ID : MRU_ 433715 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

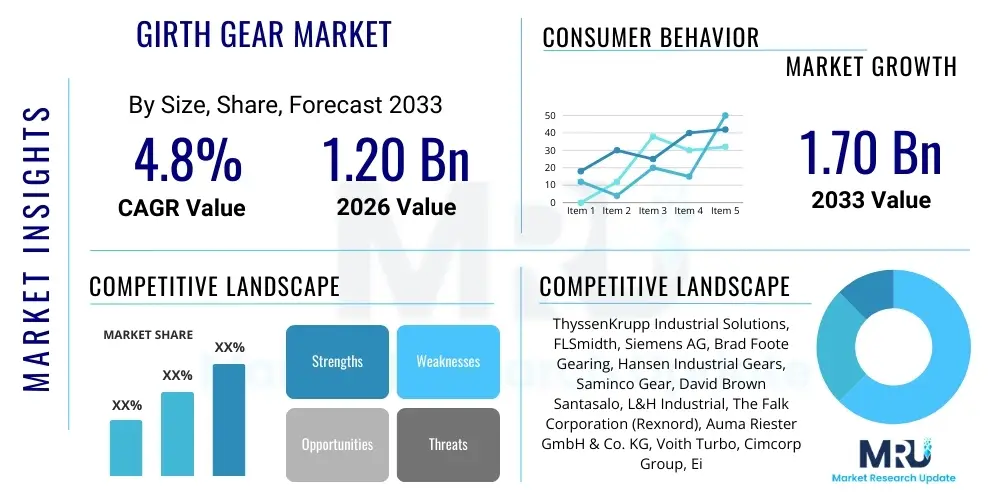

The Girth Gear Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 1.20 Billion in 2026 and is projected to reach USD 1.70 Billion by the end of the forecast period in 2033.

Girth gears are among the most critical components in heavy rotating machinery, serving as the primary mechanism for torque transmission in large-scale applications such as rotary kilns, ball mills, scrubbers, and dryers. These gears are characterized by their large diameter, robust design, and ability to operate reliably under extreme conditions, including high loads, abrasive environments, and continuous duty cycles. The design and manufacturing process of girth gears require specialized expertise, often involving sophisticated casting, forging, and machining techniques to ensure precision tooth geometry and metallurgical integrity, which is paramount for minimizing operational downtime and maximizing equipment lifespan. Their primary function is to enable the low-speed, high-torque rotation necessary for processing bulk materials in energy-intensive industries.

The market expansion is intrinsically linked to global industrialization trends, particularly in sectors requiring high-capacity comminution and thermal processing equipment. Key applications span cement manufacturing, mineral processing (mining and metallurgy), power generation, and chemical industries. The increasing global demand for essential materials like cement, copper, lithium, and other processed minerals necessitates continuous investment in new grinding and processing plants, which directly drives the demand for high-quality, durable girth gears. Furthermore, the operational longevity and efficiency gains offered by modern girth gear designs, including those utilizing specialized lubrication and monitoring systems, make them indispensable assets in plant capital expenditure planning.

Driving factors for sustained market growth include stringent regulatory standards emphasizing equipment reliability and safety, which encourages end-users to upgrade or replace aging gear systems with superior alternatives. The benefits derived from investing in advanced girth gears include significantly reduced maintenance costs, improved energy efficiency in grinding operations, and enhanced overall plant productivity. The inherent durability and custom engineering capabilities associated with premium girth gears mitigate the risk of catastrophic failure, securing operational continuity in highly capital-intensive industrial settings where downtime is exorbitantly expensive. The continual development of material science, particularly in specialized alloy steels, further enhances the performance parameters of these essential components.

The Girth Gear Market is characterized by robust demand driven primarily by infrastructure spending in emerging economies and the global push towards mineral processing necessitated by the energy transition. Current business trends indicate a shift towards modular and segmented girth gear designs, which facilitate easier transportation, installation, and replacement, thereby reducing logistical burdens and overall plant commissioning time. Consolidation within the supply chain, particularly among specialized foundries and heavy machinery manufacturers, is shaping competitive dynamics, emphasizing quality control and adherence to international standards like AGMA and ISO. Technology adoption focuses on advanced surface treatments, such as carburizing and nitriding, to enhance wear resistance and load-bearing capacity, addressing the industry's critical need for maximum operational uptime.

Regionally, the Asia Pacific (APAC) market dominates the consumption landscape, anchored by massive investments in cement and metal production facilities, particularly in China and India. The rapid pace of urbanization and related construction activity ensures sustained high demand for large-scale processing equipment. Conversely, North America and Europe demonstrate a mature market structure, with growth primarily fueled by maintenance, repair, and overhaul (MRO) activities, alongside the selective replacement of older, less efficient units to comply with modern efficiency benchmarks. Latin America and the Middle East and Africa (MEA) present significant opportunities, spurred by burgeoning mining projects (e.g., copper and gold extraction) and large-scale infrastructure projects financed through government initiatives and international development funds.

Segmentation analysis highlights the dominance of the Segmented Girth Gear type due to the logistical and maintenance advantages it offers over traditional one-piece gears, especially for applications exceeding 10 meters in diameter. By application, the mining and mineral processing sector remains the largest consumer, reflecting the high number of grinding mills required globally. Material-wise, high-strength alloy steels remain the material of choice, though specialized foundries are increasingly exploring composite materials for niche applications requiring reduced weight or enhanced corrosion resistance. The trend across all segments points towards predictive maintenance integration, requiring gears to be designed with features that allow seamless integration with digital monitoring systems.

User inquiries regarding the influence of Artificial Intelligence (AI) on the Girth Gear Market predominantly center on how AI can enhance operational efficiency, prevent catastrophic failures, and optimize manufacturing processes. Common questions revolve around the feasibility of AI-driven predictive maintenance for massive gears, the use of machine learning in optimizing tooth geometry during design, and the role of computer vision in quality inspection. The core theme is the expectation that AI and associated digital twins will transition girth gear management from reactive maintenance, based on periodic inspections, to proactive, condition-based maintenance, maximizing the component’s operational lifespan and reducing unscheduled downtime—a critical concern given the high replacement cost and long lead times associated with these components.

The immediate impact of AI is most visible in the integration of advanced sensor technology (vibration analysis, acoustic emission, thermal imaging) coupled with machine learning algorithms. These systems constantly monitor the health of the girth gear drive system, detecting minute anomalies indicative of wear, fatigue, or lubrication issues long before they become critical. AI models analyze complex multivariate datasets, providing actionable insights into optimal re-lubrication schedules, alignment adjustments, and projected remaining useful life (RUL). This shift away from fixed maintenance schedules dramatically improves operational resilience in cement and mining plants where continuous operation is essential.

Looking forward, AI is set to revolutionize the entire lifecycle, from design to end-of-life management. Generative design principles, powered by AI, can explore millions of potential tooth profile geometries, optimizing for specific load cases, reducing stress concentrations, and minimizing material usage while maintaining structural integrity. Furthermore, AI-enhanced robotics and automated inspection systems are streamlining manufacturing quality control, ensuring that casting integrity and machining tolerances meet the extremely tight specifications required for high-load applications. This digital integration elevates the standard of reliability in highly demanding industrial environments.

The Girth Gear Market dynamics are shaped by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), subjected to significant external Impact Forces. The primary drivers are the consistent growth in global mining output, necessitated by the demand for raw materials required for the energy transition (e.g., lithium, cobalt, copper), and sustained urbanization trends demanding large volumes of cement and other construction materials. These factors necessitate continuous capital expenditure on new grinding mills and rotary kilns, where girth gears are essential, high-value components. Additionally, the replacement cycle for existing heavy machinery, often after 15-20 years of continuous service, provides a steady base demand, especially in mature industrial regions focused on modernizing outdated infrastructure to improve efficiency and reduce environmental impact.

However, the market faces significant restraints. The manufacturing process for large girth gears is inherently complex, time-consuming, and capital-intensive, leading to high production costs and long lead times—often extending up to 12-18 months—which can delay project commissioning. Furthermore, the specialized metallurgical expertise and precision machining capabilities required limit the number of qualified suppliers, leading to concentrated supply risks and high barriers to entry. Economic volatility, particularly fluctuating commodity prices, can lead to the temporary deferral or cancellation of large-scale mining and cement plant projects, directly impacting new equipment procurement volumes and introducing uncertainty into revenue forecasts for gear manufacturers.

Opportunities for growth are centered on technological advancements and geographic expansion. The development of advanced materials, such as specialized high-alloy steels with enhanced fatigue resistance, allows manufacturers to offer products with superior performance warranties. Moreover, the increasing demand for customized solutions tailored to highly specific operating conditions (e.g., extreme temperatures or corrosive environments) presents opportunities for specialized engineering firms. Geographically, untapped potential lies within developing African and Southeast Asian markets, where industrialization is accelerating, necessitating the construction of local processing plants. Key impact forces include stringent environmental regulations forcing end-users to adopt more energy-efficient grinding solutions, thus favoring newer, highly optimized girth gear designs, and the pervasive global supply chain disruptions that necessitate localized manufacturing or robust inventory management strategies.

The Girth Gear Market segmentation provides a granular view of demand drivers across various product types, applications, and manufacturing methods, allowing manufacturers and suppliers to strategically focus resources. The market is primarily bifurcated based on the physical design—Segmented or Split Girth Gears versus One-Piece or Solid Girth Gears—a distinction crucial for logistical planning, installation complexity, and maintenance accessibility, particularly for extremely large diameters. Segmented gears dominate new installations due to their ease of transportation and reduced installation time on-site. Further segmentation by application clearly illustrates the market's dependence on the cement and mining sectors, which utilize the heaviest and most critical gear systems for comminution processes.

Beyond design and application, segmentation based on the manufacturing process—specifically casting versus fabrication (for specialized large units)—and the heat treatment applied (induction hardening, case hardening) highlights the variations in quality and performance characteristics demanded by different end-users. High-load, critical applications often necessitate gears made from specialized alloy steels and subjected to precise surface hardening treatments to achieve maximum operational lifespan and resistance to pitting and wear. Understanding these detailed segment preferences is vital for market positioning and for aligning production capabilities with specific industrial requirements, ensuring compliance with diverse load specifications and operating environments.

The Girth Gear market value chain is extensive and begins with highly specialized upstream activities centered around the procurement and processing of raw materials. This initial stage involves sourcing high-pgrade specialty steel alloys, notably high-strength carbon and chrome-molybdenum steels, which must meet stringent metallurgical specifications crucial for the gear's performance under extreme stress. Key upstream activities include specialized electric arc furnace steel production, meticulous alloying, and initial large-scale forging or casting preparation. The cost and quality of these raw materials significantly influence the final product price and performance envelope, making long-term procurement agreements with reputable steel suppliers a critical element of competitiveness for gear manufacturers.

The midstream phase—manufacturing and processing—is the most value-intensive stage. It encompasses highly specialized processes, including large-scale sand casting or forging, followed by essential heat treatment processes (normalization, quenching, tempering, and surface hardening like carburizing or induction hardening) to achieve the required hardness and mechanical properties. Crucially, the final step involves ultra-precision machining on large-capacity CNC gear hobbing and grinding machines to achieve the exact tooth profile and alignment tolerances (often measured in microns) necessary for smooth, high-load operation. Quality assurance protocols, including non-destructive testing (NDT) such as ultrasonic and magnetic particle inspection, are embedded throughout this stage to detect any internal flaws, ensuring product reliability before distribution.

Downstream activities involve logistics, distribution, and critical post-sale support. Due to the massive size and weight of girth gears, specialized logistics are mandatory, often requiring heavy-lift transport and specialized escorts. Distribution channels are predominantly direct, involving Original Equipment Manufacturers (OEMs) who integrate the gears into their mills or kilns, and aftermarket specialized service providers who handle replacement and MRO contracts directly with end-users like mining or cement companies. The aftermarket service component, including installation, alignment checks, and predictive maintenance contracts, often represents a significant and stable revenue stream, emphasizing the long-term relationship between the manufacturer and the operational site.

Potential customers for girth gears are predominantly heavy industrial entities operating machinery that requires large-scale, low-speed, high-torque rotational power transmission. The primary end-users are concentrated within the global mining and mineral processing industry, where girth gears are integral components of Sag (Semi-Autogenous Grinding), Ball, and Rod Mills used for comminution—the essential crushing and grinding of raw ores (e.g., iron, copper, gold, platinum). These customers require gears capable of handling continuous, cyclical loading in abrasive and often remote operational environments, prioritizing durability, minimal wear rate, and exceptional reliability to prevent costly halts in processing operations.

The second major cohort of buyers resides in the cement and lime industry, where girth gears drive large rotary kilns and associated grinding mills crucial for clinker production. Cement manufacturers demand gears that can withstand high thermal stresses and continuous operation under demanding conditions, often operating 24/7. Their purchasing decisions are heavily influenced by Total Cost of Ownership (TCO), focusing on gears that offer the longest service life with minimal maintenance intervention, translating directly into higher plant throughput and efficiency. Investment cycles in this sector are tied directly to global housing, infrastructure, and construction demand forecasts, making them highly strategic buyers.

Additional significant customers include large engineering, procurement, and construction (EPC) firms responsible for setting up entirely new industrial plants. These firms procure gears as part of a larger contract for integrating complete heavy machinery packages. Furthermore, specialized companies involved in large-scale chemical processing, power generation (e.g., coal pulverizers), and specialized industrial drying also represent important, albeit smaller, segments of the market. Across all potential customers, the critical purchasing criteria are technical adherence to API/AGMA standards, proven track record of the supplier, and comprehensive aftermarket service packages, validating the premium nature and mission-critical role of the girth gear component.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.20 Billion |

| Market Forecast in 2033 | USD 1.70 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ThyssenKrupp Industrial Solutions, FLSmidth, Siemens AG, Brad Foote Gearing, Hansen Industrial Gears, Saminco Gear, David Brown Santasalo, L&H Industrial, The Falk Corporation (Rexnord), Auma Riester GmbH & Co. KG, Voith Turbo, Cimcorp Group, Eickhoff Group, Sumitomo Heavy Industries, Renold plc, Jiangsu Nanfang Gear Group, Philadelphia Gear, SEW-EURODRIVE, Bonfiglioli, and Hangzhou Advance Gearbox Group Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Girth Gear Market technology landscape is characterized by continuous advancements aimed at improving gear durability, load-bearing capacity, and precision. A primary focus is on metallurgical innovation, specifically the development and application of specialized, high-nickel, and chrome-molybdenum alloy steels that offer superior fracture toughness and wear resistance compared to standard cast steel. Crucially, surface engineering technologies, such as deep case carburizing and high-frequency induction hardening, are standard practices. These treatments create a hard, wear-resistant surface layer while maintaining a softer, tough core, drastically extending the service life of the gear in demanding, high-impact environments characteristic of mineral processing.

Precision manufacturing technologies form the backbone of modern girth gear production. The use of large-scale, high-precision CNC gear cutting machines (hobbing and shaping) is essential to achieve the tight tolerances required for smooth power transmission and reduced noise levels. A critical aspect is quality control utilizing advanced metrology systems, including laser scanning and Coordinate Measuring Machines (CMMs), to verify tooth geometry, pitch accuracy, and alignment across the massive diameter of the gear. Innovations in manufacturing also include modular construction techniques for segmented gears, which minimize thermal stress during the casting process and streamline field assembly, directly addressing transportation and installation challenges.

Furthermore, digital technologies are rapidly integrating into the Girth Gear ecosystem. The implementation of IoT sensors for continuous condition monitoring—tracking parameters like vibration, temperature, and torsional load—is becoming standard practice, enabling the transition towards predictive maintenance models. Software tools for Finite Element Analysis (FEA) and computational fluid dynamics (CFD) are routinely used during the design phase to simulate operational stresses, optimize lubrication pathways, and minimize stress concentration points, ensuring that the gear is optimally engineered for its specific application load profile before physical production commences, thereby drastically reducing development risks and ensuring optimal performance.

The global distribution of Girth Gear demand reflects the concentration of heavy industry and resource extraction activities worldwide. Each region presents unique market dynamics based on infrastructure maturity, regulatory environment, and commodity exposure. Strategic market entry and expansion depend heavily on understanding these regional variances in capital expenditure patterns and MRO requirements.

The demand is primarily driven by the increasing global requirement for mined commodities, specifically copper, gold, and specialized battery metals. This necessitates continuous investment in high-capacity comminution equipment, such as SAG and Ball Mills, which rely fundamentally on large, durable girth gears for efficient operation.

Segmented girth gears offer significant logistical advantages, enabling easier transportation to remote industrial sites and facilitating quicker, less invasive installation and replacement. This design minimizes operational downtime and reduces the risks associated with handling extremely large, heavy components during maintenance procedures, lowering the Total Cost of Ownership (TCO).

Predictive maintenance systems, utilizing integrated IoT sensors and AI analytics, continuously monitor operational parameters like vibration and temperature. By detecting minute variations indicative of early wear or misalignment, these systems enable proactive intervention (e.g., re-lubrication, minor adjustments), preventing catastrophic failure and potentially extending the gear's lifespan significantly beyond traditional scheduled maintenance cycles.

The Asia Pacific (APAC) region currently holds the largest market share, predominantly driven by extensive capital expenditure in infrastructure and commodity processing, particularly in the cement and mining industries of China and India. The high volume of new plant commissioning projects in this region sustains robust demand for girth gear systems.

The primary technical challenges include maintaining metallurgical integrity and internal consistency during the casting and forging of massive steel sections, achieving micron-level precision during the final gear cutting (hobbing and grinding) across extremely large diameters, and ensuring uniform, deep surface hardening treatments to handle immense operational loads without premature wear or pitting failure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.