ID : MRU_ 433720 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

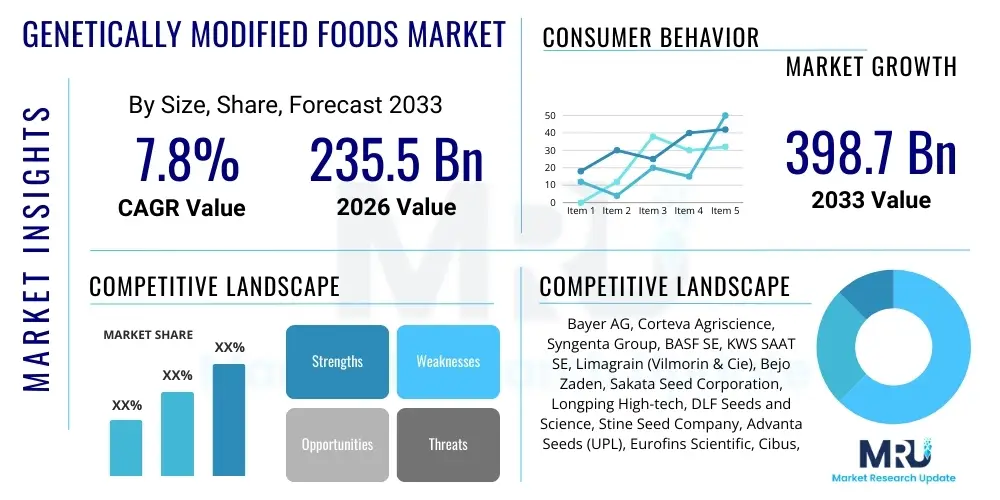

The Genetically Modified Foods Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 235.5 Billion in 2026 and is projected to reach USD 398.7 Billion by the end of the forecast period in 2033. This growth trajectory is fundamentally driven by the escalating global demand for enhanced agricultural productivity, necessitated by rapid population growth and the diminishing availability of arable land, coupled with increasing climatic volatility across key agricultural regions.

The Genetically Modified (GM) Foods Market encompasses food products derived from organisms whose genetic material (DNA) has been altered in a way that does not occur naturally through mating or natural recombination. This alteration typically introduces desired traits, such as increased resistance to pests, improved tolerance to herbicides, enhanced nutritional value, or resistance to environmental stresses like drought. Key products currently dominating the market include herbicide-tolerant and insect-resistant varieties of staple crops such as corn, soy, canola, and cotton, which form the primary input for various processed food items and animal feed globally. The development of GM foods represents a significant technological advancement aimed at addressing pressing global food security challenges.

Major applications of GM technology extend across food production and animal agriculture. In human nutrition, applications focus on crops engineered for better quality (e.g., Golden Rice engineered for enhanced Vitamin A content) and greater yield stability. In animal agriculture, GM feed accounts for a substantial portion of the market, impacting the cost structure and efficiency of livestock production. Furthermore, GM foods offer inherent benefits including reduced reliance on chemical pesticides, lower production costs for farmers in specific regions, and the potential to cultivate crops in marginal lands previously considered unproductive. These improvements contribute directly to stabilizing commodity prices and increasing the reliability of the global food supply chain, particularly critical in the face of climate change impacts.

The market is primarily driven by macro-economic factors such as sustained population expansion, which dictates an urgent need for higher agricultural output, and technological breakthroughs, particularly in gene editing techniques like CRISPR/Cas9, which are accelerating the development of new, more precise traits. Government initiatives in major agricultural economies, aimed at promoting sustainable farming practices and securing domestic food reserves, also provide significant impetus. However, the market's progression remains tightly linked to consumer acceptance and the complex regulatory frameworks governing the cultivation and importation of GM crops across different nations, highlighting a persistent tension between scientific innovation and public perception.

The Genetically Modified Foods Market is characterized by robust business trends centered on consolidation among major biotechnology corporations and intense research and development focused on next-generation gene editing technologies, moving beyond simple input traits (herbicide tolerance) to output traits (enhanced nutrition, extended shelf life). Business strategies are increasingly focused on licensing agreements and partnerships between seed developers and regional distributors to navigate fragmented regulatory landscapes and ensure market penetration in fast-growing developing economies. Furthermore, the rising investment in digital agriculture and precision breeding tools is optimizing R&D expenditure and accelerating the time-to-market for novel GM products, establishing a strong foundation for sustained revenue expansion through the forecast period.

Regionally, North America remains the dominant revenue generator, characterized by high adoption rates for GM corn, soy, and cotton, supported by a clear and established regulatory pathway, which fosters innovation and commercialization. Asia Pacific (APAC), however, is projected to exhibit the fastest growth rate, fueled by substantial investments in agricultural biotechnology in populous nations like China and India, driven by acute necessity to enhance food self-sufficiency and manage environmental challenges like water scarcity. Conversely, the European market remains constrained by stringent regulatory frameworks and strong consumer preference for non-GM labeling, forcing market players to adopt differentiated regional strategies focusing on specialized feed applications or indirect sourcing channels.

From a segmentation perspective, the market is primarily dominated by the Crop segment, specifically focusing on maize, soybean, and canola, due to their widespread use in animal feed and processed foods. The Trait segment highlights the continuing dominance of Herbicide Tolerance (HT) and Insect Resistance (IR), often stacked together in single varieties, providing multi-layered protection. However, the fastest-growing segments relate to advanced nutritional traits and stress tolerance traits (drought/salinity resistance), reflecting a shift in R&D focus toward climate resilience. Regulatory trends are crucial, with non-transgenic gene-edited products potentially opening new consumer-friendly segments previously inaccessible to traditional GM approaches, signaling future market diversification.

User queries regarding the impact of Artificial Intelligence (AI) on the Genetically Modified Foods market frequently center on three critical themes: the speed and precision of developing new traits, the ethical implications of AI-driven optimization, and the role of AI in ensuring the safety and regulatory compliance of novel GM products. Users are highly interested in how Machine Learning (ML) can accelerate the notoriously long R&D cycle for GM crops, particularly through predictive genomics and gene function modeling. There is a clear expectation that AI will drastically reduce the costs and timelines associated with traditional trial-and-error breeding and transformation processes, leading to faster deployment of climate-resilient crops.

Concerns often revolve around data privacy in precision agriculture, ensuring that AI models used for trait optimization are unbiased, and the potential for increased market concentration if AI tools become proprietary to a few dominant biotechnology players. Furthermore, users frequently question how AI algorithms can assist regulatory bodies in risk assessment, especially concerning off-target effects in gene-edited organisms. The core consensus is that AI is transformative, capable of synthesizing vast biological and environmental data sets to identify optimal genetic combinations and assess the performance of new varieties under diverse field conditions before physical planting, thereby optimizing resource allocation and enhancing the reliability of the R&D pipeline.

Ultimately, AI adoption is shifting the paradigm from 'trial and error' experimentation to 'predictive optimization.' By integrating data from genomics, proteomics, metabolomics, and environmental sensors, AI provides researchers with unprecedented foresight into trait expression and stability. This analytical power not only accelerates the discovery phase but also significantly improves the efficiency of field trials, allowing companies to focus resources on the most promising candidates, thereby lowering the cost barrier for introducing new GM traits essential for addressing global agricultural challenges.

The Genetically Modified Foods Market is shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively form the Impact Forces dictating market trajectory. Key drivers include the critical need to enhance global food security amid escalating population figures and climate change-induced agricultural volatility, necessitating high-yielding and resilient crops. Restraints predominantly center on pervasive consumer distrust and opposition, particularly in Europe and parts of Asia, coupled with complex, non-harmonized regulatory regimes across different nations, which create significant barriers to entry and operational costs for market participants. Opportunities are largely concentrated in advanced molecular techniques, such as CRISPR/Cas9, which allow for subtle, non-transgenic edits that may face less regulatory scrutiny and higher consumer acceptance compared to traditional transgenic modifications, alongside expansion into developing economies where the need for enhanced yield is most pressing.

The primary driving force is the imperative for efficiency gains in agriculture. Drivers such as the success of existing GM crops (e.g., HT and IR varieties drastically reducing pesticide use and increasing farmer profitability) create strong market pull, especially in large agricultural markets like North and South America. Furthermore, increasing investment by both public and private sectors into developing climate-smart traits, such as those resistant to extreme heat or salinity, underscores the long-term strategic importance of GM technology. These drivers propel market growth by making GM varieties an economically viable and environmentally sensible option for large-scale commercial farming operations facing diminishing natural resources.

Conversely, the greatest restraint remains the fragmented global regulatory environment. The lack of uniformity in labeling requirements, approval processes, and acceptable modification types means that a GM product approved in one region may be strictly banned in another, hindering international trade and technology transfer. Public perception, often influenced by powerful non-governmental organizations and sensationalized media reports focusing on perceived long-term health or environmental risks, also severely restricts market penetration, particularly in high-value consumer segments. However, the opportunity landscape is highly promising, particularly through innovations in advanced breeding techniques that circumvent regulatory definitions of "GM," opening the door for rapid commercialization of crops with enhanced nutritional profiles or specialized industrial uses, promising significant future revenue streams.

The Genetically Modified Foods market segmentation provides a detailed structure for analyzing market performance based on Crop Type, Trait, and Geography. The market is fundamentally segmented by the type of crop modified, with major field crops like corn, soy, and canola dominating due to their sheer volume in global agriculture and processing. Segmentation by trait reveals the functionality introduced by genetic modification, primarily focusing on input traits like herbicide tolerance and insect resistance, which offer immediate economic benefits to farmers. The geographical segmentation highlights major differences in regulatory acceptance and market maturity, driving differential growth rates across regions. This structured analysis is essential for companies to tailor their product development and market entry strategies based on specific regulatory and end-user requirements.

The value chain for the Genetically Modified Foods Market is complex, beginning with intensive upstream research and development, transitioning through seed production and distribution, and concluding with downstream processing, retail, and end-user consumption. The upstream segment is dominated by a few multinational life science companies that invest heavily in genomic research, gene discovery, and trait development, often requiring decades and billions of dollars to bring a new trait to market. This stage involves sophisticated molecular biology techniques and rigorous field testing to ensure efficacy, stability, and safety. Intellectual property protection, primarily via patents covering novel genes and transformation methods, is the most crucial element at this initial stage, creating significant barriers to entry for smaller players.

Midstream activities involve the scaling up of successful GM seeds. This includes large-scale multiplication of the proprietary seed varieties and the initial processing phases. The distribution channel is bifurcated into direct and indirect routes. Direct sales occur when major biotech firms sell directly to large commercial farming operations. Indirect channels involve collaboration with a network of licensed local seed distributors and agricultural input retailers who handle smaller farm sales and provide critical on-the-ground technical support and educational services to ensure proper use of the GM technology. Effective management of this distribution network is crucial for maximizing market penetration, especially in diverse agricultural landscapes found in APAC and LATAM.

The downstream segment encompasses food processors, manufacturers, and eventually, the end-user (consumer). Since the majority of GM crops (corn, soy) are used as commodities, the downstream market is focused on bulk trading and processing into secondary products like oils, flours, starches, and animal feed. Traceability and labeling requirements play a significant role at this stage, particularly in regions like the EU, where stringent labeling mandates require segregation of GM and non-GM derived products. The performance of the entire value chain is heavily dependent on regulatory approval at multiple jurisdictional levels, making streamlined compliance and efficient logistics management essential for mitigating risk and maintaining profitability.

The primary potential customers and end-users of the Genetically Modified Foods market span several large sectors, dictated by how the raw GM materials are utilized. Commercial farmers represent the immediate buyers of GM seeds, deriving direct benefit from reduced input costs (pesticides, labor) and increased yield stability. These farmers are categorized by scale, ranging from large-scale corporate agricultural enterprises in the Americas that dominate commodity production, to smaller, subsistence-level farmers in emerging markets seeking yield stability to ensure food security for their families and local communities. Their purchasing decision is fundamentally driven by the return on investment (ROI) offered by the proprietary traits.

Further down the value chain, the largest volume consumers are the Animal Feed Industry and the Food Processing Industry. The animal feed sector relies heavily on GM corn and soy for cost-effective livestock production (poultry, swine, cattle). Maintaining low feed costs is critical for stabilizing meat prices globally, making reliable supply of GM commodities indispensable. The food processing industry utilizes GM-derived ingredients (oils, starches, sweeteners) in a vast array of processed and packaged foods. Major food and beverage manufacturers are constantly seeking assurances regarding the purity, safety, and consistent supply of these high-volume ingredients, often leading to complex purchasing contracts with commodity traders.

Institutional buyers, such as governmental food aid programs and large distributors serving institutional catering (schools, hospitals), also represent significant potential customers, especially when purchasing staple crops where yield optimization is paramount for humanitarian objectives. Finally, the consumer remains the ultimate, albeit often indirectly influenced, end-user. While consumers do not purchase GM seeds, their perception, regulatory environment influence, and purchasing preferences for labeled or unlabeled products ultimately shape retail demand, driving the strategic focus of food manufacturers towards either GM or non-GM ingredient sourcing based on market segment demands.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 235.5 Billion |

| Market Forecast in 2033 | USD 398.7 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bayer AG, Corteva Agriscience, Syngenta Group, BASF SE, KWS SAAT SE, Limagrain (Vilmorin & Cie), Bejo Zaden, Sakata Seed Corporation, Longping High-tech, DLF Seeds and Science, Stine Seed Company, Advanta Seeds (UPL), Eurofins Scientific, Cibus, Precision BioSciences, Yield10 Bioscience, Calyxt, Arcadia Biosciences, Bioceres Crop Solutions, Benson Hill. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Genetically Modified Foods Market is rapidly evolving, driven by innovations that prioritize precision, efficiency, and potentially lower regulatory friction. Traditional genetic modification techniques relied on methods such as Agrobacterium-mediated transformation or gene guns to insert foreign DNA segments (transgenes) into the host genome. While successful, these methods often result in random insertion sites and are associated with stringent regulatory requirements. Current R&D is heavily shifting towards leveraging advanced molecular tools that offer superior control and reduce the integration of foreign DNA, focusing instead on internal gene manipulation.

The most significant technological breakthrough shaping the market is the adoption of New Breeding Techniques (NBTs), specifically clustered regularly interspaced short palindromic repeats (CRISPR/Cas systems) and other site-directed nucleases (SDNs). CRISPR allows for highly precise edits, such as deleting, inserting, or modifying specific genetic sequences without necessarily introducing genes from different species. Products developed using NBTs, particularly SDN-1 edited products that only involve minor, targeted base-pair changes, are being reviewed by regulatory bodies in some jurisdictions (e.g., the U.S. and parts of South America) as equivalent to traditionally bred crops, potentially bypassing the lengthy and costly GM approval process. This paradigm shift offers tremendous opportunities for rapid trait development.

Furthermore, the integration of computational biology and high-throughput screening technologies is transforming the discovery pipeline. Genomics, transcriptomics, and metabolomics provide massive data sets, which, when analyzed using AI and Machine Learning, significantly accelerate the identification of beneficial genetic markers and the successful design of gene-editing experiments. Technologies such as speed breeding, which uses optimized environmental conditions to cycle generations quickly, are also being combined with genetic engineering to compress the time required for trait stacking and commercial deployment, ensuring that the industry can respond more rapidly to dynamic climate and pest challenges globally.

The global Genetically Modified Foods Market exhibits significant regional disparities in terms of adoption rates, regulatory climate, and market maturity, making regional analysis crucial for understanding market dynamics. North America, encompassing the United States and Canada, represents the most mature and largest market globally. This dominance is attributed to the early and widespread commercial adoption of GM crops (especially corn, soy, and canola), strong governmental support for biotechnology, and a relatively clear, predictable regulatory framework managed by agencies like the USDA, FDA, and EPA. Farmers in this region heavily utilize stacked-trait varieties to maximize yields and minimize input costs, establishing the region as the global benchmark for commercial GM agriculture.

Asia Pacific (APAC) is projected to be the fastest-growing market during the forecast period. This rapid growth is propelled by the need for greater domestic food security in high-population economies like China and India, coupled with increasing government investment in advanced agricultural biotechnology R&D. While regulatory approvals can be slow and complex, the sheer necessity for crops resistant to endemic regional pests and suitable for drought-prone areas is driving adoption. China, in particular, has ramped up its commercialization efforts for domestic GM corn and soy varieties to reduce reliance on imports, positioning APAC as the critical growth engine for future global GM food expansion.

Conversely, the European market presents a unique and challenging landscape. Europe maintains some of the most stringent regulations globally, characterized by mandatory labeling and often highly restrictive approval processes for both cultivation and importation of GM crops, stemming from deep-seated consumer skepticism. Consequently, while limited GM cultivation occurs, the primary market activity involves the massive importation of GM commodities (mainly soy and corn) used exclusively for animal feed, creating a highly segmented and complex supply chain structure designed to segregate GM and non-GM derived products effectively.

The primary drivers include the urgent global demand for food security fueled by population growth, the necessity for crops resistant to harsh climate changes (like drought and salinity), and the economic benefits derived by farmers through reduced pesticide usage and increased yield stability offered by genetically modified traits.

The market is overwhelmingly dominated by input traits, specifically Herbicide Tolerance (HT), which allows farmers to use broad-spectrum weed killers, and Insect Resistance (IR), typically conferred by Bt genes. These two traits are often combined in 'stacked' varieties of major crops like corn and soybean for maximum protection and efficiency.

NBTs, particularly CRISPR, are revolutionizing the market by allowing precise, targeted gene edits without introducing foreign DNA. This precision can accelerate R&D timelines and may lead to new products that face fewer regulatory hurdles in certain jurisdictions compared to traditional transgenic GM crops, significantly broadening application potential.

Market restraints, especially in Europe, stem primarily from stringent regulatory policies mandating complex approval processes and strict labeling requirements. These constraints are compounded by persistent public skepticism, strong consumer activism, and perceived lack of long-term data on environmental and health impacts, leading to low consumer acceptance for cultivation.

The Asia Pacific (APAC) region is forecasted to achieve the highest Compound Annual Growth Rate (CAGR). This acceleration is driven by major economies such as China and India prioritizing national food self-sufficiency, coupled with increased government funding and regulatory easing for GM crops designed to thrive in challenging regional agricultural environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.