ID : MRU_ 434457 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

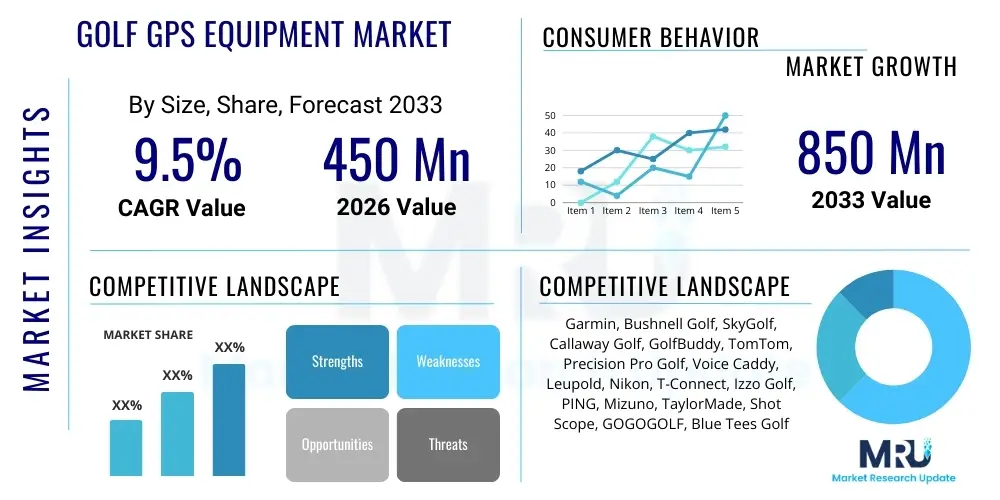

The Golf GPS Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 850 Million by the end of the forecast period in 2033.

The consistent expansion of the golf participation rates globally, particularly among younger demographics who are highly integrated with technology, is a primary factor driving this valuation growth. Furthermore, continuous product innovation, integrating high-definition mapping, enhanced battery life, and seamless connectivity with smartphones and wearables, enhances the perceived value and utility of GPS equipment, fostering replacement cycles and driving new purchases.

This steady financial trajectory is reinforced by the shift from traditional measurement tools (like simple rangefinders) toward integrated GPS solutions that offer comprehensive course management features, including hazard distances, shot tracking, and statistical performance analysis. The increasing accessibility of mid-range and budget-friendly GPS devices has broadened the consumer base, allowing amateur golfers to benefit from professional-grade insights, thereby solidifying the market's robust long-term financial outlook.

The Golf GPS Equipment Market encompasses a range of electronic devices designed to provide accurate yardage measurements and course intelligence to golfers, significantly enhancing strategic decision-making on the course. Products include handheld GPS units, GPS watches, and rangefinders with integrated GPS capabilities. Major applications revolve around maximizing performance, understanding course layout, optimizing club selection, and facilitating compliance with competitive golf rules. Benefits include faster pace of play, improved accuracy, comprehensive hazard management, and detailed post-round statistical analysis. Key driving factors involve the global expansion of golf tourism, technological miniaturization, and the increasing consumer appetite for data-driven athletic improvement.

Golf GPS equipment fundamentally transforms the experience of golf by delivering real-time, precise positional data. These devices use satellite technology to map out golf courses, providing distances to the front, middle, and back of the green, as well as critical layups and hazards. This immediate access to information allows golfers, regardless of skill level, to make better-informed decisions regarding shot power and trajectory, mitigating errors caused by guesswork or inaccurate visual estimation. The integration of advanced mapping capabilities, including 3D visualizations and aerial views, further elevates the utility of these tools beyond simple distance measurement, turning them into indispensable course management systems.

The market is defined by continuous technological convergence. Modern GPS watches, for instance, often double as fitness trackers and smartwatches, increasing their appeal to a broader, tech-savvy consumer base. Handheld devices are becoming more rugged, waterproof, and feature intuitive touchscreens akin to modern smartphones. This relentless pursuit of enhanced functionality and user experience is crucial for market growth, particularly as manufacturers strive to differentiate their offerings in a competitive landscape. Moreover, the increasing adoption of professional statistical tracking features integrated into consumer-grade devices democratizes performance analytics, making sophisticated game improvement tools accessible to the mass market.

Driving factors extend beyond basic utility; the influence of professional golf and media visibility plays a substantial role. As professional tours increasingly utilize advanced data and analytics, amateur golfers seek similar technological advantages to improve their own scores. Regulatory bodies often approve specific GPS models for tournament play, boosting consumer confidence and acceptance. Furthermore, the rising disposable income in emerging economies, coupled with significant investment in new golf course development, especially in the Asia-Pacific region, creates fertile ground for sustained market expansion over the forecast period.

The Golf GPS Equipment Market is characterized by robust growth, driven by key business trends focusing on integration, subscription models, and ecosystem development. Regional dynamics show North America maintaining dominance due to high golf participation and strong consumer spending on premium technology, while the Asia Pacific region emerges as the fastest-growing market, propelled by infrastructural investment in golf and rising middle-class affluence. Segment trends highlight the increasing preference for GPS watches due to their convenience and versatility, alongside the growing adoption of hybrid devices that combine the precision of laser rangefinders with the context provided by GPS mapping, signaling a demand for comprehensive, multi-functional solutions.

Current business trends indicate a strategic move toward creating integrated ecosystems where GPS devices communicate seamlessly with mobile applications and cloud-based performance platforms. This strategy allows manufacturers to offer value-added services, such as advanced data analytics, personalized coaching feedback, and connectivity to global golf course databases, transforming the sale of hardware into a recurring revenue model through premium subscriptions. Successful market participants are heavily investing in R&D to improve GPS accuracy (down to sub-meter levels) and optimize battery performance, addressing historical limitations that constrained user satisfaction. Furthermore, strategic partnerships with golf course operators and golf professional associations are common, enhancing device mapping quality and boosting brand visibility.

Geographically, while established markets in the US and Europe still account for the largest revenue share, future growth dynamism is largely concentrated in emerging markets. Countries like China, India, and South Korea are witnessing rapid expansion of golf infrastructure and associated leisure industries, translating into high demand for performance-enhancing gadgets. These regions often prioritize wearable technology, favoring GPS watches that blend lifestyle utility with sporting functionality. Companies are adapting their distribution strategies to penetrate these high-potential areas, often through e-commerce channels and localized marketing campaigns tailored to regional golfing cultures.

In terms of segmentation, the market’s evolution reflects a bifurcation of consumer needs. The core segment of dedicated golfers demands high-precision, robust handheld devices, often willing to pay a premium for features like slope adjustment and environmental condition compensation. Simultaneously, the casual golfer segment gravitates towards lower-cost, user-friendly GPS watches that prioritize ease of use and versatility, contributing significantly to volume growth. This dual demand structure necessitates manufacturers maintaining diverse product portfolios that cater to both the advanced, feature-rich requirements of the serious player and the fundamental needs of the recreational user.

User queries regarding the integration of Artificial Intelligence (AI) in the Golf GPS Equipment Market frequently center on concerns about real-time prescriptive analytics, the transition from descriptive data to predictive insights, and the potential for AI-driven personalized coaching tools. Users are keen to understand how AI will move beyond simple distance calculation to offer optimized strategic advice based on real-time factors like swing tempo, wind conditions, and historical course performance. Key expectations include personalized caddie recommendations and automated, precise shot tracking systems that require minimal user interaction, thereby transforming GPS devices from measurement tools into intelligent performance consultants.

The initial impact of AI is primarily observed in enhancing the data processing capabilities of GPS devices. While traditional GPS equipment provides static distances, AI algorithms leverage historical user data (such as successful shot patterns, club selection habits, and common misses) combined with real-time variables (elevation change, weather data) to offer prescriptive recommendations. For instance, an AI-enhanced device might recommend hitting a 7-iron instead of a 6-iron, factoring in the golfer's historical tendency to pull a shot under specific wind conditions, thus offering a sophisticated layer of decision support beyond simple yardage.

Furthermore, AI is crucial in refining the accuracy and user experience of shot tracking. Current manual shot tracking systems can be cumbersome. AI algorithms, particularly machine learning models trained on vast datasets of swing movements and ball flight, are enabling devices to automatically detect and classify shots with extremely high reliability, including identifying the specific club used without manual input. This automation minimizes disruption during play and ensures the collection of richer, more accurate performance data, which, in turn, feeds back into the AI model for continuous personalized optimization and improvement.

Looking forward, the role of AI is expected to extend into personalized coaching and course strategy. GPS devices integrated with AI will likely evolve into virtual caddies, offering game plan adjustments based on weaknesses identified across hundreds of previous rounds. This shift promises a democratization of high-level coaching, making sophisticated strategic analysis accessible to the average golfer. Manufacturers are focusing R&D efforts on edge computing within the device itself to allow for rapid, complex calculations without requiring constant connection to external servers, ensuring instantaneous, reliable guidance on the course.

The Golf GPS Equipment Market is significantly influenced by a dynamic interplay of Drivers, Restraints, and Opportunities. Key drivers include the global push for faster play and enhanced performance tracking, coupled with rapid technological miniaturization and price accessibility. Restraints primarily involve regulatory restrictions on features (like slope-adjusted distance calculations in competitive play), reliance on highly accurate, updated course mapping databases, and competition from multi-functional smartwatches. Opportunities lie in expanding the use of advanced sensors, integrating AI for hyper-personalized caddying experiences, and penetrating emerging markets with high-volume, mid-priced products. These forces collectively dictate the pace and direction of innovation and market penetration.

Drivers: The fundamental driver is the pursuit of athletic improvement. Modern golfers are metrics-driven, viewing technology as an essential tool for quantifying and optimizing performance. GPS technology offers an objective measure of course distance, significantly reducing uncertainty and fostering confidence, which directly translates to better scores. Furthermore, the increasing global emphasis on expediting the pace of play—a critical factor for the commercial viability of golf courses—makes GPS devices valuable assets, as they provide instant distances without the need for manual pacing or searching for yardage markers. This blend of performance enhancement and operational efficiency ensures sustained demand across both amateur and professional segments.

Restraints: Despite the benefits, significant restraints hinder wider adoption. One primary challenge is the requirement for frequent and accurate mapping updates. If course layouts change, or if the digital maps are inaccurate, the device loses its core utility, leading to consumer dissatisfaction. Furthermore, regulatory ambiguity, particularly regarding features like slope compensation, forces manufacturers to produce tournament-legal and non-legal versions, complicating product development and consumer choice. Lastly, the high initial cost of premium models and the ongoing pressure from sophisticated, non-dedicated smartwatches that offer basic GPS functionality at a similar or lower price point pose continuous competitive pressure on niche market players.

Opportunities: The market is rich with opportunities, particularly in leveraging adjacent technologies. The integration of advanced sensor fusion—combining GPS with inertial measurement units (IMUs) and barometers—can lead to highly accurate elevation data and superior shot tracking. The biggest opportunity lies in utilizing connectivity for ecosystem development, offering subscription tiers that provide deep, actionable insights and virtual coaching based on collected data. Geographically, untapped markets in Southeast Asia, Eastern Europe, and Latin America represent substantial long-term growth potential, provided manufacturers can adapt products to local course conditions and pricing sensitivities.

The Golf GPS Equipment Market is primarily segmented by product type, distribution channel, and application. Product segmentation distinguishes between handheld devices, which offer robust screen size and detailed mapping, and GPS watches, favored for their convenience and wearability, alongside the growing segment of specialized rangefinders with embedded GPS functions. Segmentation by distribution emphasizes the critical role of specialized sports retail and increasingly dominant e-commerce channels. Application segmentation divides the market based on the end-user’s skill level, catering separately to professional/serious amateur golfers who demand advanced features, and recreational golfers who prioritize ease of use and affordability.

The segmentation by Product Type reflects diverse consumer preferences regarding form factor and functionality. Handheld devices remain the gold standard for golfers who require large, detailed visualizations of the course, often incorporating features like flyover views and touch-to-target functionality. Conversely, GPS watches have surged in popularity, driven by their ease of use, instant accessibility, and often multi-sport functionality, making them appealing to younger, fitness-conscious users. The hybrid segment, combining laser precision for specific targets with GPS mapping for course context, represents the premium tier, solving the trade-off between absolute accuracy and comprehensive course knowledge.

Distribution channel analysis reveals a critical shift toward digital marketplaces. While traditional brick-and-mortar sports retailers provide essential product demonstration and expert advice, the high growth rate is observed within e-commerce platforms. Online sales benefit from price transparency, direct-to-consumer models, and access to a wider global inventory, significantly aiding market penetration into geographically diverse areas. Manufacturers must maintain robust omnichannel strategies to capture both the experiential buyer in physical stores and the price-sensitive, convenience-driven buyer online.

Application-based segmentation is crucial for targeted marketing and product development. Professional and serious amateur golfers constitute a high-value segment, requiring devices with sophisticated features such as detailed stat tracking, environmental compensation, and tournament-legal modes. The recreational segment, constituting the majority of the market volume, seeks simplicity, reliability, and value. Successful segmentation requires tailoring marketing messages and pricing strategies to address the distinct needs and purchasing power of these separate user groups, ensuring product features align perfectly with the golfer's skill level and frequency of play.

The value chain of the Golf GPS Equipment Market starts with upstream activities involving core component manufacturing, primarily satellite navigation chips, high-resolution display units, and durable battery technologies. Midstream activities encompass product design, software development (including proprietary mapping databases and algorithms), and final assembly. Downstream activities involve comprehensive distribution through both direct and indirect channels, sophisticated marketing campaigns, and extensive after-sales support, crucial for managing map updates and technical troubleshooting. The efficiency of this chain is highly dependent on securing stable supply of high-precision components and maintaining rigorous quality control over integrated software.

Upstream analysis focuses heavily on technological sourcing and strategic supply management. Key inputs include advanced Global Navigation Satellite System (GNSS) receivers capable of leveraging multiple satellite constellations (like GPS, GLONASS, Galileo) for enhanced accuracy. The competitive advantage here lies in locking in favorable agreements with specialized component suppliers, ensuring both reliability and cost-effectiveness. Furthermore, software development—the creation and maintenance of proprietary golf course maps—is a capital-intensive upstream process, requiring continuous surveying and data aggregation to maintain accuracy and geographical coverage, which is a major differentiator among competitors.

Downstream market operations involve managing a complex distribution landscape. Indirect channels, primarily through major specialty golf retailers (e.g., Golf Galaxy, PGA Superstore) and large e-commerce giants (Amazon, manufacturer websites), dominate sales volume. Direct channels, involving sales directly to golf courses or professional organizations for use in club rentals or training academies, offer higher margins but lower volume. Effective distribution necessitates efficient logistics for inventory management and returns processing, especially for international shipments. Post-sales support, including software updates and customer service, is an integral part of the downstream chain, directly influencing brand loyalty and repeat purchases.

The flow from raw materials to the end-user is characterized by significant value addition at the technology integration and software development stages. The cost structure is weighted towards R&D and mapping database licensing, rather than pure manufacturing. Success in the market is often determined by the ability to control the intellectual property related to mapping accuracy and the speed of software innovation, rather than manufacturing scale alone. Companies that tightly integrate their software development with user feedback loops create a more responsive and desirable product offering.

The potential customer base for Golf GPS Equipment spans all demographics and skill levels within the golfing population, although target segments are generally divided into three main categories: performance-driven serious amateurs, leisure-focused recreational golfers, and institutional buyers like golf course operators and teaching professionals. Serious amateurs and low-handicap players are the primary buyers of high-end, feature-rich devices, seeking quantifiable performance data and advanced statistical analysis tools to shave strokes off their game. Recreational golfers prioritize ease of use, basic yardage measurement, and robust battery life at an affordable price point, often opting for entry-level GPS watches or smartphone apps.

The serious amateur segment represents the most lucrative group for premium device manufacturers. These buyers are typically highly knowledgeable about golf technology, participate frequently in competitive or social tournaments, and view investment in high-quality GPS equipment as essential for performance optimization. They seek hybrid devices that provide hyper-accuracy (laser) combined with comprehensive course management (GPS), valuing features like slope adjustment, environmental data tracking, and seamless connectivity to performance platforms. Marketing efforts targeting this group focus on demonstrating measurable score improvement and technological superiority.

The recreational golfer segment, including beginners and casual players, forms the largest volume segment. These customers use GPS primarily to speed up play, eliminate guesswork, and enjoy the game more. Their purchase decisions are heavily influenced by ease of operation, battery endurance (often requiring multiple rounds per charge), and competitive pricing. This group is increasingly adopting GPS watches due to their non-intrusive nature and dual functionality as everyday smart devices. For this segment, visibility in broad retail channels and strong value propositions are paramount.

Institutional buyers, such as golf clubs and teaching academies, represent a growing niche, purchasing devices for rental fleets or instructional purposes. These buyers require rugged, simple-to-use devices with centralized fleet management capabilities for easy charging and maintenance. Golf professionals and coaches utilize the advanced tracking capabilities of high-end units to collect granular student data, making performance analysis more objective and targeted. This segment demands high reliability and robust service contracts, ensuring minimal downtime for their equipment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 850 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Garmin, Bushnell Golf, SkyGolf, Callaway Golf, GolfBuddy, TomTom, Precision Pro Golf, Voice Caddy, Leupold, Nikon, T-Connect, Izzo Golf, PING, Mizuno, TaylorMade, Shot Scope, GOGOGOLF, Blue Tees Golf |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Golf GPS Equipment Market is defined by the convergence of high-precision satellite technology, advanced sensor integration, and sophisticated software architecture optimized for outdoor use. Core technology centers around multi-constellation GNSS receivers (supporting GPS, GLONASS, and Galileo) to ensure global coverage and enhanced sub-meter accuracy, which is critical for trustworthy yardage readings. A major recent technological shift involves the integration of high-resolution, sunlight-readable transflective or AMOLED displays, improving device usability under bright conditions. Furthermore, the development of specialized, low-power microprocessors and highly efficient lithium-ion batteries is extending device longevity, often enabling up to 20 hours of continuous GPS tracking on a single charge.

Modern GPS equipment increasingly incorporates sensor fusion technologies to enrich data collection beyond simple location tracking. Inertial Measurement Units (IMUs), including accelerometers and gyroscopes, are vital for automatically detecting swing movement, classifying shots, and calculating distances traveled during the swing and ball flight. Barometers are integrated to measure atmospheric pressure, allowing for more accurate elevation change calculations, which are essential for adjusting effective playing distance in hilly terrain. This blending of GPS data with physical sensor inputs allows the devices to gather highly granular performance metrics that were previously only available through high-cost, specialized launch monitors.

Software and connectivity represent the critical technological differentiators. Advanced proprietary software manages vast databases of pre-loaded golf course maps (often exceeding 40,000 global courses) and facilitates quick, over-the-air updates. Bluetooth and Wi-Fi connectivity are standard, enabling seamless synchronization with smartphone apps for data review, scorekeeping, and firmware updates. The trend towards cloud-based platforms is driving the market, allowing users to store, analyze, and share performance statistics across multiple devices and interact with online communities, moving the device usage beyond the golf course and into the realm of long-term game improvement strategy.

North America maintains its position as the dominant region in the Golf GPS Equipment Market, driven by high golf participation rates, significant consumer expenditure on sporting technology, and the presence of major industry leaders like Garmin and Bushnell. The market maturity in the United States fosters high replacement rates and continuous demand for premium, feature-rich devices, particularly high-end GPS watches and hybrid rangefinders. The region benefits from early technology adoption and a well-established infrastructure of thousands of mapped golf courses, providing a robust operational environment for all types of GPS equipment.

Europe represents a stable yet highly competitive market. Countries in Western Europe, particularly the UK, Germany, and Scandinavia, show consistent demand, heavily influenced by the professional golf circuits and a cultural emphasis on outdoor sports. European consumers often exhibit a preference for sophisticated design and robust build quality, favoring established brands with strong reliability reputations. Regulatory compliance regarding device usage in competitive play is a significant factor here, driving demand for tournament-legal modes across various devices.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally during the forecast period. This growth is fueled by expanding golf infrastructure in key economies such as China, South Korea, Japan, and Australia, coupled with rising disposable incomes. South Korea and Japan, in particular, show a strong cultural inclination towards technology adoption in sports, leading to rapid uptake of advanced GPS watches and voice caddy systems. Manufacturers are actively tailoring products to meet the unique requirements of the dense urban golfing environment prevalent in parts of APAC, focusing on miniaturization and localized course databases.

The Golf GPS Equipment Market is projected to experience a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033, driven by technological integration, increased global golf participation, and rising demand for performance analytics.

The GPS Watches segment is expected to show the highest unit volume growth, owing to their convenience, miniaturization, and multi-functional capabilities that appeal to a broad base of recreational and fitness-conscious golfers.

AI is transforming GPS devices from simple measurement tools into intelligent virtual caddies by using machine learning to offer prescriptive strategic advice, automate highly accurate shot tracking, and personalize club selection recommendations based on historical performance and real-time conditions.

Key restraints include the ongoing challenge of maintaining current and highly accurate global golf course mapping databases, the high initial cost of premium models, and the complexity introduced by golf regulatory restrictions concerning specific features like slope adjustment in tournament play.

North America currently dominates the market, largely due to its extensive established golf culture, high density of mapped courses, and substantial consumer willingness to invest in advanced technology for game improvement.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.