ID : MRU_ 431965 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

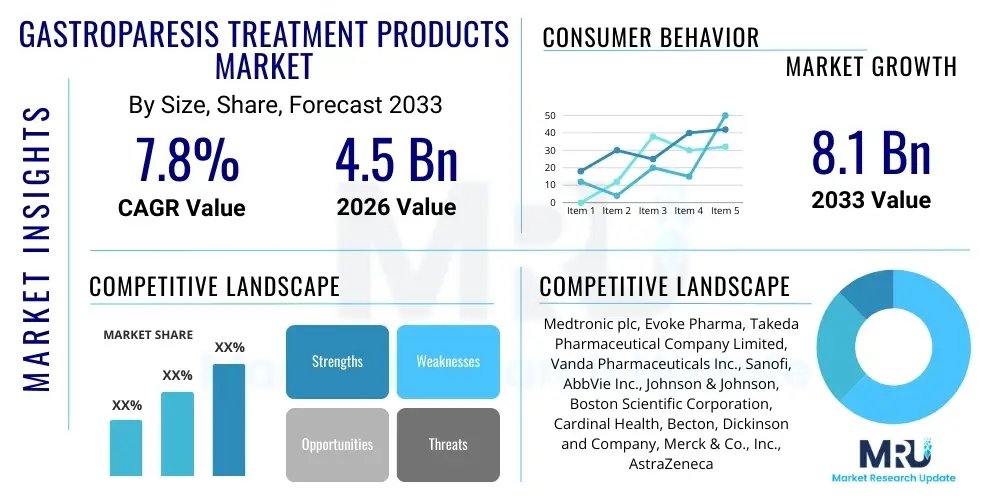

The Gastroparesis Treatment Products Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 8.1 Billion by the end of the forecast period in 2033.

Gastroparesis, a chronic digestive disorder characterized by delayed gastric emptying in the absence of mechanical obstruction, represents a significant unmet medical need globally. The complexity of this condition, primarily driven by underlying causes such as diabetes (diabetic gastroparesis) and idiopathic origins, necessitates a diverse and expanding range of therapeutic interventions. The market for gastroparesis treatment products encompasses pharmaceuticals, including prokinetic agents and antiemetics, alongside advanced medical devices like gastric electrical stimulators (GES) and surgical intervention products. Market growth is fundamentally supported by the increasing global prevalence of Type 1 and Type 2 diabetes, which is the leading cause of the condition, coupled with rising clinical awareness and advancements in diagnostic technologies, enabling earlier and more accurate identification of affected populations. These foundational elements drive demand for both symptomatic relief and disease-modifying therapies, emphasizing the need for robust R&D pipelines focused on novel mechanisms of action.

The product portfolio within this therapeutic space is heavily weighted towards pharmacological solutions aimed at improving gastric motility and alleviating core symptoms such as chronic nausea, vomiting, abdominal pain, and early satiety. Prokinetic drugs, such as metoclopramide and domperidone, form the established cornerstone of treatment, despite limitations related to efficacy, long-term safety profiles, and potential neurological side effects, particularly tardive dyskinesia associated with prolonged metoclopramide use. Consequently, there is sustained commercial and scientific interest in developing new classes of prokinetic agents and therapies that target specific receptors involved in gastric motility regulation, such as ghrelin receptor agonists and serotonin receptor modulators. Furthermore, the rising burden of refractory gastroparesis, unresponsive to standard pharmaceutical care, validates the increasing adoption and technological refinement of implantable devices, providing alternative, often palliative, management strategies for severely debilitated patients.

Major applications of these treatment products extend beyond symptom management to encompass improving nutritional status and overall quality of life for patients. The benefits include enhanced gastric emptying rates, reduced hospitalizations due to dehydration or severe vomiting, and better glycemic control in diabetic patients, as unpredictable food absorption complicates insulin management. Key driving factors include the high economic burden associated with untreated gastroparesis, pushing healthcare systems toward more effective chronic management; significant investments by pharmaceutical and medical device companies in clinical trials for specialized orphan drugs; and favorable regulatory pathways, such as the U.S. Food and Drug Administration’s (FDA) encouragement of treatments for rare and severe gastrointestinal disorders. The ongoing shift toward minimally invasive procedural options also contributes to the positive trajectory of the device segment, promising better outcomes and shorter recovery times for appropriate patient populations.

The Gastroparesis Treatment Products Market exhibits dynamic growth propelled by persistent unmet clinical needs and significant pipeline activity focused on both pharmacological and non-pharmacological interventions. Current business trends indicate a critical pivot toward precision medicine approaches, utilizing biomarkers to stratify patients and match them to the most suitable existing or investigational therapies, thereby enhancing treatment efficacy and minimizing adverse events. There is a palpable trend of consolidation among specialized pharmaceutical firms and larger biotechnology companies seeking to acquire promising late-stage assets, particularly those targeting novel receptors or demonstrating improved safety profiles over generic prokinetics. Furthermore, the integration of advanced patient monitoring technologies and smart drug delivery systems is enhancing adherence and providing real-time data on treatment response, strengthening the overall therapeutic landscape and driving value creation across the market ecosystem. Emphasis on health economics and outcomes research (HEOR) is also gaining prominence, aiming to justify the premium pricing of novel treatments by demonstrating superior long-term cost-effectiveness compared to the current standard of care.

Regional trends reveal that North America, particularly the United States, commands the largest market share, attributable to high diabetes prevalence, sophisticated healthcare infrastructure, favorable reimbursement policies for specialized treatments, and robust expenditure on advanced medical devices, such as gastric electric stimulators. Europe follows, presenting a mature market structure with increasing awareness and adoption of newer therapies, although regulatory approvals often exhibit variation across member states, impacting market penetration timelines. Asia Pacific is emerging as the fastest-growing region, driven by the escalating incidence of diabetes linked to demographic shifts and lifestyle changes, coupled with rapid modernization of healthcare facilities and expanding access to specialized gastrointestinal care in major economies like China and India. These emerging markets represent substantial future growth opportunities, contingent upon successful navigation of diverse regulatory landscapes and adaptation of treatment costs to regional economic capacities.

Segmentation trends highlight the enduring dominance of the pharmaceutical segment, specifically prokinetic agents, due to their established role as first-line therapy. However, the device segment, particularly the gastric electrical stimulation (GES) sub-segment, is experiencing accelerated growth driven by technological improvements, increased efficacy data in refractory patients, and expanding insurance coverage for these high-cost interventions. Within the drug class, a noticeable shift is occurring toward novel proprietary compounds, including ghrelin agonists and specific 5-HT4 receptor agonists, promising better tolerability and fewer systemic side effects compared to older agents. End-user analysis underscores the pivotal role of hospitals and specialized gastroenterology clinics, which remain the primary points of diagnosis, treatment initiation, and surgical/device implantation, necessitating strong marketing and distribution strategies targeted at these institutional purchasers and specialized prescribers to maximize market penetration across all therapeutic modalities.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Gastroparesis Treatment Products Market frequently center on its role in expediting drug discovery for novel prokinetic agents, improving the diagnostic accuracy and timeliness of delayed gastric emptying, and enabling personalized treatment protocols. Users are keenly interested in how machine learning algorithms can analyze vast datasets from clinical trials, electronic health records (EHRs), and patient-reported outcomes to identify unique biomarkers or patient subgroups that respond best to specific treatments, moving away from the current one-size-fits-all approach. Furthermore, there is significant inquiry into AI's capability to enhance the performance and predictability of medical devices, such as optimizing the programming parameters for gastric electrical stimulators in real-time based on patient physiological responses, thereby maximizing therapeutic benefit and reducing the need for iterative clinical adjustments. The core themes revolve around efficiency, personalization, and the potential for AI to de-risk the R&D process, bringing highly effective treatments to market faster for this challenging chronic condition.

The transformative effect of AI on market dynamics stems from its ability to revolutionize early-stage research and development. In drug design, AI algorithms can predict the efficacy and toxicity of potential drug candidates against various targets associated with gastric motility regulation (e.g., dopamine receptors, serotonin receptors, motilin pathways) far more rapidly than traditional laboratory methods. This accelerated screening process significantly reduces the time and cost associated with identifying lead compounds, which is crucial for a therapeutic area often categorized by limited R&D investment relative to major diseases. By analyzing genetic and proteomic data from gastroparesis patients, AI can help researchers understand the heterogeneous nature of the disease, leading to the development of highly specific compounds designed to address different underlying pathophysiologies, such as neuropathic versus myogenic causes of gastric delay.

Beyond drug discovery, AI’s impact is pronounced in clinical decision support and patient management. Machine learning models are being deployed to analyze high-resolution imaging data, such as scintigraphy scans, to quantify gastric emptying rates with higher precision and lower inter-observer variability, assisting clinicians in definitive diagnosis. In the context of chronic management, AI-powered predictive analytics utilize continuous glucose monitoring data (for diabetic gastroparesis) and symptom trackers to forecast flare-ups or adverse drug reactions, allowing for proactive adjustments in medication dosage or dietary advice. This proactive, data-driven management enhances patient outcomes, reduces healthcare utilization (e.g., emergency room visits), and ultimately validates the value proposition of both pharmaceutical and device treatments, thereby strengthening market uptake and optimizing resource allocation within healthcare systems globally.

The market for gastroparesis treatment products is heavily influenced by a unique combination of compelling growth drivers, significant regulatory and clinical restraints, and high-value opportunities that collectively shape its trajectory and competitive landscape. The primary driver is the exponentially rising global incidence of chronic diseases, particularly diabetes mellitus, which remains the single largest risk factor for developing gastroparesis; as the diabetic population expands, so does the pool of patients requiring specialized gastrointestinal care. Secondly, substantial advancements in understanding the complex pathophysiology of gastroparesis, including the roles of interstitial cells of Cajal (ICCs) and neuronal signaling, are catalyzing investment in innovative drug targets, moving the focus beyond historical prokinetic agents. These technological and epidemiological forces create a persistent demand floor that supports market expansion, irrespective of short-term economic fluctuations, as the condition severely impacts quality of life and necessitates continuous management, driving consistent pharmaceutical and device consumption.

However, the market faces notable restraints that temper its aggressive growth potential. A significant challenge lies in the limited long-term efficacy and unfavorable side-effect profiles associated with many currently approved pharmacological treatments; metoclopramide, a frontline therapy, carries a Black Box Warning regarding irreversible movement disorders, prompting prescribers and patients to seek safer alternatives. Furthermore, the high cost and invasive nature of advanced treatments, particularly gastric electrical stimulation devices, often necessitate stringent prior authorization and comprehensive insurance coverage, which can create access barriers for large patient segments, especially in developing economies or systems lacking robust reimbursement frameworks. The diagnostic process itself is complex, relying on highly specialized procedures like gastric emptying scintigraphy, leading to underdiagnosis or delayed diagnosis in primary care settings, thus limiting the recognized patient population eligible for treatment.

Despite these barriers, substantial opportunities exist, primarily revolving around technological and therapeutic innovation. The market presents a fertile ground for the development of drugs that qualify for Orphan Drug Designation, offering pharmaceutical companies extended market exclusivity and tax benefits, significantly de-risking the R&D process. Opportunities also arise from the exploration of non-conventional therapies, such as highly selective peripheral dopamine antagonists, cannabinoid receptor modulators for symptom management, and novel drug delivery systems that improve local action and reduce systemic exposure. Furthermore, the development of non-invasive, more accurate diagnostic tools would unlock the hidden patient population, expanding the total addressable market. The ultimate impact force is the synergy between rising disease prevalence and focused R&D, where the dire need for effective, safe, and long-lasting treatments dictates the pace of innovation and market adoption, forcing companies to continually invest in next-generation solutions that address the condition’s chronic and refractory nature.

The Gastroparesis Treatment Products Market is comprehensively segmented based on three primary categories: Treatment Type, Drug Class, and End-User, providing granular insights into market dynamics and consumption patterns across various therapeutic modalities. The segmentation by Treatment Type distinguishes between Pharmacological Treatments (drugs) and Medical Devices, reflecting the clinical dichotomy between systemic drug interventions and local procedural management. This differentiation is crucial as devices often target refractory cases, commanding higher unit prices but serving a smaller, more severely affected patient pool, while pharmaceuticals maintain dominance in volume due to their role in initial and maintenance therapy. Analyzing these segments helps stakeholders understand investment priorities, directing resources toward either high-volume drug production or high-value, technologically intensive device development, dependent on specific market penetration strategies and pipeline assets.

Further granularity is achieved through the Drug Class segmentation, which typically includes Prokinetics (motility enhancers), Antiemetics (nausea and vomiting control), and Botulinum Toxin Injections, recognizing that gastroparesis management relies heavily on controlling specific debilitating symptoms. Prokinetics remain the largest sub-segment, driven by the attempt to address the root cause of delayed emptying, yet the high growth potential resides in proprietary, specialized drug classes that are safer or offer novel mechanisms. The End-User segmentation primarily divides consumption between Hospitals and Specialty Clinics, and Ambulatory Surgical Centers (ASCs). Hospitals and specialty clinics are crucial for complex diagnosis, initiation of advanced pharmacotherapy, and device implantation, while ASCs gain relevance for less invasive procedures or follow-up device maintenance. Understanding end-user dynamics is vital for effective distribution, training, and sales strategy development within the highly specialized gastrointestinal market.

Overall market segmentation reveals a therapeutic environment shifting toward customized and combined treatment approaches. The market witnesses sustained growth in the Antiemetics sub-segment as symptom control is paramount, often used adjunctively with prokinetics or devices. The emerging importance of combination therapies—using a device alongside tailored pharmacological agents—is driving demand for synergistic product development and integrated care pathways. This structure facilitates targeted marketing, allowing companies to position their products precisely—be it an advanced GES system for severe, refractory diabetic patients within a hospital setting, or a novel orally active prokinetic for long-term home use managed through specialized clinics. The future market structure is expected to further segment based on the underlying etiology (diabetic vs. idiopathic vs. post-surgical gastroparesis) as diagnostic capabilities improve.

The value chain for the Gastroparesis Treatment Products Market is complex, stretching from initial drug discovery and raw material sourcing to specialized patient delivery and post-market surveillance, reflecting the high-value, highly regulated nature of pharmaceuticals and medical devices. The upstream segment is characterized by intense research and development activities, involving biotech startups, academic institutions, and large pharmaceutical companies collaborating to identify and synthesize novel molecular entities or design advanced biocompatible materials for devices. Key activities include clinical trials management, scale-up manufacturing of active pharmaceutical ingredients (APIs), and ensuring strict compliance with Good Manufacturing Practices (GMP). The efficiency of this upstream phase dictates the introduction timeline and the initial cost structure of the final product, with success heavily reliant on securing robust intellectual property protection and efficient synthesis protocols for complex proprietary compounds.

The middle segment of the value chain focuses on manufacturing, production, and distribution. For pharmaceuticals, this involves formulation, packaging, and quality control, while for devices, it involves intricate assembly, sterilization, and calibration of complex electronic components such as those found in gastric electrical stimulators. Distribution channels are specialized, owing to the therapeutic area’s focus on chronic care and requiring temperature-controlled logistics for certain biological or injectable products. The distribution mechanism operates via a mix of direct and indirect channels: direct distribution is often employed for high-value medical devices requiring specialized sales representatives and technical support for hospital procurement and training, ensuring proper implantation and post-operative management. Indirect distribution, leveraging wholesalers, distributors, and pharmacy chains, is dominant for widely used prescription drugs and over-the-counter antiemetics, ensuring broad market access and compliance with regional supply chain regulations.

The downstream analysis covers marketing, sales, prescription/procedure, and post-market services. Demand generation relies heavily on professional medical education, targeting gastroenterologists, endocrinologists, and general practitioners to enhance disease awareness and appropriate prescribing patterns. The final point of delivery—the healthcare provider (hospital or clinic)—is where the product is utilized. Post-market activities, including patient support programs, technical device servicing, warranty provision, and mandated pharmacovigilance (adverse event reporting), are crucial for maintaining product reputation, ensuring patient safety, and securing long-term market acceptance. The value generated at this stage is measured by patient adherence, improved quality of life metrics, and favorable health outcomes, all of which are essential for continued reimbursement and market success.

The primary customers and end-users of Gastroparesis Treatment Products are diverse, spanning both institutional purchasers and the individual patients themselves. Hospitals, particularly those with specialized gastrointestinal units, academic medical centers, and large regional health systems, constitute the largest volume purchasers of both high-cost medical devices (GES systems) and bulk pharmaceutical supplies required for inpatient treatment and pre-surgical stabilization. These institutional buyers are focused not only on cost and efficacy but also on bundled solutions, integration with existing surgical infrastructure, and favorable contract terms that include training and technical support for complex device implantation procedures. Furthermore, dedicated specialty clinics and smaller private gastroenterology practices serve as critical customers for initial diagnosis, long-term outpatient drug management, and maintenance care, requiring consistent, reliable supply of prescription medications tailored for chronic use.

A second crucial customer group comprises endocrinologists and diabetologists, who frequently manage the largest population segment—patients with diabetic gastroparesis. While not always the direct point of sale, these specialists are key influencers in the referral and prescribing pathways for advanced treatments, making them a high-priority target for pharmaceutical companies promoting novel diabetic-focused therapies. Pharmacists and pharmacy benefit managers (PBMs) act as powerful intermediaries, controlling formulary inclusion and patient access, especially for high-cost proprietary drugs, meaning market penetration often hinges on favorable formulary status secured through detailed negotiation and demonstration of clinical utility and economic value against established generics.

Finally, the individual patients suffering from chronic gastroparesis, and their caregivers, represent the ultimate beneficiaries and consumers. Their purchasing decisions (often mediated by insurance coverage) are driven by the need for symptom relief, improved quality of life, and reduced long-term complications. Patient advocacy groups and direct-to-consumer information channels play an increasing role in educating this segment, influencing demand for newer, more tolerable, and efficacious treatments. Therefore, successful market strategy requires addressing the clinical needs of specialists, the procurement requirements of institutions, and the safety/efficacy concerns of the patients and payers who ultimately foot the bill for chronic care.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.1 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Evoke Pharma, Takeda Pharmaceutical Company Limited, Vanda Pharmaceuticals Inc., Sanofi, AbbVie Inc., Johnson & Johnson, Boston Scientific Corporation, Cardinal Health, Becton, Dickinson and Company, Merck & Co., Inc., AstraZeneca, Salix Pharmaceuticals, Neurogastrx, Inc., Novartis AG, GlaxoSmithKline plc, Pfizer Inc., Teva Pharmaceutical Industries Ltd., Alfasigma S.p.A., Allergan (now part of AbbVie) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Gastroparesis Treatment Products Market is characterized by innovation focused on improving patient outcomes, reducing systemic side effects, and offering less invasive treatment modalities. In the device sector, the technology centers predominantly on Gastric Electrical Stimulation (GES) systems, such as the Enterra Therapy system. Recent advancements in GES technology focus on developing smarter, smaller, and more energy-efficient neurostimulators with enhanced programming capabilities. Next-generation GES systems are exploring adaptive stimulation protocols that adjust output based on real-time physiological feedback, potentially leveraging AI-driven algorithms to customize therapy delivery, thus moving beyond fixed parameters to optimize electrical impulses aimed at the stomach’s myoelectric activity. Furthermore, there is growing interest in non-invasive neuromodulation techniques, such as transcutaneous electrical nerve stimulation (TENS) applied externally, which aims to provide symptomatic relief without the surgical burden associated with device implantation, expanding accessibility for patients unwilling or unable to undergo surgery.

In the pharmacological domain, the technology landscape is rapidly evolving away from broad-spectrum prokinetics toward highly selective agents and novel delivery mechanisms. Key technological advancements include the development of ghrelin receptor agonists (e.g., relamorelin), which specifically target the ghrelin pathway to accelerate gastric emptying with greater precision than dopamine antagonists, potentially offering superior efficacy and reduced central nervous system side effects. Additionally, the development of specialized formulations designed to enhance bioavailability and targeted drug release within the gastrointestinal tract is a major technological focus. For example, local delivery systems, such as proprietary oral dissolution tablets or unique injectable formulations, aim to maximize the concentration of the therapeutic agent where it is needed—the stomach and duodenum—while minimizing systemic exposure, thereby enhancing the therapeutic index and improving patient compliance for chronic conditions.

The emerging technological frontier involves biological treatments and minimally invasive procedural innovations. Research into regenerative medicine and gene therapy is exploring methods to restore function to damaged vagus nerves or the interstitial cells of Cajal (ICCs), which are critical for initiating and propagating gut motility. While still nascent, these technologies hold the promise of disease modification rather than just symptom management. Procedurally, technological adoption of minimally invasive endoscopic treatments, such as Gastric Per-Oral Endoscopic Myotomy (G-POEM) and endoscopic pyloromyotomy, utilizing high-definition endoscopic instruments and specialized cutting devices, represents a significant shift. These techniques offer less trauma and faster recovery compared to traditional open or laparoscopic surgery, providing gastroenterologists with powerful, low-morbidity tools to treat pyloric outlet obstruction often associated with severe gastroparesis, further diversifying the technological tools available for managing this complex disorder.

North America, led by the United States, represents the dominant region in the Gastroparesis Treatment Products Market due to several converging factors, including the highest per capita healthcare spending, advanced infrastructure for specialized gastrointestinal care, and exceptionally high prevalence of Type 2 diabetes, the primary cause of the condition. The market benefits from favorable regulatory frameworks, particularly the FDA's accelerated approval pathways for orphan drugs treating severe GI disorders, encouraging rapid introduction and adoption of novel pharmaceutical agents and sophisticated implantable devices. High awareness levels among both clinicians and patients, coupled with comprehensive insurance coverage for complex procedures like gastric electrical stimulation, solidify North America's leadership position in terms of both market value and early technology adoption, driving demand for premium-priced therapeutic solutions.

Europe holds the second-largest share, demonstrating a mature but steadily expanding market. Growth in major economies like Germany, the UK, and France is fueled by increasing geriatric populations, improved diagnostic standards, and the adoption of clinical guidelines that standardize the management of gastroparesis. However, the market dynamics are slightly fragmented due to varying reimbursement policies and regulatory requirements across the European Union, which can influence market access and pricing strategies for new products. Nevertheless, strong academic research institutions and public health initiatives focused on diabetes management ensure a consistent patient flow and sustained demand for established and innovative treatments across the continent.

Asia Pacific (APAC) is projected to be the fastest-growing region throughout the forecast period. This rapid expansion is primarily driven by the colossal and expanding diabetic population in countries like China and India, translating directly into a rising caseload of diabetic gastroparesis. While current market penetration of advanced devices and proprietary pharmaceuticals is lower compared to Western markets, rapidly improving healthcare infrastructure, increasing disposable incomes, and growing medical tourism are spurring significant investment in specialized gastrointestinal facilities. As access to modern treatment protocols increases and local manufacturing capacity for affordable generic or biosimilar treatments expands, the APAC region will transition from a high-potential market to a high-volume consumption center, posing strategic opportunities for global players seeking geographic diversification.

The primary driver is the surging global prevalence of diabetes mellitus, particularly Type 1 and Type 2 diabetes, which is the leading underlying cause of delayed gastric emptying (diabetic gastroparesis). This high incidence translates directly into a growing patient population requiring specialized pharmacological and device-based interventions for chronic management and symptom relief, fueling sustained demand across all therapeutic categories.

The pharmacological treatment segment, encompassing prokinetic agents and antiemetics, maintains the largest share of the market by volume and value due to its role as the initial and most common long-term therapy prescribed for gastroparesis symptoms. However, the devices segment, specifically Gastric Electrical Stimulators (GES), exhibits a higher compound annual growth rate driven by technological innovation and increasing adoption for refractory, severe cases unresponsive to drug treatment.

Yes, significant safety concerns exist, most notably with Metoclopramide, a frontline prokinetic agent, which carries an FDA Black Box Warning regarding the risk of developing irreversible neurological side effects, such as tardive dyskinesia, particularly with prolonged use. These safety concerns are a major restraint on market growth for older drug classes and actively spur research into novel agents with improved side-effect profiles.

AI is set to revolutionize the market by accelerating the discovery of novel therapeutic targets, improving the precision and speed of diagnostic imaging interpretation (e.g., scintigraphy), and enabling highly personalized dosing and treatment regimens. AI tools will optimize the performance of implantable devices and enhance patient monitoring through predictive analytics, leading to better clinical outcomes and faster market access for innovative solutions.

The Asia Pacific (APAC) region is projected to register the highest growth rate during the forecast period. This acceleration is attributed to the rapidly expanding diabetic population in major emerging economies (China, India), coupled with significant improvements in healthcare infrastructure, increased patient awareness, and growing economic capacity to adopt both standard and advanced therapeutic products for chronic gastrointestinal disorders.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.