ID : MRU_ 432863 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

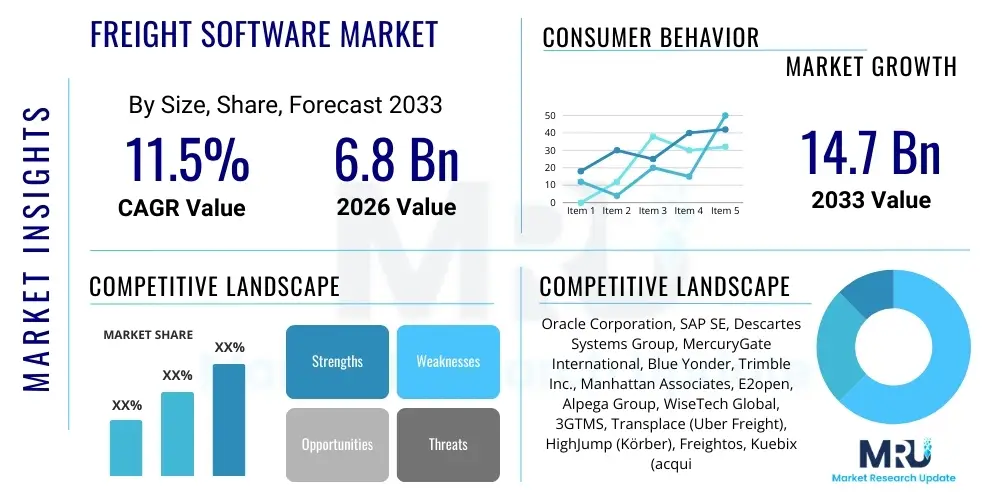

The Freight Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 6.8 Billion in 2026 and is projected to reach USD 14.7 Billion by the end of the forecast period in 2033.

The Freight Software Market encompasses a wide range of technological solutions designed to optimize and manage the complex logistics and operational requirements of the global freight industry. These solutions include Transportation Management Systems (TMS), Warehouse Management Systems (WMS), Fleet Management Software, and visibility platforms that facilitate planning, execution, and monitoring of cargo movement across various modalities—road, rail, air, and sea. The core product description involves sophisticated algorithmic tools that manage route optimization, capacity planning, rate management, customs compliance, and real-time tracking, translating physical logistics into efficient digital processes. Key benefits derived from the adoption of freight software include significant reductions in operational costs, enhanced supply chain visibility, improved delivery speed and reliability, and superior compliance management in heavily regulated international trade environments. The necessity for these advanced systems is driven by the increasing complexity of global trade, the burgeoning growth of e-commerce necessitating rapid and precise fulfillment, and the widespread mandate for higher operational efficiency and sustainability within the logistics sector.

Major applications of freight software span across crucial sectors such as third-party logistics (3PL) providers, freight forwarders, shipping carriers, and large-scale manufacturing and retail enterprises that manage their own complex distribution networks. These systems are indispensable for optimizing load planning, managing multimodal shipments, automating billing processes, and ensuring seamless integration with Enterprise Resource Planning (ERP) and Customer Relationship Management (CRM) systems. The shift towards digitalization, accelerated by the COVID-19 pandemic and subsequent supply chain disruptions, has cemented the critical role of these platforms in maintaining supply chain resilience and operational continuity. Furthermore, the imperative for improved sustainability reporting and emissions reduction is pushing companies towards software solutions that can accurately calculate and optimize carbon footprints associated with freight transport.

Driving factors fueling the market growth are numerous and intertwined, centered around the pressure for cost reduction, the increasing global volume of trade, and the rapid technological advancements in associated fields like Internet of Things (IoT) and Artificial Intelligence (AI). Specifically, the rise of cloud-based deployment models offers scalability and affordability, lowering the barrier to entry for Small and Medium-sized Enterprises (SMEs) and encouraging widespread adoption. The demand for end-to-end supply chain visibility, particularly in volatile market conditions, drives investment in modern, integrated software platforms. Additionally, regulatory shifts, such as stricter customs requirements and safety protocols, necessitate specialized freight software features that ensure adherence and mitigate financial and operational risks, ensuring the market's sustained growth trajectory through the forecast period.

The Freight Software Market is experiencing robust expansion, characterized by significant integration of advanced technologies, heightened emphasis on real-time data analytics, and a strategic shift toward cloud-native platforms. Business trends indicate a strong move toward consolidated supply chain platforms that offer TMS, WMS, and global trade management (GTM) capabilities within a single suite, appealing to large enterprises seeking unified operational control. Mergers and acquisitions remain a consistent strategic driver, with leading technology providers actively acquiring specialized software firms to quickly incorporate niche functionalities like predictive analytics and last-mile optimization into their portfolios. Furthermore, the increasing complexity of cross-border e-commerce logistics is driving demand for sophisticated rate management and automated compliance tools, making interoperability and API integration key competitive differentiators among vendors, directly influencing procurement decisions across 3PLs and shippers.

Regional trends highlight North America and Europe as dominant markets, primarily driven by high digital maturity, significant investment in infrastructure modernization, and the presence of major logistics and retail giants demanding high-performance systems. However, the Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR), fueled by rapidly industrializing economies, surging e-commerce activity, and government initiatives promoting logistics efficiency and digitalization, particularly in countries like China, India, and Southeast Asia. The Middle East and Africa (MEA) region is also demonstrating accelerated adoption, leveraging freight software to support massive infrastructure projects and diversify trade capabilities, positioning smart logistics as a cornerstone of economic development, thereby creating substantial localized opportunities for specialized vendors.

Segment trends underscore the pervasive adoption of the Cloud deployment model, overshadowing on-premise solutions due to superior scalability, reduced capital expenditure, and ease of maintenance and updates. From a component perspective, software solutions dominate, yet the demand for supplementary managed services and consulting is growing rapidly, reflecting the complexity of integrating these systems into existing enterprise ecosystems. Functionality-wise, the focus remains strongly on advanced features such as route optimization, capacity planning, and superior visibility tools, especially those enhanced by machine learning algorithms capable of predicting disruptions. The Small and Medium-sized Enterprises (SME) segment represents an increasingly important customer base, driven by affordable subscription-based (SaaS) models, democratizing access to enterprise-grade logistics tools previously exclusive to large corporations, thereby expanding the total addressable market significantly.

User inquiries regarding the integration of Artificial Intelligence (AI) and Machine Learning (ML) into freight software primarily revolve around predictive capabilities, automation efficiency, and ethical implications. Common questions center on how AI can accurately predict supply chain disruptions, optimize dynamic routing in real-time based on unexpected events (like weather or traffic), and automate complex decision-making processes, such as optimal carrier selection and dynamic pricing. Users are highly concerned about the reliability and explainability of AI models (AI ethics and transparency) and the required data infrastructure necessary to leverage these technologies effectively. Furthermore, expectations are high regarding AI's ability to drive sustainability efforts by minimizing empty miles and optimizing load consolidation, translating directly into tangible cost savings and environmental benefits for logistics operations globally.

AI's fundamental impact is transforming freight software from a transactional record-keeping tool into a strategic decision-support system. By analyzing vast, unstructured datasets—including historical shipment records, weather forecasts, global economic indicators, and real-time traffic data—AI algorithms can generate highly accurate demand forecasts and identify potential bottlenecks before they materialize. This capability enables freight software platforms to offer proactive recommendations for inventory redistribution, alternative routing, and buffer stock planning, significantly improving supply chain resilience and minimizing costly delays and penalties associated with service failures. Moreover, AI-powered automation is revolutionizing back-office operations, handling repetitive tasks like documentation processing, invoice verification, and compliance checks, which allows human logistics professionals to focus on complex, strategic problem-solving.

The implementation of machine learning is particularly powerful in the domains of dynamic pricing and fraud detection. ML models continuously learn from market fluctuations, carrier capacity, and specific customer requirements to provide highly competitive and optimized freight rates instantly, improving profitability and customer satisfaction simultaneously. In fraud and risk management, AI algorithms can quickly flag anomalous patterns in shipping documentation or route deviations, which traditional rule-based systems often miss, safeguarding cargo and preventing financial losses. Overall, the increasing sophistication of AI integration is rapidly elevating the competitive threshold in the Freight Software Market, making deep predictive and automation capabilities essential features for vendors aiming to maintain market leadership and drive true operational transformation for their clientele.

The dynamics of the Freight Software Market are dictated by a powerful combination of driving forces that mandate digital transformation, counterbalanced by significant constraints related to high integration complexity and data security concerns, presenting specific opportunities for specialized innovation. The primary driver is the accelerating pressure for operational efficiency and cost optimization across the global logistics sector, particularly in response to rising fuel costs and labor shortages, making software investment a critical necessity rather than an optional enhancement. Restraints largely center on the substantial upfront capital investment required for comprehensive system implementation, particularly for on-premise solutions, and the organizational change management challenges inherent in transitioning from legacy systems or manual processes. Impact forces—such as globalization, technological advancements (IoT, 5G), and stringent regulatory environments—act as multipliers, intensifying the need for resilient, flexible, and compliance-ready software solutions.

Opportunities are predominantly emerging from two areas: the proliferation of affordable Software-as-a-Service (SaaS) models and the need for seamless data integration across fragmented supply chains. SaaS platforms allow smaller logistics providers and shippers (SMEs) to access advanced capabilities previously reserved for large enterprises, significantly broadening the market base. Furthermore, the escalating complexity of international trade, coupled with geopolitical instability, has created an urgent demand for enhanced global trade management (GTM) software that can handle intricate tariff schedules, sanction screening, and multi-country compliance checks automatically, presenting a lucrative niche for specialized product development. The focus on environmental, social, and governance (ESG) metrics also drives demand for software that offers verifiable carbon tracking and optimization tools, aligning business goals with sustainability mandates.

Impact forces specifically accelerate market penetration by setting new standards for visibility and resilience. The deployment of 5G networks and widespread IoT sensors in fleets and cargo containers generates massive volumes of real-time data, which requires sophisticated freight software, particularly TMS and visibility platforms, to process, analyze, and translate into actionable insights. This continuous feedback loop enhances predictive maintenance, delivery precision, and overall customer experience. Simultaneously, cyber security threats, driven by the increased connectivity, impose a powerful force requiring vendors to prioritize robust, multi-layered security protocols within their software architecture, transforming data protection into a core competitive advantage and a non-negotiable feature for enterprise adoption.

The Freight Software Market is extensively segmented based on key structural and operational dimensions, including component (software and services), deployment model (cloud and on-premise), type of freight (road, rail, air, sea, multimodal), organization size (SMEs and large enterprises), and major application areas (TMS, WMS, FMS, etc.). This multifaceted segmentation allows vendors to tailor their solutions to specific industry needs, whether optimizing intricate, high-value air freight operations or managing high-volume, cost-sensitive road transportation networks. The most significant shifts observed within the segmentation analysis include the dominant growth trajectory of cloud-based solutions and the increasing market share captured by sophisticated, integrated multimodal TMS platforms that allow seamless management of entire shipment lifecycles across different carriers and geographical regions, catering to the growing demands of global supply chain orchestrators.

The value chain of the Freight Software Market begins with upstream activities focused on foundational technological development, which involves software developers, specialized data providers (e.g., mapping and real-time traffic data providers), and hardware manufacturers providing cloud infrastructure and processing capabilities. This phase is characterized by intensive R&D efforts aimed at building robust, scalable platforms incorporating advanced functionalities such as AI/ML for optimization and blockchain for enhanced security and transparency. The strategic imperative at this stage is to secure intellectual property and develop highly modular, API-first architectures that allow for rapid integration with diverse legacy and third-party systems. Key upstream players often dictate the pace of innovation, setting industry standards for data exchange protocols and security compliance.

Midstream activities involve the crucial stages of software development, testing, deployment, and marketing. Software vendors focus on customizing generic platforms to meet the specific requirements of different logistics modalities (e.g., container shipping versus last-mile delivery) and organization sizes. Distribution channels play a vital role here; direct distribution involves internal sales teams targeting large enterprise contracts, offering personalized integration services and long-term support. Indirect distribution utilizes strategic partnerships with system integrators, value-added resellers (VARs), and regional consulting firms who possess deep local market knowledge and expertise in implementing complex supply chain solutions. The successful management of these distribution channels ensures market reach and effective localization of the product offerings, bridging the gap between sophisticated technology and practical operational needs.

Downstream activities center on post-implementation support, continuous optimization, and customer relationship management, defining the long-term success of the software. This phase includes extensive training, technical support services, regular software updates, and managed services that ensure the client continuously derives maximum value from their investment. For freight software, the downstream success is highly dependent on continuous data feedback and performance tuning, often involving ongoing consulting to adapt the system to evolving supply chain demands and geopolitical shifts. Potential customers, spanning 3PLs, shippers, and carriers, become key feedback generators, influencing the roadmap for future software iterations, highlighting the cyclical and highly interactive nature of the freight software value chain where customer experience drives future product development and service expansion.

Potential customers, or end-users, of freight software are broadly categorized into entities responsible for managing, executing, or overseeing the movement of goods globally, placing Third-Party Logistics (3PL) providers and large Shippers (manufacturers and retailers) at the core of the target market. 3PLs require highly flexible, multi-tenant TMS platforms capable of managing thousands of diverse client contracts, optimizing routes for various modes of transport simultaneously, and providing transparent reporting to maintain customer trust and regulatory compliance. For large shippers, the focus is on integrating freight software with their existing ERP systems to achieve end-to-end visibility from raw material sourcing through to final customer delivery, demanding robust features in forecasting, planning, and cost allocation across business units.

A rapidly expanding customer segment includes Small and Medium-sized Enterprises (SMEs), particularly smaller freight forwarders and niche logistics providers, whose growing digitalization needs are now being met by cost-effective Software-as-a-Service (SaaS) models. These customers typically prioritize ease of implementation, low upfront costs, and scalable solutions that can grow with their business volume. Furthermore, specialized government agencies, particularly those involved in defense logistics, customs and border protection, and emergency relief supply chains, represent highly attractive niche customers who require bespoke security features, high-level auditing capabilities, and systems designed to handle complex, non-commercial logistics operations where mission success is paramount, often justifying premium pricing for highly specialized software solutions.

Maritime and air cargo carriers also form a significant customer base, although their requirements lean toward highly specialized fleet and capacity management systems, distinct from the typical TMS used by shippers. Shipping lines, for instance, need software that optimizes vessel stacking, port calls, and bunker fuel consumption, integrating directly with vessel tracking and weather data. Conversely, air carriers demand software focused on yield management, dynamic weight and balance calculations, and seamless integration with ground handling operations. The diversity of needs across these end-user segments necessitates that freight software vendors either specialize deeply in one area (e.g., container logistics) or offer a comprehensive, highly configurable modular suite that addresses the unique operational and compliance challenges faced by each distinct category of logistics stakeholder.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 14.7 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Oracle Corporation, SAP SE, Descartes Systems Group, MercuryGate International, Blue Yonder, Trimble Inc., Manhattan Associates, E2open, Alpega Group, WiseTech Global, 3GTMS, Transplace (Uber Freight), HighJump (Körber), Freightos, Kuebix (acquired by Trimble), FourKites, Project44, JDA Software, CargoWise, QAD Precision. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Freight Software Market is defined by the convergence of several high-impact technologies designed to create smart, autonomous, and resilient supply chains. Central to this evolution is the pervasive shift toward cloud computing, specifically the Software-as-a-Service (SaaS) model, which underpins modern platforms by offering rapid deployment, high scalability, and subscription-based affordability. SaaS eliminates the need for heavy, monolithic on-premise infrastructure, accelerating feature updates and ensuring that clients consistently operate on the latest, most secure version of the software. Complementing the cloud is the adoption of open Application Programming Interfaces (APIs) and microservices architecture, which are critical for achieving seamless interoperability between various disparate systems—including carrier booking platforms, customs portals, and in-house ERP/WMS solutions—thereby creating a truly integrated digital logistics ecosystem.

Artificial Intelligence (AI) and Machine Learning (ML) are rapidly transitioning from niche add-ons to core competencies within freight software solutions, driving true predictive and optimization capabilities. ML algorithms are utilized extensively for route optimization, forecasting demand volatility, predicting estimated time of arrival (ETA) with higher accuracy (often integrating real-time traffic and weather data), and dynamically adjusting pricing based on market capacity. Furthermore, the increasing integration of Internet of Things (IoT) devices—such as sensors embedded in trailers, containers, and assets—generates vast quantities of telemetry data. This data, managed by freight software, provides unprecedented levels of real-time visibility into asset location, condition (temperature, vibration), and security, which is essential for handling sensitive or high-value cargo and improving overall cold chain logistics monitoring.

Another transformative technological area is the deployment of Blockchain technology, primarily in the domain of supply chain transparency and secure documentation. While still nascent in widespread implementation, blockchain holds significant promise for creating immutable records of transactions, ownership transfers, and regulatory compliance documents, drastically reducing administrative fraud and speeding up customs clearance processes by establishing a single, verifiable source of truth accessible to all authorized participants. Simultaneously, the focus on user experience (UX) is driving the development of sophisticated, mobile-optimized applications and user interfaces that provide logistics managers and drivers with intuitive access to complex data and operational instructions, ensuring high adoption rates and practical utility in fast-paced operational environments.

A Freight Transportation Management System (TMS) is specifically designed to optimize the planning, execution, and settlement of physical freight movement, focusing on areas like carrier selection, route optimization, and tracking. An Enterprise Resource Planning (ERP) system is broader, managing core business processes such as finance, HR, and manufacturing; the TMS integrates with the ERP to handle specialized logistics functions, acting as an essential execution layer.

The transition to the Software-as-a-Service (SaaS) model significantly lowers the total cost of ownership (TCO) for Small and Medium-sized Enterprises (SMEs). SaaS platforms eliminate the need for large upfront capital investment in hardware and maintenance, offering flexible subscription models and rapid deployment, thereby democratizing access to enterprise-grade route optimization and visibility tools.

AI plays a critical role in dynamic freight rate management by analyzing historical data, real-time market capacity, and geopolitical factors to predict optimal pricing. Machine Learning algorithms allow shippers and carriers to automate complex tender processes, quickly adapt to fluctuating fuel costs, and ensure highly competitive and profitable pricing strategies based on predictive market analytics.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This accelerated growth is primarily attributed to the explosive expansion of e-commerce, sustained industrialization, massive investments in logistics infrastructure, and increasing governmental mandates for supply chain digitalization across key economies such as China, India, and Southeast Asia.

The primary security concerns for cloud-based freight software include data breaches, especially related to sensitive shipment and customer information, and the risk of unauthorized access due to reliance on external third-party cloud infrastructure. Vendors must mitigate these risks through multi-factor authentication, robust data encryption protocols, adherence to strict regional compliance standards (e.g., GDPR), and continuous vulnerability monitoring.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.