ID : MRU_ 432009 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

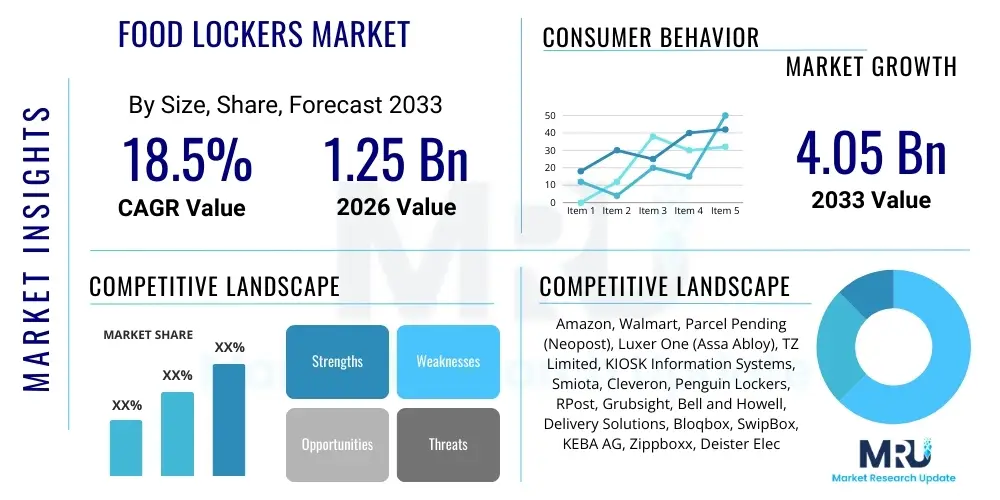

The Food Lockers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. This substantial growth is driven primarily by the escalating demand for convenient last-mile delivery solutions, especially for temperature-sensitive grocery and meal kit deliveries stemming from the continuous expansion of e-commerce platforms and quick commerce services worldwide. The market trajectory reflects a fundamental shift in consumer behavior toward automated, secure, and flexible retrieval options, mitigating issues related to failed deliveries and food spoilage.

The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 4.05 Billion by the end of the forecast period in 2033. This significant valuation increase is supported by large-scale infrastructural investments by major retailers, third-party logistics (3PL) providers, and residential and commercial real estate developers integrating smart locker systems into their essential services. The implementation of advanced technologies, such as IoT connectivity, thermal monitoring, and mobile integration, further solidifies the market's robust financial outlook and expands its applicability across diverse food delivery ecosystems.

The Food Lockers Market encompasses specialized automated storage solutions designed for the secure, temperature-controlled, and convenient delivery and retrieval of prepared meals, groceries, and other perishable food items. These systems typically maintain specific temperature zones (refrigerated, frozen, or ambient/heated) to ensure product integrity and safety during the transition phase between delivery personnel and the end consumer. The increasing penetration of online grocery shopping, amplified by global urbanization and time-constrained lifestyles, is the foundational catalyst driving the adoption of these sophisticated locker systems across various environments, including multi-family housing, corporate campuses, and public access points.

Major applications of food lockers span residential buildings seeking enhanced amenity offerings, grocery retailers aiming for optimized click-and-collect services, quick-service restaurants (QSR) utilizing them for seamless mobile order pickup, and commercial offices providing subsidized or secure employee meal solutions. The primary benefits include reduced operational costs for retailers associated with failed deliveries, improved security and anonymity for consumers, extended shelf life of delivered goods through precise temperature management, and increased customer satisfaction due to 24/7 accessibility. These systems bridge the critical gap in the cold chain logistics of last-mile delivery, which is notoriously complex and resource-intensive, transforming the economics of food e-commerce.

The core driving factors propelling market expansion include the exponential growth in online grocery penetration, particularly in North America and Europe, coupled with the rising consumer expectation for rapid, scheduled, and contactless delivery methods following recent global health crises. Furthermore, regulatory pressures related to food safety and temperature compliance are encouraging retailers to invest in certified, trackable cold chain infrastructure like food lockers. Technological advancements in battery life, thermal insulation, and software integration (e.g., seamless mobile app synchronization) are making these systems more efficient and economically viable for widespread deployment, accelerating market uptake globally.

The Food Lockers Market is characterized by vigorous growth, driven by key business trends focusing on integration, standardization, and expansion into high-density urban areas. Business trends highlight strategic partnerships between locker manufacturers and major grocery chains (e.g., Walmart, Amazon) to establish extensive, proprietary networks, alongside increased merger and acquisition activity consolidating technology platforms. The market is shifting from custom-built solutions toward modular, scalable systems that can handle varied product sizes and temperature requirements, emphasizing software interoperability with existing retail management and courier logistics platforms. Investment in IoT-enabled sensors for real-time monitoring of temperature, humidity, and locker status is becoming standard practice, ensuring adherence to stringent food safety protocols and optimizing utilization rates.

Regionally, North America maintains market leadership, propelled by high consumer disposable income, mature e-commerce infrastructure, and the widespread adoption of meal kit services and large-scale residential integration programs. Asia Pacific is emerging as the fastest-growing region, stimulated by rapid urbanization, substantial investments in smart city infrastructure, and explosive growth in quick commerce (Q-commerce) platforms, particularly in China and India. European regional trends focus heavily on sustainability and energy efficiency in locker design, supported by robust regulatory frameworks promoting contactless and environmentally friendly delivery options. The Middle East and Africa (MEA) region is exhibiting nascent growth, driven primarily by luxury residential developments and high-end grocery retailers prioritizing premium delivery experiences.

Segmentation trends indicate that the Refrigerated segment dominates the market due to the essential requirement for managing perishable items, while the App-Controlled operation segment is witnessing the highest growth rate, offering unparalleled user convenience and enhanced security features through biometric or facial recognition integrations. Within applications, Residential Buildings constitute the largest segment, acting as critical points of consolidation for multiple delivery services. However, the QSR/Restaurants segment is showing rapid expansion as fast-food chains leverage lockers to improve efficiency in high-volume, mobile-order pickup scenarios, transforming front-of-house operations and reducing staff interaction time.

User inquiries regarding the impact of AI on the Food Lockers Market predominantly revolve around themes of optimization, predictive maintenance, and enhanced security integration. Common questions focus on how AI algorithms can improve locker allocation efficiency (matching box size/temperature to delivery item), predict demand patterns to optimize locker placement in urban environments, and utilize machine learning for proactive maintenance scheduling to minimize system downtime. Users also frequently ask about AI's role in fraud detection, biometric access control improvements, and personalized user experiences, such as tailored notification timing or preferred pickup sequences. The key concern is ensuring these AI systems maintain robust data privacy standards while maximizing logistical efficiency, thereby transforming food locker networks from static storage units into dynamic, intelligent logistical assets capable of self-management and continuous performance improvement.

The Food Lockers Market dynamics are shaped by a strong combination of inherent drivers pushing adoption, specific restraints limiting expansion, and significant opportunities for growth, all interacting under various critical impact forces. The primary drivers include the global surge in online grocery ordering and the resultant necessity for secure, temperature-controlled last-mile solutions, coupled with increasing consumer demand for flexible pickup options outside traditional store hours. Restraints mainly center on the high initial capital investment required for installing refrigerated units, the complexity of integrating diverse software platforms across retailers and 3PLs, and the significant logistical challenge of securing premium real estate locations in densely populated urban centers for public locker placement. Opportunities are robust in geographical expansion into untapped developing markets and technological innovation focusing on modular design and sustainable energy usage. These forces collectively dictate the speed and shape of market evolution, rewarding companies that successfully navigate the capital and integration hurdles.

Impact forces acting upon the market include technological advancements (e.g., 5G rollout enabling real-time IoT communication), regulatory compliance mandates (especially stricter food safety and temperature logging requirements), and socio-economic shifts like the persistent trend toward contactless service interaction. The competitive impact force is significant, characterized by intense rivalry between traditional parcel locker companies expanding into cold chain solutions and dedicated food logistics technology firms. Furthermore, the economic impact force, relating to the cost-benefit analysis for retailers (weighing high CAPEX against savings from reduced failed deliveries and labor costs), remains a critical determinant of widespread commercial uptake. Successful market penetration relies on providing systems that demonstrate clear, measurable ROI despite the substantial initial costs associated with robust cooling infrastructure.

The Food Lockers Market is highly fragmented and segmented based on operational characteristics, temperature control requirements, end-user applications, and ownership models, reflecting the diverse needs of the cold chain logistics industry. Understanding these segments is crucial for manufacturers and service providers to tailor their offerings and optimize market penetration strategies. The segmentation by temperature type (Refrigerated, Non-Refrigerated, Heated) directly addresses the core function of preserving various food categories, from deep-frozen goods to hot, prepared meals. Meanwhile, segmentation by application highlights the key deployment areas—residential being the traditional stronghold, and QSR/Restaurants representing the emerging high-growth segment demanding rapid turnaround times and specific locker configurations.

The operation type, particularly the shift toward App-Controlled systems utilizing sophisticated IoT integration, defines the user experience and security protocols, differentiating modern solutions from legacy keypad-based systems. Furthermore, the ownership model—spanning retailer-owned, 3PL-managed, and shared public models—determines the primary revenue streams, investment incentives, and maintenance responsibilities. These intersecting segmentations allow for the precise mapping of market demands, confirming that the future growth trajectory is heavily reliant on highly specialized, interoperable, and scalable solutions that address the specific logistical pain points of each end-user category.

The value chain of the Food Lockers Market begins with upstream activities focused on the design, manufacturing, and sourcing of specialized components. Upstream analysis involves raw material providers (metals, plastics, insulation materials), high-tech component manufacturers (refrigeration units, IoT sensors, controllers, touch screens), and software developers creating the proprietary operating systems and cloud platforms necessary for remote management. Manufacturers often focus on modularity, thermal efficiency, and cybersecurity compliance during the production phase, ensuring the hardware meets stringent food safety and cold chain standards. Key success factors at this stage include minimizing component costs, achieving energy efficiency certifications, and securing reliable supply chains for critical cooling technology.

Midstream activities encompass the installation, integration, and service provision aspects. This involves specialized logistics firms responsible for site preparation and installation, and integrators who ensure seamless communication between the locker software, the retailer's inventory management system (IMS), and the various carrier delivery platforms. Distribution channels are varied, including direct sales from manufacturers to large retail chains, partnerships with commercial real estate developers, and indirect sales through 3PLs or value-added resellers (VARs) who bundle the locker system with ongoing maintenance and software subscriptions. The effectiveness of the midstream relies heavily on the quality of system integration and the provision of robust technical support.

Downstream analysis focuses on the end-user interaction and the continuous service loop. This stage involves the end consumers utilizing the direct access interface (mobile app or screen), the delivery personnel accessing the system, and the ongoing maintenance and monitoring services provided by the vendor or a contracted third party. Direct channels involve retailers owning the entire customer journey, while indirect channels utilize shared public networks managed by 3PLs, charging retailers a per-use or subscription fee. The primary driver of value at the downstream level is the quality of the user experience (UX), reliability, and the data generated regarding utilization rates and demand patterns, which informs future expansion and optimization strategies for all stakeholders.

The Food Lockers Market serves a diverse range of end-users whose primary goal is to securely and efficiently manage the cold chain logistics of last-mile food delivery. The largest segment of potential customers currently includes property managers and owners of multi-family residential buildings (MDUs) and large apartment complexes. These buyers invest in lockers as a high-value amenity to attract and retain residents by solving the daily challenge of secure parcel and grocery handling, often integrating the locker system into the building’s existing access control and resident management software. The investment decision here is driven by resident satisfaction and competitive differentiation in the real estate market, seeking systems that are aesthetically pleasing, highly reliable, and energy efficient.

Another major segment comprises large-scale grocery retailers and supermarket chains that are heavily invested in developing their omni-channel capabilities, specifically focusing on click-and-collect (BOPIS) services. For these buyers, food lockers are deployed both inside the store perimeter for rapid pickup and externally in high-traffic areas, reducing in-store labor costs associated with manual order fulfillment and providing consumers with enhanced convenience. The purchasing criteria for retailers center on scalability, integration compatibility with their existing ERP and e-commerce platforms, and data reporting capabilities, which allow them to track and analyze consumer behavior and operational efficiency metrics.

Emerging but high-growth potential customers include quick-service restaurants (QSRs), particularly those relying on high volumes of mobile and third-party delivery orders (e.g., Uber Eats, DoorDash). QSRs utilize heated and ambient lockers to streamline kitchen throughput, reduce order staging bottlenecks, and ensure orders are handed off quickly and securely to couriers or customers without congesting the service counter. Finally, third-party logistics (3PL) providers and dedicated parcel network operators represent a crucial customer group, as they purchase and operate neutral locker networks accessible by all carriers, monetizing the infrastructure through service fees charged to retailers and consumers, thereby driving shared public network adoption in densely populated urban cores.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 4.05 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amazon, Walmart, Parcel Pending (Neopost), Luxer One (Assa Abloy), TZ Limited, KIOSK Information Systems, Smiota, Cleveron, Penguin Lockers, RPost, Grubsight, Bell and Howell, Delivery Solutions, Bloqbox, SwipBox, KEBA AG, Zippboxx, Deister Electronic, Quadient, Pitney Bowes |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Food Lockers Market is rapidly evolving, driven by the convergence of IoT, advanced refrigeration techniques, and highly specialized access control software. The foundation of modern food lockers relies on robust Industrial IoT (IIoT) sensors that provide real-time monitoring of critical parameters such as internal temperature, humidity, door status, and power consumption. This real-time data connectivity is essential not only for security but also for regulatory compliance, as many jurisdictions require auditable proof of cold chain maintenance. Furthermore, the shift from conventional compressors to energy-efficient thermoelectric cooling (Peltier) or sophisticated variable-speed refrigeration systems is a major trend, aiming to reduce the substantial operational costs associated with large-scale cold locker deployments while adhering to sustainability mandates.

Software and connectivity represent the core differentiation in the competitive landscape. Modern food locker systems are heavily dependent on cloud-based management platforms that interface seamlessly with various stakeholders—the retailer's order management system, the carrier's tracking software, and the consumer's mobile application. Key technological features include API integration capabilities for third-party platforms, encrypted communication protocols (HTTPS/SSL) to protect consumer data, and multi-factor authentication methods for access control, often incorporating QR codes, biometrics, or mobile proximity features. The development focus is on creating highly resilient, redundant systems that can operate continuously, minimizing downtime which could lead to spoilage and significant financial loss.

Looking forward, key innovations involve predictive maintenance utilizing AI analytics, as previously mentioned, and the development of highly adaptable modular hardware designs. Modular technology allows retailers and 3PLs to easily adjust the ratio of ambient, refrigerated, and frozen compartments based on seasonal demand fluctuations or localized consumption patterns without replacing the entire unit. Furthermore, the integration of 5G connectivity is set to accelerate data transmission speeds and enhance the reliability of remote management, supporting the deployment of lockers in less developed infrastructure environments. Sustainable design, including the use of high-efficiency insulation materials and integration with solar or smart grid systems, is also a rapidly advancing area, addressing the environmental concerns surrounding energy-intensive cold storage solutions.

The global Food Lockers Market exhibits distinct regional dynamics, dictated by varying levels of e-commerce maturity, infrastructural readiness, and consumer adoption rates of automated logistics solutions.

The primary benefit for retailers is the significant reduction in costs associated with failed or missed deliveries, which often result in product spoilage, re-delivery attempts, and customer service issues. Refrigerated lockers guarantee the cold chain integrity and offer 24/7 self-service pickup, thereby optimizing last-mile logistics efficiency and enhancing customer retention by providing a reliable, secure retrieval point.

The market leverages IoT sensors for real-time monitoring of temperature, security status, and system health. AI is used for dynamic allocation, matching package size and temperature needs to available compartments, and for predictive maintenance, anticipating equipment failures before they occur. This integration maximizes operational uptime, reduces energy consumption, and provides auditable cold chain compliance data.

The chief financial barrier is the high initial Capital Expenditure (CAPEX) required for sophisticated temperature-controlled units compared to ambient parcel lockers. These systems demand costly refrigeration components, specialized insulation, and complex integration software, which mandates a strong financial justification based on high utilization rates or clear competitive necessity for implementation.

The Quick-Service Restaurant (QSR) and fast-casual dining segment is anticipated to exhibit the fastest growth. As QSRs increasingly rely on mobile ordering and third-party delivery services, automated food lockers (including heated options) provide an essential mechanism for rapid, secure, and accurate order handoff, greatly improving throughput efficiency and customer pickup experience during peak hours.

Third-Party Logistics (3PL) providers are crucial as they often own and manage neutral, shared locker networks, allowing multiple retailers and carriers to utilize the infrastructure. 3PLs drive market interoperability by acting as the centralized service provider, handling maintenance, software integration, and monetization through usage fees, which facilitates broader public access to cold chain pickup points.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.