ID : MRU_ 433601 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

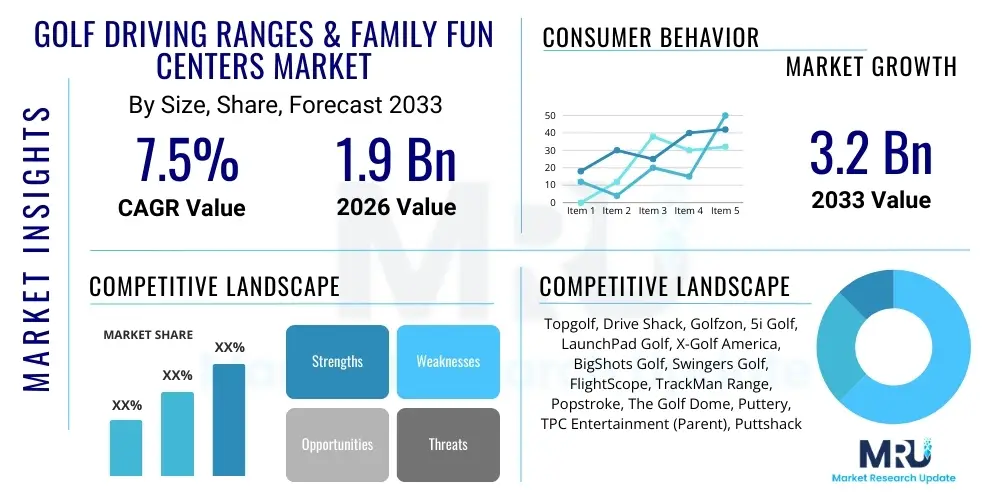

The Golf Driving Ranges & Family Fun Centers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 1.9 Billion in 2026 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2033. This substantial growth is fundamentally driven by the increasing consumer demand for experiential entertainment options that merge sports, technology, and social dining. Traditional golf participation rates, while stable, are being augmented significantly by off-course golf activities, which appeal to a broader demographic, including younger generations and non-golfers seeking casual, competitive leisure.

The expansion of the market is heavily influenced by the proliferation of technology-driven golf entertainment concepts, such as automated ball dispensing, sophisticated ball-tracking technologies (like radar and infrared systems), and integrated high-end food and beverage (F&B) services. These modern centers have successfully repositioned the traditional driving range from a practice facility into a comprehensive entertainment venue, thereby increasing average customer spend and visit frequency. Market valuation in 2026 reflects the post-pandemic recovery and the initial surge in development projects focused on these hybrid entertainment models across key metropolitan areas globally.

Moreover, the market size forecast of USD 3.2 Billion by 2033 underscores the strong investor confidence in the scalability and profitability of location-based entertainment (LBE) centered around golf. Key geographical regions, particularly North America and parts of Asia Pacific, are seeing rapid development and saturation of these technologically advanced centers. This anticipated financial trajectory requires continuous innovation in facility design, personalized user experiences, and strategic partnerships with corporate event planners and major F&B suppliers to sustain high revenue yields throughout the forecast period.

The Golf Driving Ranges & Family Fun Centers Market encompasses establishments that provide recreational golf practice facilities, often integrated with additional entertainment activities, dining options, and interactive technologies designed to appeal to a wide array of consumers, from serious golfers to families and corporate groups. The product description spans traditional grass driving ranges, automated bay systems, mini-golf courses, batting cages, and sophisticated, multi-story entertainment venues featuring proprietary ball-tracking systems and competitive gaming formats. Major applications include casual recreation, professional practice, corporate team building, and social gatherings, making these centers highly versatile leisure destinations.

The primary benefits delivered by these centers include providing accessible, non-intimidating avenues for introducing golf to new players, offering weather-independent entertainment options, and successfully leveraging premium F&B offerings to maximize revenue per guest. Furthermore, modern centers enhance the traditional golf experience by incorporating instant feedback on swing metrics and gamification elements, drastically increasing engagement and perceived value. The driving factors behind market expansion include increased urbanization leading to higher demand for local, accessible entertainment; the consumer trend towards spending on experiences over physical goods; and technological advancements that lower operational costs while improving customer experience.

In the current market landscape, differentiation is achieved through superior technology integration and the quality of the hospitality experience. Companies are continually investing in virtual reality (VR) golf simulators, improved automated hitting bays, and sophisticated scheduling and reservation systems to streamline operations. The integration of family fun center elements, such as arcades and bowling, further diversifies the revenue streams, insulating the market from fluctuations in pure golf participation. This diversification and emphasis on 'eatertainment' have cemented the market’s position as a dynamic and robust sector within the broader leisure industry, capturing significant consumer mindshare and disposable income globally.

The Golf Driving Ranges & Family Fun Centers Market is characterized by a significant shift from traditional practice facilities toward technology-enabled "eatertainment" hubs, driving rapid expansion globally. Key business trends include the increasing adoption of proprietary tracking technologies (e.g., radar, optical systems) to create competitive, social gaming experiences, exemplified by market leaders who focus heavily on high-quality food and beverage offerings to constitute a substantial portion of total revenue. Strategic partnerships with real estate developers and retail outlets are also vital for securing prime, high-traffic locations, optimizing accessibility and visibility, which is crucial for maximizing footfall and average revenue per square foot across urban and suburban environments.

Regionally, North America remains the dominant market due to high consumer spending on leisure and the early establishment of large-scale entertainment golf brands. However, the Asia Pacific (APAC) region, particularly emerging economies with growing middle-class populations and a rapid increase in recreational spending, is projected to exhibit the highest growth rates, driven by urbanization and a strong cultural affinity for tech-integrated leisure activities. Europe is also seeing steady expansion, albeit often constrained by space and regulatory complexity, resulting in a stronger penetration of indoor simulator centers alongside the hybrid outdoor ranges prevalent in the US.

Segment trends highlight the premiumization of the experience, with the "Modern Entertainment Center" segment significantly outpacing growth in the "Traditional Driving Range" segment. Revenue generation is increasingly skewed toward Food & Beverage and Event Hosting, confirming the market’s transformation into a hospitality-focused sector that utilizes golf as its core anchor activity. Furthermore, the Target Audience segmentation shows strong growth in the Family and Corporate Group demographics, necessitating highly flexible pricing models and diverse activity offerings to cater to both individual practice needs and large-group celebratory functions, ensuring optimal utilization across all operating hours.

User queries regarding AI’s impact on the Golf Driving Ranges & Family Fun Centers Market frequently center on automation, personalized coaching, predictive maintenance, and optimizing dynamic pricing strategies. Users are keenly interested in how AI can enhance the core customer experience, particularly through personalized feedback on golf swings and seamless interaction with facility services. Common concerns revolve around the potential for job displacement, especially for range attendants, and the capital expenditure required to integrate complex AI systems. Overall, the expectation is that AI will be a transformative force, enabling hyper-efficient operations and creating highly customized, engaging entertainment formats that retain customer loyalty and increase the average lifetime value of a visitor.

The market dynamics are governed by a robust combination of favorable drivers, manageable restraints, significant opportunities, and influential impact forces. The primary drivers include the escalating global demand for experiential entertainment, the successful de-formalization of golf through technology integration (making it more accessible and fun), and the strong revenue contribution from ancillary services like F&B and event hosting. Restraints typically involve the high initial capital investment required for large-scale, high-tech facilities, substantial real estate costs, especially in urban areas, and regulatory hurdles concerning liquor licenses and large entertainment venues. Opportunities center on geographic expansion into underserved international markets and deepening technological integration, particularly in augmented reality (AR) entertainment and hyper-local marketing campaigns targeting specific community groups.

Impact forces significantly shape competitive positioning. Supplier bargaining power is moderate, influenced by the specialized nature of tracking technology providers (TrackMan, FlightScope) and the standardized nature of F&B procurement. Buyer bargaining power is moderate to high, as consumers have several alternative entertainment options, necessitating continuous quality improvement and pricing innovation. The threat of new entrants, while potentially high for small, niche simulator venues, is low for large-scale, capital-intensive entertainment centers due to the massive initial investment required. Conversely, the threat of substitutes (e.g., specialized bowling alleys, immersive gaming bars, traditional golf courses) is high, requiring centers to consistently offer a superior, integrated entertainment value proposition.

These interacting forces necessitate a strategic focus on technology innovation to maintain differentiation and operational efficiency to manage high fixed costs. The industry must continuously balance the high expense of sophisticated tracking systems with the need to maintain an accessible price point for the mass market. Successfully navigating these DRO & Impact Forces involves aggressive expansion in high-density areas, diversification of activity offerings beyond golf, and leveraging data analytics to optimize every facet of the customer journey, from booking to post-visit marketing, ensuring sustainable, long-term profitability in a highly competitive leisure sector.

The Golf Driving Ranges & Family Fun Centers market is intricately segmented across various dimensions, including the type of facility, the primary source of revenue, the nature of the technology employed, and the target audience demographics. This comprehensive segmentation allows market participants to tailor their offerings, pricing, and marketing strategies to specific consumer needs and market capabilities. The fundamental shift in segmentation reflects the industry’s evolution from pure sports practice (Traditional Ranges) to integrated leisure complexes (Modern Entertainment Centers), which serve distinct customer needs and possess significantly different operational profiles and revenue streams, ultimately driving divergent growth trajectories across the submarkets.

Analysis of the Revenue Source segmentation reveals the critical importance of non-golf income streams. While traditional facilities rely almost entirely on bucket sales, modern centers derive over half of their revenue from Food & Beverage, alcoholic beverages, and high-margin event bookings (corporate events, parties). This revenue diversification acts as a stabilizing factor against seasonal or weather-related fluctuations affecting outdoor facilities. The segmentation by Technology Use further highlights the competitive edge held by facilities utilizing proprietary, high-fidelity launch monitors and gamified software, which are essential for attracting the highly valued Millennial and Gen Z demographics who seek measurable, social, and digitally enhanced experiences across their leisure activities.

The Facility Type segmentation is arguably the most crucial delineation, separating low-capital, low-margin Traditional Ranges from high-capital, high-margin Modern Entertainment Centers. The rapid expansion and strong valuation growth forecasted in this market are overwhelmingly attributable to the latter category. Understanding these segments is vital for investors and operators seeking to identify optimal entry points, determine appropriate investment scales, and benchmark performance against relevant competitive cohorts, ensuring capital allocation aligns with the fastest-growing and most profitable segments within the dynamic leisure industry ecosystem.

The value chain for the Golf Driving Ranges & Family Fun Centers Market begins with upstream activities focused on securing specialized technology and real estate development. Upstream analysis involves crucial relationships with providers of highly specialized golf tracking technology (radar/camera systems), golf ball manufacturers, turf providers, and sophisticated F&B equipment suppliers. These relationships significantly impact operational efficiency and customer experience; dependence on a few key technology vendors can exert pressure on proprietary system pricing, while quality control over raw materials like golf balls and synthetic turf is essential for maintaining accuracy and aesthetic appeal. The design and construction phase, often involving complex vertical structures for multi-level ranges, represents a major component of initial capital expenditure and risk management within this upstream segment.

Midstream activities encompass the core operation of the facility, including facility management, staffing, maintenance, and the integration of the various entertainment components. This stage involves managing key processes such as F&B preparation and service delivery, ensuring the functionality of high-tech hitting bays, implementing safety protocols, and running marketing and promotional campaigns to drive recurring foot traffic. The distribution channel is predominantly direct, as the consumer physically visits the location to consume the service. However, indirect channels play a role through digital platforms: third-party booking systems, corporate event planners (acting as intermediaries for large group sales), and online advertising networks that funnel customers directly to the venue’s point-of-sale systems.

Downstream analysis focuses heavily on the final consumer interaction and relationship management. Direct interaction involves the immediate service quality provided by staff (bay hosts, chefs, bartenders) and the reliability of the technology interface. Customer satisfaction is paramount, influencing repeat visits and word-of-mouth marketing, which are critical for sustainable revenue. Effective downstream success hinges on robust Customer Relationship Management (CRM) systems that analyze spending habits and visitation frequency to implement loyalty programs and targeted communication, ultimately driving higher lifetime customer value and solidifying market presence against competitors in the leisure sector.

Potential customers for the Golf Driving Ranges & Family Fun Centers Market are highly diverse, spanning multiple demographic and socio-economic groups, reflecting the industry's successful pivot towards mass-market entertainment rather than niche sports practice. The primary end-users or buyers fall into four distinct categories: recreational families seeking accessible weekend entertainment, corporate entities utilizing venues for team building and client entertainment, serious individual golfers requiring data-driven practice facilities, and young adults (Millennials and Gen Z) looking for social, high-energy settings that combine sports, gaming, and dining. The common thread among these diverse groups is the demand for a high-quality, memorable experiential outing that justifies the premium pricing often associated with technologically integrated LBE venues.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.9 Billion |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Topgolf, Drive Shack, Golfzon, 5i Golf, LaunchPad Golf, X-Golf America, BigShots Golf, Swingers Golf, FlightScope, TrackMan Range, Popstroke, The Golf Dome, Puttery, TPC Entertainment (Parent), Puttshack |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Golf Driving Ranges & Family Fun Centers Market is rapidly evolving, moving far beyond simple ball dispensing systems to sophisticated data capture and immersive gaming platforms. Key technologies utilized include high-fidelity launch monitors, which are central to the modern entertainment experience. These systems, whether radar-based (like Doppler radar utilized by TrackMan and FlightScope) or optical/camera-based, accurately measure critical ball flight metrics such as launch angle, spin rate, and speed. This precise data not only serves the serious golfer looking to improve but also powers the gamification interfaces, instantly translating physical actions into digital scores and interactive games, which are crucial for attracting casual participants and corporate groups seeking competitive fun.

Beyond ball tracking, the market leverages robust integrated software solutions. Point-of-Sale (POS) systems are interconnected with reservation software and customer relationship management (CRM) platforms, creating a seamless customer journey from booking a bay online to ordering food and beverages directly from the bay screen. Advanced automation is also utilized in ball management—from automated wash and return systems to robotic mowing and maintenance—significantly reducing manual labor costs and enhancing the speed and efficiency of the operation. Furthermore, digital signage, large-screen displays, and integrated audio-visual systems are essential for creating the dynamic, energetic atmosphere expected by consumers of modern location-based entertainment venues.

Future technological trends focus heavily on Augmented Reality (AR) and Virtual Reality (VR). While VR is currently dominant in indoor simulator settings, AR integration is increasingly being explored in outdoor bays to overlay digital targets, obstacles, and leaderboards directly onto the physical range, enhancing the immersive quality without sacrificing the realism of hitting a real ball. Data analytics platforms, often powered by machine learning, are the unseen infrastructure, analyzing customer behavior, optimizing staffing schedules based on predicted demand, and ensuring the dynamic pricing model adjusts effectively throughout the day and week, driving higher occupancy rates and yield management across the entire facility footprint.

The global market for Golf Driving Ranges & Family Fun Centers exhibits significant regional variations in maturity, consumer preference, and growth trajectory. North America, specifically the United States, represents the epicenter of innovation and market size, largely driven by the successful, scalable models pioneered by industry giants. The high disposable income, established culture of competitive sports, and acceptance of large-scale, high-technology LBE venues contribute to its market dominance. Regional expansion within North America often targets high-density urban corridors and major entertainment zones, maximizing exposure and year-round accessibility.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market segment. This growth is fueled by rapid urbanization, increasing middle-class affluence, and a strong technological adoption rate, particularly in countries like South Korea (a leader in indoor golf simulation technology) and China, where golf is gaining recreational popularity. Land scarcity in major APAC cities, however, often necessitates a focus on multi-story indoor simulator complexes rather than sprawling outdoor ranges, leading to intensive technology use and high customer throughput models.

Europe presents a mature but diverse landscape. Western Europe sees steady growth, with a focus on premium experiences and integration within existing leisure infrastructure. Regulatory and spatial constraints often limit the development of massive outdoor venues, encouraging the adoption of sophisticated indoor golf simulators and boutique golf lounges, catering to a clientele seeking high-end F&B paired with golf practice. The Middle East and Africa (MEA) region, while smaller, shows significant potential, particularly in the UAE and Saudi Arabia, driven by governmental investment in tourism and entertainment infrastructure and the construction of luxury, climate-controlled leisure facilities tailored for year-round operation.

The primary driver is the shift from traditional golf practice to technology-enabled, social, and experiential entertainment (eatertainment). Modern centers integrate high-quality Food & Beverage offerings, digital gaming, and sophisticated ball-tracking technology, attracting non-traditional golfers and corporate clients, significantly boosting revenue per customer visit.

F&B sales are critically significant, often contributing 40% to 60% of the total revenue for modern entertainment centers. This high contribution transforms the business model from a seasonal sports facility into a stable, year-round hospitality venue, mitigating the reliance solely on golf activity fees.

Proprietary radar-based and optical/camera-based tracking systems (e.g., those from TrackMan and FlightScope integrated into venue software) dominate the modern segment. These technologies are essential for accurate data capture and gamification, which are non-negotiable elements for the social, competitive experience demanded by consumers.

Major challenges include overcoming the extremely high initial capital expenditure required for sophisticated technology and multi-level construction, coupled with securing large parcels of prime, accessible real estate in high-density urban areas where land costs and development regulations are restrictive.

Due to severe urban land constraints and high population density, the Asia Pacific region, particularly South Korea and parts of China, is heavily focused on the growth and innovation of high-throughput indoor golf simulator venues and compact, multi-story centers, rather than large, sprawling outdoor ranges.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.