differentiation based on installation ease and performance metrics. The competitive rivalry among existing players is intense, characterized by large multinational chemical corporations leveraging scale and robust certification portfolios, alongside specialized niche players focused on specific application challenges or proprietary material science. This rivalry pushes down manufacturing costs and accelerates performance improvements, ultimately benefiting the end-user by ensuring a reliable supply of certified, innovative safety products. Successfully navigating this competitive landscape requires excellence in product certification, supply chain resilience, and strong technical support services.

The Flexible Fire Protection Sealants Market is comprehensively segmented based on product type, end-use application, and distribution channel, providing a granular view of market dynamics and specialized demand centers. Segmentation by product type—encompassing silicone, acrylic, polyurethane, and others (e.g., hybrid, epoxy)—reflects the material science driving performance characteristics such as movement capacity, longevity, and thermal behavior. Silicone sealants, known for their high temperature resistance and excellent elasticity, typically command the highest market value, especially in high-performance or external applications. Conversely, acrylic sealants remain the volume leader due to their cost-effectiveness and ease of use in general internal compartmentation within residential and light commercial structures, driving growth in emerging markets where budget sensitivity is high.

The segmentation based on end-use application delineates the primary demand sectors, including commercial, residential, industrial, and infrastructure. Commercial construction, encompassing hospitals, office buildings, and retail centers, represents the largest and most demanding sector due to complex service penetrations and strict occupancy safety requirements, mandating high fire ratings (typically FRL 120 or FRL 240). The residential segment, while requiring less stringent ratings in some jurisdictions, contributes significant volume, driven by high-density urban housing projects. Industrial facilities, such as power plants and data centers, require highly specialized sealants offering chemical resistance and extreme temperature performance. Analyzing these end-use segments is crucial for manufacturers to tailor product specifications, certification protocols, and distribution strategies effectively, aligning product benefits with specific industry needs and regulatory mandates.

A key trend within segmentation analysis involves the increasing specialization within the "Others" product category, particularly the growth of hybrid polymer sealants. These materials combine the advantages of various chemistries, offering improved adhesion without primers and better paintability than traditional silicones, positioning them as highly versatile solutions for contractors seeking multi-purpose firestopping products that simplify inventory management. Understanding the interplay between material properties and application requirements allows for precise market positioning, such as targeting the burgeoning demand for highly flexible sealants specifically engineered for timber construction projects which experience greater structural movement and necessitate specialized adhesion characteristics to comply with fire separation codes.

The Value Chain for Flexible Fire Protection Sealants commences with upstream activities involving the procurement and synthesis of highly specialized raw materials. This stage is dominated by large chemical producers supplying key components such as silicone polymers (PDMS), acrylic monomers, polyurethane prepolymers, and critical intumescent additives (e.g., graphite, vermiculite, sodium silicate) and fillers. The quality and cost of these raw materials significantly impact the final product performance and pricing, leading to intense negotiations and long-term contracts between sealant manufacturers and primary chemical suppliers. Research and development activities, focused on enhancing thermal stability, movement capability, and environmental compliance (low-VOC), are deeply embedded in this upstream stage, driving innovation in polymer science and intumescent technology, often necessitating significant capital investment in specialized compounding and blending equipment.

Midstream activities involve the formulation, manufacturing, and packaging of the final sealant products. Leading manufacturers operate sophisticated blending facilities where polymers, fillers, plasticizers, and flame-retardant additives are precisely combined under strict quality control measures to achieve desired physical properties and fire ratings, which must be validated through expensive third-party testing and certification (UL, Intertek, etc.). Efficiency in manufacturing—reducing cure times and optimizing batch sizes—is a major focus to maintain competitive pricing. Downstream activities involve market distribution and end-user application. The distribution channel is bifurcated into direct sales to large construction firms or specialized passive fire protection contractors, and indirect sales through a vast network of chemical distributors, hardware retailers, and specialized construction material suppliers. Direct sales often include technical support and training for complex industrial applications, while indirect sales focus on high-volume, readily available products for general construction.

The channel structure heavily influences market reach and service provision. Distributors play a crucial role in managing inventory, handling logistical complexities, and providing immediate local availability, essential for time-sensitive construction projects. Technical support and training provided by manufacturers or specialized distributors are critical, as the correct installation of fire sealants is paramount for life safety performance; even minor application errors can compromise the fire rating of an entire building element. Therefore, the value capture extends beyond material production to include professional services, certification management, and ongoing technical consultation, solidifying the importance of a robust, technically capable downstream network capable of ensuring proper installation compliance across diverse global regulatory environments and specialized projects.

Potential customers for Flexible Fire Protection Sealants are diverse, spanning the entire construction ecosystem, but are fundamentally categorized by their role in specifying, purchasing, or installing passive fire protection systems. General contractors and sub-contractors specializing in mechanical, electrical, and plumbing (MEP) systems constitute a significant customer base, as they are responsible for ensuring that all service penetrations through fire barriers are correctly sealed according to building plans and regulatory codes. Specialized passive fire protection (PFP) contractors represent a high-value customer segment, as they possess the expertise and certifications required to install complex firestopping systems in large commercial and industrial projects, often requiring tailored product specifications and comprehensive documentation packages for regulatory sign-off, making technical performance and ease of certification paramount purchase criteria.

Building owners, facility managers, and real estate developers are also critical end-users, particularly in the retrofit and maintenance markets. These customers prioritize long-term performance, durability, and compliance assurance, seeking sealants with extended warranties, high movement capabilities, and resistance to environmental factors to minimize future remediation costs and insurance liabilities. For new constructions, developers often drive the specification process, favoring manufacturers who can provide integrated PFP solutions and robust technical documentation supporting large-scale projects. Furthermore, architects and design engineers act as influential customers; while they may not purchase the product directly, they dictate the material specifications and fire rating requirements that ultimately determine which products are used on a project, making early engagement and inclusion in BIM libraries essential for market penetration.

Another crucial customer group includes regulatory bodies and building inspectors, whose approval is contingent upon the correct use of certified sealants. While not direct purchasers, their stringent requirements drive the need for sealants that possess comprehensive certifications (e.g., UL Classified, ETA approved) and are compliant with local installation methods. Lastly, the industrial sector, including petrochemical, power generation, and nuclear facilities, represents a niche but highly profitable customer segment. These environments demand sealants that not only meet fire resistance standards but also withstand chemical exposure, high pressure, and extreme temperatures, requiring highly specialized, often custom-formulated, products with specialized third-party approvals relevant to hazardous location standards and operational continuity requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 1.85 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Hilti Corporation, Tremco Inc., Sika AG, Bostik (Arkema Group), BASF SE, Rockwool International A/S, Nullifire (Tremco CPG), Wacker Chemie AG, Dow Inc., Rectorseal, Specified Technologies Inc. (STI), Fosroc International, Jotun A/S, Saint-Gobain (Weber), Den Braven (Bostik), Everbuild (Sika), Hodgson Sealants, Firestone Building Products (Holcim), Trafalgar Fire. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Flexible Fire Protection Sealants Market is defined by the ongoing pursuit of improved intumescent performance, enhanced chemical compatibility, and reduced environmental impact. Intumescent technology, which forms the basis of these sealants, is continually advancing, moving beyond traditional mineral-based fillers to incorporate micro-encapsulated graphite and proprietary chemical blends that ensure highly controlled, rapid, and voluminous expansion upon fire exposure. A critical development involves optimizing the char structure formed by intumescence; modern sealants aim for a dense, stable, and highly insulating char that adheres robustly to both the substrate and the penetrating element, ensuring the seal remains intact under severe thermal stress and structural movement, significantly extending the effective fire resistance period and mitigating heat transfer effectively.

Material science innovations are focused heavily on hybrid polymer systems. These systems combine the high movement capability and UV stability of silicones with the ease of application and paintability of acrylics or polyurethanes. Hybrid technology reduces the need for multiple specialized products on a job site, simplifying contractor inventory and reducing the risk of using the incorrect product. Furthermore, these newer formulations often exhibit better adhesion to difficult substrates increasingly used in modern construction, such as Cross-Laminated Timber (CLT) and complex plastic piping systems, demanding firestopping solutions that maintain integrity even with thermal cycling and differential movement between disparate materials, a performance metric that drives premium pricing and specialized certification requirements within the market.

Another major technological pillar is the emphasis on low-VOC and sustainable chemistry. Regulatory shifts, particularly in mature markets like Europe and North America, necessitate the development of water-based or solvent-free formulations that meet stringent indoor air quality standards (e.g., LEED, BREEAM certifications). Manufacturers are investing heavily in water-based acrylics and next-generation silicone systems that maintain high performance without compromising installer health or contributing to off-gassing issues in occupied spaces. This commitment to 'green' firestopping is not merely a compliance issue but a key competitive differentiator, driving the rapid adoption of highly specialized equipment in the manufacturing process to ensure precise blending and curing of these sensitive, performance-critical, and environmentally preferred chemical systems.

Intumescent sealants are formulated to swell or expand significantly (often 10x or more) when exposed to high temperatures during a fire, forming a dense, insulating char that seals gaps and prevents the spread of fire and smoke. Non-intumescent sealants typically remain stable, relying on their inherent heat resistance and flexibility to maintain the integrity of the fire barrier without expanding. Intumescent technology is crucial for sealing around combustible penetrants like plastic pipes, which burn away, leaving voids.

Key global standards include UL (Underwriters Laboratories) and ASTM (American Society for Testing and Materials) in North America, EN (European Norms/Euroclass) and ETA (European Technical Assessment) in Europe, and ISO standards internationally. Compliance with these standards, particularly certification for maintaining fire resistance ratings (e.g., FRL 120/240), is mandatory for market entry and ensuring life safety performance, driving meticulous third-party testing procedures.

Low Volatile Organic Compound (VOC) requirements mandate sealants with minimal solvent content to improve indoor air quality and worker safety. This trend drives manufacturers towards developing water-based acrylics and advanced solvent-free silicone or hybrid formulations. Customers increasingly prioritize low-VOC sealants to comply with green building certifications like LEED, ensuring better health outcomes for occupants and contributing to sustainable construction practices.

The Commercial Construction sector, including hospitals, data centers, and high-rise office buildings, generates the highest demand by value. This is due to the complexity of these structures, the high volume of mechanical and electrical service penetrations that must be sealed, and the extremely stringent fire rating requirements (often 2–4 hours) necessary to ensure occupant safety and structural integrity over long evacuation times.

Flexibility, typically expressed as joint movement capability (e.g., +/- 25%), is critical because buildings are constantly subjected to dynamic stresses from thermal expansion, structural loads, wind, and seismic activity. Flexible fire sealants ensure the firestopping seal remains intact and continuous across joints and penetrations despite this ongoing movement, preventing cracks or failure that could compromise the fire barrier during a non-fire event or during the initial stages of fire exposure when structures begin to deform.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.