ID : MRU_ 435540 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

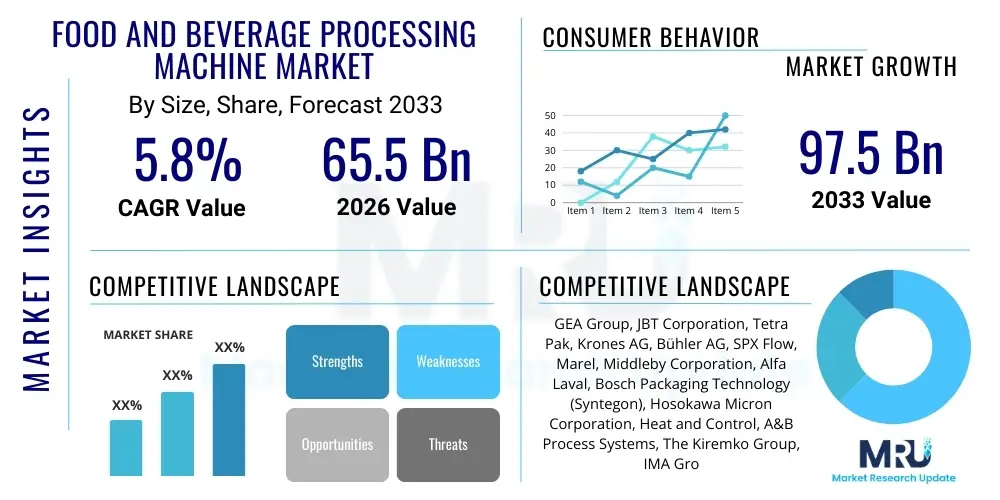

The Food and Beverage Processing Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 65.5 Billion in 2026 and is projected to reach USD 97.5 Billion by the end of the forecast period in 2033.

The Food and Beverage Processing Machine Market encompasses the manufacturing, distribution, and utilization of sophisticated mechanical and automated equipment designed to transform raw agricultural ingredients into consumer-ready food and beverage products. This machinery spans the entire production chain, including preparation, primary processing, secondary processing (such as cooking, cooling, and freezing), and packaging. Key applications range across dairy, bakery, meat, poultry, seafood, confectionery, and alcoholic and non-alcoholic beverages. These machines are critical for maintaining high standards of food safety, consistency, and efficient mass production, directly addressing the demands of a rapidly expanding global population and evolving dietary preferences.

The primary benefit derived from the deployment of these advanced processing machines is enhanced operational efficiency and significantly reduced labor costs. Modern equipment incorporates automation and precision engineering, leading to minimized waste, optimized resource utilization (energy and water), and superior product quality control. Furthermore, these machines are indispensable for enabling compliance with stringent international food safety regulations, such such as HACCP and FDA guidelines, by facilitating sterile environments and consistent temperature management during processing. The adoption of high-speed sorting, handling, and packaging machinery ensures that perishable goods reach markets swiftly while maintaining freshness and extending shelf life.

The market growth is primarily driven by several macro-level factors, including rapid urbanization, increasing consumer demand for packaged and ready-to-eat (RTE) foods, and the globalization of food supply chains. Technological advancements, particularly the integration of Internet of Things (IoT) sensors, robotics, and Artificial Intelligence (AI) into processing lines, are further fueling market expansion by offering predictive maintenance capabilities and real-time process optimization. Additionally, rising disposable incomes in developing economies are stimulating demand for diverse and premium processed food products, compelling manufacturers to invest heavily in advanced, high-capacity processing infrastructure.

The global Food and Beverage Processing Machine Market is positioned for robust expansion, driven predominantly by shifting consumer lifestyles favoring convenience foods and escalating global regulatory pressures mandating higher standards of hygiene and food traceability. Key business trends indicate a strong move toward modular and flexible processing systems that can quickly adapt to varied product batches and seasonal demands, alongside significant investment in sustainable and energy-efficient equipment. Manufacturers are prioritizing solutions that reduce environmental impact, particularly focusing on water management and waste minimization technologies, positioning sustainability as a core competitive differentiator in the B2B landscape.

Regionally, Asia Pacific (APAC) continues to dominate the market, propelled by massive population growth, rapid industrialization of the food sector, and expanding cold chain infrastructure, particularly in emerging economies like China and India. North America and Europe, while mature markets, exhibit strong demand for advanced automation, robotics, and high-pressure processing (HPP) machinery, largely driven by high labor costs and the need for sophisticated compliance solutions. Latin America and the Middle East & Africa (MEA) are emerging as high-growth potential markets, characterized by increasing foreign investment and modernization efforts in their domestic food production capabilities, specifically targeting beverage and packaged meat segments.

Segment trends reveal that the beverage processing sector, particularly for non-alcoholic and functional drinks, is experiencing accelerated growth, necessitating specialized filling and sealing machinery. Within the technology segment, advanced packaging machinery, focusing on modified atmosphere packaging (MAP) and aseptic processing, holds a dominant share due to its direct impact on extending product shelf life and ensuring microbial safety. Furthermore, the bakery and confectionery segment is rapidly adopting highly automated mixing and forming equipment to handle the rising global consumption of baked goods, reinforcing the overall market shift towards high-throughput, integrated processing lines.

Common user inquiries concerning the integration of Artificial Intelligence (AI) in the Food and Beverage Processing Machine Market frequently revolve around practical implementation, return on investment (ROI), and the tangible benefits related to quality and yield. Users are primarily concerned with how AI enhances predictive maintenance to minimize costly downtime, how machine vision systems driven by AI can perform high-speed quality inspection surpassing human capability, and how optimization algorithms can reduce ingredient waste and energy consumption during complex processes like mixing and cooking. The key themes emerging from this analysis are focused expectations regarding AI's ability to transition processing from reactive maintenance to predictive operations, achieve hyper-customization of products on existing lines, and ensure superior food safety through advanced contamination detection.

The Food and Beverage Processing Machine Market is highly influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO) which collectively dictate the direction and pace of growth. Key drivers include accelerating consumer demand for processed and convenience foods globally, coupled with stringent government regulations concerning food safety and quality, necessitating high-precision, automated machinery. This regulatory pressure acts as a powerful catalyst for technological adoption, forcing processors to upgrade obsolete equipment with modern systems capable of enhanced traceability and consistent compliance. Furthermore, the persistent challenge of labor shortages, particularly in developed economies, incentivizes rapid integration of robotics and advanced automation across all processing stages, reducing reliance on manual labor.

However, the market faces significant restraints, primarily stemming from the high initial capital investment required for state-of-the-art processing and packaging machinery, which often deters small and medium-sized enterprises (SMEs) from rapid modernization. Maintenance costs associated with complex, highly computerized systems also present a financial hurdle. Additionally, the rapid rate of technological obsolescence, especially with the introduction of new sustainable packaging materials and evolving consumer dietary preferences (e.g., plant-based alternatives), requires continuous reinvestment, posing financial pressure on manufacturers operating on tight margins. Intellectual property concerns and the complex integration challenges associated with merging legacy systems with new IoT and AI frameworks further constrain widespread adoption.

The opportunities within this sector are vast, centered largely on the sustainability agenda and the shift toward specialized nutrition. Manufacturers have a major opportunity in developing resource-efficient machinery, specifically those designed for minimal water consumption and maximum waste utilization, addressing environmental concerns. The burgeoning market for alternative proteins (plant-based meat and dairy), functional foods, and personalized nutrition opens up niches requiring entirely new categories of processing equipment. Furthermore, expanding infrastructure in emerging markets, coupled with government initiatives promoting domestic food security, creates substantial long-term growth avenues for machinery suppliers offering scalable and robust processing solutions tailored to local agricultural outputs.

The Food and Beverage Processing Machine Market is highly fragmented and analyzed across multiple dimensions, including Type, Application, Mode of Operation, and Region. Segmentation by Type includes specific equipment categories such as processing, packaging, filling, and slicing machinery, offering granular insights into which equipment types are experiencing the highest demand growth based on product complexity and automation requirements. Application segmentation is crucial, breaking down the market based on the end-product category, such as bakery, dairy, meat & poultry, beverages, and confectionery, allowing vendors to tailor R&D and marketing efforts toward high-value sectors. The mode of operation segment differentiates between manual, semi-automatic, and fully automatic machinery, reflecting the maturity and labor cost structures within different geographical markets.

The value chain for the Food and Beverage Processing Machine Market begins with upstream activities involving the sourcing of raw materials, primarily specialized alloys, components, and sophisticated electronic control systems, requiring precise engineering and reliable supply logistics. Upstream suppliers are vital for innovation, particularly in areas like hygienic design and durable material sciences, ensuring the longevity and safety of the final machinery. Integration complexity is high in the upstream stage due to the reliance on global suppliers for high-precision components such as PLC systems, robotic arms, and specialized sensor arrays, making supply chain resilience a critical factor for machine manufacturers.

The core value addition takes place during the manufacturing and assembly phase, where machine builders focus on R&D, customization, and systems integration. Manufacturers translate complex regulatory and application requirements into modular, scalable machinery solutions. Distribution channels are typically a mix of direct sales (for large, highly customized processing lines) and indirect channels utilizing local distributors or agents, particularly for standardized or smaller equipment. These intermediaries play a crucial role in providing local installation support, training, and maintenance services, which are critical components of the total cost of ownership for end-users.

Downstream analysis focuses on the end-users—the food and beverage processors themselves—and the crucial post-sale support activities. The downstream market is characterized by long service contracts, maintenance agreements, and technology upgrade cycles. Direct and indirect distribution structures are highly dependent on the geographical spread of the end-user. Direct channels ensure closer relationship management for key accounts and provide bespoke engineering solutions, while indirect channels offer broader market penetration and efficient logistics for spare parts and standard equipment across fragmented markets. The success in the downstream sector relies heavily on the machine's efficiency, reliability, and the quality of technical support provided post-installation, driving repeat business and brand loyalty.

Potential customers and end-users of food and beverage processing machines span the entire spectrum of the food production industry, ranging from multinational corporations to local artisanal producers. The primary buyers are large-scale industrial food processors operating in high-volume segments such as packaged meat, frozen foods, dairy conglomerates, and major beverage bottlers. These large enterprises prioritize high-throughput, fully automated systems that guarantee consistent quality, minimize operational variances, and comply with global food safety standards. Their purchasing decisions are driven by total cost of ownership (TCO), technological superiority, and the supplier's ability to provide comprehensive global servicing and predictive maintenance contracts.

A secondary, yet rapidly growing, customer base includes mid-sized companies specializing in emerging or niche food categories, such as plant-based proteins, gluten-free products, and specialized nutritional supplements. These customers often seek flexible, modular equipment that allows for rapid shifts between product formulations and accommodates smaller production batches, prioritizing machinery that is versatile and easy to clean (high hygienic design). Furthermore, the retail sector, particularly large grocery chains investing in private label manufacturing capabilities, also represents a growing segment of potential customers seeking efficient, reliable processing equipment to maintain control over their supply chain and product quality.

Geographically, processors in Asia Pacific, driven by increasing per capita consumption and shifting dietary habits toward Westernized processed foods, are emerging as significant volume buyers. In contrast, European and North American customers are primarily focused on replacement cycles, seeking advanced robotic integration, enhanced sustainability features, and highly specialized technology like High-Pressure Processing (HPP) equipment to meet sophisticated consumer demands for clean label and minimally processed products. Government and institutional buyers, such as military food supply chains or large institutional catering services, also represent niche, stable buyers focused on durability and compliance with strict long-term operational specifications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 65.5 Billion |

| Market Forecast in 2033 | USD 97.5 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | GEA Group, JBT Corporation, Tetra Pak, Krones AG, Bühler AG, SPX Flow, Marel, Middleby Corporation, Alfa Laval, Bosch Packaging Technology (Syntegon), Hosokawa Micron Corporation, Heat and Control, A&B Process Systems, The Kiremko Group, IMA Group, Multivac, Trepko, Meyn Food Processing Technology, Provisur Technologies, Coesia S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Food and Beverage Processing Machine Market is rapidly evolving, moving away from conventional mechanical systems toward highly integrated, smart manufacturing environments often referred to as Food Industry 4.0. Central to this transformation is the integration of the Industrial Internet of Things (IIoT), which allows machinery to communicate real-time operational data regarding temperature, pressure, speed, and energy consumption. This interconnectedness enables sophisticated monitoring and control, facilitating predictive maintenance strategies and ensuring rapid adjustments to maintain product consistency and adherence to quality standards. The advancement of sensor technology, including hyperspectral imaging and advanced chemical sensors, is crucial for improving inline quality assurance and contamination detection, thereby significantly enhancing food safety.

Robotics and advanced automation systems represent another cornerstone of the technological revolution in this sector. Modern processing lines increasingly rely on collaborative robots (cobots) for tasks requiring high precision, speed, and repetitive actions, such as sorting, picking, placing, and palletizing. This adoption is driven by the need to mitigate rising labor costs and improve hygienic standards, as robots can operate reliably in sterile or harsh environments unsuitable for human workers. Furthermore, specialized processing technologies, such as High-Pressure Processing (HPP) and Pulsed Electric Field (PEF) treatment, are gaining traction. HPP, in particular, offers a non-thermal pasteurization method that preserves nutritional value and flavor better than traditional heat treatments, catering directly to the clean-label trend and demand for minimally processed foods.

A significant focus is also placed on packaging technology, specifically on enhancing barrier properties and sustainability. Modified Atmosphere Packaging (MAP) technology is widely used to extend the shelf life of fresh produce and meat products by altering the gaseous environment inside the package. Concurrently, the industry is witnessing substantial innovation in sustainable packaging machinery capable of handling recyclable, compostable, or bio-based materials without compromising production speed or seal integrity. Digital twin technology is also beginning to emerge, allowing manufacturers to create virtual representations of entire production lines for simulation, testing, and optimization before physical deployment, thereby reducing risks and accelerating commissioning timelines.

The Food and Beverage Processing Machine Market displays distinct regional growth dynamics influenced by population size, economic development, and regulatory frameworks. Asia Pacific (APAC) stands out as the global growth engine, driven by accelerating urbanization, the proliferation of multinational food manufacturers setting up production bases in the region, and growing demand for convenience foods among a rapidly expanding middle class. Countries like China, India, and Southeast Asian nations are heavily investing in modernizing their food infrastructure to meet domestic demand and improve export capabilities, focusing primarily on high-capacity primary processing and packaging machinery. This region’s growth is characterized by volume expansion and initial automation adoption.

North America and Europe represent mature, high-value markets characterized by replacement demand and technological sophistication. Growth here is primarily driven not by capacity expansion but by the continuous upgrade to advanced, highly automated machinery incorporating AI, IoT, and robotics to combat high labor costs and meet increasingly stringent environmental and food safety regulations. European processors, in particular, are pioneers in aseptic processing and sustainable packaging solutions, maintaining a focus on energy efficiency and waste reduction. The market in these regions is dominated by specialized equipment, custom engineering, and sophisticated quality control systems.

Latin America and the Middle East & Africa (MEA) offer substantial long-term growth potential. Latin America's market expansion is tied to the growth of its domestic meat, dairy, and beverage industries, supported by foreign investment aimed at establishing regional processing hubs. MEA, while currently smaller, is projected to see significant investment in basic and semi-automatic processing equipment to address food security concerns and reduce reliance on imported processed goods. Government initiatives aimed at agricultural self-sufficiency are catalyzing demand for primary processing machinery, particularly for grains and local produce, making these regions attractive for standardized, cost-effective equipment solutions.

The market growth is primarily driven by escalating global demand for packaged and convenience foods, increasingly stringent food safety and hygiene regulations worldwide, and the necessity for automation (robotics and AI integration) to mitigate rising labor costs and enhance operational efficiency.

The integration of Industrial Internet of Things (IIoT) sensors and AI-driven machine vision systems is having the largest impact. IIoT facilitates real-time performance monitoring and predictive maintenance, drastically reducing downtime, while AI vision systems ensure instant, hyper-accurate quality control and contamination detection.

Sustainability mandates are shifting procurement towards energy-efficient systems, machinery designed for minimal water usage, and equipment capable of handling new eco-friendly packaging materials (recyclable, compostable). Processors prioritize suppliers who demonstrate reduced environmental footprint across their entire equipment lifecycle.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by massive population growth, expanding urbanization, and substantial government and private investment in modernizing and expanding local food processing capabilities, particularly in China and India.

HPP is a non-thermal pasteurization technique that utilizes extreme pressure instead of heat to eliminate pathogens and microorganisms. It is becoming essential because it significantly extends the shelf life of food while preserving essential nutrients, flavor, and texture, aligning with strong consumer preference for minimally processed and 'clean label' products.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.