ID : MRU_ 434133 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

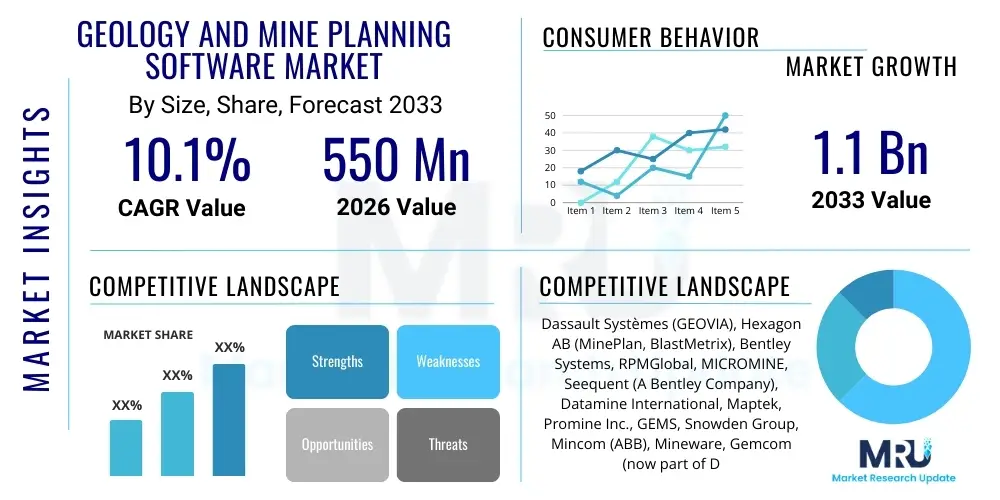

The Geology and Mine Planning Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.1% between 2026 and 2033. The market is estimated at $550 Million USD in 2026 and is projected to reach $1.1 Billion USD by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the global imperative for resource efficiency, coupled with the increasing adoption of digital transformation initiatives across the mining lifecycle, from initial exploration through to sustainable mine closure. The transition from traditional, manual planning methods to sophisticated, integrated software platforms is essential for optimizing operational performance, reducing capital expenditure, and ensuring regulatory compliance, particularly in deep-sea and remote mining environments where precise geological modeling is non-negotiable for safety and profitability.

The acceleration of infrastructure development and the increasing global demand for critical minerals—such as lithium, cobalt, and rare earth elements—are primary catalysts driving the adoption of advanced planning tools. These tools allow mining companies to accurately simulate complex geological structures, optimize blast patterns, and manage tailings facilities with greater precision, thereby mitigating environmental risk and maximizing extraction yield. Furthermore, the stringent environmental, social, and governance (ESG) standards being enforced globally necessitate the use of software that can generate auditable records, track sustainability metrics, and facilitate responsible resource development, further solidifying the market’s growth trajectory as companies invest heavily in compliance technology.

The market growth is also significantly influenced by technological convergence, including the integration of geospatial data, remote sensing technologies (like LiDAR and satellite imagery), and machine learning algorithms into core planning modules. This integration enhances the accuracy of resource modeling, enabling predictive maintenance schedules and dynamic mine scheduling that adapts in real-time to changing operational conditions or commodity prices. As mining operations become larger and more complex, particularly in low-grade environments, the necessity of sophisticated software for accurate long-term and short-term planning becomes an indispensable operational requirement, fueling continuous vendor innovation and market penetration.

The Geology and Mine Planning Software Market encompasses specialized computational tools designed to support the entire mining workflow, starting from initial geological data acquisition and interpretation through to comprehensive operational scheduling and financial closure. These products provide geologists and mining engineers with capabilities for 3D modeling of ore bodies, geostatistical analysis, resource estimation, pit optimization, mine design (including tunnels and stopes), production scheduling (long-term and short-term), and regulatory reporting. The software enables precise visualization and simulation of complex subterranean environments, reducing risks associated with inaccurate planning, optimizing capital allocation, and ensuring maximum return on investment for high-cost mining projects.

Major applications of this software suite span across both surface mining (open-pit) and underground operations, covering diverse commodities such as metals (gold, copper, iron ore), energy minerals (coal, uranium), and industrial minerals (limestone, potash). Key benefits derived from the utilization of these platforms include enhanced safety through accurate geotechnical modeling, significant improvements in production efficiency achieved via optimized fleet and cycle management, and substantial cost reduction by minimizing waste material movement. These tools standardize data management processes, transforming heterogeneous geological data into unified, actionable intelligence necessary for strategic corporate decision-making and operational execution in geographically dispersed locations.

Driving factors for the market include the global trend toward digitalization in heavy industries, the increasing complexity of accessing deeper and lower-grade deposits, and the imperative for mining companies to demonstrate operational transparency and compliance with global ESG mandates. The volatile nature of commodity prices further compels operators to rely on dynamic planning software to adjust quickly to market fluctuations, maximizing profitability during high-price cycles and minimizing losses during downturns. The demand for higher levels of automation, coupled with the necessity of integrating real-time sensor data from IoT devices within the mine, reinforces the crucial role of sophisticated planning software in the modern mining ecosystem.

The Geology and Mine Planning Software Market is experiencing robust growth driven by accelerating business trends focused on operational resilience and data integration. Key business trends include the shift towards subscription-based software services (SaaS models), favoring operational expenditure over large capital investment, and the increasing consolidation of vendors offering full-lifecycle integrated platforms. Companies are prioritizing solutions that seamlessly connect geological modeling with financial performance metrics, moving away from disparate systems. Technology adoption is high among tier-one miners seeking competitive advantages through predictive analytics and simulation capabilities, while smaller and mid-sized miners are increasingly leveraging cloud-based, scalable solutions to mitigate high upfront IT infrastructure costs.

Regionally, the market is characterized by mature demand in North America and Europe, which are centers for technical innovation and strict regulatory standards, driving investment in high-end geostatistics and geotechnical software. However, the Asia Pacific (APAC) region, spearheaded by mining economies such as Australia and China, exhibits the highest growth potential, fueled by massive investment in large-scale resource exploration and the rapid modernization of existing mining infrastructure. Latin America and the Middle East & Africa (MEA) are emerging as significant growth areas, particularly due to the exploration of major copper, iron ore, and precious metal reserves, necessitating advanced planning tools to manage complex resource geometry and challenging operational logistics effectively.

Segment trends reveal that the Cloud-Based deployment model is gaining significant traction due to its flexibility, scalability, and lower total cost of ownership, particularly for exploration and project-specific planning applications. Among application segments, Planning & Scheduling remains the largest segment by revenue, as optimized production schedules directly translate into operational profitability. Furthermore, the Services component segment, encompassing implementation, training, and consulting services, is witnessing accelerated growth as miners require specialized expertise to fully integrate sophisticated planning software with existing Enterprise Resource Planning (ERP) systems and operational technology (OT) infrastructure, ensuring optimized workflow customization and maximum utility realization.

User queries regarding AI's impact frequently center on how machine learning (ML) can enhance the accuracy of ore body modeling, automate mundane tasks currently performed by geologists, and optimize dynamic mine scheduling in response to real-time data fluctuations. Users are deeply concerned with the reliability and explainability of AI-driven resource estimation, often questioning whether these systems can truly handle the high variability and uncertainty inherent in geological data (e.g., "Will AI replace experienced geologists?", "How reliable are ML models for grade control?"). Expectations are high regarding AI’s potential to unlock value in low-grade or marginal deposits by predicting geotechnical instabilities and optimizing the blending of materials to meet strict processing plant specifications, thereby maximizing recovery rates and minimizing processing costs associated with material variability.

The integration of Artificial Intelligence, specifically deep learning and predictive analytics, is rapidly transforming the capabilities of Geology and Mine Planning Software. AI models are being trained on vast historical datasets, incorporating drill hole logs, geophysical surveys, and production metrics, allowing for the generation of significantly more accurate, probabilistic geological models compared to traditional geostatistical methods. This level of predictive accuracy enables engineers to make more informed decisions regarding capital allocation, drilling density, and processing pathway selection, fundamentally shifting the paradigm from static planning to dynamic, data-driven optimization. AI is also critical in identifying subtle patterns in data that indicate structural weaknesses or potential hazards, enhancing mine safety protocols.

Furthermore, AI algorithms are instrumental in automating highly iterative and complex planning tasks, such as optimizing ultimate pit limits and designing sophisticated underground stope layouts under multiple constraints (economic, geotechnical, operational). By rapidly testing millions of scenarios, AI can identify globally optimal solutions that manual planning processes cannot achieve within realistic timeframes. This capability extends to real-time production optimization, where ML models ingest data from mobile equipment and processing plants to suggest immediate adjustments to haul routes, blast timing, and material flow, ensuring maximum throughput and energy efficiency, thus providing a significant competitive advantage to early adopters in the mining sector.

The market dynamics are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape the competitive landscape and technological investment cycles. Key drivers include the mandatory requirement for operational efficiency improvement globally, driven by rising operational costs and decreasing ore grades, forcing reliance on precision planning software. Opportunities are abundant, especially concerning the integration of advanced technologies like AI, virtual reality (VR), and digital twins for real-time operational simulation and remote management. However, the market faces significant restraints, primarily high initial investment costs for licensing and implementation, coupled with the acute shortage of skilled personnel capable of effectively utilizing and integrating these highly specialized software solutions across disparate mining departments.

The primary impact forces propelling market growth stem from the global commodity super cycle and the push toward sustainable mining practices. The global demand for electrification minerals (copper, nickel, lithium) creates intense pressure on miners to accelerate exploration and extraction while maintaining social license to operate. This necessitates advanced software capable of detailed environmental impact assessment and waste management planning (including tailings). Conversely, a major restraining impact force is the inertia within traditional mining organizations, which often resist major digital transformation projects due to legacy system dependency and concerns over data security and interoperability between different vendor platforms, slowing down the pace of enterprise-wide adoption.

Furthermore, regulatory impact forces are crucial; stringent government regulations regarding resource reporting (e.g., JORC, NI 43-101 standards) mandate the use of auditable and technically sound modeling software, effectively driving market demand for certified solutions. The opportunities presented by the transition to cloud-native platforms are mitigating some of the cost restraints, enabling smaller exploration firms access to sophisticated tools previously restricted to large corporations. The collective force of technological innovation meeting market necessity ensures a positive long-term growth trajectory, provided vendors can successfully address the implementation complexity and the skills gap challenges inherent in this specialized software domain.

The Geology and Mine Planning Software Market is highly diversified, segmented across various dimensions including Component, Deployment, Application, and Mining Type, allowing vendors to tailor solutions precisely to the specific operational and budgetary needs of different mining entities. Understanding these segments is vital for assessing market penetration and growth avenues. The segmentation reflects the evolutionary complexity of modern mining, which demands specialized tools for everything from initial greenfield exploration to highly sophisticated underground production scheduling and operational reporting. The primary value proposition varies significantly between segments; for instance, the application segment focuses on functional efficiency while the deployment segment addresses IT infrastructure strategy and scalability.

The differentiation between Component segments (Software vs. Services) highlights the trend that while core software features are essential, the professional services required for successful customization, integration with existing infrastructure (e.g., ERP, SCADA systems), and continuous user training represent a substantial and growing portion of market expenditure. Similarly, the clear division between On-Premise and Cloud-Based deployment models underscores the industry's gradual but accelerating move towards flexible, OpEx-friendly cloud architectures, particularly among mid-tier and junior miners seeking lower upfront investment and faster scalability, ensuring broad accessibility to advanced modeling capabilities across the industry spectrum.

Analysis of the Application segment reveals that while Exploration initially drives software adoption, the recurring and highest value is generated within the Planning & Scheduling segment, as these tools are intrinsically linked to daily operational output and profitability metrics. The granularity within the Mining Type segment demonstrates that software features must be highly customized; for example, solutions for complex underground metal mining require sophisticated geotechnical stability modeling tools that differ significantly from those used for large-scale, low-complexity surface coal mining, necessitating specialized product offerings that cater specifically to the geological and regulatory environments of each commodity sector.

The value chain for the Geology and Mine Planning Software Market initiates with upstream activities focused on core R&D and proprietary algorithm development, where specialized vendors invest heavily in computational geometry, geostatistics, and predictive analytics capabilities. This upstream segment is characterized by high intellectual property barriers and a reliance on domain expertise from geology, engineering, and computer science fields. Key activities include software coding, database architecture design, and creating user interface/experience (UI/UX) tailored for complex 3D visualization, setting the foundation for the product’s capabilities and future scalability in integrating advanced features like machine learning and real-time data ingestion protocols from various sensor networks and IoT devices deployed within the operational environment.

The midstream process involves the packaging, distribution, and licensing of the software. Distribution channels are bifurcated into direct sales models, often utilized for large, custom enterprise contracts with Tier 1 mining companies, and indirect channels relying on certified resellers, regional distributors, and strategic system integrators, especially in emerging markets or for smaller customers seeking localized support and implementation expertise. The services component—including customization, integration, and training—adds substantial value at this stage, ensuring the successful deployment and maximized utilization of the sophisticated software suite within the client's complex IT and operational technology (OT) environment, which is often crucial for client retention and high lifetime value realization.

Downstream activities involve the end-users—mining companies, geological consultants, and governmental regulatory bodies—who utilize the software for operational tasks, planning, and compliance. The flow of value is completed when the software drives measurable improvements in resource utilization, safety outcomes, and cost efficiency. Direct channels offer immediate feedback loops, allowing vendors to rapidly iterate on product features based on client operational challenges, whereas indirect channels allow for broader geographic reach and local market penetration. The continuous update cycle and provision of managed services and technical support constitute essential post-deployment activities that sustain the value proposition and secure long-term revenue streams for the software provider within this highly specialized industrial domain.

The primary end-users and potential buyers of Geology and Mine Planning Software are global mining operators, ranging from multinational corporations (Tier 1 miners) with diversified portfolios of assets worldwide to mid-tier and junior exploration companies. Tier 1 miners, such as BHP Group, Rio Tinto, and Barrick Gold, represent the largest customers due to their extensive capital budgets, demand for integrated enterprise-wide solutions, and complex operational requirements spanning multiple commodities and geographical regions. These large entities typically require customized, on-premise solutions or private cloud deployments that integrate seamlessly with their proprietary data lakes and existing ERP infrastructure, often engaging in multi-year, multi-million-dollar licensing and services agreements with top-tier software vendors in the specialized mining technology domain.

Mid-tier and junior exploration companies also constitute a significant and growing customer base. While these organizations operate with tighter budgets, they are increasingly reliant on high-quality geological modeling to secure funding and justify reserves to investors, making scalable, cost-effective cloud-based solutions highly attractive. Geological consulting firms, engineering houses, and resource estimation specialists represent another crucial customer segment. These firms utilize the software to provide specialized services to miners, often requiring multiple licenses and advanced features to handle heterogeneous data from various clients efficiently and ensure compliance with stringent international resource reporting codes like JORC or NI 43-101 standards, enhancing their service offering competitiveness.

Furthermore, academic institutions and governmental regulatory agencies also function as important, albeit secondary, customer groups. Universities use this software for teaching mining engineering and geology programs, ensuring the next generation of professionals is trained on industry-standard tools, while governmental bodies, particularly those responsible for mineral licensing and environmental oversight, use planning software to verify resource declarations, optimize land use planning, and monitor environmental compliance related to mining operations. Their demand focuses on analytical rigor and regulatory compliance capabilities, ensuring the software adheres to the highest levels of scientific and legal scrutiny within resource management contexts.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $550 Million USD |

| Market Forecast in 2033 | $1.1 Billion USD |

| Growth Rate | CAGR 10.1% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Dassault Systèmes (GEOVIA), Hexagon AB (MinePlan, BlastMetrix), Bentley Systems, RPMGlobal, MICROMINE, Seequent (A Bentley Company), Datamine International, Maptek, Promine Inc., GEMS, Snowden Group, Mincom (ABB), Mineware, Gemcom (now part of Dassault Systèmes), RockWare, Inc., Tetra Tech, Deswik, Rithm. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Geology and Mine Planning Software market is defined by several core technological pillars essential for modern mining operations. At the foundational level, advanced Geostatistics (such as Kriging and conditional simulation) forms the backbone of resource estimation, ensuring high levels of confidence and auditability in reserve declaration. This is increasingly complemented by sophisticated 3D visualization and modeling engines capable of handling massive datasets generated by drilling, scanning, and geophysical surveys, allowing geologists to interact intuitively with complex geological structures and rapidly assess various extraction scenarios. Furthermore, the integration of Computational Geometry algorithms is critical for optimizing pit slopes, designing stable underground infrastructure, and ensuring the accurate calculation of volumes and material movements across the mine site.

The emerging technological focus centers heavily on cloud computing and Software as a Service (SaaS) architecture, facilitating remote access, collaborative planning across geographically dispersed teams, and efficient scalability without heavy localized IT investment. This deployment model is intrinsically linked with the adoption of Digital Twin technology, where highly accurate virtual representations of the mine site are continuously updated with real-time data from IoT sensors, drones, and fleet management systems. These digital twins enable engineers to run high-fidelity simulations for safety analysis, infrastructure stress testing, and optimized production scheduling, moving planning capabilities beyond static models toward dynamic, predictive operations management, significantly reducing operational variability and unexpected downtime caused by unforeseen geotechnical or operational failures.

Moreover, the incorporation of advanced Machine Learning (ML) techniques is transforming specific workflows, particularly in grade control, geotechnical hazard prediction, and automatic classification of geological domains based on drill core imagery and sensor data. The market is also seeing greater integration of geospatial information systems (GIS) with planning software, providing a powerful platform for environmental monitoring, land management, and regulatory compliance reporting. The convergence of these technologies—Cloud, AI, Digital Twins, and sophisticated Geostatistics—is driving a new generation of integrated platforms that offer end-to-end digital solutions for mine operators, maximizing resource recovery while adhering to stringent global sustainability mandates and ensuring long-term operational viability across challenging mining environments.

Regional analysis is crucial for understanding the diverse growth drivers and investment patterns across the global Geology and Mine Planning Software Market, reflecting differences in commodity emphasis, regulatory stringency, and technological maturity.

North America

North America is a mature but highly influential market segment, characterized by the presence of major global software vendors and a high rate of early technology adoption, driven primarily by large-scale precious metals (gold) and base metals (copper) mining operations, alongside increasing activity in critical minerals extraction. The regional market demands highly specialized software for regulatory compliance (e.g., NI 43-101 reporting), rigorous geotechnical stability analysis, and advanced integration with autonomous mining equipment. The focus here is on maximizing operational efficiency in deep underground mines and utilizing software to manage complex, multi-jurisdictional assets, leading to a strong demand for integrated, enterprise-level solutions and professional consulting services for specialized implementations. Furthermore, the region's robust technology infrastructure facilitates the deployment of cutting-edge AI and cloud-based systems, positioning it as a key innovation hub for the global mining software industry.

Europe

The European market, though perhaps smaller in raw operational size compared to APAC or North America, is pivotal due to its strong emphasis on environmental stewardship, high safety standards, and technological innovation, particularly stemming from Nordic countries (Sweden, Finland). Demand is primarily driven by iron ore, base metal mining, and quarrying operations, coupled with intensive research into sustainable mining practices. European companies are leading adopters of advanced visualization tools, digital twin technology for real-time asset management, and software facilitating complex blast optimization to minimize ground vibration and environmental impact. Strict EU directives on worker safety and environmental governance necessitate the use of comprehensive planning software that provides detailed traceability and minimizes operational risks, pushing the market toward specialized, high-compliance software tools.

Asia Pacific (APAC)

APAC represents the fastest-growing market globally, fueled by massive resource development in countries like Australia, China, Indonesia, and India, which are major producers of coal, iron ore, gold, and bauxite. This region’s growth is characterized by large-scale modernization projects and significant expansion of new mining facilities, requiring scalable and standardized planning software for large open-pit and bulk mining operations. While cost sensitivity remains a factor, the imperative to meet massive domestic and export demands drives the adoption of sophisticated scheduling and fleet management software to optimize throughput. Australia, in particular, acts as a technological pioneer, quickly adopting cloud and automation technologies, setting the benchmark for operational efficiency within the region and driving investment in highly integrated enterprise solutions for asset management.

Latin America

Latin America is a critical market due to its immense reserves of copper (Chile, Peru), iron ore (Brazil), and gold. The demand for mining software here is strongly correlated with fluctuations in global commodity prices, but the underlying trend is toward mandatory digitalization to improve recovery rates in increasingly complex and deep deposits. Geological complexity, coupled with challenging terrain and logistical issues, requires highly robust 3D modeling and geotechnical analysis capabilities. The market is witnessing increasing investment in optimization software to tackle grade variability and ensure efficient material handling, supported by government initiatives promoting foreign investment in resource exploration and modernization efforts across the continent’s key mining jurisdictions.

Middle East and Africa (MEA)

The MEA region is poised for significant growth, particularly driven by large-scale, undeveloped mineral reserves, including gold, phosphates, and strategic minerals, attracting substantial international investment, particularly in South Africa, Saudi Arabia, and various West African nations. The market is emerging, characterized by the need for initial exploration software and scalable planning tools for greenfield projects. The primary driver is the necessity for accurate resource delineation to attract foreign capital and manage high sovereign risk environments effectively. Cloud-based platforms are favored due to limited local IT infrastructure, providing cost-effective access to world-class planning capabilities essential for managing complex logistics and ensuring safe, compliant extraction processes in remote, challenging environments.

The Geology and Mine Planning Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.1% between 2026 and 2033, driven by digitalization imperatives and rising global demand for critical minerals, necessitating efficient resource extraction methodologies and advanced operational optimization tools.

AI influences resource estimation by employing machine learning algorithms to analyze complex, multi-variable geological data, enhancing the accuracy of ore body models, improving grade control prediction, and providing probabilistic risk assessment far superior to traditional geostatistical methods, thereby optimizing long-term mine profitability.

The Cloud-Based deployment model is exhibiting the fastest adoption rate, particularly among mid-tier and junior miners. This trend is due to the lower upfront capital expenditure, inherent scalability, rapid deployment capabilities, and facilitation of remote, collaborative planning crucial for managing global or highly dispersed exploration and operational assets.

Primary restraints include the high initial cost of licensing and implementation of specialized software, significant complexities involved in integrating these tools with existing legacy operational technology (OT) systems, and a persistent shortage of skilled mining engineers and geologists proficient in using advanced computational planning platforms effectively.

The Planning & Scheduling application segment consistently holds the largest share of market revenue. This is because effective production scheduling, including short-term and long-term optimization of extraction sequences and material movement, directly correlates with maximizing operational throughput and ensuring profitability across the entire mining life cycle.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.