ID : MRU_ 437207 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

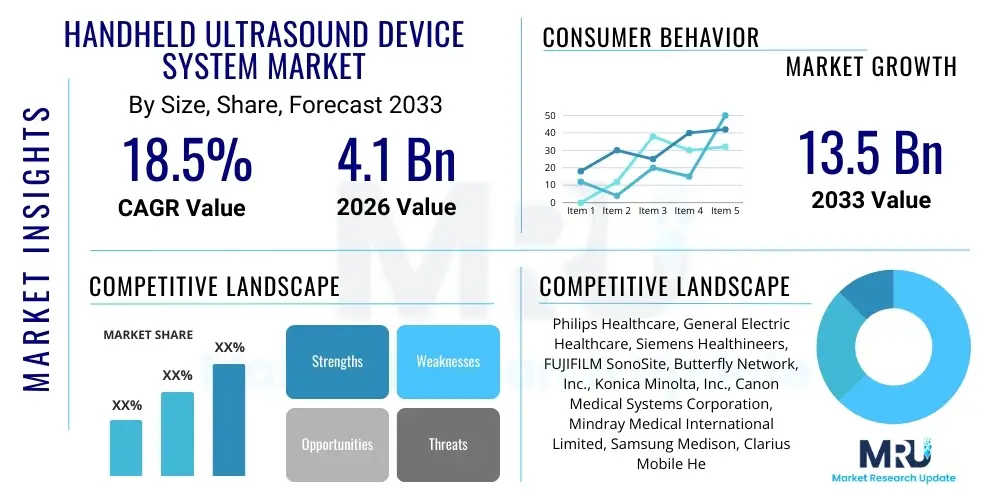

The Handheld Ultrasound Device System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 4.1 Billion in 2026 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033. This substantial growth is fundamentally driven by the accelerating shift towards point-of-care (PoC) diagnostics, especially in resource-limited settings and emergency medical services, where speed and portability are paramount. The continuous miniaturization of sophisticated transducer technology, coupled with the integration of powerful software applications accessible via smartphones and tablets, significantly lowers the barrier to entry for widespread clinical adoption. Furthermore, the enhanced diagnostic utility across numerous clinical specialties, ranging from primary care to specialized cardiology and anesthesiology procedures, solidifies the market's robust expansion trajectory through the forecast period.

The Handheld Ultrasound Device System Market encompasses highly portable, miniaturized diagnostic imaging tools that utilize high-frequency sound waves to create real-time internal images of the human body. These systems, often connected to or integrated with standard smart devices like smartphones or tablets, offer unprecedented flexibility and accessibility compared to traditional cart-based ultrasound machines. The primary product description centers on their lightweight design, robust battery life, and superior software interface, which democratizes diagnostic imaging by making it available outside conventional hospital radiology departments. These devices typically employ phased array, convex, or linear transducers optimized for specific clinical applications, such as abdominal, cardiac, vascular, and obstetrical imaging.

Major applications of handheld ultrasound systems are concentrated in Point-of-Care Ultrasound (POCUS), where rapid, bedside diagnostics are essential. This includes emergency departments for triage and rapid assessment (FAST exams), critical care units for hemodynamic monitoring, and primary care settings for initial diagnostic screening. Furthermore, handheld devices are increasingly utilized in procedural guidance, such as vascular access, nerve blocks, and musculoskeletal injections, enhancing safety and efficiency for clinicians. The devices significantly improve clinical workflow by providing immediate visualization, thereby reducing the time required for diagnosis and subsequent treatment decisions, especially in time-sensitive medical scenarios.

The principal benefits driving the adoption of these systems include enhanced diagnostic workflow efficiency, improved patient management outcomes due to immediate visualization capabilities, and substantial cost reduction compared to large console systems. Driving factors include the escalating global demand for accessible and affordable healthcare, increasing technological advancements in transducer miniaturization and artificial intelligence (AI) integration, and the growing focus on decentralized healthcare delivery models, particularly in emerging economies where fixed infrastructure is scarce. This convergence of portability, affordability, and advanced functionality positions handheld ultrasound as a disruptive technology in modern medical imaging.

The Handheld Ultrasound Device System Market is experiencing dynamic growth, characterized by significant business trends focused on strategic partnerships between medical device manufacturers and technology giants (particularly software and AI firms) to enhance image processing and connectivity capabilities. Key business trends also include the proliferation of subscription-based service models (Ultrasound-as-a-Service, or UaaS) aimed at reducing upfront capital expenditure for smaller clinics and individual practitioners, thereby accelerating market penetration. Furthermore, companies are prioritizing regulatory approvals across diverse international jurisdictions, enabling wider global access for their portable diagnostic platforms. The competitive landscape is becoming increasingly crowded, forcing established cart-based ultrasound vendors to rapidly expand their handheld portfolios while simultaneously innovative startups focus solely on high-performance, cost-effective wireless solutions, stimulating intense technological competition and driving down consumer prices.

Regional trends indicate North America currently dominates the market share, fueled by high healthcare expenditure, early adoption of POCUS protocols, and extensive reimbursement coverage for bedside ultrasound procedures. However, the Asia Pacific (APAC) region is projected to exhibit the fastest Compound Annual Growth Rate, driven by massive untapped populations, government initiatives promoting affordable diagnostic infrastructure, and rising awareness regarding early disease detection, particularly in large economies such as China and India. European regional dynamics are characterized by integrated healthcare systems actively incorporating handheld devices into primary care and ambulance services to optimize referral pathways and streamline patient flow management across diverse clinical settings. Furthermore, Latin America and the Middle East and Africa (MEA) are emerging as high-potential markets due to improvements in digital infrastructure and increased investment in mobile health solutions to bridge urban-rural healthcare disparities.

Segment trends highlight the dominance of the wireless handheld segment due to its superior convenience and seamless integration with existing hospital IT networks and personal smart devices. Application-wise, Emergency Medicine and Critical Care remain pivotal segments, although primary care and specialty segments like musculoskeletal (MSK) ultrasound are exhibiting rapid growth rates, reflecting expanded clinical utility beyond traditional abdominal and cardiac assessments. End-user trends show Ambulatory Surgical Centers (ASCs) and physician offices increasing their adoption significantly, moving handheld ultrasound from a purely hospital-centric tool to a widely distributed diagnostic modality accessible throughout the entire healthcare ecosystem. Continuous advancements in battery technology, transducer material science, and computational algorithms are defining the future trajectory of segment performance and technological differentiation across all product categories.

Common user questions regarding the influence of Artificial Intelligence on the Handheld Ultrasound Device System Market frequently revolve around improved image clarity in non-expert hands, the reliability of automated diagnostic reporting, and the ability of AI to simplify complex scanning protocols. Users are primarily concerned with whether AI integration will democratize the technology sufficiently for use by non-radiologists, how AI handles artifacts and noise inherent in handheld imaging, and the long-term cost implications of adopting AI-powered devices. Key expectations center on AI serving as an invaluable clinical assistant, automatically calculating ejection fractions, identifying pathology (e.g., fluid collections, deep vein thrombosis), and guiding the user to acquire optimal diagnostic images, thereby mitigating the steep learning curve traditionally associated with ultrasound operation. The consensus expectation is that AI will transform these portable devices from mere visualization tools into sophisticated, user-friendly diagnostic systems capable of providing quantifiable clinical insights instantly at the patient bedside, accelerating diagnostic throughput and reducing dependency on highly specialized personnel.

The integration of deep learning algorithms and machine vision into handheld ultrasound platforms fundamentally enhances their functionality and broadens their scope of application. AI algorithms are instrumental in optimizing image quality in real-time by performing noise reduction and contrast enhancement, compensating for the physical limitations of smaller, lower-power transducers compared to cart-based systems. This computational enhancement ensures that the diagnostic output remains robust and reliable, even when scanning conditions are suboptimal or when performed by clinicians with limited prior ultrasound experience. Furthermore, AI enables automated measurements (e.g., organ size, fetal biometry, vascular flow velocities) which significantly reduce the subjective variability associated with manual caliper placement, improving the standardization and consistency of diagnostic data acquired across various clinical environments.

This technological leap has significant implications for training and deployment. AI-driven feedback mechanisms can actively guide users, indicating correct probe placement and ensuring the acquisition of standard planes (e.g., cardiac windows), effectively transforming the device into a comprehensive training tool. For established practitioners, AI expedites critical analysis, automatically flagging areas of potential concern and providing preliminary interpretations that can be quickly reviewed and confirmed. As AI models continue to be trained on vast datasets of ultrasound images, the specificity and sensitivity of automated disease detection are set to improve dramatically, solidifying AI’s role not just as a feature, but as a core component of future handheld ultrasound innovation, driving adoption in settings ranging from austere environments to high-throughput outpatient clinics.

The dynamics of the Handheld Ultrasound Device System Market are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively constitute the Impact Forces shaping its trajectory. The primary driver is the pervasive demand for immediate, non-invasive diagnostic tools at the point of care, significantly reducing diagnostic turnaround times and improving critical patient outcomes, particularly in emergency and trauma scenarios. However, market expansion is restrained by significant regulatory complexities associated with medical device classification and cybersecurity vulnerabilities arising from wireless connectivity and data handling protocols. Opportunities abound in leveraging telemedicine and remote diagnostics, especially in underserved geographical regions, utilizing the inherent portability of the technology to deliver expert diagnostics virtually. These forces dictate strategic investment, product development pathways, and market entry strategies for all stakeholders, resulting in a rapid evolutionary pace characterized by continuous technological iteration and competitive pricing strategies aimed at mass market adoption globally.

Key drivers center on the decreasing cost of hardware components, particularly efficient transducers and processors, which makes sophisticated portable systems economically viable for a broader range of purchasers, including independent practitioners and low-resource clinics. Coupled with this is the escalating prevalence of chronic diseases, requiring continuous or frequent monitoring and diagnosis outside the traditional hospital setting. The robust clinical evidence supporting the efficacy of POCUS across nearly every medical specialty further validates its clinical necessity, promoting widespread professional endorsement and inclusion in standardized medical training curricula. Furthermore, government and non-governmental organization (NGO) initiatives to improve global health access, often prioritizing mobile diagnostic equipment, act as significant tailwinds, particularly in developing nations where infrastructure development is constrained.

Restraints include the necessity for standardized professional training and certification for using POCUS devices, as improper technique or misinterpretation can lead to diagnostic errors, posing patient safety risks and hindering widespread acceptance by traditional radiology departments. Cybersecurity concerns surrounding patient data transmission and storage on cloud-linked platforms remain a significant challenge, requiring robust compliance measures and continuous technological updates. Opportunities are strongly linked to the development of highly specialized application-specific transducers (e.g., specialized probes for dermatology or rheumatology) and the creation of highly intuitive, AI-driven software interfaces that minimize user dependency on extensive prior ultrasound knowledge. The integration with electronic health records (EHRs) and seamless billing systems presents a crucial area for future optimization, enhancing the device's value proposition within integrated healthcare networks and ensuring long-term profitability.

The Handheld Ultrasound Device System Market is structurally segmented based on crucial attributes including Product Type, Application, and End-User, reflecting the diverse utility and deployment scenarios of this technology. Analyzing these segments provides strategic insights into areas of highest growth potential and technological focus. Product Type segmentation differentiates between wired devices, which offer robust connectivity but limited mobility, and wireless devices, which utilize Wi-Fi or Bluetooth for imaging transmission, offering superior portability and ease of integration with existing smart infrastructure, dominating current market innovation. The application landscape is fragmented across major medical specialties, demonstrating the versatility of POCUS, while end-user classification highlights the shift from centralized hospital usage towards distributed diagnostics in ambulatory settings and physician offices.

The distinction between different segments is increasingly becoming blurred due to technological convergence; for instance, many new wired devices still offer advanced networking capabilities, and wireless devices are achieving near-parity in image quality with high-end wired portable systems. However, the wireless segment holds significant appeal due to its potential for integration into global health initiatives and tele-ultrasound models, supporting rapid deployment in remote locations without requiring complex physical infrastructure. Furthermore, niche applications, such as veterinary use and specialized military field applications, although smaller, represent high-value growth pockets driven by requirements for extreme durability and specific diagnostic parameters.

The segmentation strategy is critical for manufacturers to tailor their product offerings and marketing efforts. For instance, focusing on the Hospital and Critical Care End-User segment necessitates high-performance transducers and robust regulatory compliance, whereas targeting Physician Offices requires a focus on affordability, ease of use, and compatibility with standard clinic workflow software. The sustained growth across all segments is underpinned by the essential value proposition of handheld ultrasound: delivering fast, actionable diagnostic information at minimal cost and maximum convenience, making it an indispensable tool for future healthcare provisioning globally.

The value chain for the Handheld Ultrasound Device System Market is primarily structured around specialized technological expertise, starting with the complex upstream activities related to component manufacturing. Upstream analysis focuses heavily on the production of miniaturized high-performance piezoelectric materials, sophisticated custom semiconductor chips for image processing, and high-density, energy-efficient batteries that are critical for portability. Key players in this phase include specialized sensor companies and chip manufacturers, whose innovations in reducing size while maintaining power efficiency directly determine the final product's performance and cost structure. Strategic sourcing and long-term supply agreements with these specialized component providers are crucial for maintaining manufacturing throughput and securing a competitive advantage in a rapidly evolving hardware environment.

Midstream activities involve the Original Equipment Manufacturers (OEMs) who design, assemble, integrate the software, and secure regulatory approvals for the finished handheld devices. This phase includes the integration of advanced software platforms, including AI algorithms and cloud connectivity features, transforming raw hardware into a clinically functional tool. Downstream analysis focuses on the distribution and sales network, characterized by a dual approach: direct sales teams targeting large hospital systems for higher control over customer relationships and pricing, and indirect channels relying on specialized medical equipment distributors and value-added resellers (VARs). VARs often provide local training, maintenance, and integration services, which are critical for gaining traction in fragmented markets or regions with lower POCUS proficiency.

The distribution channel is increasingly leveraging digital platforms, offering devices directly to consumers (physicians) through e-commerce and app stores, especially for software-focused wireless products. This direct and indirect channel synergy ensures broad market reach. Direct sales are vital for securing large contracts and institutional adoption, ensuring tight control over branding and service delivery. Conversely, indirect distribution, particularly through global distributors specializing in diagnostic equipment, provides essential regional penetration and localized support. The overall efficiency of the value chain is increasingly reliant on seamless supply chain management and rapid iteration cycles driven by software updates, ensuring that devices remain technologically current and compliant with evolving clinical requirements and cybersecurity standards post-sale.

The potential customer base for the Handheld Ultrasound Device System Market is highly diversified, reflecting the versatility of POCUS across the medical spectrum. The primary end-users, or buyers of the product, encompass a broad range of healthcare professionals and institutions, moving far beyond the traditional radiology department. This shift is characterized by adoption across non-specialist clinicians who require immediate, actionable diagnostic information, positioning primary care physicians, critical care specialists, and emergency medical technicians (EMTs) as key purchasing groups. The growing realization that POCUS improves the accuracy and timeliness of initial diagnoses makes these portable devices highly desirable for any setting where diagnostic ambiguity or access to centralized imaging services presents a bottleneck in patient care progression, solidifying the market's robust customer base expansion.

Hospitals and large integrated delivery networks (IDNs) represent major customers, purchasing systems in bulk for deployment across emergency rooms, intensive care units (ICUs), and anesthesia departments for procedural guidance and rapid diagnosis. Outside institutional settings, the fastest-growing customer segments include independent physician practices, ambulatory surgery centers (ASCs), and specialized clinics (e.g., pain management, sports medicine) who leverage the devices to integrate diagnostics directly into consultation rooms, improving patient throughput and generating new revenue streams. Furthermore, global health organizations and governmental bodies procuring equipment for deployment in remote or underserved areas constitute significant volume purchasers, prioritizing ruggedness, connectivity, and ease of use in their selection criteria for these highly portable systems.

The future potential customer also includes non-traditional medical professionals, such as highly trained nurses and physical therapists, especially as AI simplifies image acquisition and interpretation, further broadening the market applicability. Educational institutions are also emerging as key customers, purchasing systems for inclusion in medical and physician assistant training programs to ensure the next generation of clinicians is proficient in POCUS techniques. The core characteristic sought by all potential customers is the system's ability to provide high-quality imaging, seamless data integration with existing electronic health records (EHRs), and dependable technical support, ensuring long-term utility and minimal workflow disruption in diverse clinical settings.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Philips Healthcare, General Electric Healthcare, Siemens Healthineers, FUJIFILM SonoSite, Butterfly Network, Inc., Konica Minolta, Inc., Canon Medical Systems Corporation, Mindray Medical International Limited, Samsung Medison, Clarius Mobile Health, Echonous, Healcerion, Vave Health, Sonoscanner, Telemed. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Handheld Ultrasound Device System Market is defined by relentless innovation aimed at balancing portability, cost, and diagnostic performance. A cornerstone of this evolution is the development of micro-electromechanical systems (MEMS) and application-specific integrated circuits (ASICs), which have allowed for radical miniaturization of the transducer array and associated beamforming electronics, dramatically reducing the size of the probe while maintaining high fidelity. Crucially, proprietary algorithms for advanced signal processing are used to compensate for the inherent lower power of handheld units, ensuring that the resulting images possess the contrast and resolution necessary for accurate clinical assessment. Battery technology, specifically the use of high-density lithium-ion chemistries, has also been pivotal, enabling multi-hour continuous operation without external power, thereby supporting extensive use in mobile and remote settings across varied environmental conditions and demanding operational schedules.

Another dominant technological force is the shift towards app-based platforms and cloud computing architecture. Modern handheld systems function as sophisticated peripheral devices connected to smartphones or tablets running specialized applications that handle complex rendering, user interface management, and data storage. This reliance on readily available consumer hardware significantly reduces the manufacturing cost and allows for rapid, over-the-air software updates, ensuring that users always have access to the latest diagnostic features and security patches. Furthermore, cloud connectivity facilitates secure and compliant image archival, enables real-time collaboration among clinicians (tele-ultrasound), and provides the necessary computational backbone for running intensive artificial intelligence and machine learning models for automated analysis and quality control, thereby enhancing diagnostic confidence and streamlining workflow integration into electronic health records.

The most transformative technology permeating this market is the integration of high-performance Artificial Intelligence (AI) at both the edge (device level) and in the cloud. Edge AI processing handles tasks such as real-time image stabilization, immediate artifact suppression, and automated measurement calculations directly on the device, minimizing latency for critical applications. Cloud-based AI systems focus on comprehensive analytical tools, offering diagnostic suggestions, performing comparative analysis against large databases of pathological scans, and quality auditing of scans performed by less experienced operators. The development of single-crystal transducers and matrix array technology is also driving performance gains, offering broader frequency ranges and deeper penetration capabilities, pushing the diagnostic utility of handheld devices closer to that of premium cart-based systems across critical applications like transesophageal echocardiography or deep abdominal imaging, thereby expanding the potential clinical utility horizon significantly.

The global Handheld Ultrasound Device System Market exhibits distinct regional adoption patterns and growth drivers, heavily influenced by local healthcare infrastructure, regulatory environments, and economic capacity. North America currently holds the largest market share, driven primarily by the sophisticated healthcare infrastructure, high awareness and acceptance of POCUS among specialists (especially emergency physicians and cardiologists), favorable reimbursement policies for bedside procedures, and the presence of leading technological innovators and competitive market players. The region's emphasis on high-throughput diagnostics, coupled with significant investment in integrating AI and connectivity solutions into clinical workflow, ensures sustained leadership in terms of both market value and technological adoption rate, setting global benchmarks for portable imaging utilization.

Europe represents a mature but dynamic market, characterized by centralized healthcare systems increasingly utilizing handheld ultrasound to optimize primary care diagnostics and reduce hospital wait times. Scandinavian countries and the UK have been early adopters of POCUS in general practice and ambulance services, focusing on cost-efficiency and preventative care strategies. Regulatory harmonization through the European Union simplifies market access for manufacturers, but pricing pressures from governmental health systems often drive demand towards robust, mid-priced devices offering high reliability and extensive clinical flexibility. The region is seeing strong growth in specialized segments such as MSK and rheumatology, reflecting an aging population requiring frequent, localized diagnostic assessments.

Asia Pacific (APAC) is projected to be the fastest-growing region throughout the forecast period. This explosive growth is underpinned by two primary factors: massive populations in countries like China and India requiring accessible healthcare solutions, and significant governmental investment aimed at modernizing healthcare infrastructure, particularly in rural and semi-urban areas where large console systems are impractical. Affordability and durability are crucial market requirements in APAC, driving the adoption of wireless, app-based systems. Japan and South Korea, with their advanced technological ecosystems, are spearheading the integration of advanced AI and high-end handheld devices, focusing on superior image quality and sophisticated diagnostic applications, while Southeast Asian nations prioritize foundational diagnostic capability and large-scale public health deployment programs to combat prevalent endemic diseases.

Latin America and the Middle East and Africa (MEA) are emerging markets offering substantial long-term opportunities. In Latin America, urbanization and expanding private healthcare sectors are accelerating the adoption of handheld ultrasound, particularly in Brazil and Mexico, focusing on optimizing services in newly established ambulatory clinics and reducing the strain on overwhelmed public hospitals. The MEA region’s growth is fueled by increasing foreign investment in healthcare, governmental initiatives to improve primary care access, and the necessity for mobile diagnostic units to serve geographically dispersed populations. Challenges in MEA include infrastructure deficits and lower healthcare expenditure per capita, meaning the focus remains on ultra-affordable, highly rugged devices capable of operating effectively in challenging field environments, often procured through humanitarian or public sector contracts leveraging global aid organizations.

The primary driver is the accelerating clinical and economic demand for Point-of-Care Ultrasound (POCUS) diagnostics, which necessitates highly portable, affordable, and immediate imaging capabilities outside traditional radiology settings, improving workflow efficiency and patient outcomes substantially.

AI integration is profoundly influential, enhancing device performance by providing real-time image optimization, automating complex measurements, guiding users for optimal probe positioning, and offering preliminary diagnostic support, thereby democratizing the technology and expanding its effective utilization by non-expert clinicians globally.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR), driven by significant unmet diagnostic needs, expanding governmental investments in affordable healthcare infrastructure, and rapid adoption of mobile health technologies in populous nations such as China and India, making accessibility crucial.

Wired devices typically offer more robust data connection and potentially higher power for deep penetration but restrict mobility. Wireless devices, favored by the market, offer superior portability, seamless integration with smart devices via Bluetooth/Wi-Fi, and ease of use, making them ideal for rapid bedside assessments and remote applications.

Primary restraints include the mandatory requirement for comprehensive professional training and standardized certification to mitigate misdiagnosis risk, persistent challenges related to cybersecurity protocols for transmitted patient data, and navigating complex, varying international regulatory approval processes for new diagnostic platforms.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.