ID : MRU_ 433183 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

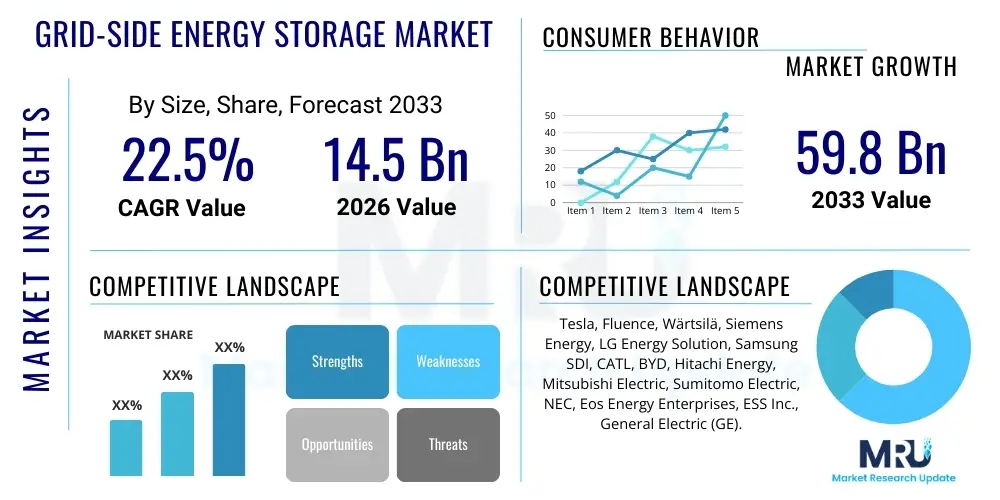

The Grid-Side Energy Storage Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2026 and 2033. The market is estimated at $14.5 Billion in 2026 and is projected to reach $59.8 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the global imperative to integrate intermittent renewable energy sources, such as solar and wind power, into existing electrical grids, ensuring stability and reliability while accelerating decarbonization efforts across major economies. The shift towards large-scale, utility-level battery installations and sophisticated control systems defines the current trajectory of market expansion.

The valuation reflects robust investment across all major geographical regions, particularly in North America and the Asia Pacific, where supportive regulatory frameworks and significant renewable energy targets are established. Grid modernization initiatives, coupled with the necessity for frequency regulation and peak shaving capabilities, have solidified the business case for multi-megawatt storage projects. Financial instruments and government mandates, including tax credits and capacity markets, are further de-risking investments, attracting large institutional capital and accelerating the deployment cycles necessary to meet the increasing demand for grid flexibility and resilience in the face of escalating climate volatility and infrastructure constraints.

Furthermore, the continuous reduction in the levelized cost of storage (LCOS), predominantly associated with Lithium-ion battery technology, acts as a primary economic catalyst. Advancements in alternative long-duration storage technologies, such as flow batteries and compressed air energy storage (CAES), are poised to capture a growing share, addressing the crucial requirement for multi-hour discharge capabilities essential for seasonal storage and managing extended periods of low renewable generation. This technological diversification, combined with optimized manufacturing processes and supply chain maturity, underpins the aggressive forecasted growth rate through 2033, translating into a transformative infrastructure investment cycle globally.

The Grid-Side Energy Storage Market encompasses technologies and systems deployed at the transmission or distribution level of the electrical grid to store electricity generated at one time for use at a later time. These systems are critical infrastructure components designed to enhance grid reliability, improve asset utilization, facilitate the seamless integration of variable renewable energy sources, and provide essential ancillary services such as frequency regulation and voltage support. The core product offering includes various battery energy storage systems (BESS), predominantly based on lithium-ion chemistry, alongside mechanical storage (Pumped Hydro, CAES, Flywheels) and thermal storage solutions, all integrated with advanced power conversion systems (PCS) and energy management software (EMS) tailored for utility operation.

Major applications for grid-side storage span across energy arbitrage, where energy is bought or stored during off-peak hours and dispatched during high-demand peak times; capacity firming, which ensures that intermittent renewable power plants deliver predictable output; and crucial transmission congestion relief, allowing existing infrastructure to handle higher loads without immediate, costly upgrades. The fundamental benefits realized by utility operators and grid stakeholders include significant reductions in operational costs, enhanced grid stability leading to fewer outages, and reduced reliance on polluting, fast-ramping fossil fuel peaker plants. This multifaceted utility makes grid-side storage an indispensable tool for achieving modern, resilient, and sustainable electrical systems capable of supporting the transition to net-zero emissions targets globally.

Driving factors for this market are centered around stringent governmental renewable portfolio standards (RPS) and decarbonization commitments, which necessitate massive scaling of intermittent resources like solar and wind power. The increasing frequency of extreme weather events requires heightened grid resilience, prompting utilities to invest heavily in distributed and centralized storage solutions that can rapidly restore power or maintain critical services during disruptions. Furthermore, falling technology costs, alongside supportive policies like the US Investment Tax Credit (ITC) extension and European Union’s clean energy packages, provide the necessary economic impetus and regulatory clarity for accelerated, large-scale deployment of storage assets across developed and emerging economies alike, defining the current investment cycle in grid infrastructure.

The Grid-Side Energy Storage market exhibits strong, favorable business trends characterized by massive utility-scale project announcements, rapid maturation of supply chains, and increasing vertical integration among key players, ranging from raw material suppliers to system integrators. Key business trends indicate a definitive shift toward larger, centralized Battery Energy Storage System (BESS) installations, often exceeding 100 MW in capacity, reflecting economies of scale and the urgent need for robust capacity additions. Technological advancements are focused intensely on improving energy density, enhancing safety protocols (particularly thermal management), and extending the cycle life of battery cells, ensuring long-term operational viability and improved financial returns for asset owners. Furthermore, sophisticated software platforms leveraging artificial intelligence are becoming standard, optimizing dispatch strategies and maximizing revenue generation across multiple stacked services.

Regionally, the market is currently dominated by North America, specifically the United States, driven by state-level mandates in California, Texas, and the Northeast, and underpinned by federal incentives supporting renewable and storage deployment. However, the Asia Pacific region, led by China, India, and Australia, is poised for the highest growth rate, fueled by aggressive national targets for renewable energy integration and significant investments in modernizing rapidly expanding grids. Europe, facing high energy costs and intermittency issues, focuses heavily on cross-border interconnection projects and storage for frequency regulation, with Germany and the UK leading adoption. These regional dynamics highlight a globally fragmented but universally essential infrastructure build-out, prioritizing localized grid needs while contributing to global decarbonization targets.

Segment-wise, Lithium-ion technology remains the undisputed leader due to its high energy efficiency, rapid response time, and proven manufacturing scalability, dominating short-to-medium duration applications (2-6 hours). The market is seeing rapid growth in the application segment of peak shaving and capacity firming, driven by the escalating cost of electricity during high-demand periods. Within the ownership structure, regulated utilities and Independent Power Producers (IPPs) are the dominant investors, seeking to leverage storage for grid optimization and to secure long-term power purchase agreements (PPAs). The emerging trend is the increasing market share of non-Li-ion technologies, particularly flow batteries and specialized long-duration solutions, aiming to address duration requirements exceeding eight hours, thereby diversifying the technological portfolio available to grid planners.

User queries regarding AI’s influence on grid-side storage primarily revolve around the optimization of asset utilization, predictive forecasting accuracy, and enhancing operational security. Users seek understanding on how AI can maximize the economic value of high-capital storage assets by making optimal dispatch decisions in volatile energy markets. Key concerns focus on the integration complexity of AI algorithms with legacy grid infrastructure and the data requirements necessary for effective machine learning models. Expectations are high for AI to deliver truly autonomous grid management, moving beyond simple scheduling to dynamic, real-time responses to grid disturbances, thereby increasing the overall efficiency and lifespan of storage units while ensuring system reliability.

Artificial intelligence is fundamentally transforming the Grid-Side Energy Storage market by moving operations from deterministic scheduling to dynamic, predictive control systems. AI algorithms leverage vast datasets of historical demand, weather patterns, market prices, and equipment performance to forecast grid conditions with high accuracy, often minutes to hours ahead. This predictive capability allows energy management systems (EMS) to execute highly optimized charging and discharging cycles, ensuring storage assets capture maximum revenue through arbitrage, participate effectively in ancillary services markets, and reduce premature degradation of the battery cells by maintaining optimal operating parameters. This software layer is critical for maximizing the economic return on substantial hardware investments.

Furthermore, AI significantly enhances the reliability and maintenance protocols of storage infrastructure. By analyzing real-time performance data—including voltage, temperature, current, and state-of-charge—AI models can detect subtle anomalies indicative of potential failures, such as thermal runaway risks or cell imbalance, well before they lead to critical system shutdowns. This predictive maintenance approach minimizes unplanned downtime, extends the useful life of the assets, and significantly improves safety standards. The deployment of AI also facilitates complex integration with hybrid resources, coordinating the output of co-located solar farms or wind turbines with the storage capacity to provide guaranteed firm power, a service increasingly valued by grid operators worldwide.

The Grid-Side Energy Storage market trajectory is governed by a dynamic interplay of powerful drivers, persistent restraints, compelling opportunities, and significant impact forces that collectively shape investment decisions and technological adoption curves. The market is primarily driven by global decarbonization mandates and the resultant need to integrate high penetrations of renewable energy, which mandates flexibility and capacity provided by storage. However, high initial capital expenditure (CapEx) and long-term uncertainty regarding regulatory market structures currently restrain faster deployment. The substantial opportunity lies in the rapid technological maturation of long-duration storage solutions and the potential for storage to defer or eliminate costly transmission and distribution (T&D) infrastructure upgrades. These elements are fundamentally impacted by shifting geopolitical dynamics concerning critical mineral supply chains, ongoing standardization efforts, and evolving safety regulations, requiring careful navigation by market participants.

Key drivers include the dramatic reduction in battery manufacturing costs, making utility-scale projects increasingly competitive against traditional gas peaker plants. Regulatory incentives, such as federal tax credits and state-level procurements, provide crucial investment certainty. Additionally, the proliferation of distributed energy resources (DERs) necessitates centralized control and balancing, a role perfectly suited for grid-side storage, enhancing overall system stability and power quality. Conversely, restraints involve the complex and lengthy permitting and interconnection processes required for large-scale projects, which often slow deployment schedules. Public perception surrounding battery safety, particularly in densely populated areas, also poses a constraint, demanding rigorous fire suppression and thermal management systems that add to system costs.

Opportunities are exceptionally strong in developing sophisticated hybrid power plants that couple solar/wind generation with storage under a single interconnection, streamlining regulatory approval and maximizing asset utilization. The emergence of 'storage-as-a-service' business models allows utilities to access storage capacity without bearing the full CapEx risk. Furthermore, impact forces, specifically the volatility in raw material prices (e.g., lithium, cobalt, nickel) and the need for ethical sourcing and recycling infrastructure, are demanding robust and diversified supply chain strategies. Standardization of communication protocols and system interoperability is a critical force that, when achieved, will drastically reduce integration costs and accelerate market scale-up, ensuring that storage effectively fulfills its potential role as the central flexibility resource of the modern grid.

The Grid-Side Energy Storage Market is comprehensively segmented based on technology type, application, ownership model, and connection point, providing granular insights into market dynamics and investment hotspots. The technology segmentation is paramount, differentiating between established chemical storage solutions like Lithium-ion, emerging long-duration options such as Flow Batteries, and mechanical solutions including Pumped Hydro and Compressed Air Energy Storage. Understanding these segments is crucial as they dictate the optimal duration, power rating, and project economics relevant for specific utility needs. The application segmentation highlights how storage assets deliver value across services like frequency regulation, energy shifting, and T&D deferral, reflecting the stacked revenue streams vital for profitability. This detailed segmentation allows stakeholders to tailor technological deployments to precise grid requirements, optimizing performance and financial returns across diverse operating environments.

The value chain for grid-side energy storage begins with the complex upstream analysis, focusing heavily on the extraction, processing, and refinement of critical raw materials, predominantly lithium, cobalt, nickel, and manganese, essential for Li-ion battery manufacturing. Upstream activities also include the production of key components such as electrodes, separators, electrolytes, and cell casing. Given the geopolitical concentration of these resources and the environmental impact of mining, securing a stable and ethically sourced supply chain remains a high-priority risk factor. Manufacturers of battery cells and modules constitute the middle segment, rapidly advancing technology and scaling production capacity to meet utility-scale demand, often consolidating production processes to achieve economies of scale and improve competitive pricing for the final storage system.

The downstream analysis focuses on system integration, deployment, and operational phases. System integrators, utilizing components like power conversion systems (PCS), advanced energy management systems (EMS) software, and balance-of-plant (BOP) components, assemble the final modular storage solutions tailored to specific site and grid requirements. Distribution channels are typically direct sales models or long-term engineering, procurement, and construction (EPC) contracts executed directly with utilities, Independent Power Producers (IPPs), and Transmission System Operators (TSOs). Indirect distribution, involving specialized third-party aggregators who manage a portfolio of storage assets for grid services, is an emerging model, particularly in decentralized markets, offering flexibility to smaller entities.

The installation and commissioning phase, followed by long-term operation and maintenance (O&M), complete the downstream segment. Direct engagement, where the storage vendor or a specialized O&M provider maintains the asset lifecycle, is the prevalent model due to the technical complexity and high-stakes reliability required by the grid. The value chain concludes with end-of-life management, including recycling and repurposing of battery materials, which is gaining critical importance due to regulatory pressures and the rising cost of raw inputs. Effective management across the entire chain, from resource extraction to recycling, is essential for sustaining the market’s rapid growth and achieving circular economy objectives within the energy sector.

The primary customers and end-users of grid-side energy storage solutions are large entities responsible for the stability, transmission, and distribution of electricity. Regulated and non-regulated electric utilities represent the largest buying segment. Utilities purchase and deploy these systems to manage congestion on their lines, defer expensive substation and feeder upgrades (T&D deferral), and meet state-mandated reliability targets. For these vertically integrated entities, storage is an operational tool integral to managing peak loads and ensuring seamless integration of distributed generation, providing a definitive return on investment through optimized asset utilization and reduced maintenance expenses on conventional infrastructure.

Independent Power Producers (IPPs) and large renewable energy developers constitute another significant customer base. IPPs utilize grid-side storage primarily to stabilize and firm the output of their large solar and wind farms, enabling them to offer dispatchable, predictable power under long-term Power Purchase Agreements (PPAs). This capacity firming service often makes the renewable project more appealing to utilities and grid operators by mitigating the inherent intermittency of renewable generation. The economic viability for IPPs is strongly linked to their ability to stack multiple revenue streams, including energy sales, capacity payments, and participation in ancillary services markets, necessitating high-performance storage assets managed by sophisticated control systems.

Furthermore, Transmission System Operators (TSOs) and Distribution System Operators (DSOs) are increasingly important customers, particularly in jurisdictions with unbundled energy markets. TSOs procure grid-scale storage for system-wide frequency regulation, inertia response, and emergency black start capabilities, which are essential for maintaining the overall health and security of the macroscopic grid network. DSOs focus on optimizing the local distribution network, using storage for voltage control and localized resilience. These operators prioritize technological features such as rapid response time, high reliability, and seamless integration with existing SCADA and grid control systems, making them critical buyers focused on system performance rather than purely energy arbitrage.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $14.5 Billion |

| Market Forecast in 2033 | $59.8 Billion |

| Growth Rate | 22.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tesla, Fluence, Wärtsilä, Siemens Energy, LG Energy Solution, Samsung SDI, CATL, BYD, Hitachi Energy, Mitsubishi Electric, Sumitomo Electric, NEC, Eos Energy Enterprises, ESS Inc., General Electric (GE). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Grid-Side Energy Storage Market is dominated by electro-chemical storage, but it is rapidly evolving to incorporate diverse solutions addressing varying duration and power needs. Lithium-ion (Li-ion) batteries, specifically Nickel Manganese Cobalt (NMC) and Lithium Iron Phosphate (LFP) chemistries, currently account for the vast majority of deployed capacity due to their high energy density, efficiency, and proven scalability in manufacturing. LFP chemistry is increasingly favored for utility applications due to its superior safety profile and longer cycle life, despite slightly lower energy density compared to NMC. The industry focus remains on optimizing thermal management systems and standardizing containerized solutions to enhance safety, reduce installation complexity, and decrease overall system costs, securing Li-ion’s immediate dominance for short- to medium-duration services (up to 4 hours).

However, the strategic imperative for decarbonization requires storage solutions capable of discharging power for eight hours or more, driving significant investment into long-duration energy storage (LDES) technologies. Flow batteries, particularly Vanadium Redox Flow Batteries (VRFBs), represent a major technological contender in this space. Flow batteries decouple energy capacity from power output, offering inherent scalability and non-flammable operation, making them highly suitable for multi-hour applications where site safety is paramount. While they currently exhibit a lower energy density and higher complexity compared to Li-ion, rapid innovation in electrolyte chemistry and system design is improving their commercial viability, particularly for use in remote areas or large industrial facilities requiring extended backup or time shifting.

Beyond chemical batteries, mechanical storage technologies like Compressed Air Energy Storage (CAES) and advanced Pumped Hydro Storage (PHS) continue to play a niche, but critical role, especially for gigawatt-hour scale, long-duration requirements. CAES leverages geographic formations to store large volumes of compressed air, offering extremely long discharge times, while modern PHS systems are being developed using closed-loop or underground concepts to overcome geographical limitations. Additionally, ongoing research into alternative technologies, such as gravitational storage and next-generation solid-state batteries, aims to further diversify the technological portfolio, ultimately offering grid planners a resilient mix of short-term, high-power response mechanisms and long-term, large-capacity reserves necessary for a fully decarbonized and stable electric grid of the future.

The market is overwhelmingly driven by Lithium-ion (Li-ion) battery technology, specifically the decreasing Levelized Cost of Storage (LCOS) and the proven capability of LFP chemistry to provide short-to-medium duration (2–4 hours) services required for frequency regulation, capacity firming, and energy arbitrage at the utility scale.

Grid-side storage systems, particularly those installed at distribution substations, can absorb peak loads and manage localized congestion, effectively postponing or eliminating the need for expensive, time-consuming traditional infrastructure upgrades such as installing new transformers or reinforcing transmission lines, providing significant economic value to utilities.

The market trend shows accelerating interest and investment in LDES technologies, such as Flow Batteries (e.g., Vanadium Redox) and advanced Compressed Air Energy Storage (CAES). This shift is driven by the necessity to store power for 8 hours or more, which is essential for managing seasonal renewable variability and achieving deep grid decarbonization targets.

North America, led by the United States, currently dominates the grid storage market in terms of deployed capacity and immediate project pipeline. This leadership is sustained by strong regulatory mandates, significant federal tax incentives, and highly active capacity and ancillary services markets.

AI is crucial for optimizing the economic performance and longevity of grid storage assets. It uses advanced machine learning for predictive forecasting of energy prices and demand, facilitating optimal dispatch decisions, and enabling predictive maintenance to minimize operational downtime and extend the battery system's lifespan.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.